US OUTLOOK/OPINION: Macro Since Last FOMC - Labor: Stabilization Elsewhere

Dec-09 20:11

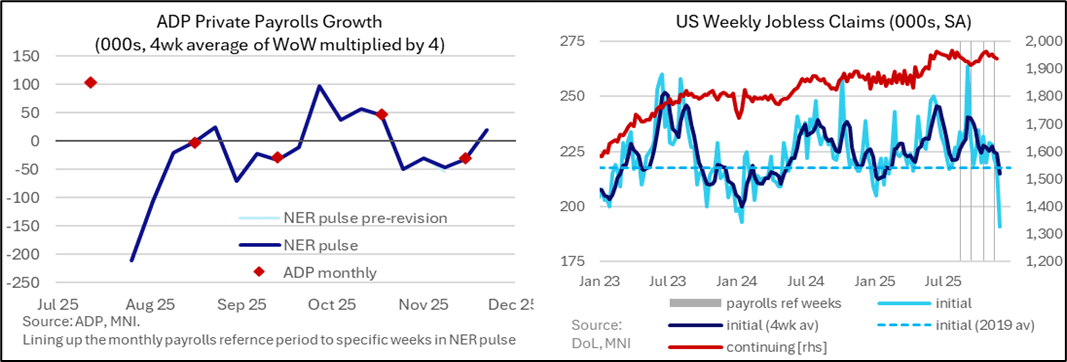

- Since the delayed September payrolls report, ADP employment has sent mixed signals – it surprisingly firmed in October after declining in September, returned to declining with a -32k drop in the main November report for a third monthly decline in the space of four months before some stabilization in latest weekly data.

- However, some unemployment rate trackers such as the Chicago Fed’s nowcast point to no further deterioration in the labor market ahead, with this nowcast tracking at the same 4.44% in November after 4.46% in October.

- Granted, the surprise increase in the BLS unemployment rate in September has clearly appeared sufficient to sway Williams and seemingly other core FOMC members to the need for another cut in what might be viewed as a further insurance cut.

- Certainly, hawks will point to weekly jobless claims data not showing any additional deterioration in the labor market, with initial claims at very low levels even when looking through the latest slide to its lowest in three years in what looks like a Thanksgiving adjustment distortion. Granted, re-hiring conditions are softer as evidenced by continuing claims but they roughly remain at levels seen in payrolls reference periods from earlier in the year.

- In an addition to what we wrote in the Fed preview, the double JOLTS report for September and October on day one of the two-day FOMC meeting saw much higher than expected job openings but with quit and hire rates casting a more dovish light. Higher frequency Indeed job openings data had suggested stabilization before a recent increase into November.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

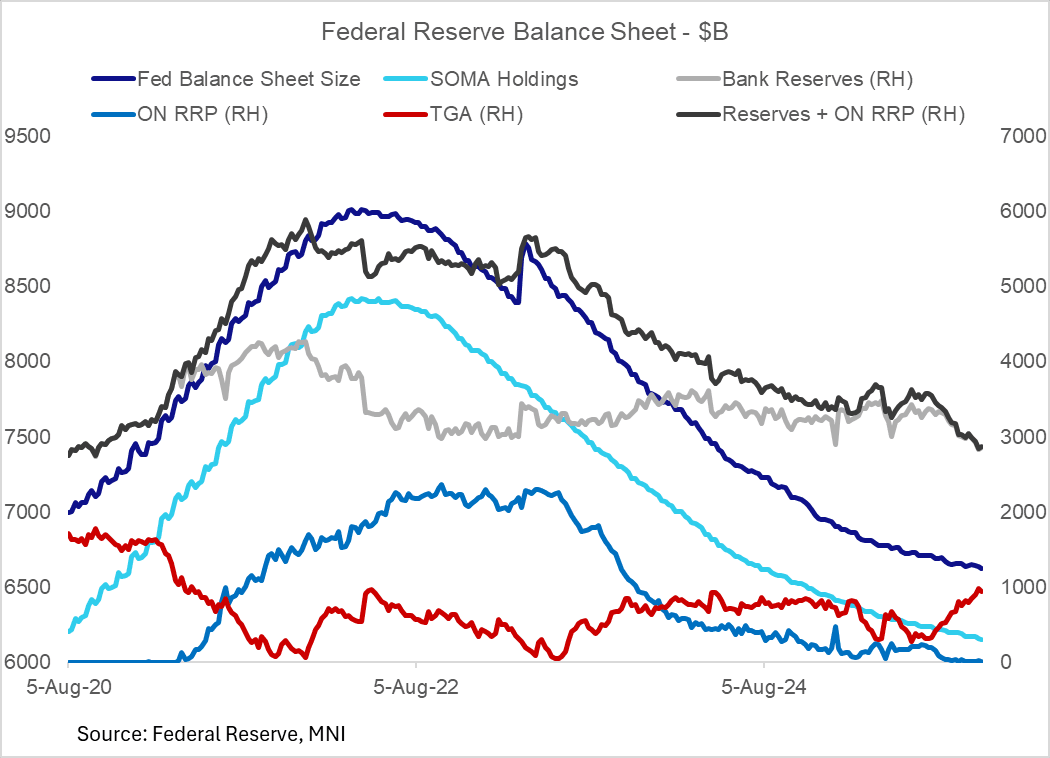

FED: Fed Assets Pull Back, But Reserve Management Buys Eyed In 2026 (2/2)

Nov-07 21:58

Indeed NY's Williams has already begun pointing to potential for balance sheet re-expansion to begin again, with "reserve management" purchases intended to keep Fed liabilities rising in line with market demand:

- "Looking forward, the next step in our balance sheet strategy will be to assess when the level of reserves has reached ample. It will then be time to begin the process of gradual purchases of assets that will maintain an ample level of reserves as the Fed’s other liabilities grow and underlying demand for reserves increases over time. Such reserve management purchases will represent the natural next stage of the implementation of the FOMC’s ample reserves strategy and in no way represent a change in the underlying stance of monetary policy."

