MNI ASIA OPEN: Will JOLTS Job Rise Affect FOMC Decision

EXECUTIVE SUMMARY

- MNI FED: SEP/Dot Plot: Steady Course

- MNI FED: Inter-Meeting Communications: Even Divide Between Cutters And Holders

- MNI US OUTLOOK/OPINION: Macro Since Last FOMC - Labor: Stabilization Elsewhere

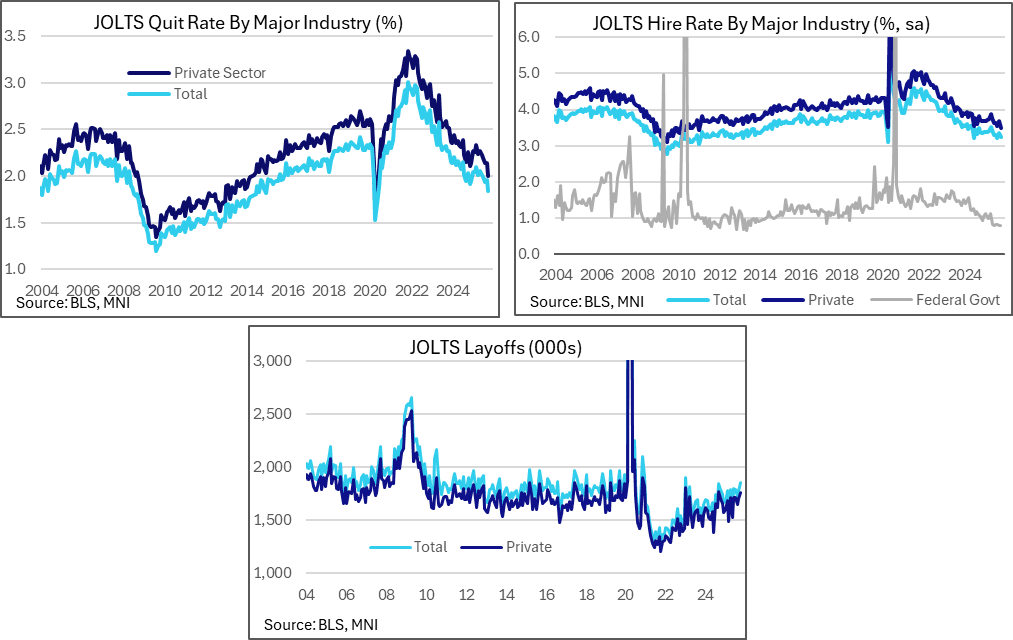

- MNI US DATA: … But Other JOLTS Indicators Read Clearly Softer

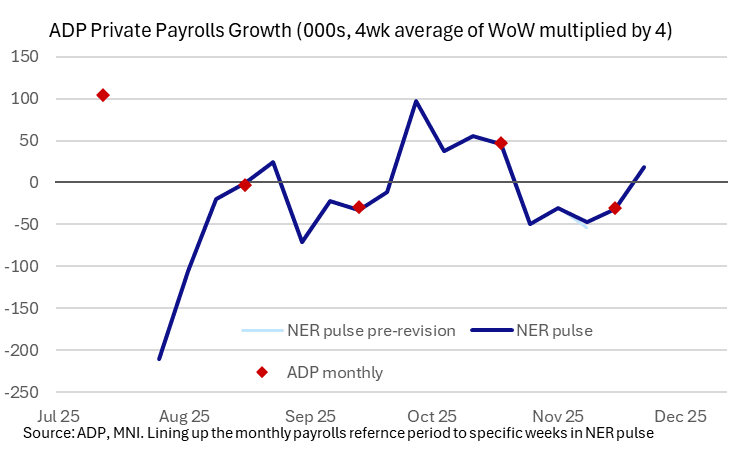

- MNI US DATA: Weekly ADP Improves In Late November

- MNI US DATA: Much Higher Than Expected JOLTS Job Openings…

US

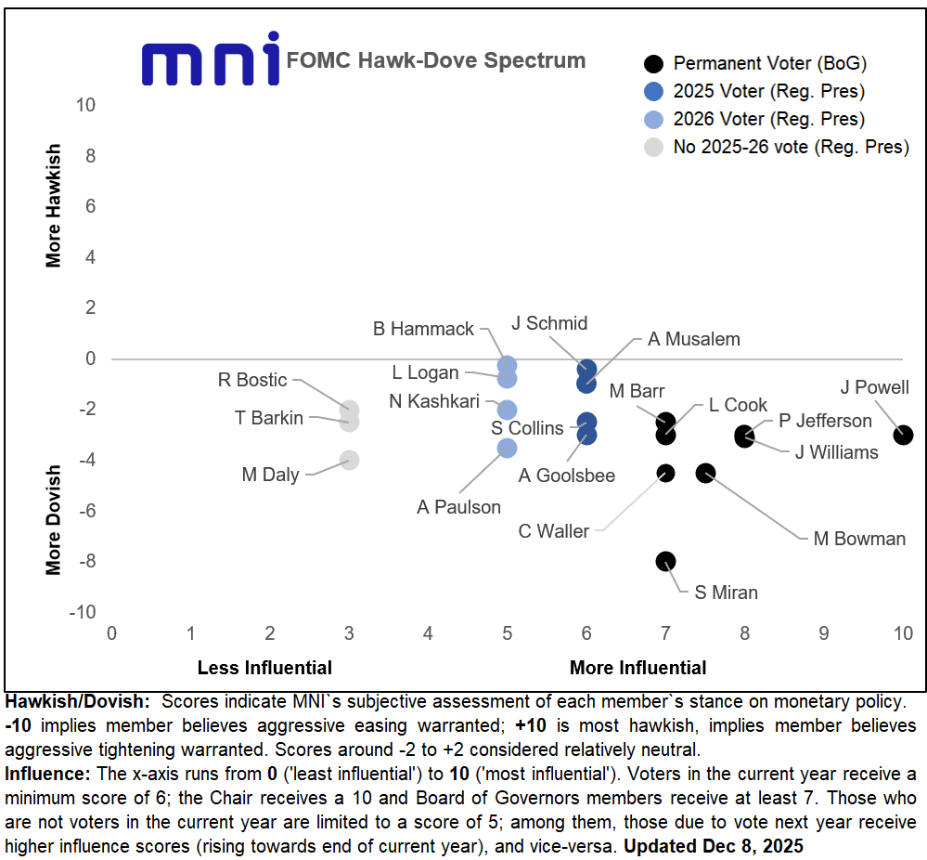

MNI FED: Inter-Meeting Communications: Even Divide Between Cutters And Holders

Inter-meeting communications reinforced that the FOMC is finely split between those who would ease further and those who are resistant - if not outright opposed - to providing further accommodation. Overall there were no members who became more dovish on the rate outlook since October, while there were signs that at least a few have become more hawkish. While we include the most relevant commentary by each member since the last meeting our preview, we summarize our assessment of the current state of play among the 19 FOMC participants as follows:

MNI US OUTLOOK/OPINION: Macro Since Last FOMC - Labor: Stabilization Elsewhere

Since the delayed September payrolls report, ADP employment has sent mixed signals – it surprisingly firmed in October after declining in September, returned to declining with a -32k drop in the main November report for a third monthly decline in the space of four months before some stabilization in latest weekly data.

- However, some unemployment rate trackers such as the Chicago Fed’s nowcast point to no further deterioration in the labor market ahead, with this nowcast tracking at the same 4.44% in November after 4.46% in October.

