MNI CHINA MONEY MARKET INDEX: PBOC Easing Expectations Fall

Chinese interbank traders see a lower chance of further monetary easing in the rest of 2025 than they did in July as economic growth continues to be solid, and expect more upwards pressure on bond yields as funds are lured into a rising stock market, MNI’s China Money Market Index for August indicated.

The PBOC’s seven-day repo rate sub-index fell to 54.3, the lowest this year, with 91.5% of participants expecting the PBOC would hold its policy rate stable in the coming month, and only 8.5% of traders seeing a cut, the lowest proportion so far this year.

First half GDP growth of 5.3% y/y has reduced the need for more counter-cyclical policy moves, said a trader from Jiangsu Province, while a Hebei trader predicted the authorities would guide market expectations by stressing their commitment to flexibly respond to economic developments. (See MNI: PBOC To Make Slight Cuts In Q4, A-Share Rally Welcomed)

The monetary policy outlook sub-index was 14, with 70.2% of traders saying policy would loosen in six months, falling from 74.5% in July. Some 51.1% of participants thought the policy bias will become easier, the lowest this year, while the current policy bias sub-index was 24.5, this year’s highest, with higher readings indicating a tighter expected policy stance.

Some 14.9% of traders thought the seven-day reverse repo for deposit-taking institutions rate (DR007) would rise next month due to quarter-end cash demand, the highest this year, although 74.5% of participants bet on fluctuations around the current level, with the DR007 outlook sub-index dropping to 47.9, the lowest in 2025. DR007 is benchmarked by the PBOC’s key seven-day repo rate.

The coming month liquidity outlook sub-index edged up to 48.9 from 46.8, below the 50 threshold, indicating comfortable liquidity conditions, with 80.9% of participants expecting a continuation of the current easing stance.

STOCK MARKET

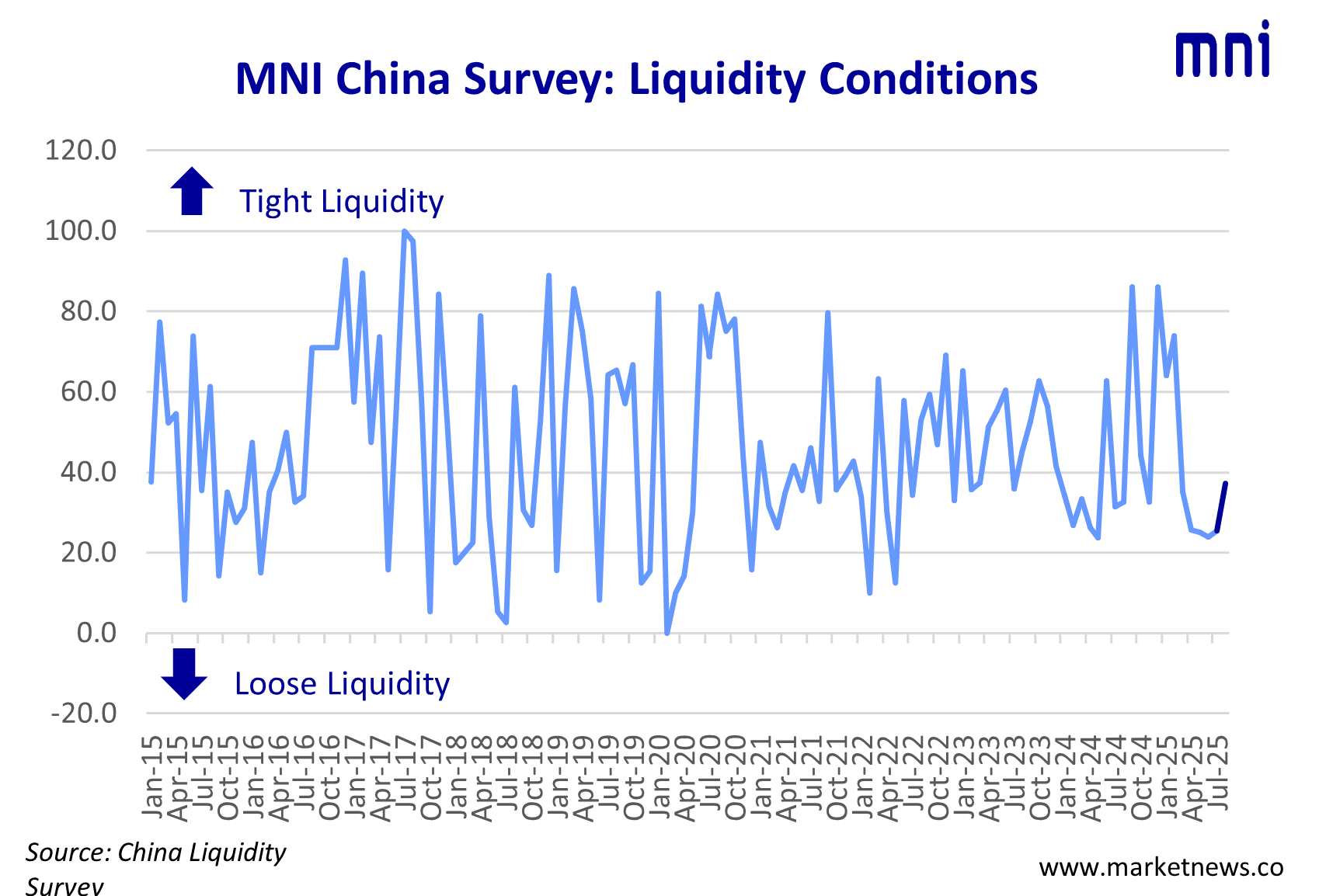

Tax payments and a rising stock market meant interbank liquidity fluctuated this month, and the current liquidity conditions sub-index was 37.2, the highest in six months, with 10.6% of participants seeing tight liquidity and none reporting tightness last month. The lower the sub-index, the easier liquidity conditions.

