MNI CHINA MONEY MARKET INDEX: PBOC Seen Restarting PSL

The People’s Bank of China looks set to restart Pledged Supplementary Lending to boost investment as economic headwinds rise in the second half of the year, but it will keep its key policy rate unchanged, according to the latest MNI China Money Market Index survey.

MNI’s July survey saw just over half of respondents seeing the PBOC as “very likely”to resume the PLS -- a tool through which the central bank provides long-term, low-cost funding to policy banks for support areas such as infrastructure.

The central bank’s cut to the PSL rate in May to 2% from 2.25% was a significant policy signal, indicating that PSL is likely to be restarted and have a large leveraging effect in terms of funding, one Jiangsu trader said, with a Tianjin-based trader saying the additional funds for policy banks would prevent financial stability risks while the real estate sector maintains sluggish and external pressure remain uncertain. (See MNI: China's GDP Faces H2 Growth Challenges)

ACCOMODATIVE

Traders believe the PBOC would keep an accommodative stance on liquidity provision, with the outlook sub-index for the coming month falling to 46.8 from 47.8 in June, with 81% of respondents seeing a continued easing stance.

The sub-index for the PBOC’s OMO outlook over the coming month slipped to 47.9 from June’s 52.2, with more than half of traders predicting the PBOC would maintain its easing bias. Moreover, the sub-index for policy outlook over next six months fell to 12.8 from 13.0 as further easing was predicted by three-quarters of respondents.

The sub-index covering the PBOC’s current OMOs provision rose to 47.9 from last month’s 48.9, with 95.7% of traders assessing OMOs as being “in line with” market demand.

One trader based in Anhui predicted the PBOC would resume government bond trading in H2 and ensure enough liquidity to support fiscal expansion and help the economy.

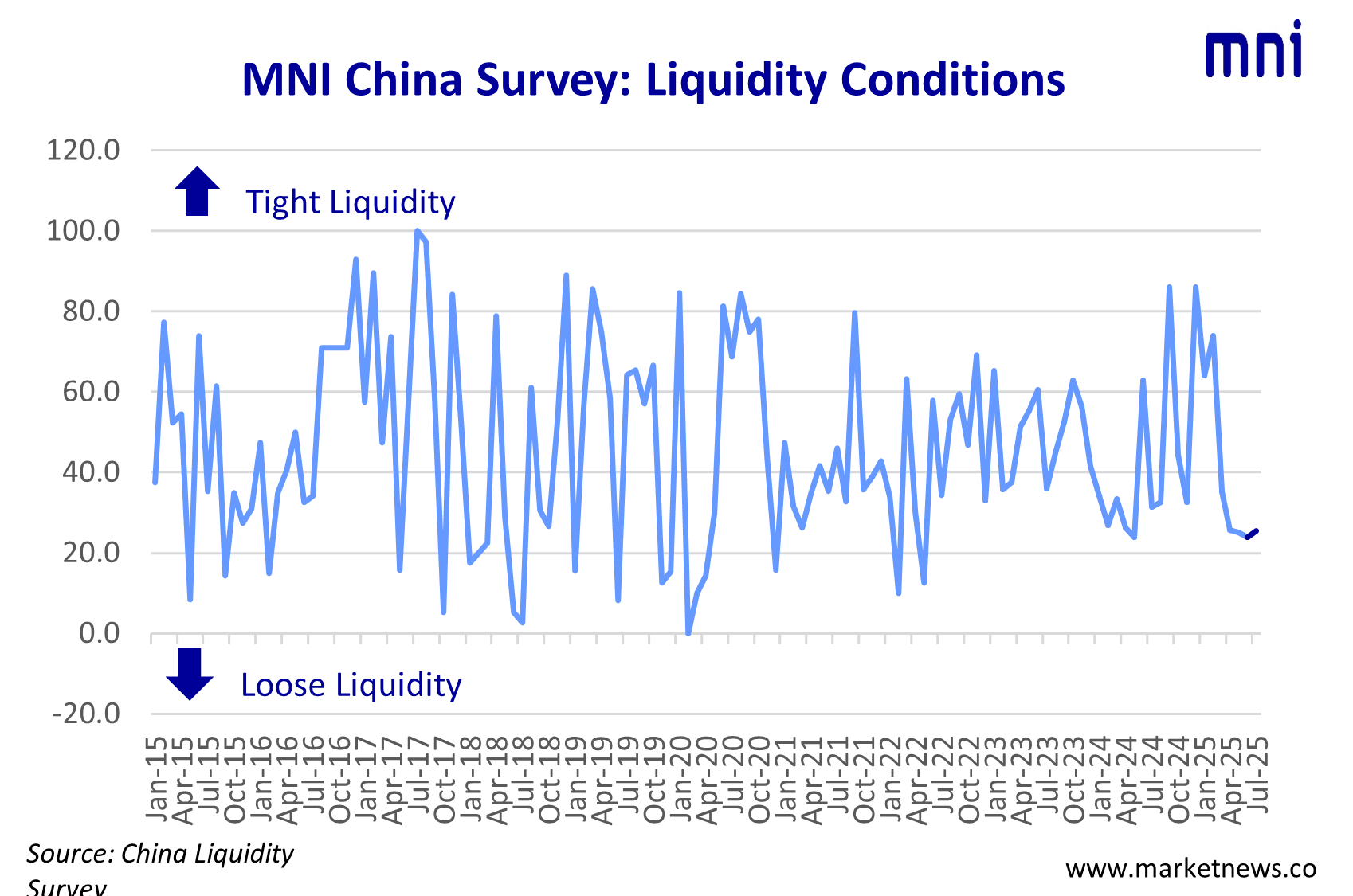

The sub-index covering current liquidity conditions was 25.5, up from 23.9. The lower the index shows, the easier the liquidity condition performs.

