MNI ASIA OPEN: Soft US/Canada Data Supports Early Treasury Bid

EXECUTIVE SUMMARY

- MNI SECURITY: EU's Costa Vows Support For Kyiv As Slovak PM Dissents

- MNI EU-RUSSIA: Kallas Echoes VdL Saying 19th Sanctions Package Coming In September

- MNI SECURITY: Russia Foreign Minister Vague On Trump-Backed Putin-Zelenskyy Meeting

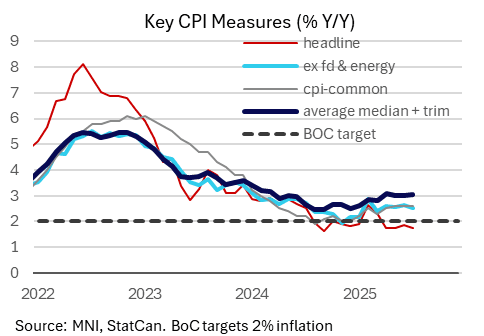

- MNI CANADA DATA: July CPI Aggregates Come In On Soft Side

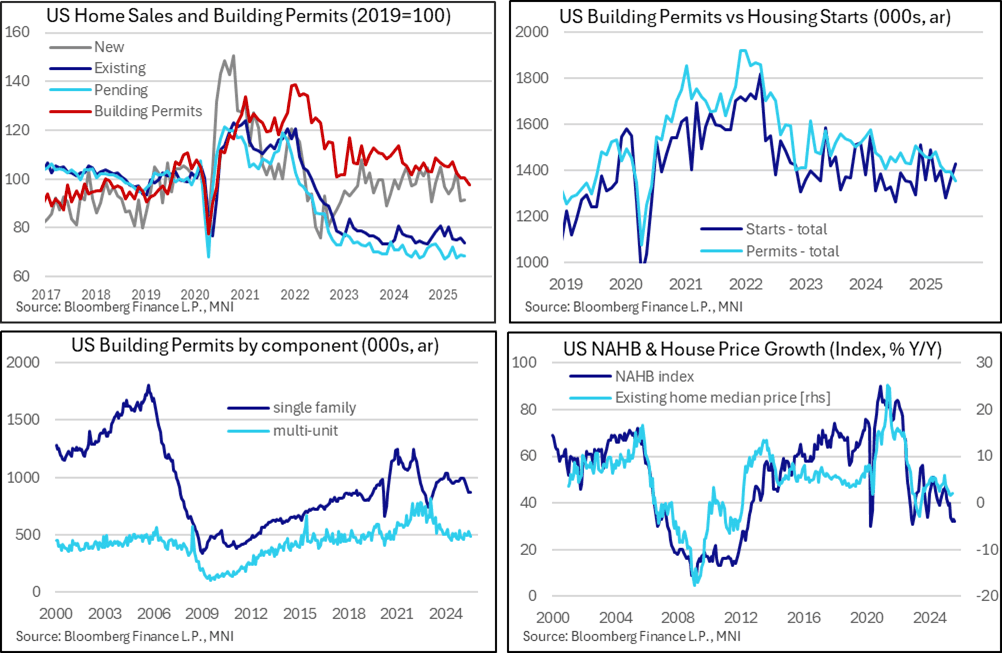

- MNI US DATA: Building Permits Downtrend Continues

NEWS

MNI SECURITY: EU's Costa Vows Support For Kyiv As Slovak PM Dissents

European Council President Antonio Costa posts on X following the conclusion of an extraordinary European Council videoconference and a call with Ukrainian President Volodymyr Zelenskyy. Costa: "I underlined the EU’s unity and unwavering support for Ukraine, as well as our commitment to maintaining pressure on Russia."

MNI EU-RUSSIA: Kallas Echoes VdL Saying 19th Sanctions Package Coming In September

European Commission High Representative for Foreign Affairs and Security Policy Kaja Kallas posts on X regarding today's European Council summit call on Ukraine and the prospect of further EU sanctions on Russia. Kallas: "...Putin cannot be trusted to honour any promise or commitment. Therefore, security guarantees must be strong and credible enough to deter Russia from re-grouping and re-attacking."

MNI SECURITY: US-EUR-UKR To Work On Security Architecture In Coming Days - Axios

Axios reports that the US, Ukraine, and European countries are expected to work together “in the coming days” on a detailed proposal for security guarantees for Ukraine, “likely involving US air power,” according to two sources with knowledge of the discussions.

