MNI ASIA OPEN: Nothing Cook-ing

EXECUTIVE SUMMARY

- MNI US: Implied Probability Of Govt Shutdown Ticks Over 50% As Schumer Digs In

- MNI FED: FHFA's Pulte Maintains That Cook Mortgage Allegations Are Authentic

- MNI US DATA: A Still Strong Increase In Final August Mfg PMI Despite Lower Revision

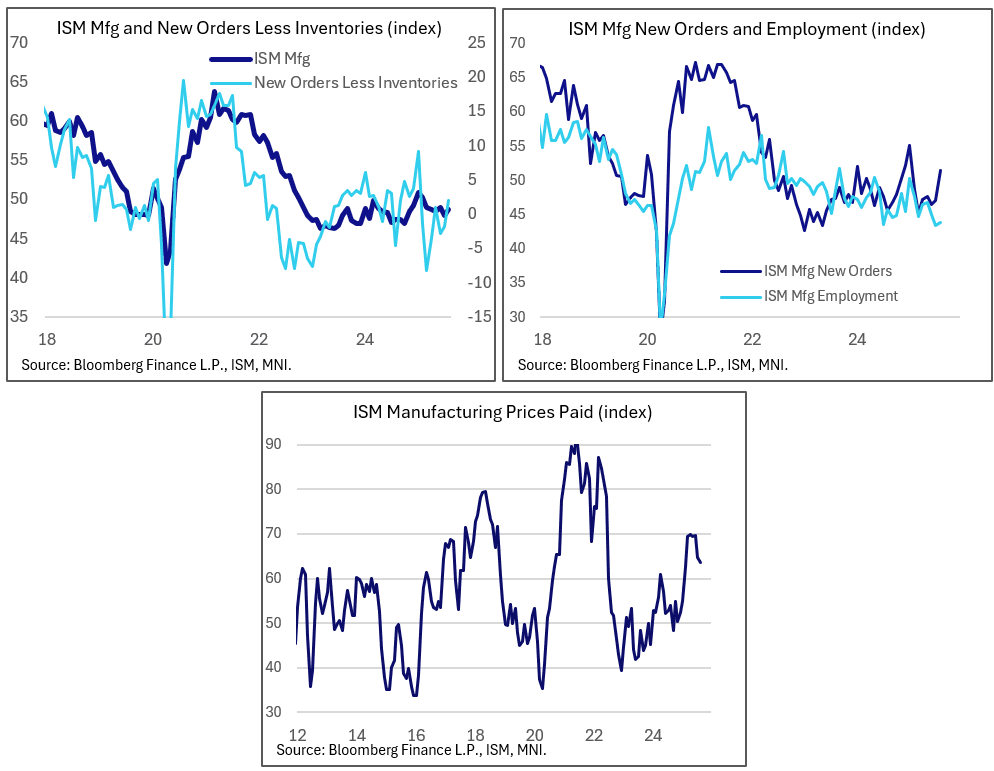

- MNI US DATA: ISM Manufacturing Improves On New Orders, But Tariffs Still Taking Toll

US

MNI STIR: Not Much Cook-ing On The Fed Implied Rates Front

The implied Fed funds path was little changed Tuesday, with Fed Funds futures implying roughly 23bp of cuts in September (ie 90+% probability of a 25bp rate cut two weeks from tomorrow).

- The incremental movement was in a hawkish direction, with about 2bp of cumulative cuts priced out of the path over the next year or so. Through next June there is 105bp of cuts implied, with 55bp through year-end (unch from Monday).

- There was a modest but notable pullback in expected cuts a little after 9am ET as the USD extended to session highs, before reversing on a soft ISM Manufacturing gain and unexpected Prices Paid pullback.

- One potential market-mover today, a decision in Fed Gov Cook's lawsuit to stop her firing, didn't materialize as the judge gave the Justice Department until Thursday to file another brief.

