MNI ASIA OPEN: Tsys Retreat on Stronger New Home Sales

EXECUTIVE SUMMARY

- MNI FED: Low R-Star Era Far From Over – NY Fed Staff

- MNI FED: Chair Candidate Hassett: Powell's "Pivot" Was "Data-Driven" And "Sound"

- MNI US DATA: Building Permits Revised Up Slightly, Single Family Activity Still Weak

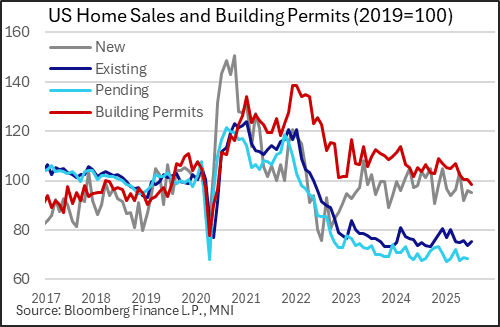

- MNI US DATA: New Home Sales Activity Not As Bad As Once Thought, But Still Weak

US

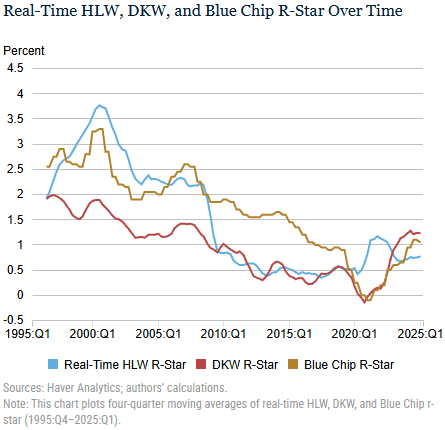

MNI FED: Low R-Star Era Far From Over – NY Fed Staff

A Liberty Street Economics blog post from NY Fed staff including President John Williams (FOMC permanent voter) writes that “a reasonable estimate is that r-star has risen by a relatively modest 1/4 to 1/2 percentage point from its 2018 level. Thus, despite the recent rise in TIPS yields, the evidence suggests that the low r-star era is far from over.” This is “significantly smaller” than the 1.5pp increase in the longer-term TIPS yield over the same period. However, we add that this isn’t new rhetoric ahead of Williams’ appearance later today at 1915ET.

NEWS

MNI FED: Chair Candidate Hassett: Powell's "Pivot" Was "Data-Driven" And "Sound"

NEC director Kevin Hassett (known to be a candidate for the next Fed Chair) tells CNBC that Chair Powell's Jackson Hole speech showed a Fed that is "late" to cut but that Powell's presentation was "sound" and "data driven". He also suggests that it could be another few months before President Trump makes his decision on the next Chair. "I think that the pivot was accurate. It was data driven. If you look at the trailing six month inflation rate, it's 1.9%; core is about half percent higher than that, and so inflation has gone way down.

TRUMP FLOATS 200% TARIFF THREAT ON CHINA IF MAGNETS NOT DELIVERED, Bbg

TRUMP: WILL PROBABLY GO TO CHINA THIS YEAR OR SHORTLY AFTER, Bbg

TRUMP: IF I PLAYED MY CARDS, IT'D DESTROY CHINA; I WON'T, Bbg

TRUMP ADMIN. WEIGHS SANCTIONS ON EU OFFICIALS: REUTERS

US TSYS

MNI US TSYS: Tsys Retreat, Greenback Bounce, Both Unwind Half Fri's Post Powell Move

- Relatively quiet start to the week with London out for annual bank holiday. Treasuries opened weaker - scaling back a fair portion of Friday's post-Chair Powell speech in Jackson Hole that left the door open to a possible rate cut at the next FOMC annc on September 17.

- NEC director Kevin Hassett (potential Fed Chair candidate) tells CNBC that Chair Powell's Jackson Hole speech showed a Fed that is "late" to cut but that Powell's presentation was "sound" and "data driven".

- Treasury futures maintained losses after higher than expected new home sales - but climbed back to mildly weaker levels on the open. After the bell, Se'25 10Y contract trades -6.5 at 111-30 vs. 111-27.5 low. Support around the 50-day EMA, at 111-13. A clear break of this average would expose support at 110-23+, the Aug 1 low.

- The June reading of 652k (seasonally-adjusted, annualized) was better than the 630k Bloomberg consensus, but actually represented a slight fall (-0.6%) on the month due to a sizeable upward revision to June to 656k (from 627k).

- July's building permits were revised up in the final reading to 1,362k (annualized, seasonally-adjusted), vs 1,354k in the initial estimate. That got the data a little closer to the 1,386k consensus estimate going into the initial reading last week, though either way it is a pullback from 1,393k in June (a 2.2% fall vs the 2.8% initially recorded).

