MNI ASIA OPEN: Pres Trump to Interview Gov Waller for Chairman

EXECUTIVE SUMMARY

- MNI US DATA: AHE A Mixed Bag Rather Than A Clear Miss In Two-Month Update

- MNI US DATA: Unemployment Rate Jump Driven By Prime Joblessness, But Caveats Abound

- MNI US DATA: Higher-Than-Usual Uncertainty Over Unemployment Rate Clouds Signal

- MNI EU: No Sign Of Agreement On Use Of Frozen Russian Assets Pre-EUCO

- MNI US DATA: Core Retail Sales Maintained Strong Momentum At Start Of Q4

US

WSJ: Trump Set to Interview Fed's Christopher Waller for Chair -- President Trump is set to interview Fed governor Christopher Waller for Federal Reserve chair on Wednesday, according to people familiar with the matter.

NEWS

MNI GLOBAL: WSJ Headlines on Panama Ports Deal and US/China Trade Talks

The Wall Street Journal have published an article indicating that the White House consider China's new demand regarding a Panama Ports deal as unacceptable.

- "President Trump's push to loosen China's influence in the Panama Canal has hit a wall now that Beijing is demanding that China's largest shipping company get a controlling stake in a deal to sell dozens of ports to a BlackRock-led group."

MNI EU: No Sign Of Agreement On Use Of Frozen Russian Assets Pre-EUCO

The chances of an agreement being reached within the EU on the use of frozen Russian assets held in the Union to fund 'reparations loans' for Ukraine in time for sign-off at the 18 Dec EUCO summit appear to have evaporated. On 15 Dec, Belgium once again rejected Commission overtures regarding legal and financial guarantees. EU ambassadors meet today to further discuss the plans.

MNI FRANCE: National Assembly Set To Pass Social Security Budget This Evening

The National Assembly has begun its final reading of the draft Social Security Bill (PLFSS), ahead of its expected passage later this evening. The far-left La France Insoumise (LFI, 'France Unbowed) tabled a motion to reject the bill outright at the start of the session, but this was in turn rejected. In the previous vote that sent the PLFSS to the Senate, lawmakers voted by a margin of 247 to 234 in favour of the bill.

Bloomberg: "BESSENT: WILL SHRINK BUDGET GAP SEVERAL HUNDRED BLN USD THIS YR .. PLENTY OF REVENUE ALTERNATIVES TO IEEPA TARIFFS"

Reuters: "JOINT STATEMENT OF 8 EU STATES IN FINLAND: RUSSIA IS THE MOST SIGNIFICANT, DIRECT AND LONG-TERM THREAT TO OUR SECURITY AND TO PEACE AND STABILITY IN THE EURO-ATLANTIC AREA."

US TSYS

MNI US TSYS: Back Near Highs After Rejecting Post-NFP Gap Bid

- Treasuries look to finish moderately higher, off post data highs as focus turned away from this morning's 4.6% unemployment rate with possible assistance from that heavy -105k in Oct NFP.

- Rounding and already known higher survey error saw Treasuries extend lows soon after, 10Y yield rising to 4.1939% high while the 2s10s curve climbed to new/near 4Y high of 69.086 - only to retreat to 66.624 after the bell.

- Retail sales growth was flat in October after rising 0.1% prior, a little softer than the expected 0.1% gain - core sales were significantly stronger than expected, implying strong retail momentum at the start of Q4.

- TYH6 currently trades 112-17 (+8) vs. 112-06 low / 112-22.5 high. Curves mildly flatter: 2s10s -.045 at 66.624 after climbing to new - near 4Y high of 69.086 this morning.

- US dollar index pullback to 97.87, the lowest level since October 03. However, the slightly messy release and associated uncertainty surrounding DOGE deferred resignations saw the Greenback rebound to 98.15.

- No Fed speakers during the session, Chicago Fed Pre Goolsbee will appear on CNN at 1600ET. Focus on Wednesday: several regional Fed economic measures, Fed speakers (Waller, Williams, Bostic) and $13B 20Y Bond re-open (912810UQ9).