LIQUIDITY LEVELS

The liquidity situation in the interbank market has remained stable since the PBOC injected a net of CNY200 billion via outright reverse repo and a net of CNY100 billion through medium-term lending facility in July, the Jiangsu trader said.

Many traders see the chance for policy rate reduction as low. The PBOC’s 7-day repo rate outlook sub-index edge up to 58.5 from 56.5, with 83% of participants expecting the PBOC to hold its policy rate stable in the coming month. As a result, some 78.7% thought the key rate (DR007) will hold at current levels through next month, with the DR007 outlook sub-index dropping to 50.0 from 54.3. (See MNI PBOC WATCH: LPR, RRR Cuts Seen Later In 2025; Held For Now)

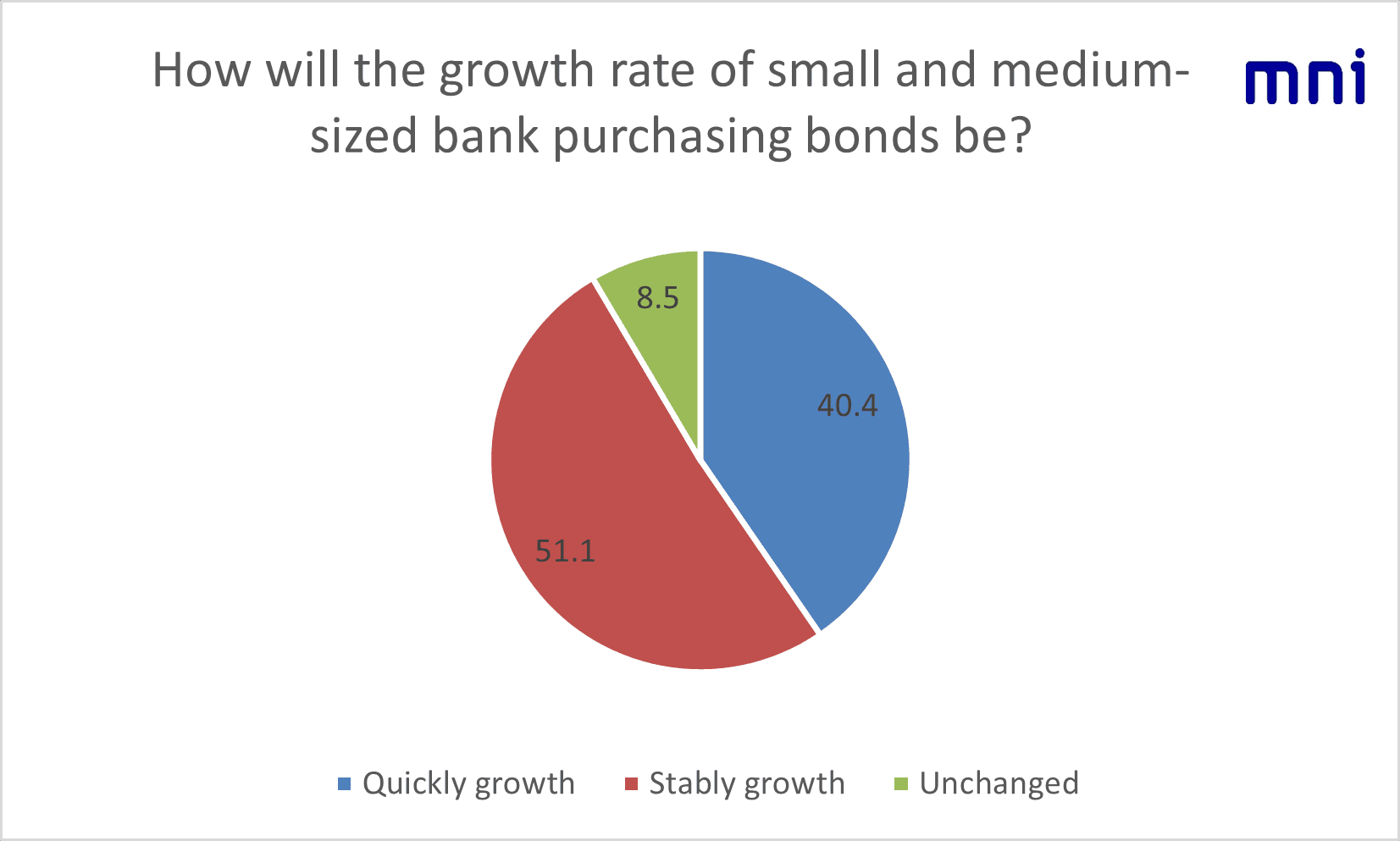

The other special questions this month showed 51.1% of participants thinking smaller banks’ bond buying would see “stable growth” while 40.4% saw “quick growth”.

With the increasing difficulty of expanding lending, smaller banks have to allocate fixed assets to maintain returns and improve liquidity, a Henan traders noted. A Shanghai trader said increasing bond purchase has become inevitable in a complex operating environment marked by deposit competition and interest rate reductions, warning any aggressive bond buying could trigger liquidity strains and raise default risk considering the limited funding sources at small and medium-sized banks.

The MNI China Money Market Index (MMI) survey was conducted from July 14 to July 25, with the participation of 47 traders from both state-owned and joint-venture banks.