MNI ASIA OPEN: KC Fed Schmid - Little Reason to Lower Rates

EXECUTIVE SUMMARY

- MNI FED BRIEF: KC Fed Schmid Sees 'Little Reason' To Lower Rates

- MNI FED: Daly: Incoming Data Looks Promising, Policy In A Good Place

- MNI US DATA: FOMC Will Have PCE Data Through January By Its March Meeting

- MNI US: Risk Of Partial Govt Shutdown Ticks Up, But Impact On Markets Limited

- MNI US DATA: Inflation Softens But Divergence In Manufacturing Prices Received

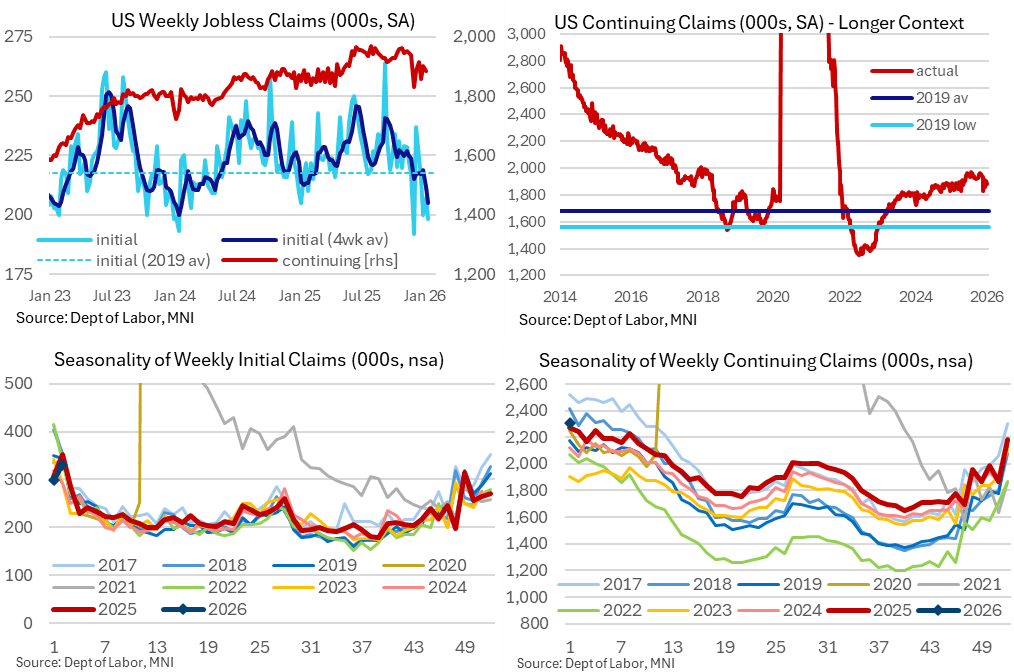

- MNI US DATA: Claims Point To (Particularly) Low Firing and Low Hiring Jobs Market

US

MNI FED BRIEF: KC Fed Schmid Sees 'Little Reason' To Lower Rates

The Federal Reserve needs to keep monetary policy somewhat tight to continue putting downward pressure on an inflation rate that has shown some improvement but remains too high, Kansas City Fed President Jeffrey Schmid said Thursday. "I see little reason at this point to further lower the policy rate, though of course, I will be watching the data closely for signs that growth is losing momentum or that the labor market is weakening more substantially," Schmid said in prepared remarks.

MNI FED: Daly: Incoming Data Looks Promising, Policy In A Good Place

SF Fed's Daly ('27 voter) has posted a chain on X (link), noting that incoming data looks promising but with the Fed needing to be deliberate as it calibrates policy to achieve its full mandate. "The Federal Reserve’s job is to serve the American people. In monetary policy that means achieving our dual mandate goals of price stability and full employment.

MNI US DATA: FOMC Will Have PCE Data Through January By Its March Meeting

The Bureau of Economic Analysis has announced updated release dates for delayed data: The Q4 GDP / 2025 second estimate will be published March 13 (was originally scheduled for Feb 26); with the third estimate out April 9 (originally scheduled for March 27). These will follow the advance estimate for the quarter on February 20.

NEWS

MNI US: Risk Of Partial Govt Shutdown Ticks Up, But Impact On Markets Limited

The Senate is expected to pass a 3-bill appropriations minibus today, taking the total number of completed FY26 funding bills to 6 (out of 12). Senate appropriators are expected to release another package over the weekend, covering Defense, Transportation-HUD and Labor-HHS-Education.