OVERNIGHT DATA

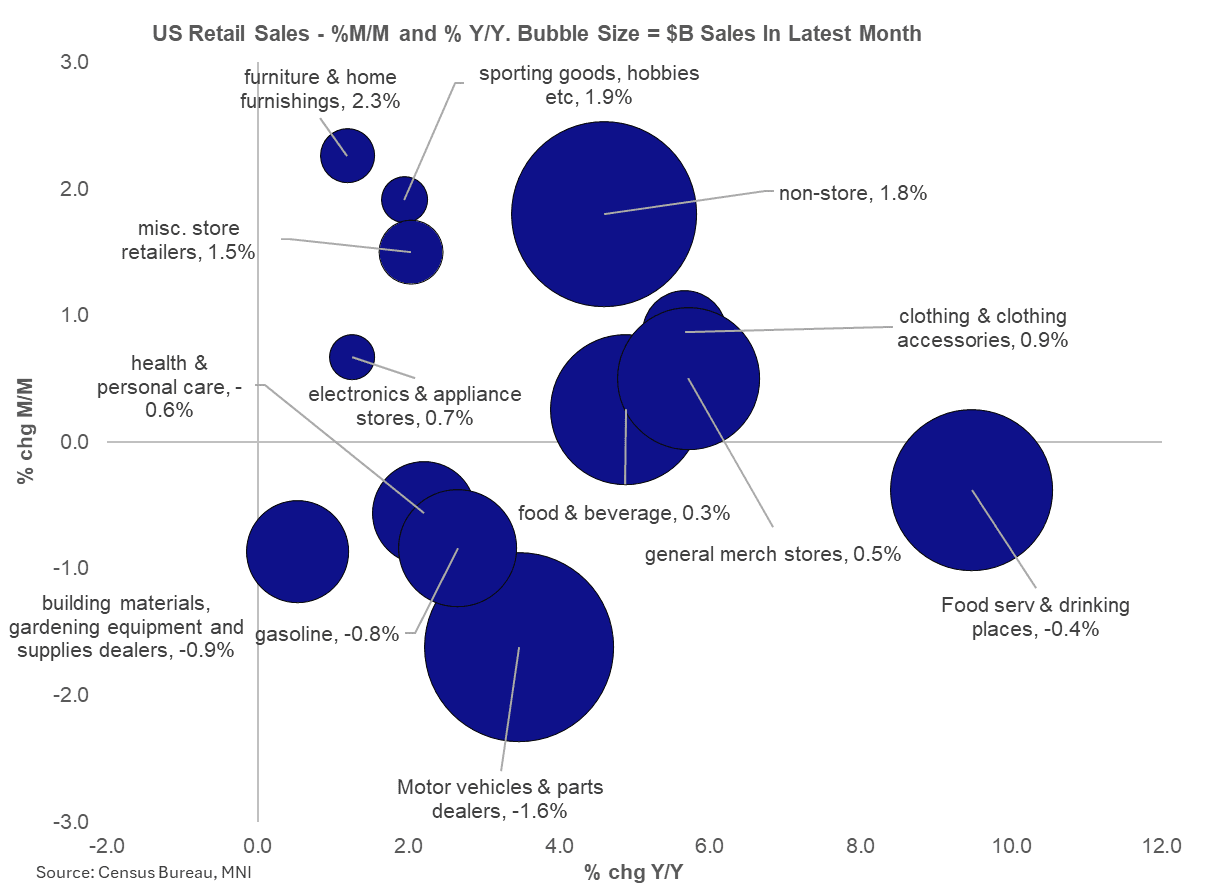

MNI US DATA: Core Retail Sales Maintained Strong Momentum At Start Of Q4

Retail sales growth was flat in October after rising 0.1% prior, a little softer than the expected 0.1% gain - but core sales were significantly stronger than expected, implying strong retail momentum at the start of Q4.

- The Census Bureau's delayed report showed Control retail sales grew at the fastest monthly pace since June in October, with a 0.85% M/M gain (0.4% consensus) more than reversing September's unexpectedly poor -0.09%. Overall ex-autos sales grew by 0.4% (0.1% prior; 0.2% consensus), with ex-autos/gas up 0.5% (just under 0.0% prior, 0.4% consensus).

- The headline/core divergence was widely expected on account of soft gasoline (7-month worst -0.8% M/M) and auto (6-month worst -1.7%) sales, neither of which are included in the Control Group.

