MNI CHINA MONEY MARKET INDEX: PBOC Bond Buys Seen Resuming

Chinese interbank traders mainly expect the People’s Bank of China to resume government bond purchases in Q3 to support fiscal expansion, according to MNI’s China Money Market Index, which also showed that the interbank liquidity injections increased to offset mid-year fund demand.

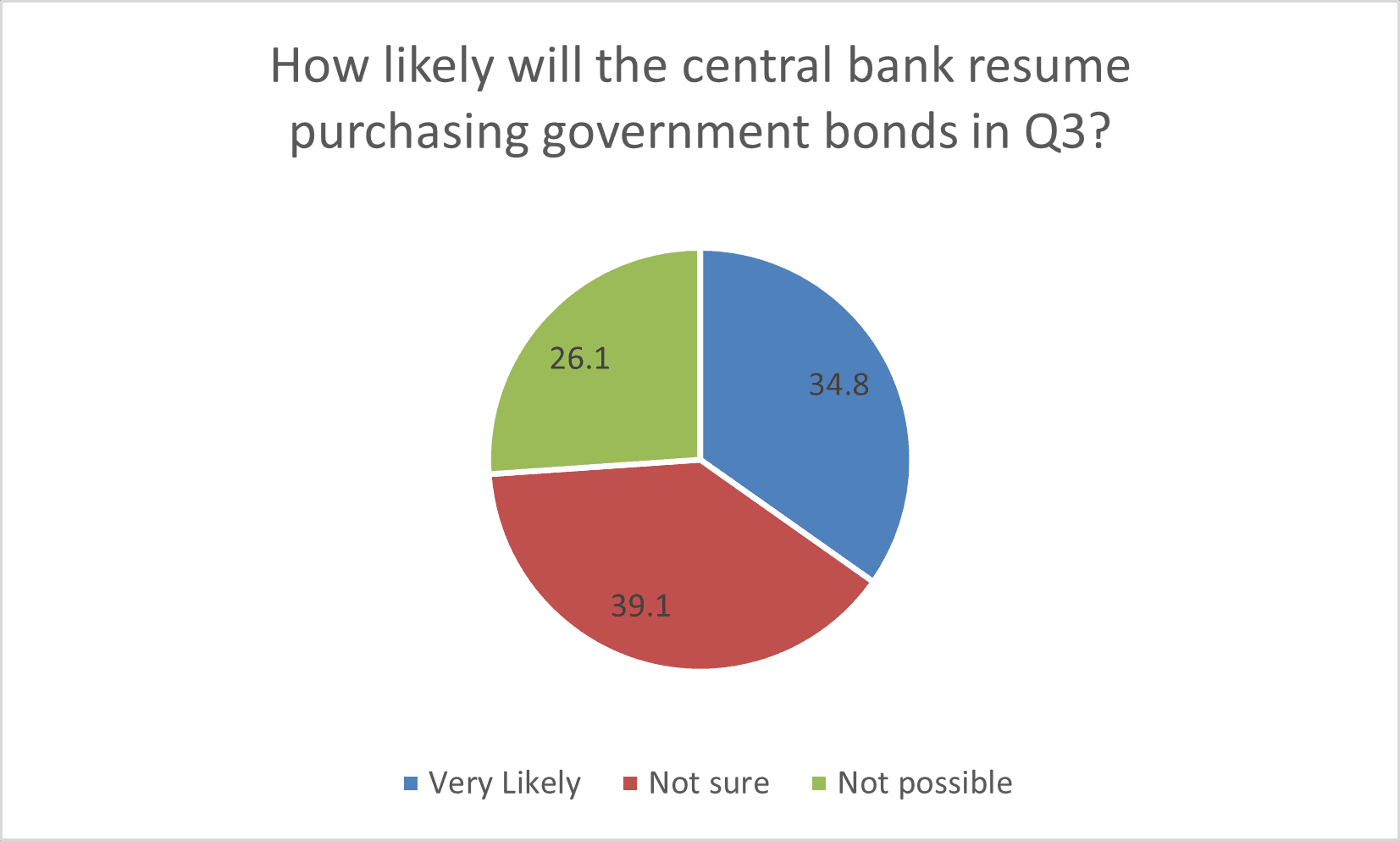

MNI’s special question this month showed 34.8% of participants expected the PBOC would “very likely” resume bond buying in Q3, while 26.1% thought it was “not possible”

PBOC purchases in July or August would coincide with sustained heavy government bond issuance and would ease upwards pressure on yields, a Jiangsu trader said. A Shandong trader said that a recent bond-buying spree by big banks was likely made in preparation for the return to market by the PBOC, which usually buys from large lenders.(See MNI: PBOC Seen Resuming Bond Purchases As Gov't Issuance Rises)

Resuming treasury purchases would ease pressure on banks’ bond underwriting and inject base money as short-term debt held by the PBOC matures, a Shanghai trader said, noting major banks primarily bought one to three-year bonds.

However, an Anhui trader disagreed, saying that restarting treasury operations would depend on macroeconomic conditions, and that the PBOC is likely to rely more on liquidity tools as it continues to monitor the effects of its recent cuts to banks’ reserve requirements and its policy rate.