MNI US: Trump Urges Congress To Enact 'Great Healthcare Plan'

US President Donald Trump has announced in a video message on X and a fact sheet on the White House website that he has requested Congress enact, "a comprehensive plan to lower drug prices, lower insurance premiums, hold big insurance companies accountable, and maximize price transparency." The proposal, entitled "the Great Healthcare Plan" would "execute the President’s vision to send money directly to the American people, lower health insurance premiums, and cut kickbacks that raise insurance premiums."

Trump says the US ‘shouldn’t even have an election’ in 2026 because of all his accomplishments (The Independent) - President Donald Trump told Reuters the U.S. should not have an election later this year because of his accomplishments in office.

US TSYS

MNI US TSYS: Yields Rising on 5Th Straight Weekly Claims: Low Fire/Hire

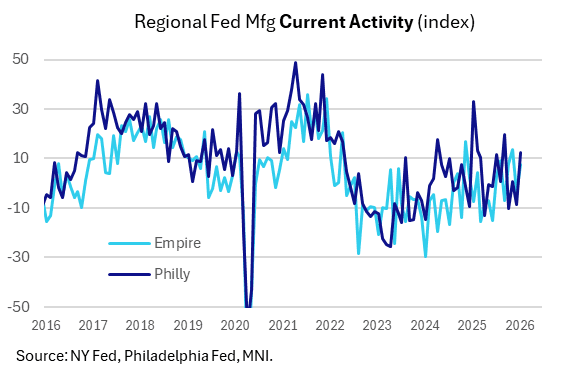

- Treasuries look to finish mostly weaker Thursday, near session lows, curves flatter with the 30Y Bond outperforming. Futures retreated after weekly & continuing claims come out lower than expected, regional fed data higher than est for Philly Fed Business Outlook & Empire Mfg.

- Tsys rebounded late morning - tracking a similar move in Bunds before see-sawing near lows for the balance of the session. The TYH6 currently trades -8.5 at 112-06.5 vs. 112-06 low, attention is on support at 111-29, the Dec 10 low and bear trigger. A break of it would resume the bear cycle.

- Initial claims came in at just 198k (sa, cons 215k) in the week to Jan 10 after a marginally downward revised 207k (initial 208k) in the previous week. Continuing claims also surprised lower at 1884k (sa, cons 1897k) in the week to Jan 3 after a downward revised 1903k (initial 1914k)

- Kansas City Fed Schmid commented on the economy late Thursday: "I see little reason at this point to further lower the policy rate" while watching data "for signs that growth is losing momentum or that the labor market is weakening more substantially."

- The Bureau of Economic Analysis has announced updated release dates for delayed data: The Q4 GDP / 2025 second estimate will be published March 13 (was originally scheduled for Feb 26); with the third estimate out April 9 (originally scheduled for March 27). These will follow the advance estimate for the quarter on February 20.

- Look ahead to Friday: data limited to Industrial Production & Capacity Utilization at 0915ET, otherwise multiple Fed speakers are scheduled: Boston Fed Collins welcoming remarks (1050ET), Fed VC Bowman on economy & monetary policy (1100E) and Fed VC Jefferson at 1130ET.

OVERNIGHT DATA

MNI US DATA: Claims Point To (Particularly) Low Firing and Low Hiring Jobs Market

Initial jobless claims surprised lower for a fifth consecutive week. There are residual seasonality concerns, which could see increases heading into February, but it was still left one of the lowest single weekly readings of recent years and the lowest four-week average since Jan 2024. Continuing claims continue to hold their easing back from cycle highs seen through Jun-Oct.

- Initial claims came in at just 198k (sa, cons 215k) in the week to Jan 10 after a marginally downward revised 207k (initial 208k) in the previous week. Continuing claims also surprised lower at 1884k (sa, cons 1897k) in the week to Jan 3 after a downward revised 1903k (initial 1914k)

MNI US DATA: Empire And Philly Manufacturing Start Year Strong, Except Jobs

Manufacturing activity in the neighboring New York and Philadelphia Fed regions picked up in January after a weak December, boding well for a national pickup in industrial activity at the start of the year. That included better new orders and shipments across both surveys. However if there was a note of caution in activity, it was in employment, which deteriorated in both region - particularly New York.

