MNI ASIA OPEN: French Government On The Brink ... Again

MNI (NEW YORK) -

EXECUTIVE SUMMARY

- FRANCE: Lecornu Accepts Macron's Request For Last-Ditch Stability Talks

- MNI: Canada Shifting Budget To Fall From Spring Starting Nov 4

- TARIFFS: Trump: 25% Truck Tariffs To Start Nov 1

- MNI BRIEF: Brazil Inflation Progress To Target Slows-Galipolo

FRANCE: Lecornu Accepts Macron's Request For Last-Ditch Stability Talks

Outgoing French Prime Minister Sébastien Lecornu has accepted President Emmanuel Macron's request for “last-ditch talks” with parliamentary leaders aimed at restoring stability. Lecornu wrote on X, “I have accepted, at the request of the President of the Republic, to hold final discussions with the political forces for the stability of the country. I will tell the head of state on Wednesday evening whether this is possible or not, so that he can draw all the necessary conclusions.”

MNI: Canada Shifting Budget To Fall From Spring Starting Nov 4

Canada will switch to presenting the government's full budget in the fall starting with the one due Nov 4 and move its mid-year update to the spring, Finance Minister Francois-Philippe Champagne said Monday, adding that it will begin splitting the books into capital and operating accounts.

MNI BRIEF: Champagne Unfazed By CAD90B Deficit For NATO Goal

Canada's Finance Minister Francois-Philippe Champagne on Monday responded to an opposition question at a committee hearing about Canada's deficit reaching CAD90 billion to meet a higher NATO target by saying: “Are you suggesting that we should not meet our NATO commitments?”

Trump and Brazilian President Lula have 'friendly' call (BBC)

President Donald Trump and his Brazilian counterpart, Luiz Inácio Lula da Silva, have had a call described by both sides as friendly and positive as Brazil seeks to reduce a 50% US tariff on imports. In Monday's video chat, Lula asked Trump to remove most of the duties. Trump said on social media they had a "very good telephone call". It is the first time the two have spoken formally since they had a brief encounter at the United Nations General Assembly in New York last month.

MNI BRIEF: Brazil Inflation Progress To Target Slows-Galipolo

Central Bank of Brazil Governor Gabriel Galipolo said Monday that the resilience of economic activity is causing a slower convergence of inflation toward the 3% target, making it necessary for policy to remain restrictive. " It’s necessary to preserve the gains seen in the labor market over recent years, because inflation erodes and undermines those gains," Galipolo said at an event sponsored by Fundacao Fernando Henrique Cardoso (FHC), in Sao Paulo.

OVERNIGHT DATA

No major data released in the US market session

US TSYS: Bear Steepening In Line With Peers

The Treasury curve bear steepened Monday, aligning with global developments.

- Most of the uptick in yields was on the open, triggered by pressure in long-end JGBs following the surprise win in the LDP leadership election of Sanae Takaichi, who has been a proponent of fiscal expansion to support growth.

- Indeed, political intrigue was a pervasive theme on the day, with the French Prime Minister unexpectedly resigning, trigging a brief risk-off rally in core instruments including Treasuries.

- But apart from another move lower in mid-morning, yields were content to drift higher through most of the rest of the session, set to close near the highs.

- TY futures remain between near-term support/resistance levels - Dec 10-Yr futures (TY) down 9.5/32 at 112-12 (L: 112-11.5 / H: 112-19.5), remaining poised around support at 112-12+/01 50-day EMA / 50.0% of Jul 15 - Sep 11 upleg).

- Latest cash levels: The 2-Yr yield is up 2.1bps at 3.5966%, 5-Yr is up 3.1bps at 3.7462%, 10-Yr is up 4.5bps at 4.1637%, and 30-Yr is up 4.9bps at 4.7605%.

- There was no major data scheduled for publication Monday but the federal government shutdown (which seems not to be close to being resolved) ensures there will be limited releases the rest of the week: Tuesday brings Redbook retail sales, the NY Fed consumer expectations survey, and the Federal Reserve's consumer credit release.