- Potential points of interes Wednesday include an appearance by FOMC voter Musalem, JOLTS job openings data, and the Fed Beige Book in the afternoon.

| Meeting | Current FF Implieds (%), LH | Cumulative Change From Current Rate (bp) | Incremental Chg (bp) | Yesterday (Sep 01) | Chg Since Then (bp) |

| Sep 17 2025 | 4.10 | -22.9 | -22.9 | 4.11 | -0.5 |

| Oct 29 2025 | 3.97 | -35.7 | -12.8 | 3.98 | -0.2 |

| Dec 10 2025 | 3.78 | -55.5 | -19.8 | 3.77 | 0.3 |

| Jan 28 2026 | 3.67 | -66.2 | -10.7 | 3.65 | 1.5 |

| Mar 18 2026 | 3.53 | -79.7 | -13.5 | 3.52 | 0.5 |

| Apr 29 2026 | 3.44 | -88.7 | -9.0 | 3.42 | 2.5 |

| Jun 17 2026 | 3.28 | -104.8 | -16.1 | 3.26 | 2.3 |

NEWS

MNI US: Implied Probability Of Govt Shutdown Ticks Over 50% As Schumer Digs In

Political betting markets upgraded the risk of a government shutdown in 2025 after Senate Minority Leader Chuck Schumer (D-NY) issued a 'letter to colleagues' this morning taking a hard line on President Trump's decision to use a 'pocket rescission' to unlilaterally cancel roughly USD$5 billion in Congressionally appropriated funding. According to Polymarket and Kalshi, the implied probability of a shutdown in 2025 is now above 50%. A new market on Polymarket focused specifically on the upcoming September 30 funding deadline shows more volatility, but is likely to settle near the same mark.

MNI FED: FHFA's Pulte Maintains That Cook Mortgage Allegations Are Authentic

FHFA's Pulte sticks to his claims that his allegations against Fed Governor Cook of mortgage fraud on three separate occasions are authentic, whilst briefly touching on the housing emergency declaratiothat has been floated by Tsy Sec Bessent. A reminder that we could see headlines from the Fed Gov. Cook court case after US District Judge Jia Cobb on Friday asked Cook’s lawyers to file a brief today spelling out their arguments for why Trump’s firing of Cook was unlawful. This is a case that seems likely to ultimately end up in the Supreme Court.

US TSYS

MNI US TSYS: Bear Steepening As Supply Weighs

The Treasury cash curve bear steepened in the return from the Labor Day weekend Tuesday, taking the lead of global peers and shrugging off soft US data.

- Treasuries took an early cue from overnight weakness in European and Japanese government bonds, which in turn was triggered by a combination of fiscal/ political/ supply factors.

- Europe (including UK) saw a record single day's issuance today per Bloomberg, just under EUR 50B. For good measure, Tuesday will have seen 58 investment-grade corporate bond offerings in the US, roughly $43.3B for a 2025 high (per Bloomberg) and narrowly exceeding last year's post-Labor Day sales.

- With UK and German 30Y yields hitting multi-year highs intraday, 30Y Tsys touched their highest levels since July 18 at a shade under the 5% mark (4.9966% session high).

- That move (around 830ET) would mark the intraday high for yields, with a smaller-than-expected improvement in the ISM Manufacturing index and continued weakness in construction spending (both out at 1000ET) helping keep a lid on yields through the rest of the session.

- Latest levels: The 2-Yr yield is up 3.1bps at 3.6474%, 5-Yr is up 3.8bps at 3.7339%, 10-Yr is up 4.5bps at 4.2731%, and 30-Yr is up 4.2bps at 4.9696%. Dec 10-Yr futures (TY) down 10/32 at 112-06 (L: 111-31 / H: 112-16)

- Friday's nonfarm payrolls report is the focus of the week. In the meantime, Wednesday's scheduled highlights include an appearance by St Louis Fed President Musalem (2025 FOMC voter, hawk), factory orders and JOLTS data, and the latest edition of the Fed's Beige Book.

OVERNIGHT DATA

MNI US DATA: ISM Manufacturing Improves On New Orders, But Tariffs Still Taking Toll

August's ISM Manufacturing report was weaker than expected on the headline figure, with some sub-components telling a slightly more mixed story, and price pressures unexpectedly diminished. Overall the ISM survey continues to portray a manufacturing sector that is failing to convincingly regain traction after the summer's tariff-related policy uncertainty. Indeed, tariffs were mentioned extensively in the sector-by-sector anecdotes in the report, and not in a positive light.

- The headline index ticked up a little less than expected, to 48.7 (49.0 expected, 48.0 prior) for a 6th consecutive sub-50 reading, notably with the improvement in the Employment sub-component disappointing at 43.8 (45.0 expected, 43.4 prior - per ISM, "panelists indicated that managing head counts is still the norm at their companies, as opposed to hiring").

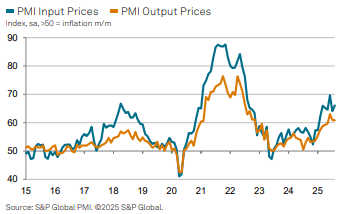

MNI US DATA: A Still Strong Increase In Final August Mfg PMI Despite Lower Revision

- S&P Global US mfg PMI: 53.0 in Aug final (cons & prelim 53.3) after 49.8 in July.