- The Empire State Manufacturing Survey's General Business Conditions index jumped to 7.7 from -3.7 in December, and vs the 1.0 expected - partially retracing the large drop from 18.7 in November.

- And the Philadelphia Fed's Manufacturing Business Outlook Survey showed a general activity index that likewise surprised to the upside in reversing a negative print prior, printing 12.6 after -8.8 in December, and better than the -1.4 expected. This was a 4-month high for the Philly index.

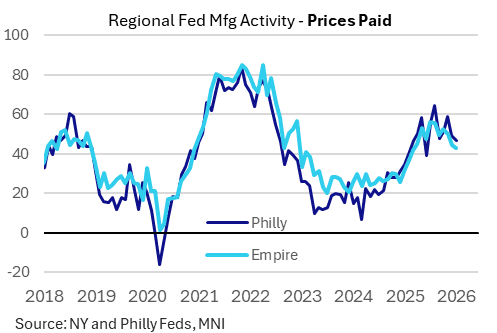

MNI US DATA: Inflation Softens But Divergence In Manufacturing Prices Received

Prices paid indices fell across both surveys as the tariff-related increase seen through much of 2025 shows increasing signs of dissipating.

- In the New York region, the prices paid index dipped 1.4 points in January to 42.8, a fresh 10-month low and indicating input price increases remained elevated but at least moderated.

- In Philadelphia, current prices paid fell to 46.9 from 49.3, marking a 7-month low.

MNI CANADA DATA: Autos Lead Declines in Nov Factory And Wholesale Sales

- Wholesale excluding petroleum and grains -1.8% in Nov, second largest fall in the past two years, StatsCan said Thursday.

- Factory sales -1.2% in Nov; -1.1% YOY. Volumes -2.3%.

- Wholesale sales of autos -11.5% and factory sales of autos -15.9%; the lowest level since Oct 2022 in both categories leading the declines. StatsCan cited a semiconductor shortage hampering production.

- Motor vehicle manufacturing -21% YOY in November amid US tariffs.

- Sales in new autos and parts +2.1% while sales of used autos -14.6% and auto parts -26.9% in Nov as per the Wholesale report.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 259.5 points (0.53%) at 49411.12

S&P E-Mini Future up 12.25 points (0.18%) at 6979.25

Nasdaq up 55.6 points (0.2%) at 23528.63

US 10-Yr yield is up 3.4 bps at 4.1655%

US Mar 10-Yr futures are down 9.5/32 at 112-5.5

EURUSD down 0.0037 (-0.32%) at 1.1607

USDJPY up 0.12 (0.08%) at 158.59

WTI Crude Oil (front-month) down $2.96 (-4.77%) at $59.06

Gold is down $24.58 (-0.53%) at $4601.54

European bourses closing levels:

EuroStoxx 50 up 36.09 points (0.6%) at 6041.14

FTSE 100 up 54.59 points (0.54%) at 10238.94

German DAX up 66.15 points (0.26%) at 25352.39

French CAC 40 down 17.85 points (-0.21%) at 8313.12

US TREASURY FUTURES CLOSE

Curve update:

3M10Y +3.123, 51.33 (L: 46.956 / H: 51.33)

2Y10Y -1.893, 59.925 (L: 58.941 / H: 62.591)

2Y30Y -4.329, 122.667 (L: 121.659 / H: 127.796)

5Y30Y -4.41, 102.527 (L: 101.943 / H: 107.367)

Current futures levels:

Mar 2-Yr futures down 3.375/32 at 104-5.75 (L: 104-05.75 / H: 104-09.375)

Mar 5-Yr futures down 7.5/32 at 108-31.75 (L: 108-31.5 / H: 109-08)

Mar 10-Yr futures down 9.5/32 at 112-5.5 (L: 112-05.5 / H: 112-17.5)

Mar 30-Yr futures down 4/32 at 116-6 (L: 116-04 / H: 116-19)

Mar Ultra futures steady at at 118-26 (L: 118-20 / H: 119-08)

MNI US 10YR FUTURE TECHS: (H6) Bear Threat Still Present

- RES 4: 113-00+ 61.8% retracement of the Nov 25 - Dec 10 bear leg

- RES 3: 112-31 High Dec 18 and key short-term resistance

- RES 2: 112-25+ High Dec 30 / 31

- RES 1: 112-22 High Jan 7

- PRICE: 112-06+ @ 1200 ET Jan 15

- SUP 1: 111-29 Low Dec 10 and the bear trigger

- SUP 2: 111-19 1.236 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 3: 111-11 1.382 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 4: 111-00 Round number support

