MNI ASIA OPEN: Focus on Midweek PPI, 3Y Note Stops Through

EXECUTIVE SUMMARY

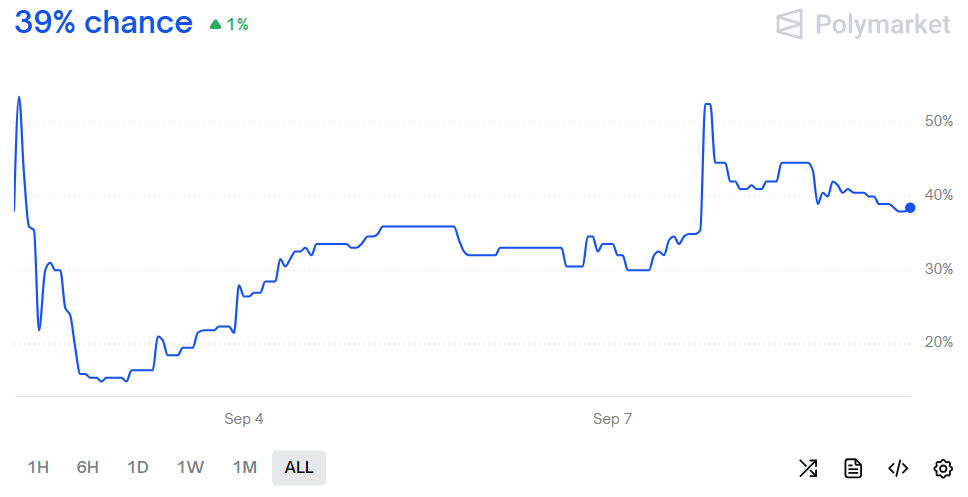

- MNI US: Govt Shutdown Risk Recedes Slightly But White House Position Remains Unclear