MNI SECURITY: Russia Foreign Minister Vague On Trump-Backed Putin-Zelenskyy Meeting

Speaking to Russia-24 TV, Foreign Minister Sergey Lavrov says that "Russia does not reject any formats to discuss the peace process in Ukraine", but adds "any contacts of [national] leaders should be prepared thoroughly," hardly a firm commitment to talks taking place. Lavrov's comments come after the high-profile White House summit where leaders, including US President Donald Trump, called for a meeting between Russian President Vladimir Putin and Zelenskyy.

MNI ISRAEL: PMO Demands Release Of All Hostages Before Gaza Ceasefire

Channel 12 reports comments from the prime minister's office regarding the Hamas response to the latest ceasefire proposal. Says that the Israeli requirements to end the conflict have always been clear, and that is the release of all 50 hostages (20 of whom are believed to still be alive) held by Hamas.

US TSYS

MNI US TSYS: Early Support From Soft US Build Permits & Canadian CPI Data

- Treasuries look to finish near late Tuesday session highs (TYU5 +8.5 at 111-25), curves bull flattening with bonds outperforming (2s10s -2.245 at 54.607, 5s30s -.571 at 107.952).

- Rates rebounded after this morning's data - lower than expected build permits outweighing higher than expected housing starts, while softer Canadian CPI aggregates added to support.

- Housing starts were far stronger than expected in July at 1428k (saar, cons 1297k) after an upward revised 1358k (initial 1321k) in June. It left starts rising 5.2% M/M (cons -1.8%) after a stronger than first thought 5.9% (initial 4.6%) as they bounced after a -8.3% M/M decline in May (also revised from -9.7%).

- Canadian all-items CPI rose 1.73% Y/Y unrounded (1.86% prior, 1.8% expected by MNI median), and 0.12% M/M (0.18% prior, 0.4% expected).

- US$ rising to one week highs, price action was assisted by a dip lower for the major equity benchmarks, as a cautious risk off mood prevails given the lack of progress regarding a Russia/Ukraine ceasefire and the notable weakness for tech stocks in the US.

- Stocks in retreat (Nasdaq -323.04 at 21306.66) ahead of Wednesday's July FOMC minutes not to mention Friday's annual economic symposium in Jackson Hole Wyoming.

OVERNIGHT DATA

MNI US DATA: Building Permits Downtrend Continues

Housing starts and building permits data for July offered firmly conflicting signs of housing activity, but with the less weather-sensitive permits series pointing to a clearer downtrend that chimes more closely with dour NAHB homebuilder sentiment.

- Housing starts were far stronger than expected in July at 1428k (saar, cons 1297k) after an upward revised 1358k (initial 1321k) in June. It left starts rising 5.2% M/M (cons -1.8%) after a stronger than first thought 5.9% (initial 4.6%) as they bounced after a -8.3% M/M decline in May (also revised from -9.7%).

- This series continues to be heavily driven by multi-units, which increased 10% M/M after 34% in June and -26% in May. Single family starts meanwhile increased 2.8% M/M after -3.8% and 0.1%.

- However, building permits are less volatile, not least because they are more resilient to weather changes, and these disappointed as they continued to show a clear downtrend, slipping to 1354k (saar, cons 1386k) in preliminary July data after 1393k in June.

MNI CANADA DATA: July CPI Aggregates Come In On Soft Side

The major July Canadian CPI aggregates came in on the soft side, with some signs that underlying inflation momentum has peaked. All-items CPI rose 1.73% Y/Y unrounded (1.86% prior, 1.8% expected by MNI median), and 0.12% M/M (0.18% prior, 0.4% expected). It's the 4th consecutive month headline has printed below 2.0% Y/Y, while ex-food/energy Y/Y dipped to a 5-month low 2.50% (2.64% prior).

- The key trim/median readings came out roughly in line too, with trim at 3.00% Y/Y and median 3.10% for an average 3.05%. Technically this marked the highest since April because the June figures were downwardly revised (Median to 3.00%, making the average 3.00% instead of 3.05% - seasonally-adjusted figures like this can be revised on a month-to-month basis by StatCan).