- As such, it was revised modestly lower but is still the highest since May 2022 after a strong monthly increase.

Press release (link) highlights point to a similar story to that from the flash at first glance:

- “US manufacturing operating conditions improved to the greatest degree in over three years during August amid a surge in production and solid growth in new order books.”

- “Firms also took on workers to a greater degree amid evidence of capacity constraints. Inventory building in part fueled the upturn in output, with finished goods stocks rising to the greatest degree in over a year amid worries over prices and supply constraints.”

- “This was again linked to tariffs, which served to raise input costs steeply during August and, in turn, sharply drive up typical selling prices.”

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 249.07 points (-0.55%) at 45295.81

S&P E-Mini Future down 28.5 points (-0.44%) at 6444.5

Nasdaq down 175.9 points (-0.8%) at 21279.63

US 10-Yr yield is up 3.3 bps at 4.2614%

US Dec 10-Yr futures are down 7.5/32 at 112-8.5

EURUSD down 0.0069 (-0.59%) at 1.1641

USDJPY up 1.17 (0.79%) at 148.36

WTI Crude Oil (front-month) up $1.5 (2.34%) at $65.51

Gold is up $59.08 (1.7%) at $3534.97

European bourses closing levels:

EuroStoxx 50 down 76.04 points (-1.42%) at 5291.04

FTSE 100 down 79.65 points (-0.87%) at 9116.69

French CAC 40 down 53.65 points (-0.7%) at 7654.25

US TREASURY FUTURES CLOSE

3M10Y +5.155, 12.796 (L: 8.481 / H: 14.873)

2Y10Y +0.843, 61.808 (L: 60.674 / H: 63.632)

2Y30Y +0.937, 131.805 (L: 129.752 / H: 132.867)

5Y30Y +0.792, 123.785 (L: 121.253 / H: 124.172)

Current futures levels:

Dec 2-Yr futures down 1.5/32 at 104-7.125 (L: 104-05 / H: 104-09.25)

Dec 5-Yr futures down 4/32 at 109-11 (L: 109-04.75 / H: 109-15.25)

Dec 10-Yr futures down 7.5/32 at 112-8.5 (L: 111-31 / H: 112-16)

Dec 30-Yr futures down 21/32 at 113-19 (L: 113-02 / H: 114-07)

Dec Ultra futures down 28/32 at 115-22 (L: 115-01 / H: 116-11)

MNI US 10YR FUTURE TECHS: (Z5) Pullback Appears Corrective

- RES 4: 113-06 2.236 proj of the Jul 15 - 22 - 28 price swing

- RES 3: 113-00 Round number resistance

- RES 2: 112-28+ 2.000 proj of the Jul 15 - 22 - 28 price swing

- RES 1: 112-20+ High Aug 28 / 29

- PRICE: 112-05 @ 1240 ET Sep 2

- SUP 1: 111-31 20-day EMA

- SUP 2: 111-18+ 50-day EMA

- SUP 3: 111-13+ Low Aug 18 and a key support

- SUP 4: 110-25 Low Aug 1

The trend outlook in Treasury futures is bullish and the latest pullback appears corrective. Last week’s gains delivered a print above 112-15+, the Aug 5 high and a bull trigger. A breach of this hurdle confirms a resumption of the bull cycle and paves the way for a climb towards the 113-00 handle. Moving average studies are in a bull-mode position, reinforcing a bull theme. First support to watch is 111-31, the 20-day EMA.

SOFR FUTURES CLOSE

Current White pack (Sep 25-Jun 26):

Sep 25 +0.005 at 95.910

Dec 25 -0.005 at 96.225

Mar 26 -0.015 at 96.470

Jun 26 -0.025 at 96.730

Red Pack (Sep 26-Jun 27) -0.04 to -0.035

Green Pack (Sep 27-Jun 28) -0.03 to -0.02

Blue Pack (Sep 28-Jun 29) -0.02 to -0.02

Gold Pack (Sep 29-Jun 30) -0.02 to -0.015

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.34% (+0.00), volume: $2.880T

- Broad General Collateral Rate (BGCR): 4.33% (+0.00), volume: $1.129T

- Tri-Party General Collateral Rate (TCR): 4.33% (+0.00), volume: $1.102T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $115B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $224B