Rising stock and commodity prices have diverted funds from bonds into higher-risk assets, a Shanghai trader noted.

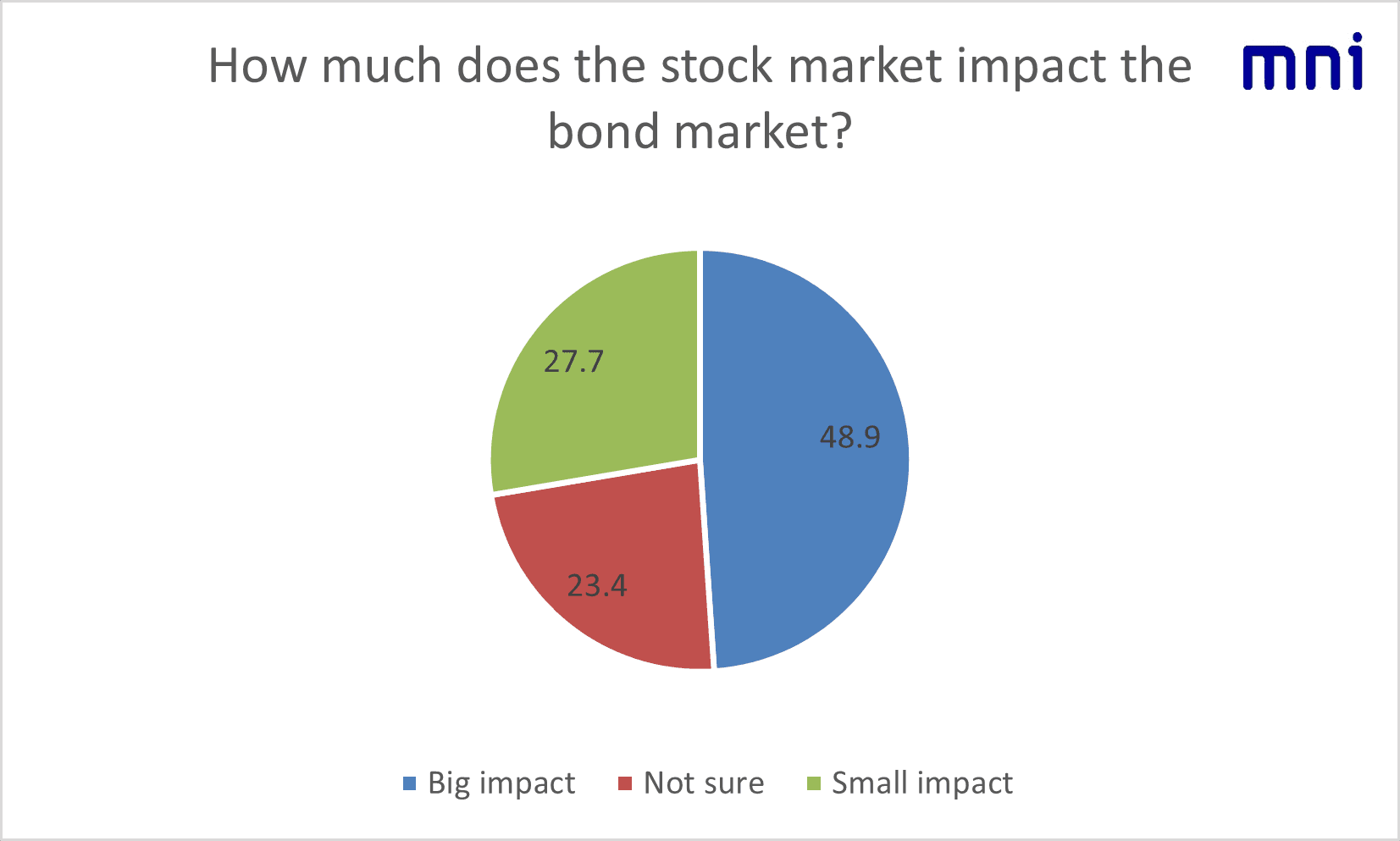

One of MNI’s special questions this month showed 77% of participants expected the bullish stock market to pressure bonds. A Shanxi trader called rising stocks a major contributor to recent falls in bond prices, while a Jiangsu trader warned that bond market volatility would be amplified, with medium and long-term yields rising in the short term.

AMPLE LIQUIDITY

Another special question was about the liquidity outlook. Even though the PBOC has reiterated its intention of preventing “idle funds” from circulating inside the financial system, 63.8% of traders responded that the stance of “maintaining ample liquidity” would not be changed. (See MNI PBOC WATCH: Ample Liquidity Ensured Amid Bull Stock Market)

The sub-index for the PBOC’s OMOs over the coming month edged down to 46.8 from 47.9, with 59.6% of traders predicting unchanged levels. The current OMO provision sub-index fell to 45.7 from 47.9 , with 91.5% of traders assessing OMOs as being “in line with” demand.

The PBOC has demonstrated an active stance in liquidity injection, an Anhui trader said, pointing to the Bank’s announcement of an outright reverse repo operation early this month as the country restarted VAT collection on government bond issuance.

The PBOC outright reverse repo sub-index showed 51.1% of traders expect the Bank to maintain the current level of operations in the coming month, with the index at 31.9, rising from last month’s 27.7.

The MNI China Money Market Index (MMI) survey was conducted from Aug 11 to Aug 22, with the participation of 47 traders from both state-owned and joint-venture banks.