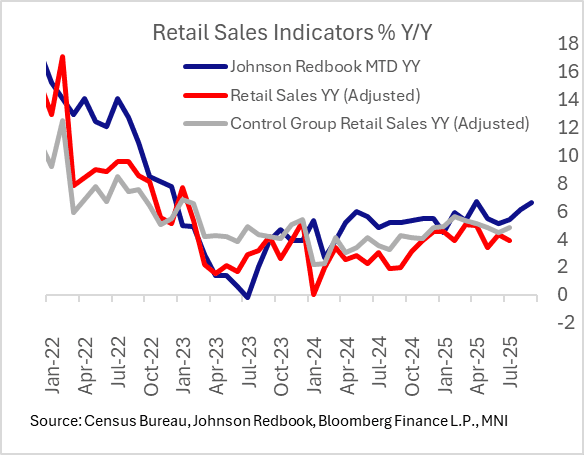

- MNI US DATA: Redbook Retail Sales Picking Up Through Q3

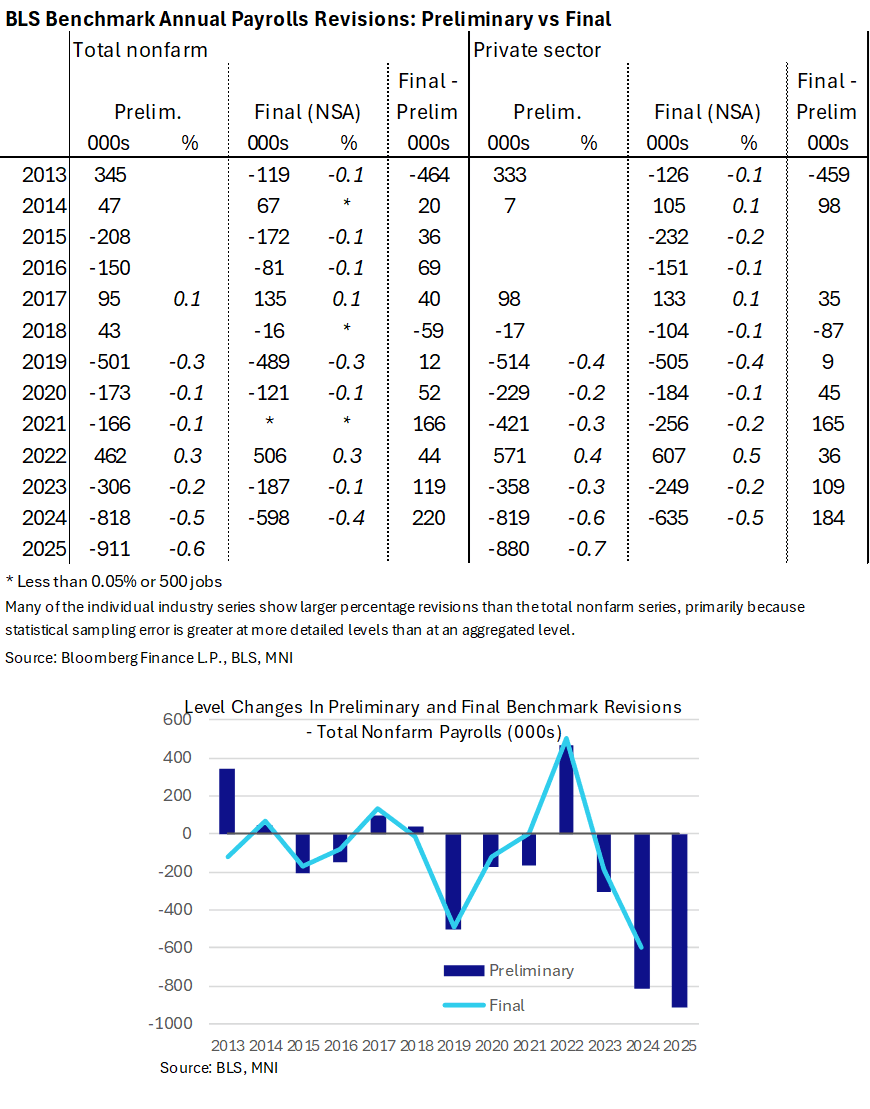

- MNI US DATA: Prelim. NFP Annual Revision More Negative Than Median But Within Ranges

- MNI US PREVIEW: Core CPI Pressures Seen Sustained In August As Goods Prices Pick Up

US

MNI US: Govt Shutdown Risk Recedes Slightly But White House Position Remains Unclear

The implied probability of a government shutdown on October 1 receded slightly after appropriators huddled yesterday for a bipartisan and bicameral meeting to discuss the funding deadline. House Democratic appropriator Rosa DeLauro (D-CT) said, “Everybody is very cognizant of the deadline.” House Majority Leader Steve Scalise (R-LA) said House leadership may let bipartisan talks go further than March, when Democrats swallowed a partisan funding extension: “We want to give [Republican appropriator Tom Cole] the latitude to get the agreement first...”

Figure 1: Government Shutdown by October 1

Source: Polymarket

NEWS

MNI US: Bessent, Vance Renew Criticism Of BLS, Fed After Downside Jobs Revision

Treasury Secretary Bessent and Vice President Vance make nearly simultaneous comments on x.com on today's 911k downward benchmark job revisions through Q1 2025, criticizing both the Fed and the Bureau of Labor Statistics. Bessent: "Now it’s official: 2024 job gains were exaggerated by nearly 1M workers, and this is on top of an already reported 577K in downward revisions. Vance: "It’s difficult to overstate how useless BLS data had become. A change was necessary ton [sic] restore confidence."

MNI SECURITY: Israel Strikes Hamas In Qatar, Likely Ends Prospect Of Diplomacy

Israel has conducted a major air strike on members of Hamas' leadership in Qatar. The strike is a significant escalation of Israeli extraterritorial operations, hitting a Gulf Cooperation Council (GCC) member for the first time. Qatar, an intermediary between Hamas and Israel, has long been viewed as a valuable conduit to ceasefire talks, despite providing diplomatic protection for Hamas officials.