- Additionally, nominal Treasury auction supply resumes with the first sale of the month ($58B in 3Y Note).

- We hear from KC Fed's Schmid on the economic outlook and monetary policy after the cash close today, with Tuesday bringing Bostic, Bowman, Kashkari, and Miran.

US 10YR FUTURE TECHS: (Z5) Monitoring Support

- RES 4: 114-10 High Apr 7 (cont.)

- RES 3: 114-00 Round number resistance

- RES 2: 113-12/29 High Sep 18 / High Sep 11 and the bull trigger

- RES 1: 113-00 High Sep 24

- PRICE: 112-13+ @ 16:59 BST Oct 6

- SUP 1: 112-12+/01 50-day EMA / 50.0% of Jul 15 - Sep 11 upleg

- SUP 2: 111-26 Low Aug 26

- SUP 3: 111-13+ Low Aug 18 and a key support

- SUP 4: 111-01+ 76.4% retracement of the Jul 15 - Sep 11 bull phase

Treasuries have pulled back from last week’s high print of 112-31+ (Oct 3). Attention is on support at the 50-day EMA, at 112-12+. It has recently been pierced but for now remains intact. A clear break of it would undermine a bull theme and signal scope for a deeper retracement. This would open 111-13+, the Aug 18 low and the next key support. On the upside, initial firm resistance to watch is 113-00, the Sep 24 high. A break would be bullish.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

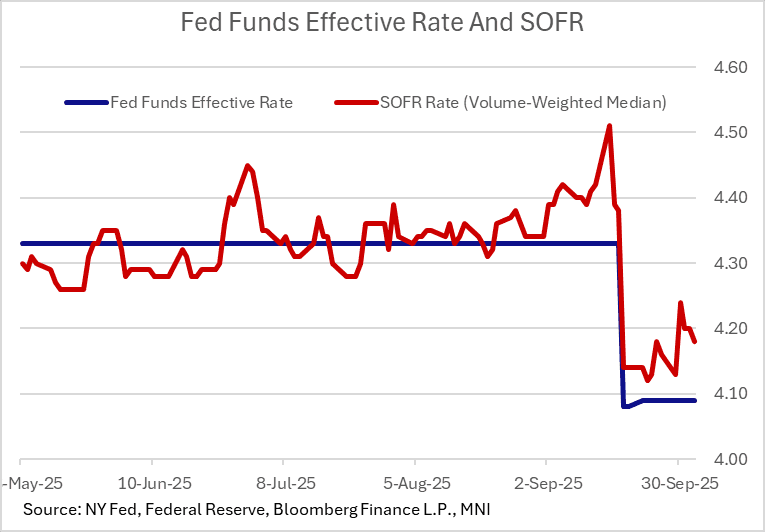

US TSYS/OVERNIGHT REPO: SOFR Continues Downtick From Month-/Quarter-End

Secured rates continued to descend Friday from the month-/quarter-end highs in late September, with SOFR down 2bp to 4.18% (lowest since Sep 29, and vs 4.24% peak on Sep 30). All in all, repo markets showed relatively limited stress in September and through quarter-end despite reserves having fallen to below the $3T mark in the last couple of weeks. Rates could continue to descend today before stalling Tuesday on Treasury bill auction settlements ($17B net cash).

- Effective Fed funds rates have maintained their late-September 1bp uptick to 4.09%.

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.18%, -0.02%, $3018B

* Broad General Collateral Rate (BGCR): 4.16%, -0.01%, $1177B

* Tri-Party General Collateral Rate (TGCR): 4.16%, -0.01%, $1148B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.09%, no change, volume: $95B