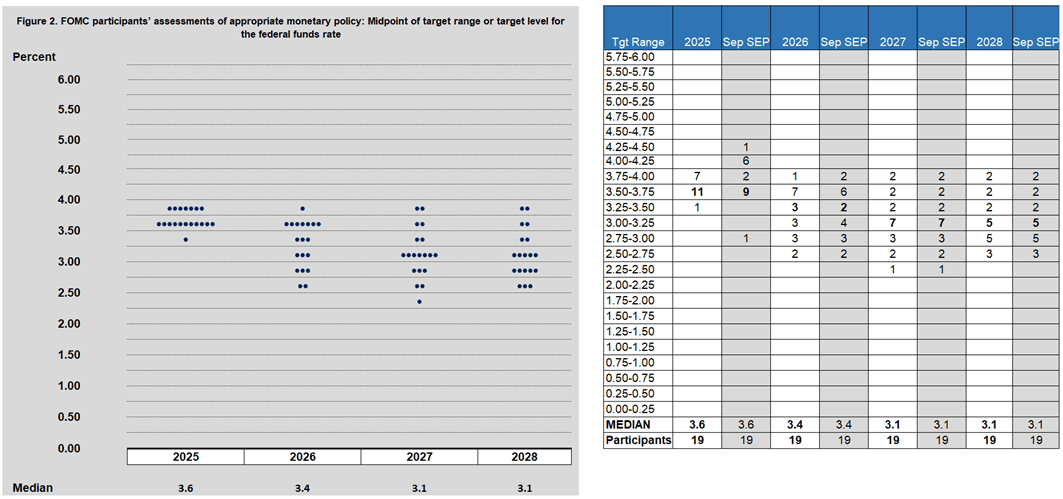

MNI FED: SEP/Dot Plot: Steady Course

The lack of major data since the September projections round portends only limited changes to the macro and rate forecasts in the December edition out Wednesday. None of the rate dot medians are expected to change, with 2025 confirmed at 3.6% (though with an unusual amount of disagreement in the dot distribution for an end-year SEP in a form of "soft dissent" against the cut), 2026 at 3.4% (implying one 25bp cut), with 2027 at 3.1% (another 25bp cut).

- In short, we expect most of the attention to be on the rate distribution. For 2026, the September dots were closely poised between 3.4% and 3.1% (10 above 3.25% vs 9 below 3.25%). We don’t see much change here but if anything the risks to the median skew to the downside. For example, if one member who put their dot at 3.4% in September also saw rates ending 2025 at 3.9%, they might mark-to-market the rate view one notch lower.

NEWS

MNI FRANCE: Lawmakers Back Spending Part Of Social Security Budget

- "*FRENCH LAWMAKERS BACK SPENDING PART OF SOCIAL-SECURITY BUDGET" - bbg

- Le Monde, translated: "Members of Parliament adopt the third part of the Social Security budget relating to expenditure. On Tuesday, members of parliament adopted the third part of the draft social security financing bill (PLFSS) for 2026, relating to expenditure, with 227 votes in favor and 86 against."

US/UKRAINE: US Pres "TRUMP GIVES ZELENSKIY ‘DAYS’ TO RESPOND TO PEACE PROPOSAL" Financial Times

MNI US-EU: Trump Lambasts European Leaders As 'Weak'

In an interview with Politico, US President Donald Trump lambasted European leaders for perceived weaknesses. Trump said, when asked about the leaders of US' European allies,“I think they’re weak, but I think they also want to be so politically correct…I think they don’t know what to do. Europe doesn’t know what to do.”

- Trump also reiterated that his administration would not refrain from endorsing European politicians and parties with which it agrees. Earlier in 2025, VP JD Vance faced criticism among European moderates for meeting with figures from the far-right Alternative for Germany during his visit to Germany for the Munich Security Conference. Trump said when asked about offending the governments of allies by backing their opponents, “I’d endorse, I’ve endorsed people, but I’ve endorsed people that a lot of Europeans don’t like. I’ve endorsed Viktor Orbán.”

US TSYS

MNI US TSYS: JOLTS Jobs Opening Surge Ahead Final FOMC for 2025

- Treasuries look to finish near late session lows Tuesday, initial impetus after Job openings were far higher than expected in October at 7670k (sa, cons 7117k) and were also higher than presumably expected at 7658k in September data also released today. It’s a marked increase compared to the 7227k seen in August shortly before the government shutdown.

- Treasuries extended lows after a block Sale -6,000 TYH6 112-03, post time bid at 1356:11ET, DV01 $403,000. Treasuries extended session lows following the cross - TYH6 tapped yesterday's low of 112-02.5 (-5.5) - before drawing some support to 112-04.