- US$ continued to climb in late trade, recovering appr half of Friday's decline. Today's move said to be EUR related after the French confidence vote call earlier. The Bbg $ index: BBDXY +5.94 at 1207.43 vs. 1201.02 low.

OVERNIGHT DATA

MNI US DATA: New Home Sales Activity Not As Bad As Once Thought, But Still Weak

New home sales were much stronger than expected in July, with an upward revision to June suggesting that activity has been stronger this summer than previously estimated - but nonetheless, broader trends of elevated inventories and falling prices continue to suggest increasing slack in the new build market. The June reading of 652k (seasonally-adjusted, annualized) was better than the 630k Bloomberg consensus, but actually represented a slight fall (-0.6%) on the month due to a sizeable upward revision to June to 656k (from 627k).

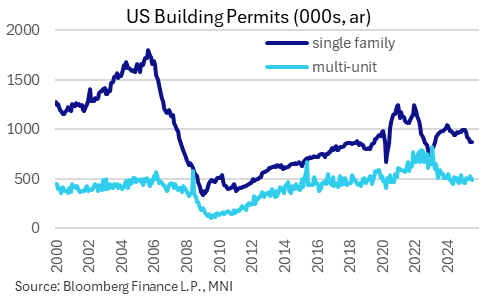

MNI US DATA: Building Permits Revised Up Slightly, Single Family Activity Still Weak

July's building permits were revised up in the final reading to 1,362k (annualized, seasonally-adjusted), vs 1,354k in the initial estimate. That got the data a little closer to the 1,386k consensus estimate going into the initial reading last week, though either way it is a pullback from 1,393k in June (a 2.2% fall vs the 2.8% initially recorded). The upward revision was due to both single family permitting getting revised up 5k to 875k, and multi-unit up 3k (to 487k).

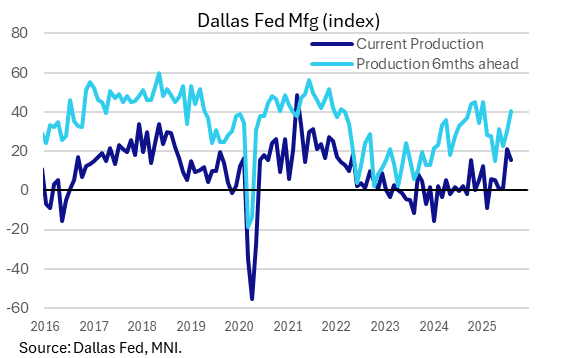

MNI US DATA: Better Activity, Still-Elevated Inflation In Texas Manufacturing Sector

The Dallas Fed's Texas Manufacturing Outlook Survey for August showed continued growth in regional production, albeit with a slightly bigger than anticipated relapse in the overall general business activity index and slightly firmer price pressures. While these readings are volatile month-to-month, they continue to suggest improvement in activity after a tariff-hit period, but price pressures remain elevated (and regional firms still sound extremely concerned about tariff impacts).

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 322.61 points (-0.71%) at 45312.05

S&P E-Mini Future down 16.5 points (-0.25%) at 6467

Nasdaq up 17.6 points (0.1%) at 21514.68

US 10-Yr yield is up 2.7 bps at 4.2809%

US Sep 10-Yr futures are down 7/32 at 111-29.5

EURUSD down 0.0111 (-0.95%) at 1.1607

USDJPY up 0.93 (0.63%) at 147.87

WTI Crude Oil (front-month) up $1.12 (1.76%) at $64.77

Gold is down $3.42 (-0.1%) at $3368.60

European bourses closing levels:

EuroStoxx 50 down 44.27 points (-0.81%) at 5443.96

German DAX down 89.97 points (-0.37%) at 24273.12

French CAC 40 down 126.65 points (-1.59%) at 7843.04

US TREASURY FUTURES CLOSE

3M10Y +2.508, 8.027 (L: 3.369 / H: 8.677)

2Y10Y -1.056, 54.472 (L: 53.728 / H: 56.795)

2Y30Y -1.95, 115.76 (L: 115.269 / H: 120.951)

5Y30Y -1.211, 110.268 (L: 109.557 / H: 114.709)

Current futures levels:

Sep 2-Yr futures down 3/32 at 103-27.125 (L: 103-27 / H: 103-29.625)

Sep 5-Yr futures down 5.25/32 at 108-28.25 (L: 108-27 / H: 109-01)

Sep 10-Yr futures down 6.5/32 at 111-30 (L: 111-27.5 / H: 112-05)

Sep 30-Yr futures down 7/32 at 114-20 (L: 114-10 / H: 115-00)

Sep Ultra futures down 8/32 at 117-7 (L: 116-24 / H: 117-20)