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 35.79 points (-0.08%) at 44876.54

S&P E-Mini Future down 41 points (-0.63%) at 6428.5

Nasdaq down 312.4 points (-1.4%) at 21317.84

US 10-Yr yield is down 3.3 bps at 4.3004%

US Sep 10-Yr futures are up 8/32 at 111-24.5

EURUSD down 0.0014 (-0.12%) at 1.1647

USDJPY down 0.38 (-0.26%) at 147.51

WTI Crude Oil (front-month) down $0.83 (-1.31%) at $62.59

Gold is down $16.22 (-0.49%) at $3316.40

European bourses closing levels:

EuroStoxx 50 up 48.64 points (0.9%) at 5483.28

FTSE 100 up 31.48 points (0.34%) at 9189.22

German DAX up 108.3 points (0.45%) at 24423.07

French CAC 40 up 95.03 points (1.21%) at 7979.08

US TREASURY FUTURES CLOSE

3M10Y -0.759, 9.167 (L: 8.195 / H: 11.644)

2Y10Y -2.035, 54.817 (L: 54.382 / H: 57.457)

2Y30Y -1.781, 115.08 (L: 114.349 / H: 117.594)

5Y30Y -0.47, 108.053 (L: 107.675 / H: 109.172)

Current futures levels:

Sep 2-Yr futures up 1.375/32 at 103-26.625 (L: 103-25 / H: 103-27.125)

Sep 5-Yr futures up 4.75/32 at 108-24.75 (L: 108-19.5 / H: 108-25.25)

Sep 10-Yr futures up 8/32 at 111-24.5 (L: 111-15 / H: 111-26)

Sep 30-Yr futures up 19/32 at 114-12 (L: 113-21 / H: 114-13)

Sep Ultra futures up 25/32 at 117-4 (L: 116-07 / H: 117-07)

MNI US 10YR FUTURE TECHS: (U5) Monitoring Support

- RES 4: 113-23 76.4% retracement of the Sep’24 - Jan’25 sell-off

- RES 3: 113-07 76.4% retracement of the Apr 7 - 11 sell-off

- RES 2: 112-23 High May 1

- RES 1: 112-15+ High Aug 5

- PRICE: 111-25+ @ 1400 ET Aug 19

- SUP 1: 111-10+ 50-day EMA

- SUP 2: 110-23+/08+ Low Aug 1 / Low Jul 15 & 16

- SUP 3: 110-03 76.4% retracement of the May 22 - Jul 1 bull leg

- SUP 4: 109-28 Low Jun 6 and 11

The underlying bullish theme in Treasury futures remains intact, supported by the recent clearance of 112-12+, the Jul 1 high. Short-term weakness is considered corrective. A resumption of gains would open 112-23, the May 1 high and the next important resistance. Above 112-23, retracement levels are layered between 113-07 and 113-23. Key support is 110-08+, the low on Jul 15 and 16. First key support is yet to be tested at 110-23+, the Aug 1 low.

SOFR FUTURES CLOSE

Sep 25 +0.013 at 95.905

Dec 25 +0.015 at 96.210

Mar 26 +0.025 at 96.435

Jun 26 +0.025 at 96.655

Red Pack (Sep 26-Jun 27) +0.015 to +0.020

Green Pack (Sep 27-Jun 28) +0.025 to +0.040

Blue Pack (Sep 28-Jun 29) +0.045 to +0.050

Gold Pack (Sep 29-Jun 30) +0.050 to +0.055

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.34% (-0.02), volume: $2.810T

- Broad General Collateral Rate (BGCR): 4.33% (-0.01), volume: $1.159T

- Tri-Party General Collateral Rate (TCR): 4.33% (-0.01), volume: $1.134T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $112B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $244B

FED Reverse Repo Operation

RRP usage retreats to $22.344B this afternoon (lowest since April 5, 2021) from $38.240B yesterday, total number of counterparties at 29.

MNI PIPELINE: Corporate Bond Update: $15.9B to Price Tuesday

- Date $MM Issuer (Priced *, Launch #)

- 08/19 $5B *IBRD (World Bank) 10Y SOFR+60

- 08/19 $4B *EIB 5Y SOFR+39

- 08/19 $1.25B #Allianz Perp-NC8.7 6.55%

- 08/19 $1B #DBJ 3Y SOFR+50

- 08/19 $1B #MetLife $600M 3Y +45, $400M 3Y SOFR+70

- 08/19 $750M #CCDJ 5Y +75

- 08/19 $700M #National Rural Utilities 3Y +48

- 08/19 $600M #Pricoa Global Funding 7Y +73

- 08/19 $600M #MassMutual 10Y +78

- 08/19 $500M #Hanover Insurance 10Y +120

- 08/19 $500M #American National Grp 30NC5 7%

- Expected Wednesday:

- 08/20 $Benchmark British Colombia 5Y SOFR+56

- 08/20 $Benchmark ADB 5Y SOFR+42a

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Underperform Again Pre-UK CPI

European curves flattened Tuesday, with Gilts underperforming yet again ahead of UK CPI data.