MNI US DATA: Broad-Based Softening, Higher Prices Signaled By December Flash PMIs

Some highlights from the S&P Global flash December PMIs which were slightly below-expected (Manufacturing 51.8 vs 52.1 consensus and 52.2 prior; Services 52.9 vs 54.0 consensus and 54.1 prior):

MNI US DATA: Higher-Than-Usual Uncertainty Over Unemployment Rate Clouds Signal

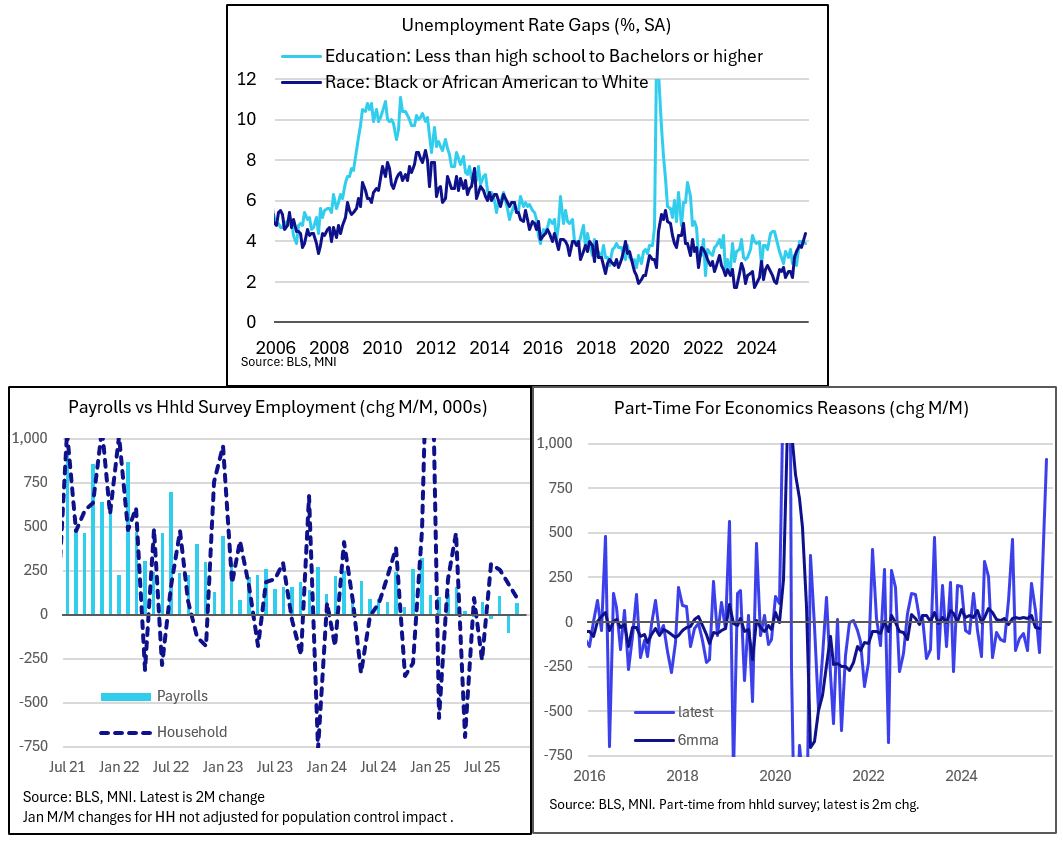

Going back to other weak/mixed notes from November's Household Survey: Those working part-time for economic reasons rose 909k over the 2 months to November, easily the highest for a 2-month period since the pandemic (the preceding 8-month average had been +13k), though we'd guess this is at least partly related to the federal government shutdown.

- And the demographic breakdown was extremely mixed, suggesting potential quirks driven by the unusual survey: White unemployment ticked up 0.1pp to 3.9% and fell 0.8pp for Asian (3.6%) and 0.5pp for Hispanic/Latino Americans (5.0%), but the Black/African American rate jumped 0.8pp to 8.3%.

MNI US DATA: NY Fed Services Activity Stays Weak At Year-End, With Prices A Concern

The New York Fed's monthly regional services firm (aka "Business Leaders") survey showed continued weak activity in December, with a notable pickup in price pressures. As the first of the monthly regional Fed services surveys, as with the prior day's Empire manufacturing report, it suggested little cause for cheer over economic developments at end-year.