- Round number support in focus: 112-00, the 1.00 projection of the Oct 17 - Nov 5 - 25 price swing. Clearance of this level would open 111-19, the 1.236 projection.

- Curves flattened (2s10s -1.569 at 57.155, 5s30s -2.681 at 102.702) while forward rate cut pricing projections consolidated ahead what is still expected to be a 25bp cut by the FOMC tomorrow.

- Wednesday's FOMC policy annc, includes summary of economic projections at 1400ET, Chairman Powell press conference at 1430ET.

- Inter-meeting communications reinforced that the FOMC is finely split between those who would ease further and those who are resistant - if not outright opposed - to providing further accommodation. Overall there were no members who became more dovish on the rate outlook since October, while there were signs that at least a few have become more hawkish.

OVERNIGHT DATA

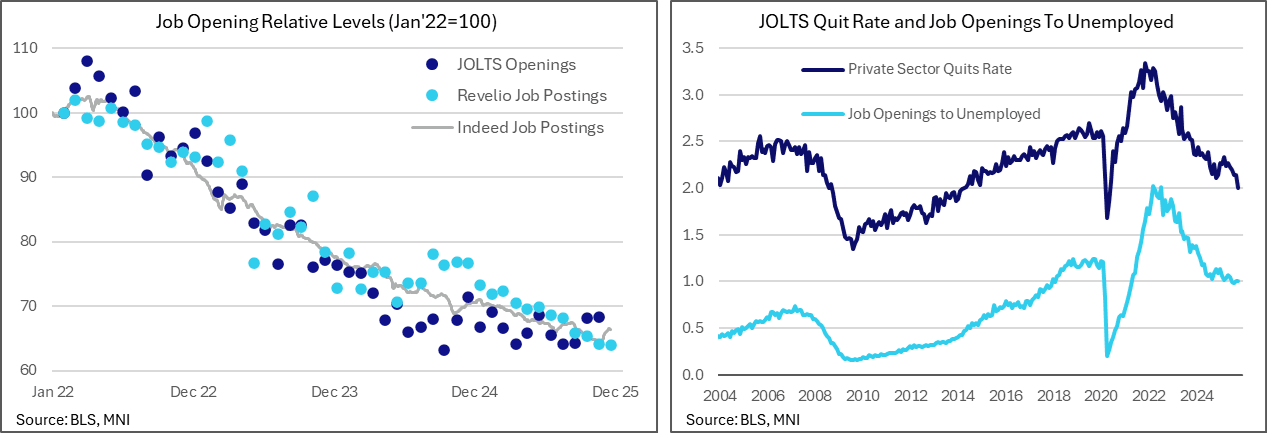

MNI US DATA: Much Higher Than Expected JOLTS Job Openings…

Job openings in the delayed BLS JOLTS report were far higher than expected in October. There was rare relative outperformance to alternative sources such as Indeed or Revelio that had helped form expectations of a modest steady decline compared to August data last released just prior to the government shutdown.

- Job openings were far higher than expected in October at 7670k (sa, cons 7117k) and were also higher than presumably expected at 7658k in September data also released today. It’s a marked increase compared to the 7227k seen in August shortly before the government shutdown. As the chart below shows, the size of this deviation from alternate indicators such as Indeed or Revelio isn’t new but JOLTS being relatively higher than them certainly is.

MNI US DATA: … But Other JOLTS Indicators Read Clearly Softer

The quits rate fell further in October to its lowest since 2014 when excluding two pandemic months of 2020 and the hires rate broadly confirmed August’s decline to lows since 2021.

- The quits rate was reported at 1.8%, down from 1.96 in September and 1.94 in August. We have taken this October quits rate from the 1.d.p value reported by the BLS rather than our usual unrounded calculations which use the usually already known level of payrolled employment in the month.

