MNI ASIA OPEN: Tsy Yields Slip Lower, Focus on Wk's PPI, CPI

EXECUTIVE SUMMARY

- MNI INTERVIEW: US Job Market At Potential Pivot Point - Shin

- MNI FRANCE: PM Bayrou Loses Confidence Vote As Expected

- MNI INTERNATIONAL TRADE: Familiar Themes In China's August Goods Trade Data

- MNI US DATA: NY Fed Consumer Survey: Inflation Expectations Looking Stubborn

US

MNI INTERVIEW: US Job Market At Potential Pivot Point - Shin

A raft of soft U.S. jobs data adds weight to Fed Chair Jerome Powell's view that labor market risks have increased, though central bank officials need more time to determine whether employment has hit a pivot point, Yongseok Shin, a St. Louis Fed research fellow and economist at Washington University in St. Louis, told MNI. "We saw this coming. Chair Powell indicated the balance of risks is shifting. It's not red lights flashing yet, but a lot of things are pointing in same direction," he said in an interview. The FOMC is expected to cut rates by a quarter point next week and Shin said he does not see a case for a larger 50 bp cut.

NEWS

MNI FRANCE: PM Bayrou Loses Confidence Vote As Expected

In headlines that were very much expected, PM Bayrou has lost a confidence vote in parliament: "*FRENCH PREMIER BAYROU LOSES CONFIDENCE VOTE IN PARLIAMENT" - bbg

- France is “drowning in a tide of debt,” Bayrou told lawmakers Monday ahead of the vote. “You have the power to bring down the government but you don’t have the power to erase reality.” As noted earlier, French PM Francois Bayrou told the French National Assembly that lawmakers can vote "according to their conscience" today in a no-confidence vote that was expected to result in Bayrou being ousted.

MNI INTERNATIONAL TRADE: Familiar Themes In China's August Goods Trade Data

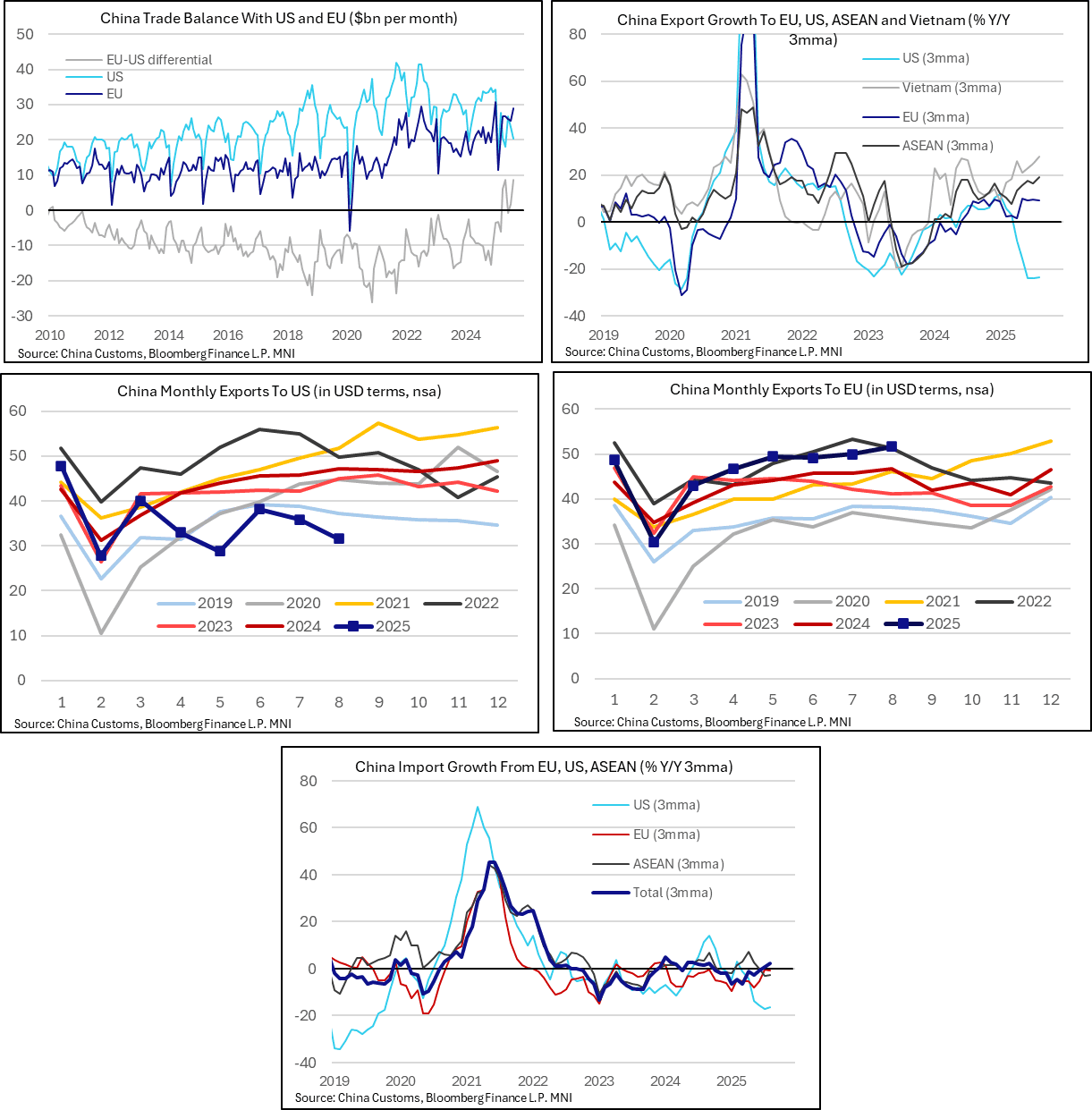

The Chinese merchandise trade surplus was wider than expected in August at $102.3bln (vs $99.45bln cons, $98.2bln prior). This came as export growth, although weaker-than-expected at 4.4% Y/Y (vs 5.5% cons, 7.2% prior) exceeded import growth of 1.3% Y/Y (vs 3.4% cons, 4.1% prior).

- Export growth to the US remains sharply negative and the value of exports remains well below recent seasonal norms. In August, exports to the US fell 33.1% Y/Y, corresponding to a -23.6% 3mma Y/Y rate. However, as we have noted on several occasions, this fall in direct exports to the US appears to be being compensated by increased transhipments to nations such as Vietnam (and other ASEAN members). Chinese exports to Vietnam were up 31.2% Y/Y in August.

- Exports to the EU remain solid but are not accelerating – pushing back against fears of tariff-related disinflationary Chinese trade diversion into the bloc. In August, exports grew at a 10.4% Y/Y clip, corresponding to a 9.1% 3mma Y/Y rate (vs 9.7% in July, 10.0% in May). The Chinese trade surplus with the EU (in USD terms for comparability) nonetheless exceeds the US trade surplus for the first time since 2010.

US TSYS

MNI US TSYS: Treasuries Drift Higher Ahead Midweek PPI/CPI Data

- Treasuries look to finish moderately higher after a flat open Monday, back near Friday's post NFP highs, stocks gaining as well as rate cut pricing into year end gathers momentum.

- Currently, the Dec'25 10Y contract trades +4.5 at 113-17 vs. -19 high, curves bull flatten: 2s10s -1.392 at 54.905, 5s30s -5.675 at 111.680. Projected rate cuts firmer vs. morning (*) levels: Sep'25 at -28.7bp (-28.4bp), Oct'25 at -49.6bp (-48.2bp), Dec'25 at -71.4bp (-70.6bp), Jan'26 at -85.1bp (-87.7bp).

- Slow start to the week regarding data, main focus is on PPI and CPI this Wednesday-Thursday respectively.

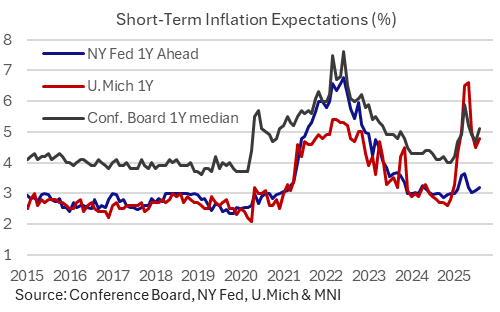

- The New York Fed's Survey of Consumer Expectations leaned in a stag-flationary direction in August, showing both an uptick in short-term inflation expectations and increasing pessimism on the labor market front.

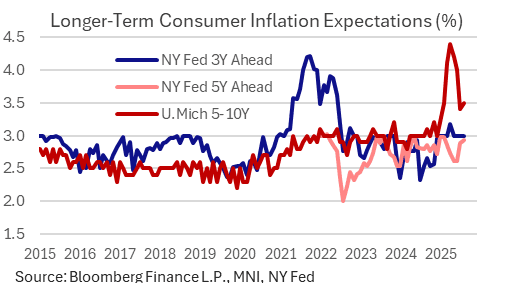

- Starting with the closely-watched inflation expectations, the survey saw a rise in the 1Y median to a 3-month high 3.20% from 3.09% prior. The 3Y median was steady at 3.00% for a 4th consecutive month, but the 5Y median ticked up to a 6-month high 2.93% (2.88% prior).

- Weaker-than-expected US employment data continues to keep the risks tilted towards the weaker dollar narrative, emphasised by the USD index spending today’s US session consolidating close to six-week lows.

OVERNIGHT DATA

MNI US DATA: NY Fed Consumer Survey: Inflation Expectations Looking Stubborn

The New York Fed's Survey of Consumer Expectations leaned in a stag-flationary direction in August, showing both an uptick in short-term inflation expectations and increasing pessimism on the labor market front. Overall the deterioration in the labor market outlook is likely to be the main takeaway from the FOMC going into its meeting next week, stubborn inflation expectations are unlikely to be ignored, illustrative of the Fed's current policy dilemma.

- Starting with the closely-watched inflation expectations, the survey saw a rise in the 1Y median to a 3-month high 3.20% from 3.09% prior. The 3Y median was steady at 3.00% for a 4th consecutive month, but the 5Y median ticked up to a 6-month high 2.93% (2.88% prior). The 1Y reading mirrors August increases in other consumer expectations surveys of 1Y inflation expectations, including UMichigan (4.80% from 4.50%) and Conference Board (6.20% from 5.70%). All are below tariff-related peaks earlier this year but appear to have bottomed out.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 66.23 points (0.15%) at 45465.4

S&P E-Mini Future up 10 points (0.15%) at 6499.5

Nasdaq up 103.6 points (0.5%) at 21804.04

US 10-Yr yield is down 3.1 bps at 4.0436%

US Dec 10-Yr futures are up 5/32 at 113-17.5

EURUSD up 0.0044 (0.38%) at 1.1761

USDJPY up 0.04 (0.03%) at 147.48

WTI Crude Oil (front-month) up $0.5 (0.81%) at $62.37

Gold is up $49.83 (1.39%) at $3636.46

European bourses closing levels:

EuroStoxx 50 up 44.66 points (0.84%) at 5362.81

FTSE 100 up 13.23 points (0.14%) at 9221.44

German DAX up 210.15 points (0.89%) at 23807.13

French CAC 40 up 60.06 points (0.78%) at 7734.84

US TREASURY FUTURES CLOSE

3M10Y -4.566, 1.353 (L: 1.163 / H: 7.7)

2Y10Y -1.392, 54.905 (L: 54.684 / H: 58.549)

2Y30Y -5.358, 119.176 (L: 118.97 / H: 127.361)

5Y30Y -5.675, 111.68 (L: 111.507 / H: 119.184)

Current futures levels:

Dec 2-Yr futures up 0.875/32 at 104-16.25 (L: 104-13.875 / H: 104-16.875)

Dec 5-Yr futures up 1.75/32 at 109-31.5 (L: 109-25.75 / H: 110-01)

Dec 10-Yr futures up 5/32 at 113-17.5 (L: 113-07.5 / H: 113-19)

Dec 30-Yr futures up 1-00/32 at 117-14 (L: 116-09 / H: 117-15)

Dec Ultra futures up 1-20/32 at 121-2 (L: 119-06 / H: 121-03)

MNI US 10YR FUTURE TECHS: (Z5) Bullish Structure

- RES 4: 114-10 High Apr 7 (cont.)

- RES 3: 114-00 Round number resistance

- RES 2: 113-26+ 2.764 proj of the Jul 15 - 22 - 28 price swing

- RES 1: 113-21+ High Sep 5

- PRICE: 113-11+ @ 11:19 BST Sep 8

- SUP 1: 112-28+/112-07+ Low Sep 5 / 20-day EMA

- SUP 2: 111-24 50-day EMA

- SUP 3: 111-13+ Low Aug 18 and a key support

- SUP 4: 110-25 Low Aug 1

Treasury futures rallied sharply higher on Friday and the contract remains closer to its recent highs The move higher highlights an acceleration of the uptrend. Note too that moving average studies are in a bull-mode position, highlighting a dominant uptrend. This paves the way for an extension through 113-21 next (pierced), the 2.618 projection of the Jul 15 - 22 - 28 price swing. Initial firm support to watch is 112-07+, the 20-day EMA.

SOFR FUTURES CLOSE

Current White pack (Sep 25-Jun 26):

Sep 25 +0.003 at 95.990

Dec 25 +0.015 at 96.385

Mar 26 +0.020 at 96.650

Jun 26 +0.020 at 96.905

Red Pack (Sep 26-Jun 27) +0.025 to +0.030

Green Pack (Sep 27-Jun 28) +0.010 to +0.025

Blue Pack (Sep 28-Jun 29) +0.010 to +0.015

Gold Pack (Sep 29-Jun 30) +0.015 to +0.030

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.42% (+0.01), volume: $2.847T

- Broad General Collateral Rate (BGCR): 4.40% (+0.02), volume: $1.161T

- Tri-Party General Collateral Rate (TCR): 4.40% (+0.02), volume: $1.127T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $116\B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $225B

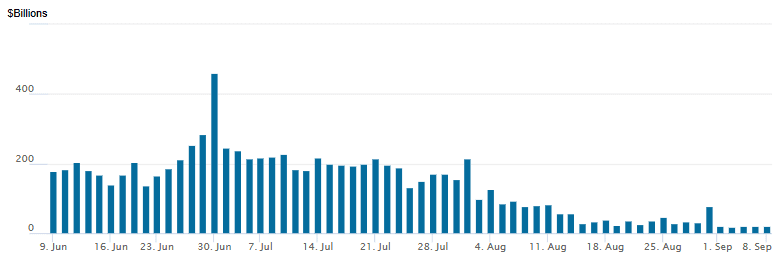

FED Reverse Repo Operation

RRP usage slips to $19.416B with 20 counterparties this afternoon from $20.997B last Friday. Compares to $17.923B on Wednesday, Sep 3 - the lowest levels since early April 2021. This year's high usage of $460.731B occurred on June 30.

MNI PIPELINE: Late Corporate Bond Update: $4B Well Fargo 3Pt Leads

At least $22B corporate debt to issue today, still waiting for potentially large supply from Bank of Nova Scotia, Hewlett Packard and Capital One.

- Date $MM Issuer (Priced *, Launch #)

- 09/08 $4B #Wells Fargo $1.5B 4NC3 +62, $750M 4NC3 SOFR+88, $1.75B 11NC10 +85

- 09/08 $3B #Elevance $750M 3Y +55, $750M 7Y +85, $1B +10Y +100, $500M 30Y +105

- 09/08 $2.25B #Uber $1B +5Y +60, $1.25B 10Y +80

- 09/08 $2.05B NCL Corp $1.025B each: 5.25NC2, 8NC3

- 09/08 $2B #PIF 10Y +95

- 09/08 $2B #Home Depot $500M 3Y +30, $500M 5Y +45, $1B 10Y +63

- 09/08 $1.75B #Duke Energy $1B 10Y +95, $750M 30Y +103

- 09/08 $1.1B #Ares Strategic $600M +3Y +160, $500M +5Y +185

- 09/08 $1.1B #Equitable America $300M 2Y +50, $300M 2Y SOFR+71, $500M 7Y +93

- 09/08 $750M #Danske Bank 6NC5 +85

- 09/08 $750M #Westpac NZ 5Y +65

- 09/08 $500M #Puget Sound Energy WNG 30Y +88

- 09/08 $500M Millrose Properties 7NC3 65

- 09/08 $500M Antero Midstream 8NC3

- 09/08 $Benchmark Bank of Nova Scotia 3NC2 +55, 3NC2 SOFR+76, 6NC5 +77

- 09/08 $Benchmark Hewlett Packard 2Y +58, 3Y +70, 3Y SOFR, 5Y +85

- 09/08 $Benchmark Capital One 6NC5 +92, 11NC10 +115

- 09/08 $Benchmark Virginia Electric 10 +87, 30Y +92

MNI BONDS: EGBs-GILTS CASH CLOSE: OATs Shrug Off French Gov't Collapse

EGBs and Gilts resumed the rally that began late last week, with bull flattening seen across curves Monday.

- Core instruments got off to a steady start, largely looking through weekend Japanese political headlines (JGB curve twist steepened overnight after LDP leader Ishiba resigned).

- But the recent rally (helped by Friday's weak US employment data) soon resumed, with limited data / macro headlines to get in the way. 10Y Gilt yields fell to the lowest since Aug 14; Bund Aug 8.

- After the cash close, French PM Bayrou lost a confidence vote in parliament that triggered his resignation, with President Macron now set to name his replacement within days.

- This chain of events was entirely expected and there was no discernable reaction in OAT futures, indeed French spreads tightened on the day.

- In data, German industrial production was slightly stronger than expected.

- Gilts slightly outperformed Bunds on the day, with both curves bull flattening. Periphery/semi-core EGB spreads tightened, with OATs among the outperformers.

- We get some 2nd tier data Tuesday (including arious national-level Eurozone industrial production figures), with the week's European focus being Thursday's ECB decision - MNI's preview will be published Tuesday.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.3bps at 1.926%, 5-Yr is down 1bps at 2.209%, 10-Yr is down 2bps at 2.642%, and 30-Yr is down 3.3bps at 3.264%.

- UK: The 2-Yr yield is down 0.7bps at 3.903%, 5-Yr is down 2.5bps at 4.023%, 10-Yr is down 4.1bps at 4.605%, and 30-Yr is down 4.5bps at 5.459%.

- Italian BTP spread down 1.3bps at 82.9bps / French OAT spread down 2bps at 76.6bps

MNI FOREX: JPY Volatility in Focus, USD Index Tilts Weaker

- The Japanese yen was the main focus across G10 currency markets on Monday, following the resignation of PM Ishiba and the associated sharp initial negative reaction at the open. USDJPY gapped higher from last Friday’s close around 147.40, swiftly erasing the post payrolls decline to trade as high as 148.58. Resistance in USDJPY at 148.78, the Aug 22 high, remains intact for now.

- Thatcherite MP Sanae Takaichi is a front-runner among many opinion polls to takeover, having previously made clear her preference for easy monetary policy and a bigger role for fiscal spending - reminiscent of the Abenomics policy set from 2012 - 2020. Markets have subsequently calmed, and USDJPY tracks back towards 147.75 ahead of Tuesday’s APAC crossover.

- Overall, weaker-than-expected US employment data continues to keep the risks tilted towards the weaker dollar narrative, emphasised by the USD index spending today’s US session consolidating close to six-week lows. Associated strength in G10 has been led by the likes of AUD and NZD, while political risks in France may have contained the EURUSD price action somewhat.

- The NZDUSD (+0.65%) rally places a clear focus on 50-day EMA resistance (intersecting today at 0.5921), a breach of which would counter the most recent bearish theme. Furthermore, spot has also closed in on 0.5944, short-term trendline resistance drawn from the July 01 high. Further gains would target the August 13 high at 0.5996.

- Tuesday’s calendar will be centred around the preliminary annual payrolls benchmark revision, which is widely expected to imply large downward revisions to nonfarm payrolls growth through the twelve months to March 2025. SNB Chairman Schlegel will also participate in a fireside chat titled "Future-proofing central banks" at the BIS Innovation Summit, in Basel.

- Focus this week remains on the US inflation picture, with PPI and CPI prints due on Wednesday and Thursday respectively.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 09/09/2025 | 0645/0845 | * | Industrial Production | |

| 09/09/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 09/09/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 09/09/2025 | 1150/1350 | SNB's Schlegel at BIS fireside chat | ||

| 09/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 09/09/2025 | 1515/1615 | BOE Breeden Moderates BIS Fireside Chat | ||

| 09/09/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 10/09/2025 | 0130/0930 | *** | CPI | |

| 10/09/2025 | 0130/0930 | *** | Producer Price Index |