MNI CHINA MONEY MARKET INDEX: Easing Bets Rise For Q2

repeats version sent at 0700 30/4/2025

Chinese interbank money market traders expect the central bank to provide additional monetary easing after pressures on exports from U.S. tariffs appear some time later in the second quarter, and to continue to support the financial system with liquidity, MNI’s China Money Market Index indicated on Wednesday.

The China liquidity outlook for the coming month sub-index remained stable at 45.6 from last month’s 45.5, below the 50 threshold, indicating accommodative liquidity conditions. A majority of participants anticipated no change to the monetary policy stance, though expectations are building for accelerated easing later this quarter. (See MNI PBOC WATCH: PBOC Seen Easing, Guiding LPR Lower, In Q2)

As trade tensions persist, stronger policy efforts will be required to consolidate Q1’s upward economic momentum, said a Hebei-based trader. A Zhejiang trader expected the People’s Bank of China to cut banks’ reserve requirements and policy interest rates this quarter.

The sub-index for the PBOC’s OMOs over the coming month outlook was 46.7, barely changed from 46.6, with 53.3% of traders predicting the same level of liquidity support. The sub-index for the policy outlook over the next six months rose to 14.4, the highest this year, with further easing predicted by 71.1% of traders.

But traders see a lower likelihood of an immediate cut to interest rates. The PBOC’s 7-day repo rate outlook sub-index fell to 60.0 from March’s 63.6, with 80% of participants expecting the PBOC would hold its policy rate stable in the coming month, compared with 72.7% last month. Some 71.1% thought DR007 would be stable next month, with the DR007 outlook sub-index dropping to 60.0 from 72.7. DR007 is benchmarked by the PBOC’s key 7-day repo rate.

Considering the uncertainties of the China-U.S trade conflict, it is prudent for authorities to adopting a wait-and-see approach, said a Fujian-based trader. A Beijing trader noted the probability of substantial monetary easing remains low before formal U.S.-China trade talks, but with recent increase in government bond issuance, the central bank may preemptively inject liquidity to smooth markets. (See:MNI: Low Credit Demand Feeds PBOC Easing Caution; Tariffs Key)

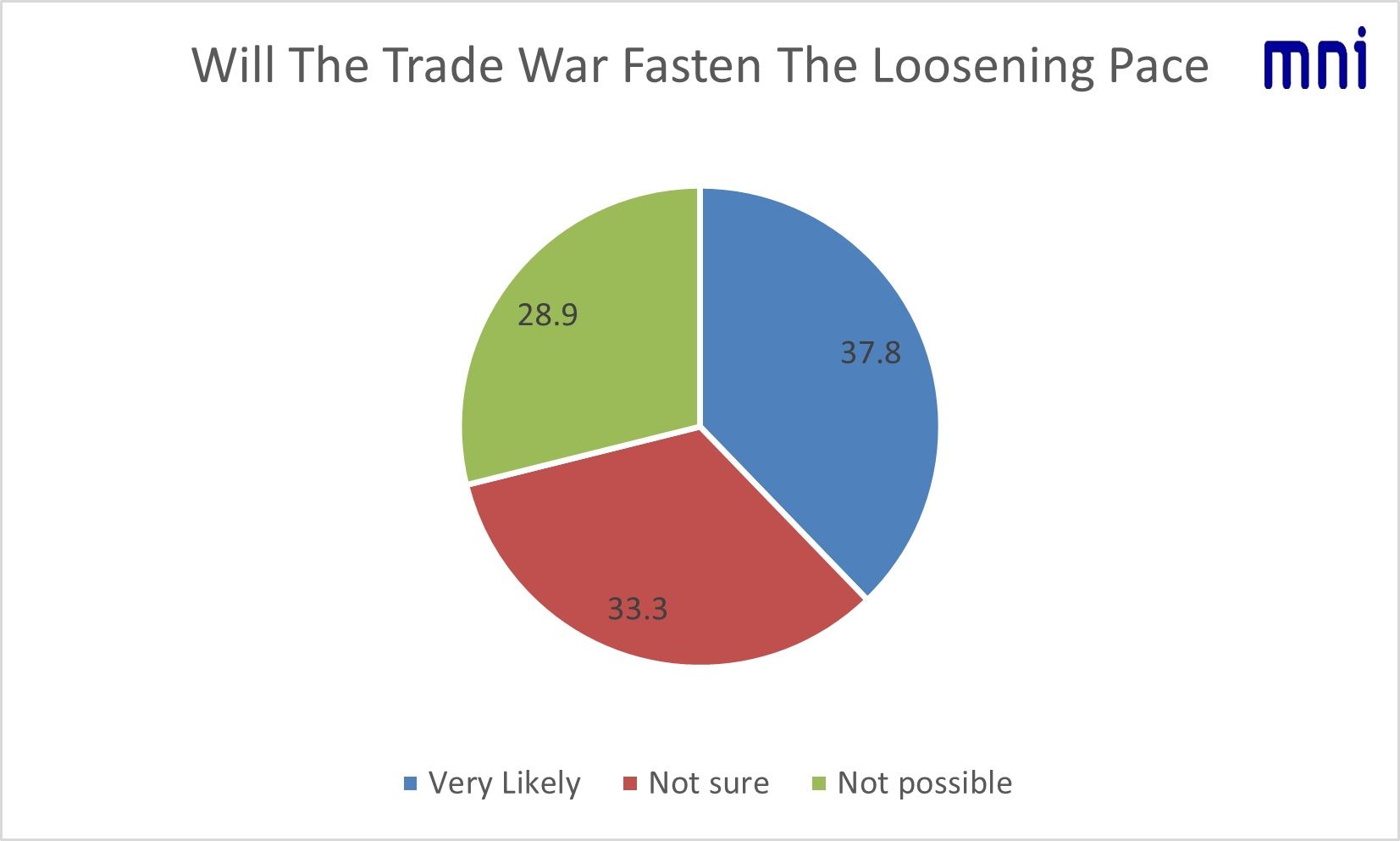

MNI’s special questions this month showed 53.3% of participants concerned that trade tensions would significantly impact the economy, while 37.8% of traders bet on further easing.