Despite a recovery this week in Treasuries, a bear threat remains intact and short-term gains are considered corrective. Attention is on support at 111-29, the Dec 10 low and bear trigger. A break of it would resume the bear cycle. Note too that a head and shoulders reversal pattern on the daily chart continues to highlight a bearish threat. Scope is seen for a move towards 111-19, a Fibonacci projection. Key S/T resistance is 112-31, Dec 18 high.

SOFR FUTURES CLOSE

Current White pack (Mar 26-Dec 26):

Mar 26 -0.020 at 96.375

Jun 26 -0.050 at 96.545

Sep 26 -0.065 at 96.705

Dec 26 -0.070 at 96.775

Red Pack (Mar 27-Dec 27) -0.08 to -0.07

Green Pack (Mar 28-Dec 28) -0.065 to -0.06

Blue Pack (Mar 29-Dec 29) -0.055 to -0.045

Gold Pack (Mar 30-Dec 30) -0.04 to -0.03

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.64% (-0.01), volume: $3.148T

- Broad General Collateral Rate (BGCR): 3.62% (-0.01), volume: $1.328T

- Tri-Party General Collateral Rate (TCR): 3.62% (-0.01), volume: $1.293T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $94B

- Daily Overnight Bank Funding Rate: 3.63% (+0.00), volume: $180B

FED Reverse Repo Operation

RRP usage slips to $2.003B with 6 counterparties this afternoon vs. $3.223B Wednesday. Compares to December 12 low of $0.838B (lowest level since mid-March 2021); this years highest excess liquidity measure: $460.731B on June 30.

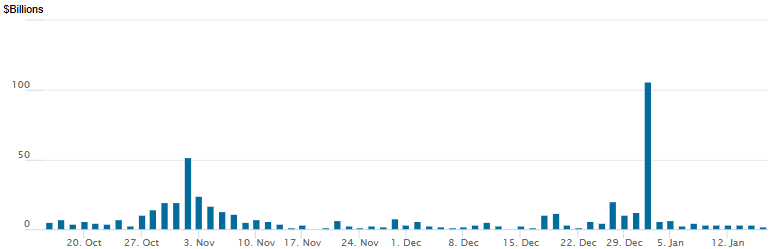

MNI PIPELINE: Corporate Bond Roundup: $42.5B Debt to Price Thursday, GS 6Pt Leads

A total of $42.5B in corporate debt to price today, domestic dealers leading the charge with Goldman Sachs $16B over 6 tranches - the largest since Meta issued $30B back in late October.

- Date $MM Issuer (Priced *, Launch #)

- 01/15 $16B #GS $3.75B 3NC2 +58, $750M 3NC2 SOFR+71, $3.75B 6NC5 +75, $500M 6NC5 SOFR+96, $4.5B 11NC10 +90, $2.75B 21NC20 +80

- 01/15 $8B *Morgan Stanley $2.5B 4NC3 +65, $750M 4NC3 SOFR+80, $3.25B 6NC5 +75, $1.5B 15NC10 +117

- 01/15 $8B #Wells Fargo $2B 4NC3 +58, $500M 4NC3 SOFR+74, $3.5B 11NC10 +80, $2B 21NC20 +70

- 01/15 $3B *IADB 10Y SOFR+41

- 01/15 $1.5B #JBIC $500M WNG 5Y SOFR+44, $1B WNG 10Y SOFR+60

- 01/15 $1.5B *Kuaishou Tech $60M 5Y +50, $900M 10Y +70

- 01/15 $1.25B *OPEC Fund 5Y SOFR+54

- 01/15 $1B *Nordic Inv Bank 5Y SOFR+29

- 01/15 $1B *Saudi Ntnl Bank perpNC5.5 6.15%

- 01/15 $750M #Apollo Debt Solutions 5Y +195

- 01/15 $500M #American National Global Funding 5Y +113

MNI BONDS: EGBs-GILTS CASH CLOSE: Short-End Underperformance As Data Comes In Solid

Gilts bear flattened Thursday, with core EGBs twist flattening.

- Short-end underperformance was the theme globally as firmer risk sentiment and equities, as well as solid economic data, prompted modest central bank easing/cutting repricing.