- With no evident catalysts today amid a thin data/speaker slate, Monday's weakness in Gilts on the back of lingering fiscal concerns spilled over into today's session. 10Y Gilt yields hit a fresh post-May high (4.756%) in early trade.

- Bund yields traded almost entirely within the prior session's ranges, with the 2.80% level holding for the 10Y. Longer-end German instruments led the space overall in a broader rally over the most of the remainder of the session, with Buxl rallying after yields hit a fresh post-2011 high.

- Yields fell to session lows a little over an hour before the cash close, as equities tumbled (led by US megacap tech), resulting in a modest safe-haven bid that also saw periphery EGB spreads move a little wider.

- The German curve bull flattened on the day, with the UK's twist flattening. Periphery/semi-core EGB spreads closed mixed, with BTPs underperforming.

- Attention Wednesday will be on the UK CPI report. MNI's preview is here: the BOE MPC is focused on headline CPI which is expected to come in higher than in June.

- We also get an appearance by ECB's Lagarde and the Swedish Riksbank decision, as well as final Eurozone July inflation.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.1bps at 1.958%, 5-Yr is down 1.3bps at 2.306%, 10-Yr is down 1.3bps at 2.75%, and 30-Yr is down 1.5bps at 3.323%.

- UK: The 2-Yr yield is up 1.5bps at 3.98%, 5-Yr is up 1.5bps at 4.138%, 10-Yr is up 0.2bps at 4.74%, and 30-Yr is down 0.9bps at 5.602%.

- Italian BTP spread up 1.2bps at 80.5bps / French OAT down 0.1bps at 68.3bps

MNI FOREX: CAD Weakens Post CPI, Softer Equities Weigh on AUD & NZD

- Despite some initial weakness on Tuesday, the USD index tilted back into positive territory late in the session, set to moderately extend the rally this week. Price action was assisted by a dip lower for the major equity benchmarks, as a cautious risk off mood prevails given the lack of progress regarding a Russia/Ukraine ceasefire and the notable weakness for tech stocks in the US.

- Canada inflation data came in slightly below expectations and while unlikely to prompt renewed easing from the BOC, the Canadian dollar has sold off today. USDCAD has risen 0.4% to 1.3860, closing in on the August 01 highs off 1.3879. A break of this level would cancel a bear threat and resume the recent bull cycle.

- Elsewhere, risk dynamics have negatively impacted the likes of AUD and NZD, while Norwegian Krone is at the bottom of the G10 leaderboard.

- For AUDUSD, the pair is comfortably off its most recent highs but continues to trade in a range. From a trend perspective, the condition remains bullish highlighted by MA studies that remain in a bull-mode position; however, spot has narrowed the gap substantially to key support at 0.6419, the Aug 1 low.

- Kiwi weakness is notable ahead of Wednesday’s RBNZ decision, recording the first print below 0.5900 in two weeks. With a 25bp cut widely forecast, attention will be on the revised RBNZ outlook and tone of the statement and press conference. The focus is likely to be on the projected OCR path and whether it is revised lower suggesting further easing towards stimulatory territory as excess capacity persists.

- GBPUSD has consolidated around the 1.35 mark on Tuesday amid gilts paring some of yesterday's weakness. A technical bull cycle remains intact, keeping sights on 1.3636, the 76.4% retracement of the bear leg between Jul 1 and Aug 1 ahead of tomorrow's UK CPI release.

- FOMC minutes are also due for release tomorrow before the Jackson Hole symposium kicks off Thursday.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 20/08/2025 | 0600/0700 | *** | Consumer inflation report | |

| 20/08/2025 | 0600/0800 | ** | PPI | |

| 20/08/2025 | 0710/0910 | ECB Lagarde at WEF Intl Business Council | ||

| 20/08/2025 | 0730/0930 | *** | Riksbank Interest Rate Decison | |

| 20/08/2025 | 0900/1100 | *** | HICP (f) | |

| 20/08/2025 | 0900/1100 | Q2 Flash Vacancies and Labour Cost Index | ||

| 20/08/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 20/08/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 20/08/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 20/08/2025 | 1500/1100 | Fed Governor Christopher Waller | ||

| 20/08/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 20/08/2025 | 1800/1400 | FOMC Minutes | ||

| 20/08/2025 | 1900/1500 | Atlanta Fed's Raphael Bostic | ||

| 21/08/2025 | 2300/0900 | *** | Judo Bank Flash Australia PMI | |

| 21/08/2025 | 0030/0930 | ** | Jibun Bank Flash Japan PMI |