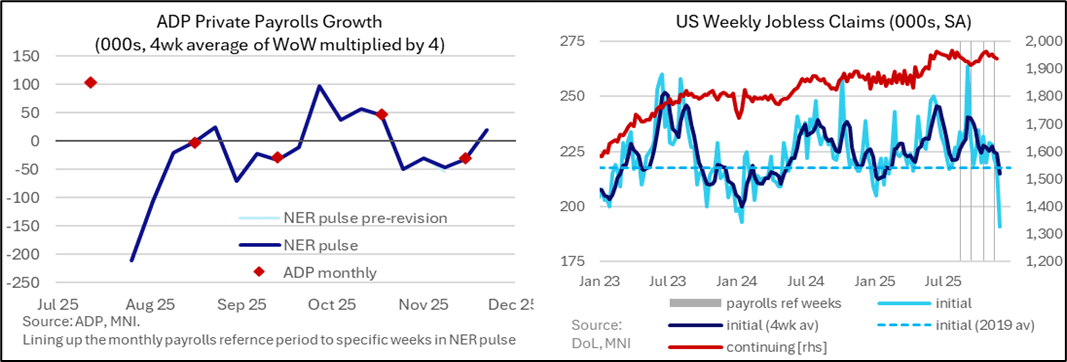

MNI US DATA: Weekly ADP Improves In Late November

The resumption of the latest weekly ADP estimate improved in late November although it’s still too early to be an useful gauge of momentum heading into the monthly payrolls/ADP reference period. ADP employment saw an average week-on-week increase of 4.75k in the four weeks to Nov 22, a reasonable turnaround after declining into the reference period earlier in November.

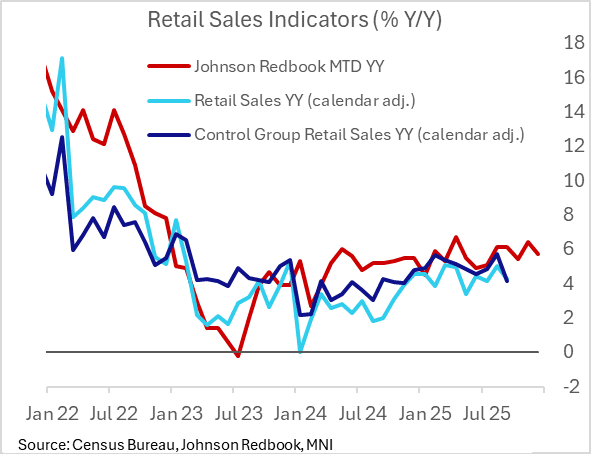

MNI US DATA: Redbook Retail Sales Continue To Grow At Near 6% Pace

Johnson Redbook Retail Sales continued to post solid growth into December, with the week ending December 6 (and therefore the month-to-date) seeing 5.7% Y/Y expansion. This follows 6.4% sales in November.

- We'll only get October Census Bureau retail sales data out on Dec 16 due to federal government shutdown postponements, but since September Redbook has been averaging 5.8% Y/Y growth - suggesting continued solid dynamics even if only in nominal terms. Final Chicago Fed CARTS ex-autos retail sales data for November is due out Dec 19; the prelim release showed +0.4% M/M expansion, or 0.3% in inflation-adjusted terms.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 178.51 points (-0.37%) at 47560.81

S&P E-Mini Future down 7 points (-0.1%) at 6848.5

Nasdaq up 30.6 points (0.1%) at 23576.49

US 10-Yr yield is up 1.8 bps at 4.1819%

US Mar 10-Yr futures are down 5/32 at 112-3

EURUSD down 0.0011 (-0.09%) at 1.1627

USDJPY up 1.02 (0.65%) at 156.93

WTI Crude Oil (front-month) down $0.51 (-0.87%) at $58.37

Gold is up $21.26 (0.51%) at $4211.85

European bourses closing levels:

EuroStoxx 50 down 7.27 points (-0.13%) at 5718.32

FTSE 100 down 3.08 points (-0.03%) at 9642.01

German DAX up 116.64 points (0.49%) at 24162.65

French CAC 40 down 55.92 points (-0.69%) at 8052.51

US TREASURY FUTURES CLOSE

Curve update:

3M10Y +1.02, 46.965 (L: 43.124 / H: 47.356)

2Y10Y -1.581, 57.143 (L: 56.398 / H: 59.103)