- The general activity index ticked up to -20.0 from -21.7, but this is firmly negative and little changed over the last 4 months (the report describes the upshot as "activity continued to decline significantly"). Likewise, the business climate index at -44.2 (-42.2 prior) remained sub -40 for a 4th consecutive month, though the latest reading was narrowly a 6-month worst.

MNI US DATA: Redbook Retail Sales Show Continued Momentum Toward End-Year

Moving beyond the release of the delayed Census Bureau retail sales report that showed strong activity in October, the Johnson Redbook Retail Sales Index posted gains of 6.2% Y/Y in the week ending December 13, an acceleration from 5.9% in the prior week. That brought month-to-date sales to 5.9%, which coming off a 6.4% gain in November suggests that retail momentum continued through the latter 2 months of Q4.

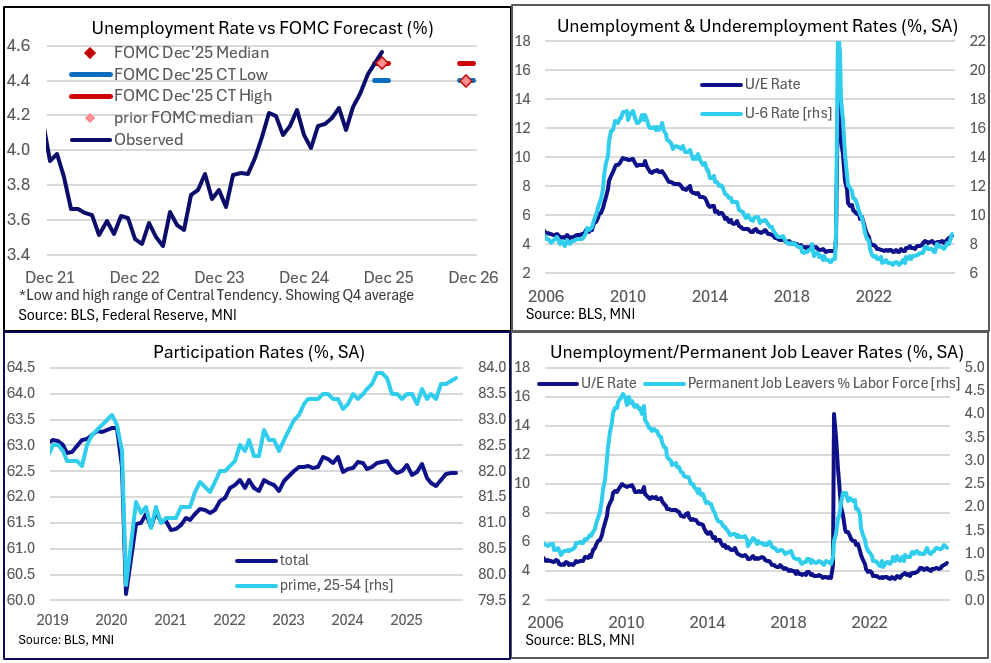

MNI US DATA: Unemployment Rate Jump Driven By Prime Joblessness, But Caveats Abound

The rise in the unemployment rate to 4.56% unrounded in November from 4.44% in September represented a higher-than-expected reading and a fresh high for joblessness since September 2021. Analyst median consensus was 4.5%, with many more leaning toward 4.4% unrounded than 4.6% - and while the interpolated 0.06pp average monthly increase implies a slower pace of rises vs the preceding 3 months, this puts the U/E rate on track for an overshoot of the FOMC's 4.5% median expectation for Q4.

MNI US DATA: Government Leads Both October Payrolls Weakness And Downward Revisions

Nonfarm payrolls growth was a little better than expected in November at 64k (cons 50k) but it was more than offset by a weaker than expected -105k in October (we’d seen a median estimate of -25k). However, private payrolls were on balance very close to expectations, at 69k (cons 50k) in Nov after 52k (cons 65k, again from the median in the MNI preview).