With domestic demand weak, the tariff shock to exports would exacerbate supply-demand imbalances and further suppress import demand, exerting significant downward pressure on activity in Q2, said a Zhejiang-based trader.

A Henan trader noted that the latest Politburo meeting had emphasised additional policy strengths, implying that fiscal authorities would expedite both new borrowing and the employment of funds already raised while the PBOC introduces new easing tools.

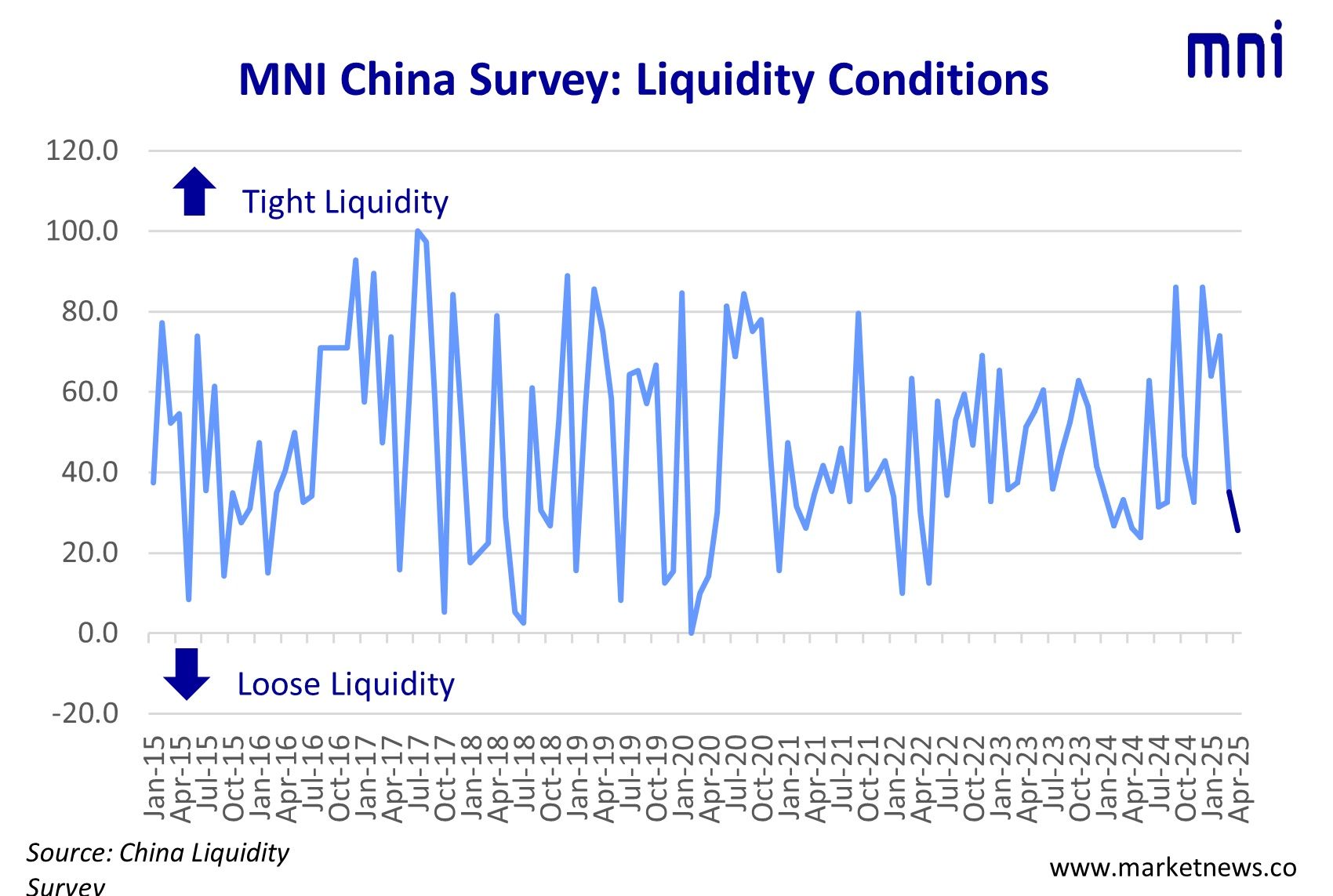

The sub-index covering current liquidity conditions fell to 25.6 from 35.2 last month, with 57.8% of participants seeing loosening liquidity. The situation was in line with MMI survey results in March predicting an easing stance for trade tensions.

The sub-index covering the PBOC’s current OMOs rose to 43.3 from 38.6, with 86.7% of traders assessing OMOs as being “in line with” market demand.

The central bank increased short-term liquidity injections to counterbalance funding strains caused by mid-month tax payments and increased bond financing, said a Shandong trader.

The participants assessed the PBOC’s easing stance as unchanged, with the sub-index of current policy bias remaining stable this month at 13.3 from March’s 10.2 (the lower it reads, the easier the expected policy stance). No trader thought the current policy bias was tightening.

The survey was conducted from April 14 to April 25, with participation of 45 traders from both state-owned and joint-venture banks.

This month's official press release is also available to read: