MNI ASIA OPEN: Tariff Uncertainty Still Driving The Outlook

MNI (NEW YORK) -

EXECUTIVE SUMMARY

- MNI INTERVIEW: Tariff Uncertainty To Drive Factory Outlook-ISM

- MNI INTERVIEW: Fed Will Face ‘Tough Calls’ In H2-Holtz-Eakin

- MNI BOC WATCH: Core Inflation Too Hot For Returning To Cut

- US DATA: Tariff Impact Courses Through Weak Manufacturing ISM Report

- US Pushes Countries For Best Offers By Wednesday As Tariff Deadline Looms (Reuters)

NEWS

US: MNI INTERVIEW: Tariff Uncertainty To Drive Factory Outlook-ISM

Uncertainty over trade policy will drag on U.S. manufacturing until at least the fourth quarter, as demand remains weak and the preemptive build-up of inventories begins to deplete, Institute of Supply Management survey chief Susan Spence told MNI on Monday. The ISM manufacturing PMI fell two-tenths to 48.5 in May, below expectations for a slight rebound to 49.2, in a third straight month of contraction after a brief two-month expansion earlier in the year. The vast majority of respondents expressed concern over tariffs even as duties on imports fell last month, Spence said.

US/TARIFFS: US Pushes Countries For Best Offers By Wednesday As Tariff Deadline Looms (Reuters)

The Trump administration wants countries to provide their best offer on trade negotiations by Wednesday as officials seek to accelerate talks with multiple partners ahead of a self-imposed deadline in just five weeks, according to a draft letter to negotiating partners viewed by Reuters.

US/TARIFFS: Trump Tariff Foes Ask Trade Court to Halt Levies for Appeal (Bloomberg)

A group of small businesses who won a ruling that most of President Donald Trump’s global tariffs are illegal want them blocked during the administration’s appeal, saying they are suffering immediate harm from economic uncertainty around the levies. In a Monday filing in the US Court of International Trade, which last week ruled that Trump exceeded his authority in imposing his broad April 2 “Liberation Day” trade levies, the group opposed the administration’s request that the tariffs remain in place during its appeal. The government has separately asked a federal appeals court for the same thing. The appellate process will likely continue for months, so a pause that long would be a win for the White House.

FED: MNI INTERVIEW: Fed Will Face ‘Tough Calls’ In H2-Holtz-Eakin

Federal Reserve officials will face a difficult choice on interest rates later this year as a significant reprieve on tariffs remains unlikely, so inflation will rise at the same time as economic growth falters, former White House economist Douglas Holtz-Eakin told MNI. Wall Street is too sanguine about the notion that the worst is over on the trade war front simply because U.S. President Donald Trump has temporarily paused some tariffs while facing legal setbacks on others, Holtz-Eakin said in an interview.

BOC: MNI BOC WATCH: Core Inflation Too Hot For Returning To Cut

Canada's central bank is seen by a majority of economists as leaving interest rates unchanged for a second meeting Wednesday after core inflation moved above the target band and growth held up in the early days of the U.S. trade war. Thirteen economists surveyed by MNI see the overnight rate staying 2.75% in a decision due at 9:45am EST on June 4, compared with eight seeing a quarter-point reduction. Several forecasters at Canada's biggest banks switched to a hold after Friday's data showing GDP grew at a 2.2% annualized pace in the first quarter, while traders made that move after a May 20 report showed the Bank's two preferred core indexes quickening past 3%.

BOE: MNI BRIEF: BOE Mann Says Can't Offset QT Impact With Rate Cut

It is not possible to simply offset the impact of quantitative tightening on financial conditions by cutting Bank Rate, Bank of England Monetary Policy Committee member Catherine Mann said. QT, which the BOE is engaged in both passively and actively, by running down and selling its gilt stock, is likely to have some tightening effect on monetary and financial conditions. A policymaker could seek to offset this through an extra rate cut, or cuts if the effect was large enough, but Mann argued against doing so.

TARIFFS/EU: MNI BRIEF: EC Retaliation On Hold Despite US Tariff Blow

The European Commission will continue to refrain from tariff retaliation against the U.S. for the moment despite President Donald Trump's decision to double tariffs on steel and aluminium to 50% over the weekend, Commission Trade Spokesperson Olof Gill said on Monday. Reaching a negotiated solution to the EU-U.S. trade dispute remains the priority, Gill said, though retaliatory measures could be announced on July 14 if not earlier should no satisfactory solution be reached in the coming weeks, Gill said.

BANXICO: MNI INTERVIEW: Banxico Should Pause, But Probably Won't-Kaiser

The Central Bank of Mexico should pause its rate-cutting cycle to reaffirm its independence and its commitment to reducing inflation, but it is more likely to keep cutting for now, former Banxico director and advisor Federico Rubli Kaiser told MNI.

CNB: MNI INTERVIEW: FinStab Changes Could Allow CNB June Cut - Kral

The Czech National Bank is likely to consider the use of macroprudential tools to slow the pace of house price growth when it meets this week, a move which ould allow it to cut rates further later this month, though its current hawkish bias means a hold is more probable, a former senior official told MNI.

POLAND (BLOOMBERG): Polish Premier Tusk Calls Vote of Confidence in His Government

Polish Prime Minister Donald Tusk said he’ll call a vote of confidence soon to shore up support for his coalition government after a candidate backed by his party was defeated in Sunday’s presidential election.

US TSYS: Light Bear Steepening To Start The Week

Treasuries gave back some of Friday's month end gains on Monday, with the cash curve lightly bear steepening.

- Yields ticked up at the open from Friday's multi-week lows, with a prevailing negative tone on US assets (weaker USD and equities) following Friday's post-close announcement by President Trump that the administration would double steel and aluminum tariffs.

- Most of the session's data was on the soft side of expectations if somewhat stagflationary, with May's ISM manufacturing below-expected (with weak sub-components, albeit prices paid in-line), and construction spending contracting again in April.

- But reaction was muted and yields would head to session highs and stay there after Atlanta Fed GDPNow for Q2 was upgraded to 4.6% (from 3.8%) and equities turned positive into the cash close. Fed speakers (Logan, Goolsbee, Powell) likewise saw no discernable reaction.

- Yields were set to close near the highs: the 2-Yr yield is up 4.3bps at 3.9407%, 5-Yr is up 5.4bps at 4.0156%, 10-Yr is up 5.9bps at 4.4596%, and 30-Yr is up 6.3bps at 4.9935%.

- Sep 10-Yr futures (TY) are down 8.5/32 at 110-15.5 (L: 110-13.5 / H: 110-30), having fallen just through Friday's lows in orderly fashion.

- Tuesday's calendar includes factory orders and JOLTS data, with an appearance by Fed's Cook among other speakers, while the week's focus is Friday's employment report for May.

OVERNIGHT DATA

US DATA: Tariff Impact Courses Through Weak Manufacturing ISM Report

The ISM Manufacturing headline PMI reading unexpectedly fell to 48.5 in May (49.5 survey, 48.7 prior), leaving it in contractionary territory for a 4th month. As the survey put it, "contraction in most of the indexes that measure demand and output have slowed, while inputs have started to weaken". Tariffs cast a heavy shadow over this stagflationary report report, impacting everything from exports to prices paid.

- New Orders ticked 0.4 points higher to 47.6, with the closely-watched (in a nonfarm payrolls survey week) Employment reading up for a 2nd consecutive month by 0.3 points to 46.8. Production rose 1.4 points to 45.4. As such there was some stability evident in the May subcategories - though these should be seen in the context of very weak recent figures (New Orders has now declined 4 consecutive months after 3 months of expansion; Production: 3 consecutive contractions after 2 months of expansion.)

- Supplier Deliveries continued to slow - considered a "positive" per the ISM survey - with the index rising 0.9 points to 56.1. Backlogs picked up 3.4 points to 47.1 but still contractionary. And on employment, the report notes "remained in contraction, as head-count reductions continued. Companies generally opted for layoffs because they are quicker to implement than attrition".

- The big drags came from trade. New Export Orders fell 3 points to 40.1 (outside of Covid, the lowest since March 2009) - and the report notes that Imports "plunged into extreme contraction", down 7.2 points to 39.9 (a 16-year low). Inventories fell 4.1 points from 50.8 prior.

- The report notes re inventories that "the pull forward of materials by companies to minimize the financial impacts of tariffs is largely completed", with Customers' inventories perhaps now a bit on the low side (44.5, down 1.7 points), potentially pointing to overall stability at weak levels.

- Prices paid were basically in line with expectations, dipping to 69.4 (69.3 survey, 69.8 prior) though still around the highest since June 2022, "driven by increases in steel and aluminum prices impacting the entire value chain, as well as the general 10-percent tariff applied to many imported goods".

US DATA: Construction Spending Suggests Deepening Private Sector Retrenchment

Construction spending looks increasingly recessionary, with the latest drop of 0.4% M/M in April representing the 3rd consecutive sequential contraction (with the readthrough exacerbated by a 0.3pp downward revision to March to -0.8%).

- Construction spending is now falling at a 4.6% 3M/3M annualized (ie quarterly) pace, which is the weakest momentum since the start of 2010. To put this into perspective, total value is lower than it was a year earlier.

- Even more worryingly, it's led by private sector construction which saw spend drop 0.7% M/M for a 3rd consecutive fall, leaving the 3M/3M annual pace at -6.9%, the poorest since 2009.

- Public sector construction is keeping the rest of the sector afloat, rising for a 4th straight month and accelerating to 3.4% 3M/3M.

- In turn, private residential (-10.7% 3M/3M) saw its first double-digit quarterly annualized drop since 2009, and private non-residential (-2.1%) was the weakest since the pandemic in 2020, with the pullback in manufacturing spending increasing.

- These figures are by value and not in volume terms, so the "real" impact is trickier to gauge. But the retrenchment looks broad-based and for residential construction in particular we see few reasons to expect a re-acceleration.

- Additionally this report provides some evidence that private sector ex-residential investment is falling, potentially owing to tariff/policy-related uncertainty, with the three largest sectors - commercial, power, and manufacturing - the biggest drags in April.

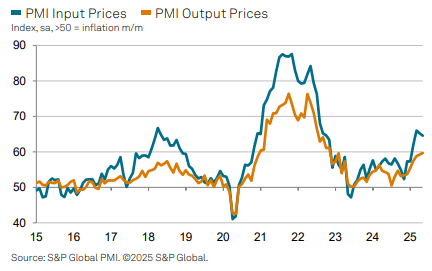

US DATA: Final Mfg PMI Sees Minor Downward Revision But Still Hot Prices

The S&P Global US manufacturing PMI was revised a little lower in the final May report but shows a similar picture to that from the flash, with activity still bolstered by front-running of tariffs amidst continued large changes in US trade policy. Manufacturing output charge inflation was trimmed a touch as well but is still strong, now the highest since Nov 2022 vs Sep 2022 with the flash.

- S&P Global US manufacturing PMI: 52.0 (cons 52.3, flash 52.3) in May final after 50.2 in April

- Press release highlights (with the full release found here):

- “Tariffs and trade policy continued to dominate the manufacturing landscape in May, according to the latest PMI survey data from S&P Global.

- Amid evidence of client efforts to front-run tariff related price increases and supply chain disruption, new orders to US manufacturers increased.

- Similar factors led to a survey record increase in stocks of inputs, whilst higher input prices due to tariffs were signaled and output charge inflation was the highest since November 2022. Delivery delays were at their most acute since October 2022.”

- The data were collected May 12-27 vs the 12-20th collection period for the flash.

US OUTLOOK/OPINION: Atlanta Fed GDPNow Rises To 4.6% For Q2

Despite soft-looking ISM Manufacturing and construction spending data this morning, the Atlanta Fed's GDPNow estimate for Q2 GDP growth picked up to 4.6% vs 3.8% Friday.

- Of the 0.8pp upgrade, about 0.2pp can be attributed to higher equipment investment and another 0.5pp to stronger PCE consumption. "The nowcasts of second-quarter real personal consumption expenditures growth and real gross private domestic investment growth increased from 3.3 percent and -1.4 percent, respectively, to 4.0 percent and 0.5 percent."

- The latest estimate is easily the highest yet for GDPNow this quarter, and would represent a very strong rebound from -0.2% in Q1. Detailed table below:

CANADA DATA: PMI Suggests Stagflationary Manufacturing Dynamics In May

The S&P Global Canada Manufacturing PMI saw a slight uptick to 46.1 in May from 45.3 prior. Despite the apparent stabilization in the headline reading, highlights from the report (link) suggest a stagflationary May for Canadian manufacturers:

- "Output and new orders both fell again, largely due to tariffs, whilst employment was reduced at the fastest rate in nearly five years. Confidence in the outlook remained subdued, and inflation rates picked up since April. Delays related to the delivery of inputs intensified and further inventory reductions were recorded."

- "Panellists widely blamed tariffs, noting an ongoing malaise in product markets with clients generally reluctant to commit to new contracts given the uncertainty of trade policies. International demand remained especially hard hit, with new export business again declining to a steeper degree than overall sales. Trade with the neighbouring United States was again reported to be weak."

- Meanwhile inflationary pressures remained acute:

- "Price data meanwhile showed an acceleration of input cost inflation. There was again evidence that tariffs had led to a general uplift in input costs, with vendors reportedly raising their charges....Overall, input price inflation was broadly in line with March’s 31-month peak. In response to rising input costs and tariff challenges, many firms saw little choice but to raise their own charges. Latest data showed a marked overall increase in output charges, despite the rate of inflation dropping to a three-month low. "

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

US TSYS/OVERNIGHT REPO: SOFR Ticks Up, Month-End Pressures To Spill Over Monday

Secured rates picked up again Friday, with SOFR up 2bp to 4.35%. That's the highest since the start of the month, with the rise at both ends of May reflecting month-end dynamics. Upside pressure is expected to persist Monday before subsiding over the rest of the week.

- Fed funds were unchanged as usual.

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.35%, 0.02%, $2641B

* Broad General Collateral Rate (BGCR): 4.34%, 0.02%, $1049B

* Tri-Party General Collateral Rate (TGCR): 4.34%, 0.02%, $1013Bd

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.33%, no change, volume: $105B

* Daily Overnight Bank Funding Rate: 4.33%, no change, volume: $228B

US TSYS/OVERNIGHT REPO: Reverse Repo Takeup More Than Reverses Month-End Jump

Overnight reverse repo takeup fell $180B Monday, the biggest drop since the start of the year ($233B on Jan 2) and more than reversing Friday's $150B jump.

- The latest level of $135.8B represents an 11-session low.

- A sharp drop-off in takeup was expected due to month-end dynamics reversing. Indeed the latest level is within the roughly $125-175B range seen in most of late April through the start of last week.

BONDS: EGBs-GILTS CASH CLOSE: Light Bear Steepening To Open Week

European curves lightly bear steepened to open the week.

- Core FI opened the week on the back foot, hitting the session's highs in mid-morning trade as weekend news was digested including Ukranian attacks on Russian military equipment and the US's announcement that it would raise tariffs on aluminium and steel to 50%.

- Also adding to the early bearish tone were EU bond suppply and Spanish manufacturing PMI coming in above expected.

- But yields would pare their rises over most of the rest of the session, as equities stabilized and US desks came in.

- In futures, rolling activity was heavy, with most Eurex contracts now around 40% through the Jun/Sep roll.

- Gilts mildly outperformed Bunds; periphery/semi-core EGB spreads traded mixed, closing off the early session wides.

- Tuesday brings Eurozone flash inflation and BOE appearances at the Parliamentary Treasury Committee, with the week's focus remaining on Thursday's ECB decision.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.3bps at 1.789%, 5-Yr is up 1.9bps at 2.083%, 10-Yr is up 2.4bps at 2.524%, and 30-Yr is up 3.2bps at 3.012%.

- UK: The 2-Yr yield is up 0.6bps at 4.029%, 5-Yr is up 1.9bps at 4.163%, 10-Yr is up 2bps at 4.667%, and 30-Yr is up 3.8bps at 5.41%.

- Italian BTP spread down 0.4bps at 97.6bps / French OAT unchanged at 66.4bps

FOREX: US Dollar Weakness Prevails, AUD & NZD Outperform

- The US dollar lost ground on Monday as markets assess the latest geopolitical concerns regarding the Russia/Ukraine conflict and tariff related developments between the US and China. The prevailing trend of greenback weakness has resumed, placing the USD Index at the lowest level for a month and narrowing the gap with the bear trigger at 97.92. The formation of a bearish engulfing daily candle on Thursday last week adds to the S/T downside focus.

- An extension of dollar weakness was seen following a below-expectation ISM manufacturing print, however, the subsequent stabilisation for equity markets allowed the DXY (-0.50%) to moderately recover from its worst levels.

- Despite the initial pessimistic tone for broader risk sentiment, AUD, NZD and NOK are the best performing currencies to start the week. AUDUSD received support in the low 0.6400s last week keeping bullish trend signals intact. A continuation higher would open 0.6550, a Fibonacci retracement, and the November 25 high. Above here, the key medium-term focus is on the US election related highs at 0.6688.

- In similar vein, a 1% rise during today’s session has prompted NZDUSD to return to an important zone of resistance between 0.6025/40. A close at current levels would be the highest since the US election, signalling scope for a more protracted recovery towards 0.6168, the 76.4% retracement of the Sep ’24 – Apr ’25 selloff.

- USDJPY extended its pullback from last Thursday’s 146.28 high, and spot now trades back below 143.00. A continuation lower would expose 142.12, the May 27 low. Clearance of this level would resume the bear leg and signal scope for a move towards a key medium-term pivot around the 140.00 mark.

- RBA minutes kick off Tuesday’s economic calendar, before Swiss and Eurozone inflation data. JOLTS job openings will headline the US session. Bank of Japan Governor Ueda is due to speak at the Research Institute of Japan, in Tokyo.

DATA/EVENTS CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 03/06/2025 | 0130/1130 | Business Indicators | ||

| 03/06/2025 | 0130/1130 | Balance of Payments: Current Account | ||

| 03/06/2025 | 0145/0945 | ** | S&P Global Final China Manufacturing PMI | |

| 03/06/2025 | 0630/0830 | *** | CPI | |

| 03/06/2025 | 0700/0300 | * | Turkey CPI | |

| 03/06/2025 | 0900/1100 | *** | HICP (p) | |

| 03/06/2025 | 0900/1100 | ** | Unemployment | |

| 03/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 03/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 03/06/2025 | 0915/1015 | BOE Bailey, Breeden, Dhingra, Mann At TSC | ||

| 03/06/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 03/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 03/06/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/06/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 03/06/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 03/06/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/06/2025 | 1645/1245 | Chicago Fed's Austan Goolsbee | ||

| 03/06/2025 | 1700/1300 | Fed Governor Lisa Cook | ||

| 03/06/2025 | 1930/1530 | Dallas Fed's Lorie Logan | ||

| 04/06/2025 | 2300/0900 | * | S&P Global Final Australia Services PMI | |

| 04/06/2025 | 2300/0900 | ** | S&P Global Final Australia Composite PMI | |

| 04/06/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 04/06/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 04/06/2025 | 0130/1130 | *** | Quarterly GDP |