* Daily Overnight Bank Funding Rate: 4.09%, no change, volume: $183B

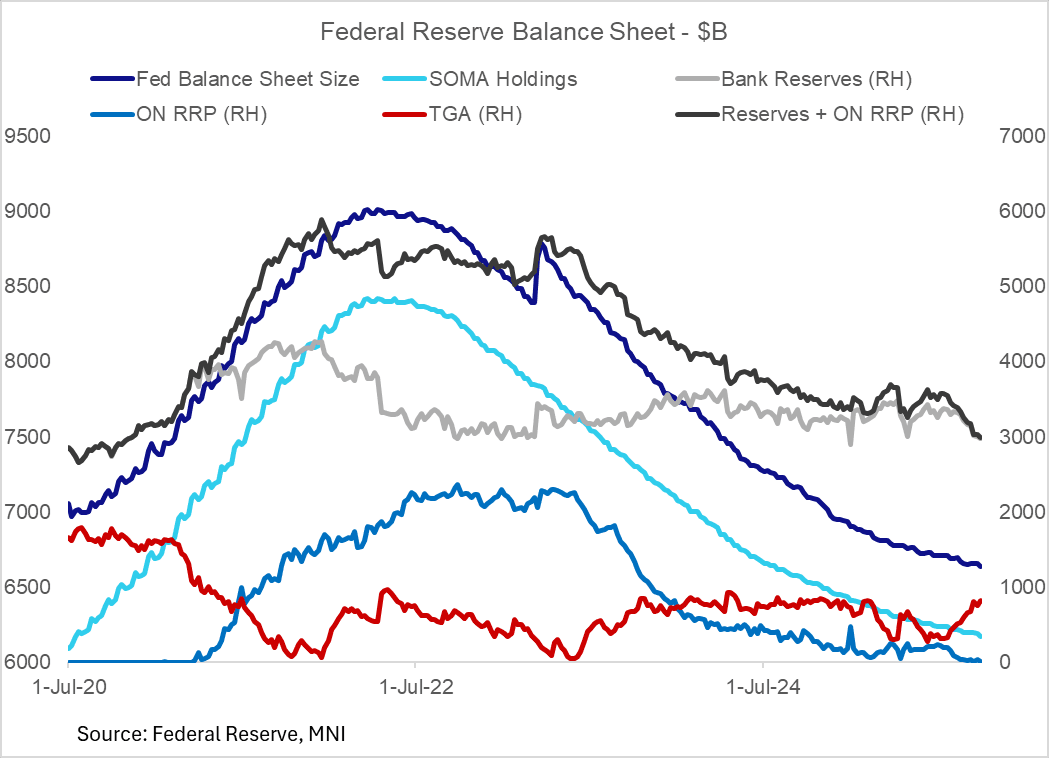

US TSYS/OVERNIGHT REPO: ON RRP Takeup Dips, Remains Negligible

Overnight reverse repo takeup fell $3.6B Monday to $21.8B.

- That's up from the multi-year low $8.4B posted Thursday after quarter/month-end takeup reversed, but overall takeup effectively remains negligible.

- ON RRP + reserves were under $3T as of last Wednesday, potentially getting nearer to the Fed's "ample" threshold of reserves from the current "abundant" regime.

BONDS: EGBs-GILTS CASH CLOSE: Curves Steepen Amid French Political Uncertainty

Long-end yields rose across EGB and Gilt curves, with OATs underperforming on renewed political/fiscal concern.

- The surprise resignation of Prime Minister Lecornu saw OAT spreads widen sharply, with President Macron giving his now ex-PM 48 hours to hold final discussions with political parties to see whether the ongoing budget impasse can be overcome.

- Other semi-core and periphery EGB spreads widened, but more modestly, and closed below session wides.

- More broadly, global curves steepened after longer-end JGBs underperformed following the election of a new Japanese PM overnight.

- On the day, the German curve twist steepened, while the UK's bear steepened.

- In data, Eurozone retail sales extended their recent tepid trend in August, while underlying Spanish industrial production momentum remains constructive despite two consecutive monthly falls.

- Tuesday's calendar includes German factory orders, and appearances by ECB's Nagel and Lagarde.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.2bps at 2.007%, 5-Yr is up 0.3bps at 2.305%, 10-Yr is up 2.1bps at 2.719%, and 30-Yr is up 2.9bps at 3.296%.

- UK: The 2-Yr yield is up 2.6bps at 3.992%, 5-Yr is up 3.5bps at 4.153%, 10-Yr is up 4.6bps at 4.736%, and 30-Yr is up 5.4bps at 5.555%.

