MNI BCB Preview - July 2025: Set for Extended Pause

Download Report Here

Executive Summary:

- Copom are expected to leave the Selic rate unchanged at 15.00% this week, after it signalled a pause in the tightening cycle

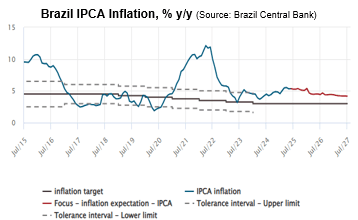

- Although inflation has begun to edge lower, it remains well above target, and the Board is still concerned about unanchored expectations

- With the labour market remaining tight, rate cuts are still unlikely to be discussed by the Board

After delivering a 25bp hike to 15.00% last month, a hawkish Copom signalled a pause in the hiking cycle but emphasised that monetary policy will remain in significantly contractionary territory for a very prolonged period. The decision to hike further came amid still unanchored inflation expectations, elevated inflation projections, resilient economic activity and ongoing labour market pressures. Although it didn’t rule out further rate hikes, the bar to further tightening appears to be high given the mounting global uncertainties, which warrant caution. Indeed, the committee clearly signalled that if the scenario materialises as expected, then the Selic rate would likely remain unchanged for some time while it assesses the cumulative impact of previous rate hikes.