MNI US: ROK: South Korean Foreign Minister Seeks Clarity On Georgia Immigration Raid

South Korean Foreign Minister Cho Hyun is in Washington today to discuss an immigration raid at a Hyundai-LG battery factory in Georgia that prompted a furious reaction in Seoul, and threatens to rupture relations with one of the most critical partners in the Trump administration’s high-tech revitalisation programme. South Korean President Lee Jae Myung told a Cabinet meeting today that he hopes this "unjust infringement" never happens again.

US TSYS

MNI US TSYS: Eyes on PPI, Cash 2s10s Remains Dis-Inverted, 3Y Stops Through

- Treasuries look to finish weaker, off late morning lows with rates paring losses after a decent $58B 3Y Note auction broke a four consecutive auction run of tails w/ 3.485% high yield vs. 3.492% WI; 2.73x bid-to-cover vs. 2.53x prior.

- After some sharp two-way action - Tsys retreated after BLS Prelim Benchmark Revision to Establishment Survey Data comes out much lower than anticipated: -911k vs. -682k est from -818k prior.

- Meanwhile, Johnson Redbook Retail Sales Index rose 6.6% Y/Y in the first week of September (ending Sep 6), running a little above retailers' targeted 6.3% gain for the month.

- Currently, the Dec'25 10Y trades -6.5 at 113-11 (yld 4.0722 +.0324) vs. 113-07 low -- Initial firm support to watch is 112-11+, the 20-day EMA. Yield curves flatter: 2s10s -2.311 at 52.831, 5s30s -1.536 at 114.416. Cash 2s10s adjusted for carry/rolldown remains dis-inverted 58.9.

- US$ off lows, BBG index BBDXY currently +2.6 at 1201.15 vs. 1196.68 post data low.

- Focus turns to US price data, as PPI and CPI releases are expected across Wednesday and Thursday respectively. China CPI and PPI figures will be released during APAC hours tomorrow.

OVERNIGHT DATA

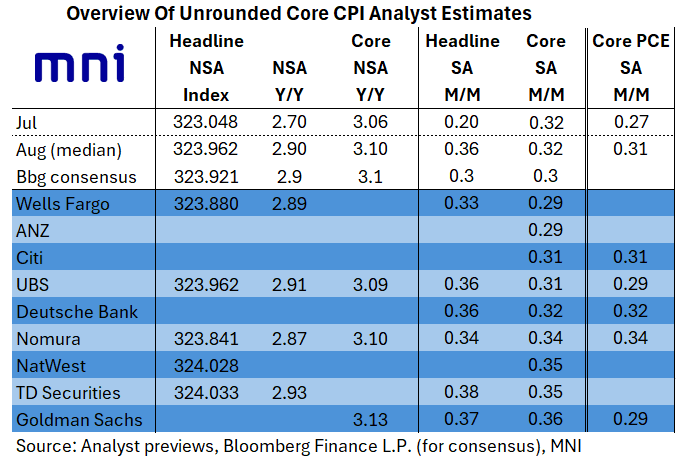

MNI US PREVIEW: Core CPI Pressures Seen Sustained In August As Goods Prices Pick Up

The following table shows the unrounded estimates we've seen so far for August's various CPI readings (release is Thursday 0830ET). We will have more detail in our full CPI preview out later Tuesday.

- Bloomberg consensus is for core CPI to come in at 0.3% M/M rounded. Unrounded core CPI expectations suggest a slight skew toward risks of a rounded-up 0.4%, with an unrounded MNI median of 0.32% and range of 0.29% to 0.36%. That would be steady from 0.32% in July for the joint-highest M/M since January.

- Early core PCE expectations largely align with core CPI views, ranging from 0.29-0.34% with a 0.31% median - pending Wednesday's PPI data which precede Thursday's CPI release.

- In terms of the category-by-category breakdown, supercore CPI is seen slowing from July's 0.48% (albeit there is a very wide range of views) with housing CPI seen relatively steady but upside pressure vs July in areas such as lodging and car insurance (airfares are also seen remaining strong).

- And core goods prices are roundly seen higher (had printed a below-expected 0.21% in Jul), with vehicle prices seen driving much of the upside, and tariff-impacted categories like apparel seen accelerating in the month.