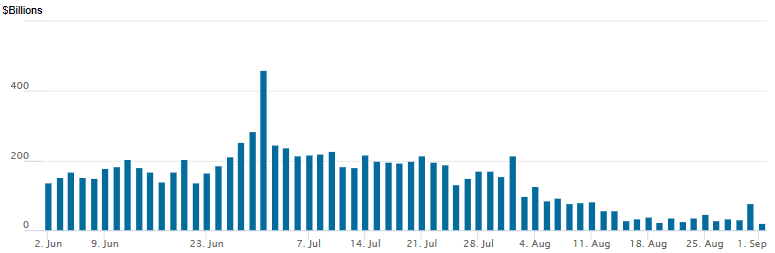

FED Reverse Repo Operation

RRP usage retreats to lowest level since early April 2021 today: $21.066B with 17 counterparties this afternoon, from $77.898B last Friday. Compares to prior low of $22.344B on Tuesday, Aug 19 vs. this year's high usage of $460.731B on June 30.

MNI PIPELINE: Corporate Bond Roundup: Unexpected $47.45B Priced Tuesday

- Date $MM Issuer (Priced *, Launch #)

- 09/02 $6B Merck $750M 2Y +25, $500M 2Y SOFR+46, $750M 5Y +45, $1B 7Y +58, $1.75B 10Y +68, $1.25B 30Y +75

- 09/02 $4.5B *Cigna $1B 5Y +80, $1.25B 7Y +90, $1.5B 10Y +100, $750M 30Y +110

- 09/02 $4B *MUFG $1B 6NC5 +80, $1B 6NC5 SOFR+113, $1B 11NC10 +93, $1B PerpNC10 6.35%

- 09/02 $2.5B *CIBC $850M 3NC2 +60, $650M 3NC2 SOFR+80, $1B 6NC5 +85

- 09/02 $2B *Royalty Pharma $600M +5Y +93, $900M 10Y +118, $500M 30Y +128

- 09/02 $2B *Volkswagen Grp $700M 2Y +82, $700M 3Y +95, $600M 5Y +112

- 09/02 $2B *Toyota Cr $800M 3Y +47, $500M 3Y SOFR+72, $700M 7Y +68

- 09/02 $2B AIIB WNG 5Y SOFR +34a

- 09/02 $1.75B *Brazil $750M 11/30 tap 5.2%, $1B 30Y +7.5%

- 09/02 $1.75B *Sumitomo Mitsui $750M 3Y SOFR+75, $500M 5Y +65, $500M 11NC10 +115

- 09/02 $1.65B *Mitsubishi $300M 3Y +45, $400M 3Y SOFR+70, $500M 5Y +50, $400M 10Y +65

- 09/02 $1.65B *American Honda $700M 3Y +65, $300M 3Y SOFR+90, $650M 5Y +80

- 09/02 $1.5B *BHP Billiton $500M +10Y +77, $1B 30Y +83

- 09/02 $1.5B *HSBC 11NC10 +147

- 09/02 $1.5B *ING PerpNC7 7.0%

- 09/02 $1.35B *Jersey Central Power $350M +3Y +55, $500M +5Y +70, $500M +10Y +90

- 09/02 $1.25B *Ford Motor Cr 5Y +198

- 09/02 $1.25B *Credit Agricole PerpNC10 7.125%

- 09/02 $1.2B *Kodiak Gas $600M 8NC3 6.5%, $600M 10NC5 6.75%

- 09/02 $1B *Norinchukin $500M 5Y +93, $500M 10Y +108

- 09/02 $1B *Guardian Life $550M 3Y +45, $450M 7Y +70

- 09/02 $750M *Nomura 10.75NC5.75 +130

- 09/02 $650M *Ares Capital +5Y +160

- 09/02 $600M *Antofagasta 10Y +140

- 09/02 $600M *First Citizens 10NC5 +185

- 09/02 $500M *Jackson National Life 5Y +85

- 09/02 $500M *Alabama Power +5Y +60

- 09/02 $500M *Orix Corp 5Y +75

- 09/02 $Benchmark Kingdom of Saudi Arabia Sukuk 5Y +65, 10Y +75

- Expected Wednesday:

- 09/03 $Benchmark OKB 5Y SOFR+46a

MNI BONDS: EGBs-GILTS CASH CLOSE: Fiscal Concerns Apply Bear Steepening Pressure

European long-end instruments remained under pressure Tuesday.

- Fiscal and political concerns were at the forefront globally, starting with Japan overnight pushing long-end JGB yields up, a move that spilled over into European morning trade. Gilts underperformed amid continued UK fiscal uncertainty, which also saw GBP underperform peers.