- Indeed, public payrolls fell -5k in Nov after slumping -157k in Oct (likely on DOGE deferred resignations with all analysts we’d seen expecting a smaller hit than the circa -150k in press reports earlier in the year)

- Nonfarm payrolls were revised down a combined -33k in Sep (-11k) and Aug (-22k)

- Private payrolls were revised down only -1k, with Sep (+7k) and Aug (-8k)

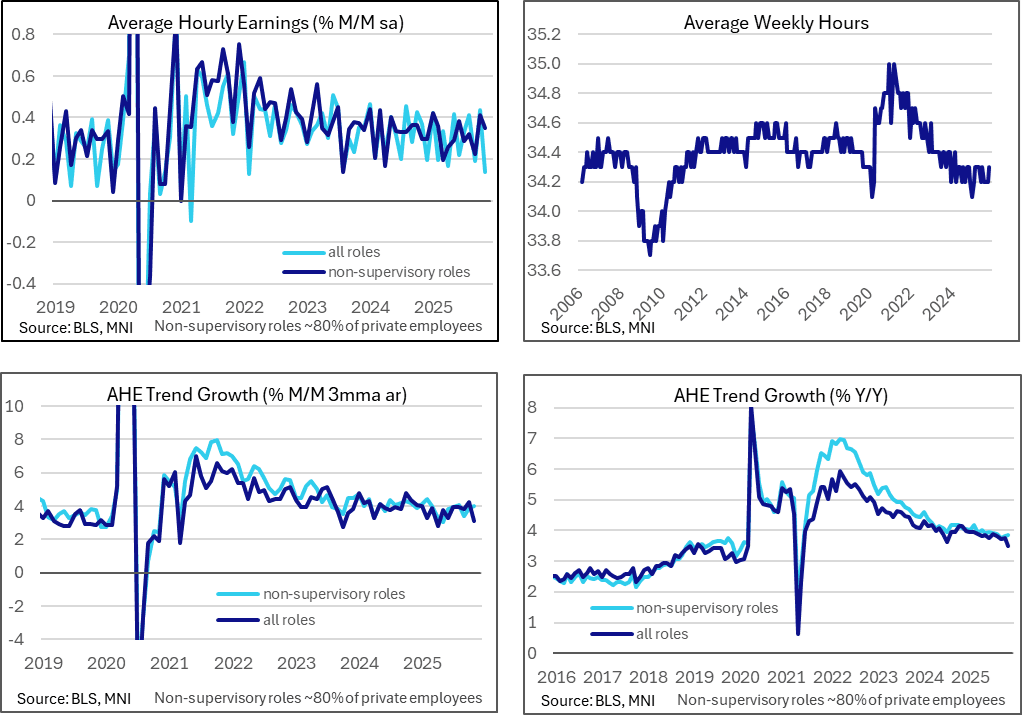

MNI US DATA: AHE A Mixed Bag Rather Than A Clear Miss In Two-Month Update

The two months of average hourly earnings data were a mixed bag rather than the outright weakness that the headlines suggest, with non-supervisory employee wage growth running firmer and hours worked also increasing in November.

- Overall AHE growth of 0.14% M/M in November was clearly softer than the 0.3% M/M widely expected although it was countered by a stronger than expected 0.44% M/M in Oct (we had seen limited estimates with a median 0.3 but with risks skewed lower). Still, September was also revised lower to 0.19% M/M vs the previously estimated 0.25% M/M. The combination meant the Y/Y rate surprised lower, with 3.51% Y/Y (cons 3.6) after 3.75% in Oct for a fresh low since May 2021.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 263.32 points (-0.54%) at 48158.98

S&P E-Mini Future down 16.75 points (-0.24%) at 6865

Nasdaq up 77 points (0.3%) at 23136.9

US 10-Yr yield is down 2.7 bps at 4.145%

US Mar 10-Yr futures are up 8/32 at 112-17

EURUSD down 0.0004 (-0.03%) at 1.1748

USDJPY down 0.46 (-0.3%) at 154.77

WTI Crude Oil (front-month) down $1.64 (-2.89%) at $55.17

Gold is down $1.46 (-0.03%) at $4303.94

European bourses closing levels:

EuroStoxx 50 down 34.69 points (-0.6%) at 5717.83

FTSE 100 down 66.52 points (-0.68%) at 9684.79

German DAX down 153.04 points (-0.63%) at 24076.87

French CAC 40 down 18.72 points (-0.23%) at 8106.16

US TREASURY FUTURES CLOSE

Curve update:

3M10Y -2.433, 52.05 (L: 49.721 / H: 55.97)

2Y10Y -0.449, 66.22 (L: 65.262 / H: 69.086)

2Y30Y -0.976, 133.325 (L: 130.914 / H: 137.1)

5Y30Y +0.266, 112.319 (L: 110.182 / H: 114.524)

Current futures levels:

Mar 2-Yr futures up 1.625/32 at 104-12.75 (L: 104-10.875 / H: 104-15)

Mar 5-Yr futures up 5.75/32 at 109-11.5 (L: 109-04.75 / H: 109-15)

Mar 10-Yr futures up 8/32 at 112-17 (L: 112-06 / H: 112-22.5)

Mar 30-Yr futures up 18/32 at 115-14 (L: 114-17 / H: 115-15)

Mar Ultra futures up 19/32 at 118-6 (L: 117-06 / H: 118-10)

MNI US 10YR FUTURE TECHS: (H6) Bearish Outlook

- RES 4: 113-09 76.4% retracement of the Nov 25 - Dec 10 bear leg

- RES 3: 113-00+ 61.8% retracement of the Nov 25 - Dec 10 bear leg

- RES 2: 112-27+ High Dec 5

- RES 1: 112-23 High Dec 11

- PRICE: 112-11+ @ 13:50 GMT Dec 16

- SUP 1: 111-29 Low Dec 10 and the bear trigger

- SUP 2: 111-19 1.236 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 3: 111-11 1.382 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 4: 111-00 Round number support

A bear theme in Treasuries remains intact. Today’s volatile activity resulted in a brief test above the 20-day EMA, at 112-20. The outlook remains bearish. A continuation lower would refocus attention on key support at 111-29, the Dec 10 low. Clearance of this level would confirm a resumption of the bear leg and open 111-19, a Fibonacci projection. On the upside, a clear breach of 112-23, the Dec 12 high would strengthen a S/T bull cycle.

SOFR FUTURES CLOSE

Current White pack (Dec 25-Sep 26):

Dec 25 steady00 at 96.293

Mar 26 +0.010 at 96.480

Jun 26 +0.005 at 96.690

Sep 26 +0.020 at 96.850

Red Pack (Dec 26-Sep 27) +0.025 to +0.045

Green Pack (Dec 27-Sep 28) +0.040 to +0.050

Blue Pack (Dec 28-Sep 29) +0.035 to +0.040

Gold Pack (Dec 29-Sep 30) +0.020 to +0.030

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.75% (+0.08), volume: $3.270T

- Broad General Collateral Rate (BGCR): 3.73% (+0.08), volume: $1.315T

- Tri-Party General Collateral Rate (TCR): 3.73% (+0.08), volume: $1.288T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $97B

- Daily Overnight Bank Funding Rate: 3.64% (+0.00), volume: $167B

FED Reverse Repo Operation

RRP usage recedes to $1.554B with counterparties falling to 2 this afternoon, vs. Monday's $2.601B. Compares to last Thursday's $0.838B (lowest level since mid-March 2021); this years highest excess liquidity measure: $460.731B on June 30.

PIPELINE

No new US$ corporate bond issuance Tuesday

MNI EGB BONDS: EGBs-GILTS CASH CLOSE: Gilts Underperform On UK PMIs, Wage Growth

EGB yields dipped Tuesday amid mixed global labor market and activity data, but Gilts weakened.

- Slightly weaker-than-expected Eurozone December flash PMIs had little impact on core EGBs. In the UK however Gilts were kept on the back foot amid a firm PMI print and labour market data that showed higher-than-expected earnings growth.

- The delayed US nonfarm payrolls report was initially seen as weak due to a sizeable unemployment rate rise, but the move fully reversed in part due to strong US retail sales alongside, and saw Gilts and Bunds yields hit session highs.

- Yields were content to come off of the lows into the cash close, ahead of Wednesday's UK CPI release and Thursday's ECB / BoE decisions.

- On the day, the German curve bull steepened slightly, with the UK's bear steepening. Periphery/semi-core EGB spreads fell modestly.