MNI US DATA: Prelim. NFP Annual Revision More Negative Than Median But Within Ranges

The BLS preliminary estimate for the annual payrolls benchmark revision. Analyst estimates were wide-ranging but we estimated a median of -750k, mainly in a range of -500k to -1mn (sometimes given as a similar range by each analyst, for example Goldman Sachs saw between -550k and -950k) but with Barclays more pessimistic still with -1.1-1.3mn.

- This compares with last year’s preliminary estimate of -818k before the -598k in the actual benchmark revision published with the January monthly payrolls report released in February.

- Taking these revisions at face value (which history suggests is likely overly negative), the average pace of monthly payrolls growth of 147k in the twelve months to Mar 2025 would have been 71k.

- As for private payrolls, the -880k preliminary downward revision implies average monthly private payrolls growth would be revised down from 122k to 49k.

- Beware extrapolating this monthly downward revision to the three-month average in seasonally adjusted payrolls growth of 29k as of August (private payrolls also 29k), but the risk is certainly on payrolls growth to have been even weaker than currently estimated.

MNI US DATA: Redbook Retail Sales Picking Up Through Q3

The Johnson Redbook Retail Sales Index rose 6.6% Y/Y in the first week of September (ending Sep 6), running a little above retailers' targeted 6.3% gain for the month. If sustained, this rate of sales would mark an acceleration from 6.1% in August and would be just below April's 6.7% for the 2nd-highest monthly growth since 2022.

- While reminding of the usual caveat that this is in nominal terms so may reflect ongoing tariff-related goods price inflation, the same can be said for Census Bureau retail sales data (for which the August release is on Sep 16, currently seen at +0.3% M/M for headline and 0.5% ex-auto/gas; the latter would imply the fastest Y/Y growth in 5 months at 4.9%).

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 177.47 points (0.39%) at 45694.06

S&P E-Mini Future up 10.25 points (0.16%) at 6516.5

Nasdaq up 56.7 points (0.3%) at 21856.03

US 10-Yr yield is up 4 bps at 4.0799%

US Dec 10-Yr futures are down 8/32 at 113-9.5

EURUSD down 0.0058 (-0.49%) at 1.1705

USDJPY down 0.05 (-0.03%) at 147.45

WTI Crude Oil (front-month) up $0.46 (0.74%) at $62.72

Gold is down $2.23 (-0.06%) at $3634.01

European bourses closing levels:

EuroStoxx 50 up 6.01 points (0.11%) at 5368.82

FTSE 100 up 21.09 points (0.23%) at 9242.53

German DAX down 88.68 points (-0.37%) at 23718.45

French CAC 40 up 14.55 points (0.19%) at 7749.39

US TREASURY FUTURES CLOSE

3M10Y +3.739, 4.711 (L: 0.509 / H: 6.014)

2Y10Y -2.165, 52.977 (L: 52.418 / H: 56.196)

2Y30Y -2.957, 117.419 (L: 116.844 / H: 122.136)

5Y30Y -1.446, 111.506 (L: 111.092 / H: 115.203)

Current futures levels:

Dec 2-Yr futures down 3.5/32 at 104-12.75 (L: 104-12.625 / H: 104-16.875)

Dec 5-Yr futures down 5.75/32 at 109-25.75 (L: 109-24.5 / H: 110-02)

Dec 10-Yr futures down 8/32 at 113-9.5 (L: 113-07 / H: 113-20)

Dec 30-Yr futures down 13/32 at 117-1 (L: 116-25 / H: 117-14)

Dec Ultra futures down 21/32 at 120-11 (L: 120-00 / H: 121-00)

MNI US 10YR FUTURE TECHS: (Z5) Bull Cycle Remains In Play

- RES 4: 114-10 High Apr 7 (cont.)