- Italian BTP spread up 0.8bps at 82.1bps / French OAT up 3.8bps at 85.1bps

FOREX: JPY Slide Holds, But Gains Could be Limited Above Y150

- JPY slid sharply against all others Monday in the extended response to the surprise victory for Takaichi in the LDP leadership race. Trump congratulated the new Japanese PM, setting the leaders up for their first face-to-face summit on October 28th. Ahead of Takaichi's first formal actions in government, one of her primary policy advisers Honda stated that Takaichi wants the Bank of Japan to proceed "cautiously" on interest rates, and that an October rate hike is "difficult". While the comments appeared to pressure the Bank away from tightening policy, the view that a December hike is not a problem and that the currency is approaching levels deemed too weak helped boost the JPY off lows.

- The EUR traded weaker in early Europe, following the resignation of the French PM Lecornu - and bedding markets in for an extended period of political risk and

budget brinkmanship. French equities also see weakness - with the CAC40 easily the underperformer in Europe. Next major support in EURUSD crosses at

1.1646, the late Sept low. Weakness through here snaps the weak uptrend posted off the August 1st low. - The USD's NY morning fade aided EURUSD and GBPUSD well off earlier lows, helping EURUSD almost entirely erase the PM resignation losses. EURGBP still

traded heavy, however, meaning GBPUSD's rally has the price within range of the Friday high at 1.3486. It's fiscal and political risk that's likely a more primary GBP

driver for the rest of this year - The front-end of the GBP vol curve provide a further signal for market concern over the Autumn Budget. The flatter

front-end of the curve and the building premium for 2m implied vols shows markets building a risk premium into the event. - We see GBP's driver as the fiscal policy mix ahead. The Gilt curve and, in particular, the longer-end has regained a sense of stability after being marked sharply higher at the beginning of September. How valid and long-lasting this proves to be should determine GBP/USD's ability to trade within range of 1.3525 (50% mid-Sept downleg) and make meaningful headway toward the bull trigger of the July 1st high at 1.3789.

- Australia's Westpac Consumer Confidence data is the Tuesday highlight, followed by German factory orders for August. US trade balance data was set for release Tuesday, however the extended government shutdown will keep that figure quiet for now. There remains very little pressure on either side to make concessions and rush toward a conclusion for the shutdown at this point - leaving markets with a core expectation for a further week or so of no Federal government activity.

- Various Fed speakers are due Tuesday, including Bostic, Bowman, Miran and Kashkari - who will be carefully watched for any suggestions that a prolonged government shutdown will hinder the US economy further, and require a more forceful response from the FOMC.

DATA/EVENTS CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 06/10/2025 | 2100/1700 | Kansas City Fed's Jeff Schmid | ||

| 07/10/2025 | 2330/0830 | ** | Household spending | |

| 07/10/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 07/10/2025 | 0645/0845 | * | Foreign Trade | |

| 07/10/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 07/10/2025 | 1230/0830 | ** | Trade Balance | |

| 07/10/2025 | 1230/0830 | ** | Trade Balance | |

| 07/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 07/10/2025 | 1400/1000 | * | Ivey PMI | |

| 07/10/2025 | 1405/1005 | Fed's Miki Bowman | ||

| 07/10/2025 | 1430/1030 | Fed Governor Stephen Miran | ||

| 07/10/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 07/10/2025 | 1530/1130 | Minneapolis Fed's Neel Kashkari | ||

| 07/10/2025 | 1610/1810 | ECB Lagarde Speech at Business France Event | ||

| 07/10/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 07/10/2025 | 1900/1500 | * | Consumer Credit | |

| 07/10/2025 | 2005/1605 | Fed Governor Stephen Miran | ||

| 08/10/2025 | - | Reserve Bank of New Zealand Meeting | ||

| 08/10/2025 | 2330/0830 | ** | average wages (p) | |

| 08/10/2025 | 2350/0850 | Balance of Payments | ||

| 08/10/2025 | 0100/1400 | *** | RBNZ official cash rate decision |