- The prevailing consensus is that such reserve management purchases will begin by the end of Q1 2026 if not earlier, with t-bills bought and in amounts of up to $20B a month.

- Meanwhile in the final countdown to the end of QT on December 1, net SOMA runoff was around $4B in the last week, with a pace of around $20B overall over the last month.

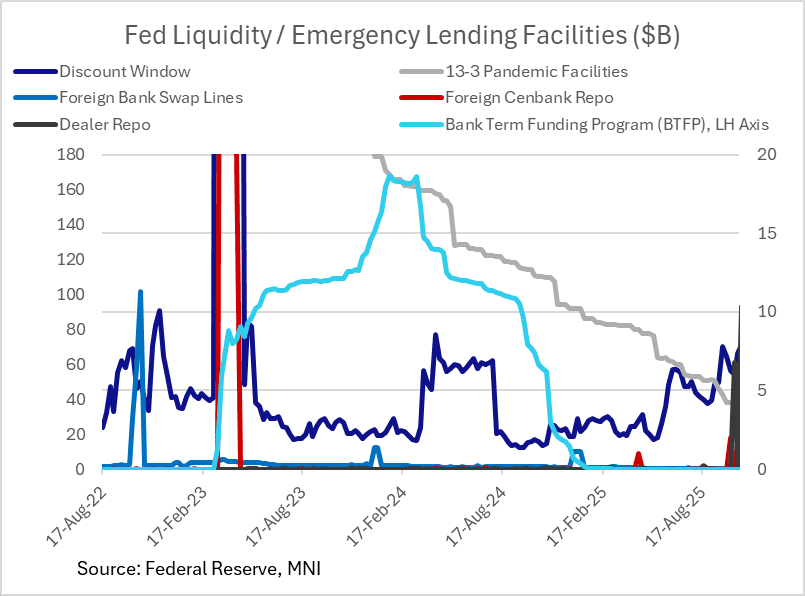

- Takeup of the Fed's lending facilities pulled back in the week to Wednesday Nov 5, halving to just over $11B as month-end pressures abated. This was due almost entirely to a $10.2B drop in dealer repo operation takeup, the spike in which last week marked the highest since 2020.

FED: Reserves Tick Up Slightly In Latest Week, But Still Near "Ample" (1/2)

Nov-07 21:53

The Fed's latest H.4.1 release on Nov 5 showed reserves picked up from the prior week's post-2020 lows to $2.85T, up $24B in the latest week but still down $182B over the last month.

- This of course has been the mirror image of movements in the Treasury General Account which briefly touched $1T though settled Wednesday at $943B (a fall of $41B on the week, but a rise of $149B in a month).

- Treasury indicated this week that it maintained its $850B quarter-end cash target, with the recent buildup due in part to the federal government shutdown slowing outflows but also a typical cautionary cash rase ahead of large seasonal expenditures.

- The Fed's reverse repo facilities remained in relatively negligible territory albeit with a slight pickup at month-end October.

- Overall the Fed has recognized that it may be getting close to the transition point between once-"abundant" and now merely "ample" reserves, hence October's decision to end net asset runoff as of Dec 1.

- NY Fed President Williams said Friday morning “Based on recent sustained repo market pressures and other growing signs of reserves moving from abundant to ample, I expect that it will not be long before we reach ample reserves."

FED: Financial Stability Report Eyes Term Premia And "Opaque" Financing Risks

Nov-07 21:31

A few highlights from the Fed's latest Financial Stability report out today (link):

- In terms of asset valuations, "Prices remained high relative to their historical relationship with fundamentals across a range of markets."

- The report highlights high leverage in the financial sector: "Vulnerabilities associated with financial leverage remained notable. Over the past few years, hedge funds’ leverage has steadily increased across a broad range of strategies, including those involving Treasury securities, interest rate derivatives, and equities"

- However "Vulnerabilities from business and household debt remained moderate" and "The banking sector remained sound and resilient overall, and most banks continued to report capital levels well above regulatory requirements."

- In terms of future risks, "A further increase in term premiums leading to higher-than-anticipated long-term interest rates, particularly if accompanied by

persistent inflation, could pose risks for both borrowers and lenders" - And the Fed has its eye on "opaque off-balance-sheet funding arrangements" re the recent voliatility caused by First Brands and Tricolor: "The recent bankruptcies of two privately held firms, an auto parts supplier and a subprime auto lender, so far appear to be isolated events. However, these examples highlight that unexpected losses could arise from opaque off-balance-sheet funding arrangements that may be used by certain privately held firms."