- RES 3: 114-00 Round number resistance

- RES 2: 113-26+ 2.764 proj of the Jul 15 - 22 - 28 price swing

- RES 1: 113-21+ High Sep 5

- PRICE: 113-08 @ 1300 ET Sep 9

- SUP 1: 112-28+/112-11+ Low Sep 5 / 20-day EMA

- SUP 2: 111-26+ 50-day EMA

- SUP 3: 111-13+ Low Aug 18 and a key support

- SUP 4: 110-25 Low Aug 1

Treasury futures rallied sharply higher last Friday and the contract remains closer to its recent highs The move higher highlights an acceleration of the uptrend. Note too that moving average studies are in a bull-mode position, highlighting a dominant uptrend. This paves the way for an extension through 113-21 next (pierced), the 2.618 projection of the Jul 15 - 22 - 28 price swing. Initial firm support to watch is 112-11+, the 20-day EMA.

SOFR FUTURES CLOSE

Sep 25 -0.023 at 95.970

Dec 25 -0.055 at 96.330

Mar 26 -0.080 at 96.570

Jun 26 -0.080 at 96.825

Red Pack (Sep 26-Jun 27) -0.075 to -0.045

Green Pack (Sep 27-Jun 28) -0.04 to -0.03

Blue Pack (Sep 28-Jun 29) -0.025 to -0.02

Gold Pack (Sep 29-Jun 30) -0.02 to -0.015

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.40% (-0.02), volume: $2.872T

- Broad General Collateral Rate (BGCR): 4.39% (-0.01), volume: $1.151T

- Tri-Party General Collateral Rate (TCR): 4.39% (-0.01), volume: $1.120T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $110B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $215B

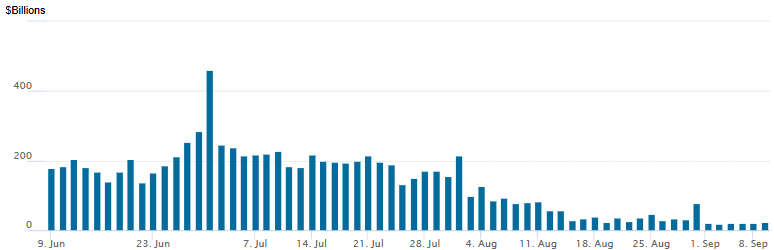

FED Reverse Repo Operation

RRP usage rebounds to $22.915B with 15 counterparties this afternoon from $19.416B Monday. Compares to $17.923B on Wednesday, Sep 3 - the lowest levels since early April 2021. This year's high usage of $460.731B occurred on June 30.

MNI PIPELINE: Corporate Bond Update: $1.5B Raymond James 2Pt Launched

- Date $MM Issuer (Priced *, Launch #)

- 09/09 $2.5B #Repsol E&P Capital $500M 3Y +130, $1B 5Y +160, $1Y 10Y +190

- 09/09 $2.05B *NCL Corp $1.025B each: 5.25NC2 5.875%, 8NC3 6.25%

- 09/09 $2B #Turkiye Govt International Bond 10Y 7%

- 09/09 $1.5B #Raymond James $650M 10Y +85, $850M 30Y +95

- 09/09 $1B *Korea Development Bank 5Y SOFR+64

- 09/09 $750M #Huntington Bancshares PerpNC5 6.25%

- 09/09 $650M #NBN Co 5Y +60

- 09/09 $600M UWM Holdings 5.5NC2.5

- 09/09 $500M #Met Tower 5Y +65

- 09/09 $Benchmark Stellantis 3Y +145, 3Y SOFR+169, 5Y +180

- 09/09 $Benchmark DTE Energy 3Y +57, 10Y +102

- Expected Wednesday:

- 09/10 $3B KFW 3Y SOFR+33a

- 09/10 $1B Federal Home Loan 2Y +4

- 09/09 $Benchmark IDA (International Development Association) 7Y SOFR+57a

MNI BONDS: EGBs-GILTS CASH CLOSE: Rally Takes A Breather Ahead Of ECB

European yields rose modestly Tuesday, with some of the bull flattening seen over the past week taking a breather.

- Gilt and Bund yields gapped higher on the open, but largely traded within recent ranges in the morning session. Gilts outperformed Bunds early, in part helped by a strong 20Y UK auction.