- Aside from UK CPI (MNI's preview here), German IFO and Eurozone final November inflation data feature Wednesday.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.6bps at 2.134%, 5-Yr is down 1.7bps at 2.452%, 10-Yr is down 0.8bps at 2.845%, and 30-Yr is down 0.6bps at 3.466%.

- UK: The 2-Yr yield is up 1.2bps at 3.766%, 5-Yr is up 1.3bps at 3.96%, 10-Yr is up 2.2bps at 4.518%, and 30-Yr is up 1.9bps at 5.258%.

- Spanish bond spread down 1.2bps at 43.6bps / French OAT down 0.4bps at 70.5bps

MNI FOREX: Dollar Index Ending Volatile Session Lower, GBP Outperforms

- The long-awaited release of the latest US employment report painted a mixed picture of the US labour market, prompting a volatile session for the US dollar. Despite the higher-than-expected headline NFP change of +64k, the -105k adjustment in October certainly dampened the release, while the above consensus unemployment rate at 4.564% contributed to an immediate extension lower for the US dollar.

- This resulted in the dollar index printing fresh pullback lows at 97.87, the lowest level since October 03. However, the slightly messy release and associated uncertainty surrounding DOGE deferred resignations made the initial greenback pessimism short-lived. Indeed, with the heavy central bank calendar ahead and US inflation data due Thursday, momentum quickly stalled and two-way price action within a relatively contained range persisted across the US session.

- With that said, the DXY is holding 0.3% declines on the session as we approach the APAC crossover and GBP has maintained its position at the top of the G10 leaderboard, rising 0.45% to 1.3435.

- Price action was assisted by a strong set of labour market figures in the UK, with firmer-than-expected wage data denting prospects of easy policy through 2026. Cable bridged the gap to 1.3452, the 61.8% retracement of the Sep 17 - Nov 4 bear leg, and clearance of this hurdle would strengthen a bull theme and open 1.3527, the Oct 1 high. UK inflation data is scheduled tomorrow before Thursday’s BOE decision.

- USDJPY has also tracked lower, initially dented overnight by souring equity sentiment across the APAC session, and the overall adjustment lower for US yields confirming the negative bias for the pair. Lows today came within 5 pips of the December 05 low at 154.35, and also narrow the gap to the key 50-day EMA located just above the 154 handle. A clear breach of this average would undermine the bull theme and signal scope for a deeper retracement.

- Elsewhere, EURUSD had a very brief test above 1.1800 before settling closer to 1.1775. US inflation and the ECB decision/press conference will keep the pair in focus as the week progresses. Above here, 1.1848 is a notable chart point, the Sep 18 high.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 17/12/2025 | 0700/0700 | *** | Consumer Inflation Report (1dp) | |

| 17/12/2025 | 0700/0700 | *** | Producer Prices | |

| 17/12/2025 | 0700/1500 | ** | MNI China Money Market Index (MMI) | |

| 17/12/2025 | 0700/0700 | *** | Consumer Inflation Report (2dp) | |

| 17/12/2025 | 0900/1000 | *** | IFO Business Climate Index | |

| 17/12/2025 | 1000/1100 | *** | EZ HICP Final | |

| 17/12/2025 | 1000/1100 | *** | EZ HICP Final | |

| 17/12/2025 | 1000/1100 | *** | EZ HICP Final | |

| 17/12/2025 | 1000/1100 | *** | EZ HICP Final (2dp) | |

| 17/12/2025 | 1100/1100 | ** | CBI Industrial Trends | |

| 17/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 17/12/2025 | 1315/0815 | Fed Governor Christopher Waller | ||

| 17/12/2025 | 1330/0830 | * | International Canadian Transaction in Securities | |

| 17/12/2025 | 1405/0905 | New York Fed's John Williams | ||

| 17/12/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 17/12/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 17/12/2025 | 1730/1230 | Atlanta Fed's Raphael Bostic | ||

| 17/12/2025 | 1800/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 18/12/2025 | 2145/1045 | *** | GDP | |

| 18/12/2025 | - | European Central Bank Meeting | ||

| 18/12/2025 | - | NorgesBank Meeting | ||

| 18/12/2025 | - | Bank of Japan Meeting | ||

| 18/12/2025 | - | Riksbank Meeting |