- Supply was a constant pressure as well. with Bloomberg noting a record one-day corporate/govvy supply total of just under E50B, including UK and Italian sovereign syndications.

- ECB talk was plentiful: Schnabel noted upside inflation risks from tariffs and Muller reiterated his previous patient stance, while Villeroy said that inflation allowed for "favourable" interest rates and Simkus suggested a rate cut toward the end of year is plausible.

- European data was less impactful, with Eurozone flash August inflation slightly above-expected. Somewhat weak US ISM Manufacturing data helped global FI recover from its weakest levels of the day, however.

- The UK and German curves bear steepened. Multiple landmarks were reached, with a 14-year / 27-year highs reached in 30Y German / UK yields, respectively.

- Periphery/semi-core EGB spreads widened, with Portugal outperforming after Friday's ratings upgrade from S&P.

- Wednesday brings BOE TSC testimony, along with August final PMIs.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.9bps at 1.974%, 5-Yr is up 3.4bps at 2.313%, 10-Yr is up 3.8bps at 2.786%, and 30-Yr is up 4.6bps at 3.406%.

- UK: The 2-Yr yield is up 1.7bps at 3.982%, 5-Yr is up 3.9bps at 4.171%, 10-Yr is up 5bps at 4.8%, and 30-Yr is up 5.3bps at 5.693%.

- Italian BTP spread up 2.9bps at 89bps / Portuguese PGB up 0.4bps at 44.8bps

MNI FOREX: USD Off Best Levels Following ISM Manufacturing, GBP Weakness Stands Out

- Tuesday’s session was characterised by a sharp move higher for the US dollar across the European morning. Acute pressure on the longer-end of the UK, US and European yield curves drove risk-off sentiment, echoed by weakness for the major equity benchmarks. The USD index rose as much as 0.9% before stabilising and reversing a small portion of the gains following the ISM manufacturing data release.

- August's ISM Manufacturing report was weaker than expected on the headline figure, with some sub-components telling a slightly more mixed story, and price pressures unexpectedly diminished. This may have led participants to question the outright bullish dollar bias from earlier in the day, especially ahead of the crucial US labour market report on Friday.

- GBP weakness has been most notable Tuesday, with cable remaining 1.2% lower as a window-dressing UK reshuffle (not expected to resolve Starmer's popularity crisis in the near-term) was looked at unfavourably by investors. Cable had a punchy 208 pip range, printing a near 4-week low of 1.3341. Immediate focus will be on trendline support, drawn from the years lows. This level intersects around the 1.33 handle. Below here, 1.3249 is another notable chart level, the 76.4% retracement of the Aug 1 - 14 bull leg.

- Today’s EURGBP price action has resulted in a breach of resistance at 0.8674, the Aug 25 and 29 high. The break signals a stronger reversal and suggests scope for climb towards 0.8744, the Aug 7 high. Key resistance and the bull trigger is at 0.8769, the Jul 28 high. A break of this level would place the cross at the highest level since May 2023.

- The dynamic of widening yield differentials and heightened political uncertainty in Japan underpinned an impressive USDJPY rally to highs of 148.94 ahead of the US data. Fibonacci resistance at 149.12 has held for now, with the late reversal taking the pair back to 148.30 ahead of the APAC crossover.

- Australian Q2 GDP headlines the calendar on Wednesday, before final Eurozone services PMIs and US JOLTS data.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 03/09/2025 | 0700/0300 | * | Turkey CPI | |

| 03/09/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0730/0930 | ECB Lagarde Speaks at ESRB Conference | ||

| 03/09/2025 | 0730/0830 | BOE Mann at Signum's London Westminster Day roundtable | ||

| 03/09/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0815/0915 | BOE Breeden at Innovation in Money and Payments Conference | ||

| 03/09/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 03/09/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 03/09/2025 | 0900/1100 | ** | EZ PPI | |

| 03/09/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 03/09/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 03/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 03/09/2025 | 1300/0900 | St. Louis Fed's Alberto Musalem | ||

| 03/09/2025 | 1315/1415 | BOE testify at TSC: Bailey, Greene, Lombardelli, Taylor | ||

| 03/09/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/09/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 03/09/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 03/09/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/09/2025 | 1730/1330 | Minneapolis Fed's Neel Kashkari | ||

| 03/09/2025 | 1800/1400 | Fed Beige Book | ||

| 04/09/2025 | 0130/1130 | ** | Trade Balance |