- With European data (including French industrial production and UK BRC shop sales) not proving impactful, attention was on US benchmark payroll revisions.

- The latter delivered a bigger downward revision to payrolls through Q1 2025, triggering a rally for global core FI upon release (10Y Gilt yields briefly hit a fresh post-Aug 14th low).

- But the move slowly reversed as the revision was within a broad range of analyst forecasts and attention swiftly turned to US inflation data coming Wednesday and Thursday.

- Both the German and UK curves bear steepened modestly, with periphery/EGB spreads mixed (OATs outperformed).

- The week's European focus is Thursday's ECB decision. MNI's preview went out today (here): there appears to be little to no appetite for a September rate cut amongst ECB Governing Council members but we suspect there still an underlying easing bias.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.5bps at 1.941%, 5-Yr is up 1.6bps at 2.225%, 10-Yr is up 1.7bps at 2.659%, and 30-Yr is up 1.6bps at 3.28%.

- UK: The 2-Yr yield is up 1.1bps at 3.914%, 5-Yr is up 1.4bps at 4.037%, 10-Yr is up 1.8bps at 4.623%, and 30-Yr is up 1.8bps at 5.477%.

- Italian BTP spread down 0.8bps at 82.1bps / French OAT down 2.6bps at 81.0bps

MNI FOREX: USD Index Moderately Higher after Volatile Session

- USDJPY volatility led a whippy session in global currency markets, as market participants digested a deeply negative NFP annual revision but also await significant PPI and CPI releases, due later in the week.

- Initial USDJPY downside momentum was prompted by a set of hawkish comments from the BOJ, indicating there is a "chance of" a hike this year despite the political turmoil following PM Ishiba's resignation Sunday. "Some officials are even of the view that a hike might be appropriate as early as October", the Bloomberg article added. USDJPY reached as low as 146.31, trading within 10 pips of key short-term support.

- Intra-day positioning dynamics may have then fostered a bounce as the market awaited the BLS payrolls revision, with USDJPY trading closer to 147 ahead of the release. Despite a quick dip back down to 146.53, spot has subsequently been grinding higher and currently stands around 147.25 ahead of the APAC crossover.

- Dollar strength has been most notable against the Euro, with EURUSD slipping 0.35% to 1.1720. Lingering French political risks will likely be dampening topside momentum for the single currency. Short-term parameters for EURUSD appear well defined at 1.1829 (Jul 01 high and bull trigger) and 1.1625 (50-day EMA support).

- Price action for the likes of AUD and NZD has been much more contained, particularly allowing AUDUSD to consolidate close to the highest levels of the year, located at 0.6625. In similar vein, GBPUSD sits just 0.09% lower on the day as the pair’s strong technical recovery consolidates. Early strength saw GBPUSD trade within 5 pips of resistance at 1.3595, the Aug 14 high and a bull trigger. This remains the key short-term hurdle for a stronger bounce.

- Focus turns to US price data, as PPI and CPI releases are expected across Wednesday and Thursday respectively. China CPI and PPI figures will be released during APAC hours tomorrow.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 10/09/2025 | 0600/0800 | *** | CPI Norway | |

| 10/09/2025 | 0600/0800 | ** | Private Sector Production m/m | |

| 10/09/2025 | 0700/0900 | ** | Industrial Production | |

| 10/09/2025 | 0800/1000 | * | Industrial Production | |

| 10/09/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 10/09/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 10/09/2025 | 1145/1345 | SNB's Schlegel on Central Bank Communication in Vezia | ||

| 10/09/2025 | - | *** | Money Supply | |

| 10/09/2025 | - | *** | New Loans | |

| 10/09/2025 | - | *** | Social Financing | |

| 10/09/2025 | 1230/0830 | *** | PPI | |

| 10/09/2025 | 1230/0830 | *** | PPI | |

| 10/09/2025 | 1400/1000 | ** | Wholesale Trade | |

| 10/09/2025 | 1400/1000 | ** | Wholesale Trade | |

| 10/09/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 10/09/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 10/09/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 11/09/2025 | - | European Central Bank Meeting |