MNI CHINA MONEY MARKET INDEX: Liquidity Boost As Maturities Up

Chinese interbank traders expect the central bank to increase liquidity injections next month to cope with sizeable maturities, increased speculation of lower rates and concern tensions will resurface between China and the U.S despite a short-term truce, MNI’s China Money Market Index indicated.

The China liquidity outlook sub-index rose to 49.0 from last month’s 46.9, the highest since June, pointing to a possible liquidity shortage next month, with 10.2% of traders concerned about the maturity of policy tools, particularly CNY900 billion from the PBOC’s medium-term lending facility.

Most traders expect the People’s Bank of China to continue to provide liquidity support, taking the overall sub-index for the OMOs outlook to 49.0, with 26.5% of participants seeing more injections next month, the highest since June.

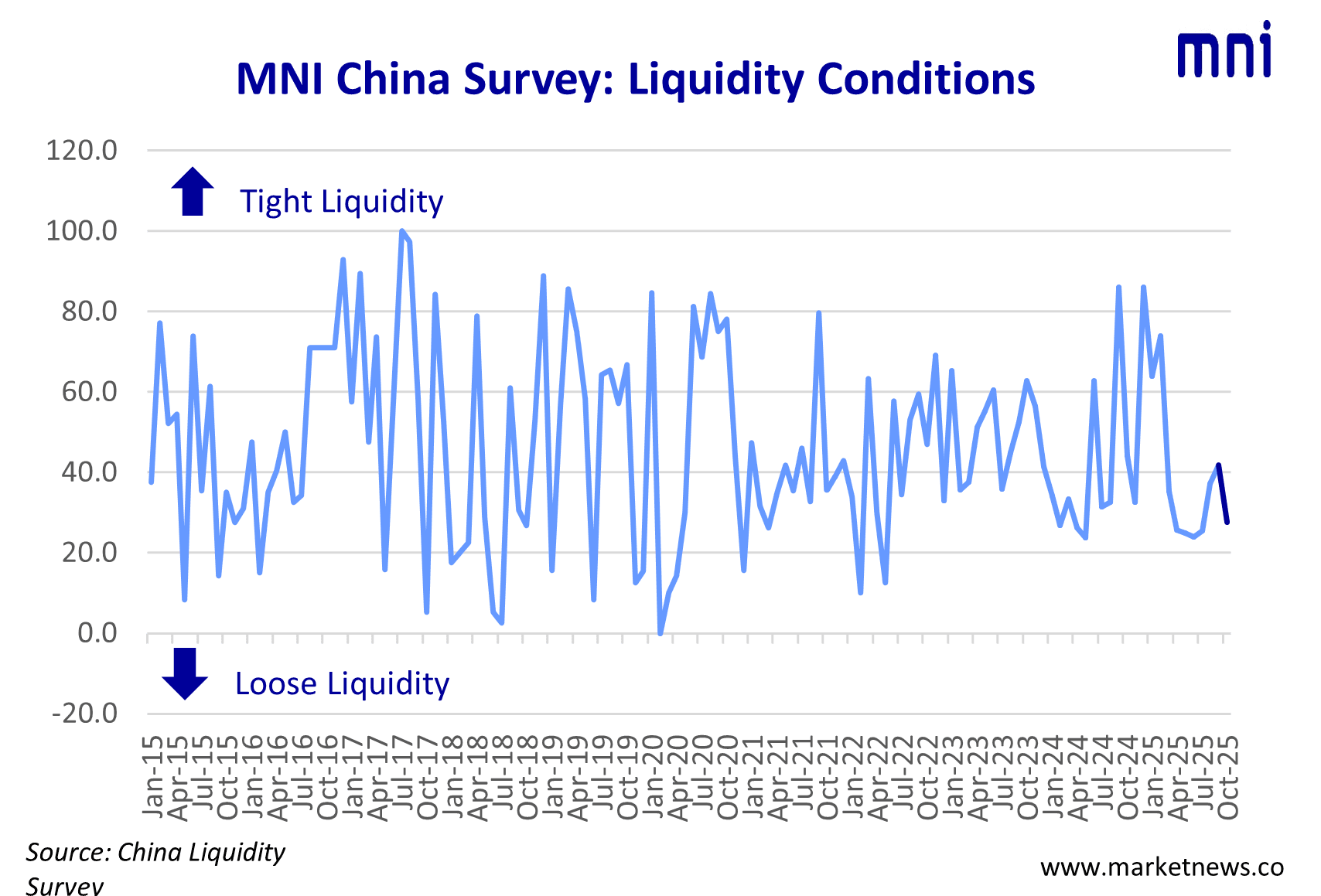

The sub-index covering current liquidity conditions fell to 27.6 from 41.8, the first fall in four months, indicating a benign environment, with 49.0% of participants seeing loosening.

“IN LINE WITH DEMAND”

The PBOC has continued to inject medium-term liquidity, with MLF operations increasing for the eighth consecutive month, noted a Nanjing trader. A Shandong trader said conditions eased after the National Day holiday, with overnight and seven-day funding rates falling, while light supply of government bonds also eased pressure.

The sub-index covering the PBOC’s current open market operations rose to 50 from 43.9, with all traders assessing OMOs as being “in line with demand”. (See MNI: Relaxed Policy To Drive PBOC Over Next Five Years - Advrs)

The PBOC’s seven-day reverse repo rate outlook sub-index rose to 60.2, the highest since April, with 20.4% of participants expecting a policy rate reduction in the coming month, the most in seven months, but 79.6% thinking the PBOC would hold. Some 67.3% thought the seven-day repo rate for deposit-taking institutions (DR007) would remain stable next month, with the sub-index rising to 54.1 from 52.0. DR007 is benchmarked by the PBOC’s key seven-day reverse repo.

MNI’s special question for October showed China-U.S trade tensions would continue to perturb markets. Some 34.7% of traders said recent accelerating trade tensions had a “big impact” on Chinese markets, while 57.1% said it was too early to tell.