2Y30Y -2.837, 119.644 (L: 119.155 / H: 123.087)

5Y30Y -2.829, 102.554 (L: 102.426 / H: 105.916)

Current futures levels:

Mar 2-Yr futures down 2.125/32 at 104-5.125 (L: 104-05 / H: 104-08.25)

Mar 5-Yr futures down 4.25/32 at 108-29.75 (L: 108-29.5 / H: 109-05.25)

Mar 10-Yr futures down 5/32 at 112-3 (L: 112-02.5 / H: 112-14)

Mar 30-Yr futures up 5/32 at 115-8 (L: 115-02 / H: 115-23)

Mar Ultra futures up 6/32 at 118-12 (L: 118-06 / H: 118-30)

MNI US 10YR FUTURE TECHS: (H6) Support Breached

- RES 4: 113-29+ High Oct 17 and a key resistance

- RES 3: 113-23 High Oct 23

- RES 2: 113-07/22+ High Dec 3 / High Nov 25

- RES 1: 112-28 20-day EMA

- PRICE: 112-07 @ 1230 ET Dec 9

- SUP 1: 112-02+ Low Dec 08 & Sep 25

- SUP 2: 112-00+ 50% of the July - October Upleg

- SUP 3: 112-00 1.000 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 4: 111-19 1.236 proj of the Oct 17 - Nov 5 - 25 price swing

A bearish theme in Treasuries remains intact and Monday’s move down reinforces current bearish conditions. Price has traded through 112-07, the Nov 5 high and a bear trigger. The breach strengthens a bear theme and signal scope for a move towards 112-00 next, the 1.00 projection of the Oct 17 - Nov 5 - 25 price swing. Clearance of this level would open 111-19, the 1.236 projection. Initial firm resistance is seen at 112-28, the 20-day EMA.

SOFR FUTURES CLOSE

Current White pack (Dec 25-Sep 26):

Dec 25 -0.003 at 96.265

Mar 26 -0.025 at 96.405

Jun 26 -0.030 at 96.595

Sep 26 -0.035 at 96.725

Red Pack (Dec 26-Sep 27) -0.055 to -0.04

Green Pack (Dec 27-Sep 28) -0.05 to -0.035

Blue Pack (Dec 28-Sep 29) -0.035 to -0.025

Gold Pack (Dec 29-Sep 30) -0.025 to -0.02

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.95% (+0.02), volume: $3.209T

- Broad General Collateral Rate (BGCR): 3.93% (+0.03), volume: $1.311T

- Tri-Party General Collateral Rate (TCR): 3.93% (+0.03), volume: $1.290T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.89% (+0.00), volume: $84B

- Daily Overnight Bank Funding Rate: 3.89% (+0.00), volume: $160B

FED Reverse Repo Operation

RRP usage rises to $3.211B with 10 counterparties this afternoon from $1.703B Monday. Compares to Tuesday November 18: $0.905B - lowest level since mid-March 2021; this years highest excess liquidity measure: $460.731B on June 30.

MNI PIPELINE: Corporate Bond Update: Issuance Slows Ahead Final FOMC for 2025

- Date $MM Issuer (Priced *, Launch #)

- 12/09 $750M #Bank of Montreal 2NC1 +50

- 12/09 $500M #American National Global Funding 3Y +100

- $3.6B Priced Monday

MNI BONDS: EGBs-GILTS CASH CLOSE: Modest Bounce Ahead Of Fed Meeting

European yields fell modestly Tuesday, with Gilts slightly outperforming Bunds.

- EGBs and Gilts resumed the weakness seen in the prior two sessions in early trade, coming off session lows around 0830ET as European equities pulled back from what would be session highs.

- There was no obvious macro driver to the latter move, with the rest of the session seeing relatively limited movement amid a thin data slate (US job openings saw bonds come off session highs) and events docket and ahead of Wednesday's Federal Reserve decision.

- Ahead of next week's rate decision, BoE Deputy Governor Ramsden leaned a little dovish in TSC testimony though this brought limited market reaction.

- OAT futures gained slightly after hours as the French parliament passed the spending part of the contentious Social Security budget.

