MNI BoC Review-Jan 2026: Uncertainty Remains The Watchword

Jan-28 16:45By: Tim Cooper

Canada

Hidden PDF

EXECUTIVE SUMMARY

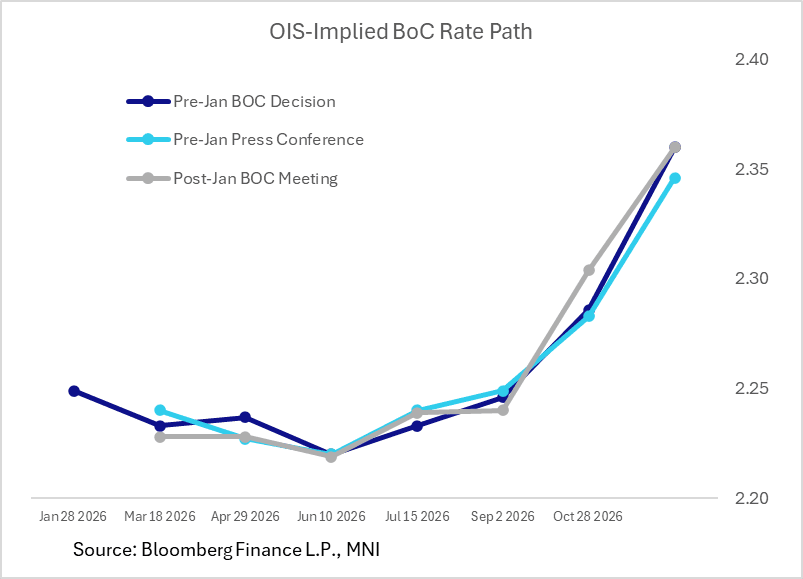

The Bank of Canada accompanied the unanimously-expected overnight rate hold at 2.25% at its January meeting with a largely unchanged appraisal of the economic and policy outlook. There was a very slight dovish tilt to the communications but not enough to sway market pricing of the expected policy path which continues to show no change in rates through 2026.

- While the BOC remains uncertain about the “timing or direction of the next change in the policy rate”, the opening statement highlighted the “unusually high” degree of uncertainty due in large part to upcoming North American free trade negotiation which the Bank’s forecasts assume will result in the status quo, at worst.

- And the updated Monetary Policy Report forecasts didn’t deviate from expectations that inflation will converge with the 2% target, while maintaining that there remains slack in the economy despite upgraded growth forecasts.

- Gov Macklem was asked in the press conference whether elevated uncertainty raises the bar for either cutting or hiking, and offered a little bit more colour on Governing Council's deliberations without revealing any particular lean, noting merely that CUSMA presented “obvious” risks to the outlook.

- Markets came out of the meeting expecting largely the same path of rates as seen coming into the day, with modest cuts implied through July (~5bp) but rates ultimately ending the year higher (~9bp) vs current levels.

- The next major data points to watch are November GDP on Friday, with January labour force data on Feb 6 and January CPI on Feb 16. The next rate decision will be on March 18.

- See PDF report for:

- MNI View

- MNI Instant Answers

- Press Conference Transcript

- BOC Meeting Links

- Policy Statement Changes

- Monetary Policy Report Updates