MNI US 10YR FUTURE TECHS: (U5) Trend Structure Remains Bullish

- RES 4: 113-23 76.4% retracement of the Sep’24 - Jan’25 sell-off

- RES 3: 113-07 76.4% retracement of the Apr 7 - 11 sell-off

- RES 2: 112-23 High May 1

- RES 1: 112-15+ High Aug 5 and the bull trigger

- PRICE: 112-01+ @ 11:26 BST Aug 25

- SUP 1: 111-13 50-day EMA

- SUP 2: 110-23+/08+ Low Aug 1 / Low Jul 15 & 16

- SUP 3: 110-03 76.4% retracement of the May 22 - Jul 1 bull leg

- SUP 4: 109-28 Low Jun 6 and 11

A bullish theme in Treasury futures remains intact and the contract continues to trade above support around the 50-day EMA, at 111-13. A clear break of this average would expose support at 110-23+, the Aug 1 low. For bulls, sights are on 112-15+, the Aug 5 high and the bull trigger. Clearance of this hurdle would resume the uptrend and pave the way for a climb towards 112-23 initially, the May 1 high.

SOFR FUTURES CLOSE

Current White pack (Sep 25-Jun 26):

Sep 25 -0.015 at 95.880

Dec 25 -0.035 at 96.195

Mar 26 -0.055 at 96.435

Jun 26 -0.060 at 96.675

Red Pack (Sep 26-Jun 27) -0.055 to -0.035

Green Pack (Sep 27-Jun 28) -0.035 to -0.025

Blue Pack (Sep 28-Jun 29) -0.02 to -0.01

Gold Pack (Sep 29-Jun 30) -0.005 to steady

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.36% (+0.04), volume: $2.738T

- Broad General Collateral Rate (BGCR): 4.35% (+0.04), volume: $1.143T

- Tri-Party General Collateral Rate (TCR): 4.35% (+0.04), volume: $1.118T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $117B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $263B

FED Reverse Repo Operation

RRP usage rises to $47.567B this afternoon from $36.275B Friday -- compares to $22.344B on Tuesday, Aug 19 - lowest since April 5, 2021. Total number of counterparties at 23. This year's high usage of $460.731B on June 30.

MNI PIPELINE: Corporate Bond Roundup: $1.05B SEB Launched

- Date $MM Issuer (Priced *, Launch #)

- 08/25 $1.05B #Skandinaviska Enskilda Banken AB (SEB) $750M 5Y +73, $300M 5Y SOFR+106

MNI BONDS: EGBs-GILTS CASH CLOSE: OAT Spreads Widen Sharply On Confidence Vote

Periphery/semi-core EGB spreads widened amid a broader sell-off Monday, with the Gilt market closed for holidays.

- EGBs were under some pressure in early trade, with Bund yields moving back above the levels seen just prior to Friday's speech by Federal Reserve Chair Powell at Jackson Hole which triggered a broad global bond rally.

- And just over an hour before the European cash close, OATs sold off and Bunds rallied in a risk-off move after French PM Bayrou called for a confidence vote in the government to be held on September 8 (an extraordinary meeting that is two weeks before lawmakers were set to return) in a gambit to get his controversial fiscal legislation passed.

- Having already widened modestly earlier in the session, 10Y OAT/Bund jumped to its widest close since April at 75.2bp.

- Similarly, earlier widening in other periphery EGBs (Italy/Greece most notably) extended after the French news.

- Earlier in the session, German IFO was broadly in line with expectations.

- The belly underperformed on the German curve, in a bear-flattening lean overall.

- Focus for the week is on national/Eurozone flash August inflation data, most of which arrives on Friday.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 2.7bps at 1.975%, 5-Yr is up 3.8bps at 2.315%, 10-Yr is up 3.5bps at 2.757%, and 30-Yr is up 2.3bps at 3.332%.

- Italian BTP spread up 3.4bps at 83.8bps / French OAT up 5.7bps at 75.2bps

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 26/08/2025 | 0600/0800 | ** | PPI | |

| 26/08/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 26/08/2025 | - | DMO to hold FQ3 consultations with investors / GEMMs | ||

| 26/08/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 26/08/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 26/08/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 26/08/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 26/08/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 26/08/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 26/08/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 26/08/2025 | 1300/0900 | ** | FHFA Quarterly Price Index | |

| 26/08/2025 | 1300/0900 | ** | FHFA Quarterly Price Index | |

| 26/08/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 26/08/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 26/08/2025 | 1400/1500 | BOE Mann at Banxico Conference (text release) | ||

| 26/08/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 26/08/2025 | 1700/1300 | * | US Treasury Auction Result for 2 Year Note | |

| 26/08/2025 | 1830/1430 | BOC Governor speech in Mexico City | ||

| 27/08/2025 | 0130/1130 | *** | CPI Inflation Monthly | |

| 27/08/2025 | 0130/1130 | *** | Quarterly construction work done |