Short-term risk aversion and medium-to-long-term conflicts have led to significant divergences across assets, said a Fujian trader. Bonds have benefited from safe-haven demand, the trader said, noting the 10-year government bond yield fell by three basis points to 1.74% during a moment of tension, but rebounded to 1.78% as stock markets recovered.

TRADE UNCERTAINTY

Long-term uncertainty is rising. A Beijing trader said that while the weekend’s China-U.S. talks in Kuala Lumpur signalled easing tensions, disagreements in key areas such as technology remain unresolved. This week’s APEC summit could be critical, with sentiment to improve if China and the U.S. can agree on extending the tariff suspension and restarting technology dialogues, a Henan trader said. (See MNI: More China-US Tensions Likely Despite Progress-Advisors)

Another special question indicated bond markets would remain volatile this quarter, mainly due to robust equities, looser liquidity, and a possible rate cut as well as soft economic recovery.

Yields should continue to rise, but decline as the central bank injects liquidity, a Shanghai trader said, with a Tianjin trader predicting the 10-year would fluctuate within a 1.7%-1.8% range from the current 1.8% in the rest of this quarter.

The PBOC’s restarting of treasury bond purchases and exceptions on a reserve requirement ratio cut this quarter should suppress yields, noted a Jiangsu trader. A Hebei trader argued weak recovery, tariff impacts on exports, persistent low inflation, and insufficient domestic demand would limit any upside in bond yields.

The PBOC bond trade outlook sub-index was 28.6, with 42.9% of traders expecting the central bank to increase holdings from last month’s 36.7%. Governor Pan Gongsheng said on Monday the Bank would resume bond trading.

Further easing over the next six months was predicted by 59.2% of traders, taking the policy outlook sub-index to 20.4, this year’s highest. The sub-index of policy bias edged up to 28.6 from 25.5, with 42.9% of participants foreseeing an easing stance.

The MNI China Money Market Index (MMI) survey was conducted from Oct 13 to Oct 24, with participation of 49 traders from both state-owned and joint-venture banks.

Fot the official MNI press release, see below:

Hidden PDF