AMPLE LIQUIDITY

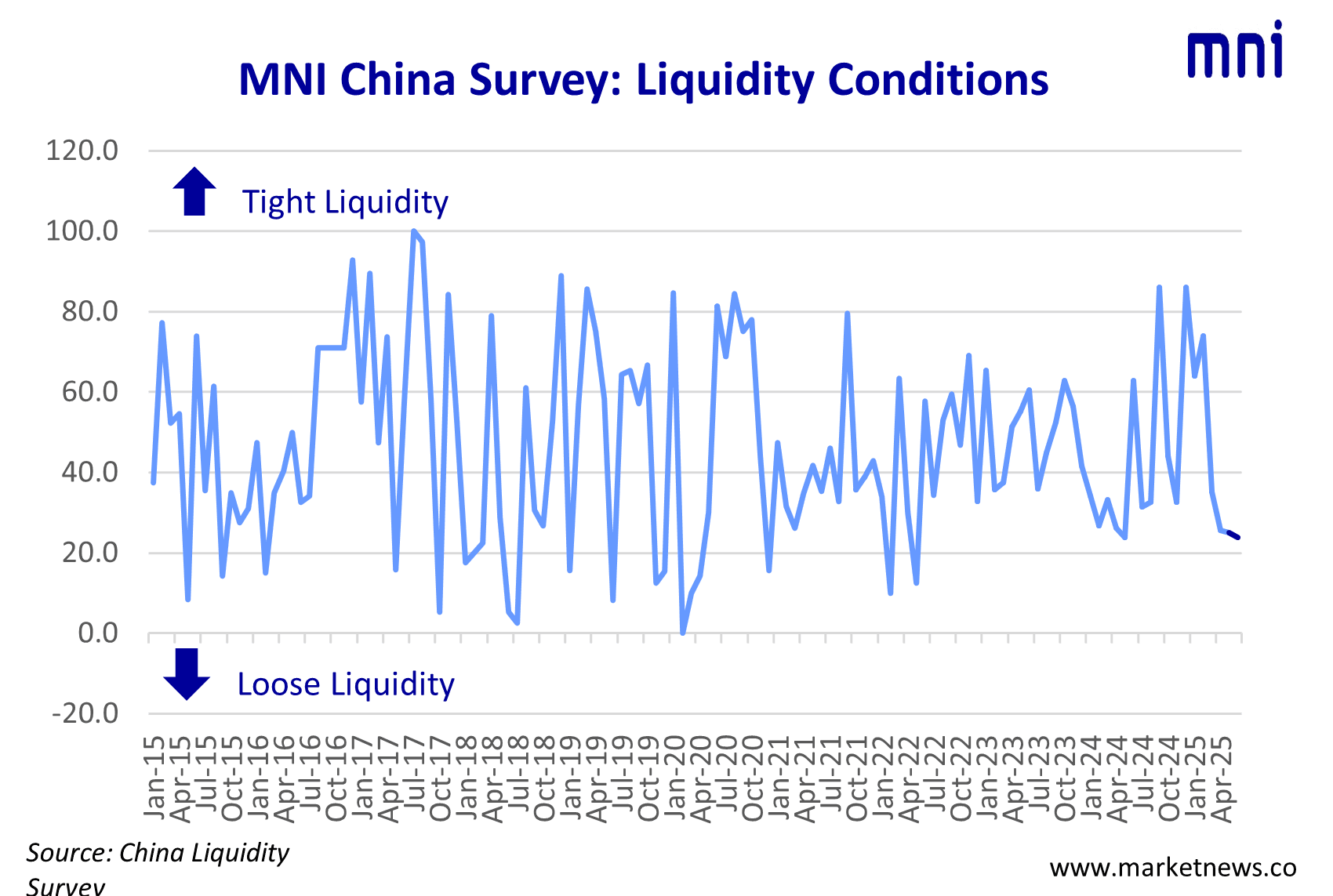

The current liquidity conditions sub-index printed at 23.9, the lowest this year, with 54.3% of participants seeing loosening liquidity. The lower the index, the easier conditions.

The Bank’s CNY1 trillion in three-month outright reverse repos and CNY400 billion in six-month repos plugged funding gaps in a timely manner, a Jilin trader said, while a trader in Shanxi said the PBOC's accommodative stance will provide a smooth quarter-end transition.

The participants believed the easing stance of the Bank had not changed, with the current policy bias sub-index stable this month at 15.2 from 13.0 last month (the lower it reads, the easier the expected policy stance), with no trader thinking the current policy bias was tightening.

However, traders do not see rate cuts as imminent. The PBOC 7-day repo rate outlook sub-index fell to 56.5, the lowest this year, with 87% of participants expecting the PBOC would hold its policy rate stable in the coming month. Some 78.3% thought DR007, which is benchmarked by the PBOC 7-day reverse repo rate, will also be stable next month, with the DR007 outlook sub-index dropping to 54.3 from 60.9. (See MNI: Tariffs, Weak Demand To Drive Moderate PBOC Easing In H2)

OPEN MARKET OPERATIONS

Another special question asked about expectations for outright reverse repo operations, with 41.3% of traders betting the Bank would increase these operations in the future. The coming month outright reverse repo sub-index fell to 31.5 from May’s 35.9.

A Henan trader said outright reverse repos would combine with reverse repos and the medium-term lending facility to help the Bank adjust the yield curve.

The PBOC OMO provision sub-index rose to 48.9, the highest in 10 months, with 97.8% of traders assessing OMOs as being “in line with” market demand.

The coming-month liquidity outlook sub-index fell to 47.8 from last month’s 51.1, below the 50 threshold, indicating comfortable liquidity conditions as 78.3% participants estimated continuity in the current easing stance.

The coming-month OMO sub-index edged up to 52.2 from 51.1, with 47.8% of traders predicting unchanged support. The six-month policy outlook sub-index fell to 13.0 from 16.3 as further easing was predicted by 73.9% of traders.

The MNI China Money Market Index (MMI) survey was conducted from June 6 to June 20, with participation of 46 traders from both state-owned and joint-venture banks.

Full press release is available

Hidden PDF