- Wednesday's calendar includes Italian industrial production data and appearance by ECB's Lagarde and Makhlouf, but most global attention will be on the Fed meeting where policymakers are set to deliver a "hawkish cut" of 25bp.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.5bps at 2.154%, 5-Yr is down 1.3bps at 2.466%, 10-Yr is down 1.2bps at 2.85%, and 30-Yr is down 0.2bps at 3.459%.

- UK: The 2-Yr yield is down 2.6bps at 3.785%, 5-Yr is down 2.4bps at 3.972%, 10-Yr is down 2.3bps at 4.505%, and 30-Yr is down 3.3bps at 5.195%.

- Italian BTP spread down 0.5bps at 69.5bps / French OAT down 0.5bps at 71.3bps

MNI FOREX: USD Index Modestly Higher Pre-Fed, AUDJPY Extends Sharp Upswing

- The USD index has mirrored a turbulent session for US yields, and tilts moderately higher as we approach the APAC crossover. The main boost for the USD index came after the stronger-than-expected double release of US JOLTS data, painting a better picture of the US labour market.

- The next key driver for the greenback will be tomorrow's FOMC, with more attention than usual on the Statement to see how resolutely the easing bias remains. Forward guidance is likely to be amended to reflect a more patient stance on cuts. As such the market reaction to the meeting could hinge on how Chair Powell portrays the burden of proof for further easing ahead.

- Clearer direction was seen elsewhere in G10 FX, with AUD and SEK clear outperformers, while the Japanese yen struggled once more.

- AUD has been primarily driven by a hawkish RBA, following its decision to hold rates at 3.6% and the balance of risks now tilted toward a potential hike next year to contain inflationary pressures. AUDUSD briefly rose to a fresh recovery high at 0.6654, keeping bullish conditions firmly intact. 0.6707 remains the key AUDUSD resistance, the Sep 17 high.

- Downward pressure on the JPY continues to be in focus this week, amid the hawkish repricing for core fixed income markets and regional geopolitical uncertainty taking its toll. Combining this with a firm risk backdrop (major equity indices maintaining a stable tone towards recent highs), Cross/JPY has been a notable beneficiary of the overall dynamics. AUDJPY briefly extended gains to over 1% on the session, printing a high of 104.40.

- In emerging markets, the Mexican peso is performing relatively well today, maintaining its resilient profile of late. Above expectation inflation data has prompted a hawkish repricing across the TIIE-F swaps curve, as the market assesses a potential imminent turning point for Mexican monetary policy.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 10/12/2025 | 0700/0800 | *** | CPI Norway | |

| 10/12/2025 | 0700/0800 | ** | Private Sector Production m/m | |

| 10/12/2025 | 0900/1000 | * | Industrial Production | |

| 10/12/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 10/12/2025 | 1000/1000 | Chancellor Reeves Testifies at TSC on Budget | ||

| 10/12/2025 | 1045/1045 | BOE Bailey Pre-recorded Chat on Financial Stability | ||

| 10/12/2025 | 1055/1155 | ECB Lagarde Interview on Currencies/Digital Euro | ||

| 10/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 10/12/2025 | 1200/0700 | ** | Brazil Final CPI | |

| 10/12/2025 | - | *** | Money Supply | |

| 10/12/2025 | - | *** | Social Financing | |

| 10/12/2025 | - | *** | New Loans | |

| 10/12/2025 | 1330/0830 | *** | Employment Cost Index | |

| 10/12/2025 | 1445/0945 | *** | Bank of Canada Policy Decision | |

| 10/12/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 10/12/2025 | 1530/1030 | BOC press conference | ||

| 10/12/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 10/12/2025 | 1900/1400 | ** | Treasury Budget | |

| 10/12/2025 | 1900/1400 | *** | FOMC Statement | |

| 10/12/2025 | 1930/1430 | Fed Chair Powell Press Conference | ||

| 11/12/2025 | - | Swiss National Bank Meeting | ||

| 11/12/2025 | 0001/0001 | * | RICS House Prices | |

| 11/12/2025 | 0030/1130 | *** | Labor Force Survey |