- UK GDP data proved firmer than expected, helping Gilts underperform Bunds early and indeed throughout the day.

- Later, there was some hawkish repricing in the US front end that maintained pressure in Europe, after data showed lower-than-expected jobless claims, stronger regional Fed manufacturing surveys, and solid import price data helping the US dollar jump for a spell.

- Eurozone data didn't have much impact: Spanish and French final December HICP confirmed flash estimates, German 2025 GDP was in line at 0.2%, and Eurozone industrial production for November surprised to the upside following

Italian data earlier. - Yields closed near the session highs. Periphery/semi-core EGB spreads tightened modestly on the day.

- Friday's calendar includes final December inflation data from Germany and Italy, with an appearance by ECB's Escriva and release of a speech text from BOE's Bailey.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 2.3bps at 2.098%, 5-Yr is up 1.8bps at 2.386%, 10-Yr is up 0.5bps at 2.819%, and 30-Yr is down 1.8bps at 3.404%.

- UK: The 2-Yr yield is up 4.5bps at 3.67%, 5-Yr is up 5.6bps at 3.86%, 10-Yr is up 4.8bps at 4.388%, and 30-Yr is up 3.4bps at 5.126%.

- Italian BTP spread down 1.1bps at 62.5bps / French OAT down 0.6bps at 67.4bps

MNI FOREX: USD Index Extends 2026 Rally, AUD Outperforms amid Equity Rebound

- Firmer risk sentiment/equities on Thursday have helped bolster the US dollar overall, with the ‘sell-US’ theme from earlier in the week attached to Fed independence concerns and geopolitical uncertainty dissipating somewhat. This has helped the USD index extend its strong run in 2026, with the index briefly rising to 99.50, a six-week high.

- This dynamic weighed on the likes of EURUSD and GBPUSD, which fell back to 1.16 and 1.34 respectively. The GBP move came despite a better-than-expected UK monthly GDP print, with the market looking through the data as much of it was payback after the soft October (itself driven by the cyberattack on Jaguar Land Rover, which hit manufacturing production). GBPUSD losses generally being led by the USD leg of the trade, but the YTD pullback in Gilt yields has led to a sell-on-rallies backdrop for GBP so far this year.

- The recovery for risk/equities has helped the Australian dollar outperform its G10 peers, with the overall optimistic backdrop for higher beta currencies remaining strong. This dynamic weighed on EURAUD earlier in January, prompting a notable breach of the 2025 June low of 1.7462. While downside momentum for the cross quickly stalled, it is worth highlighting that during a period of consolidation, EURAUD remained below this breakdown level, maintaining the bearish potential for the move.

- Sure enough, today’s 0.65% decline has seen us rapidly approach last week’s cycle lows at 1.7291. We highlight the next key target is 1.7248, the May 2025 low, before the medium-term objective of 1.7050, the March 2025 low.

- In similar vein, emerging market currencies have been happy to look through this spell of dollar strength, with carry/risk dynamics significantly supporting the likes of ZAR and MXN, with the latter extending notably to a fresh cycle high. This narrows the gap to next noted support at 17.6067 for USDMXN, the Jul 12 ‘24 low, a clearance of which would open 17.4466.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 16/01/2026 | 0700/0800 | *** | Germany CPI (f) | |

| 16/01/2026 | 0700/0800 | *** | Germany CPI (f) | |

| 16/01/2026 | 0900/1000 | ** | Italy Final HICP | |

| 16/01/2026 | 0900/1000 | *** | HICP (f) | |

| 16/01/2026 | 1000/1000 | BOE Bailey at Bellagio meeting (with Lombardelli) Text | ||

| 16/01/2026 | 1315/0815 | ** | CMHC Housing Starts | |

| 16/01/2026 | 1330/0830 | * | International Canadian Transaction in Securities | |

| 16/01/2026 | 1415/0915 | *** | Industrial Production | |

| 16/01/2026 | 1500/1000 | ** | NAHB Home Builder Index | |

| 16/01/2026 | 1550/1050 | Boston Fed's Susan Collins | ||

| 16/01/2026 | 1600/1100 | Fed Vice Chair Michelle Bowman | ||

| 16/01/2026 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 16/01/2026 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 16/01/2026 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 16/01/2026 | 2030/1530 | Fed Vice Chair Philip Jefferson |