MNI ASIA OPEN: Fed Barkin: Tariff Clarity Will Take a While

EXECUTIVE SUMMARY

- MNI TARIFFS: Japan, China, ROK Signal Closer Cooperation Ahead Of US Tariffs

- MNI EU-RUSSIA: G5 Plus: Willing To Put More Pressure On Russia, Inc. New Sanctions

- MNI US: Senate Republicans Aim To Adopt Compromise Budget Resolution This Week

- MNI FRANCE: Le Pen Barred From Running In 2027 Election

- MNI US DATA: Uncertainty (And Prices) Still Rising In Texas Manufacturing Sector

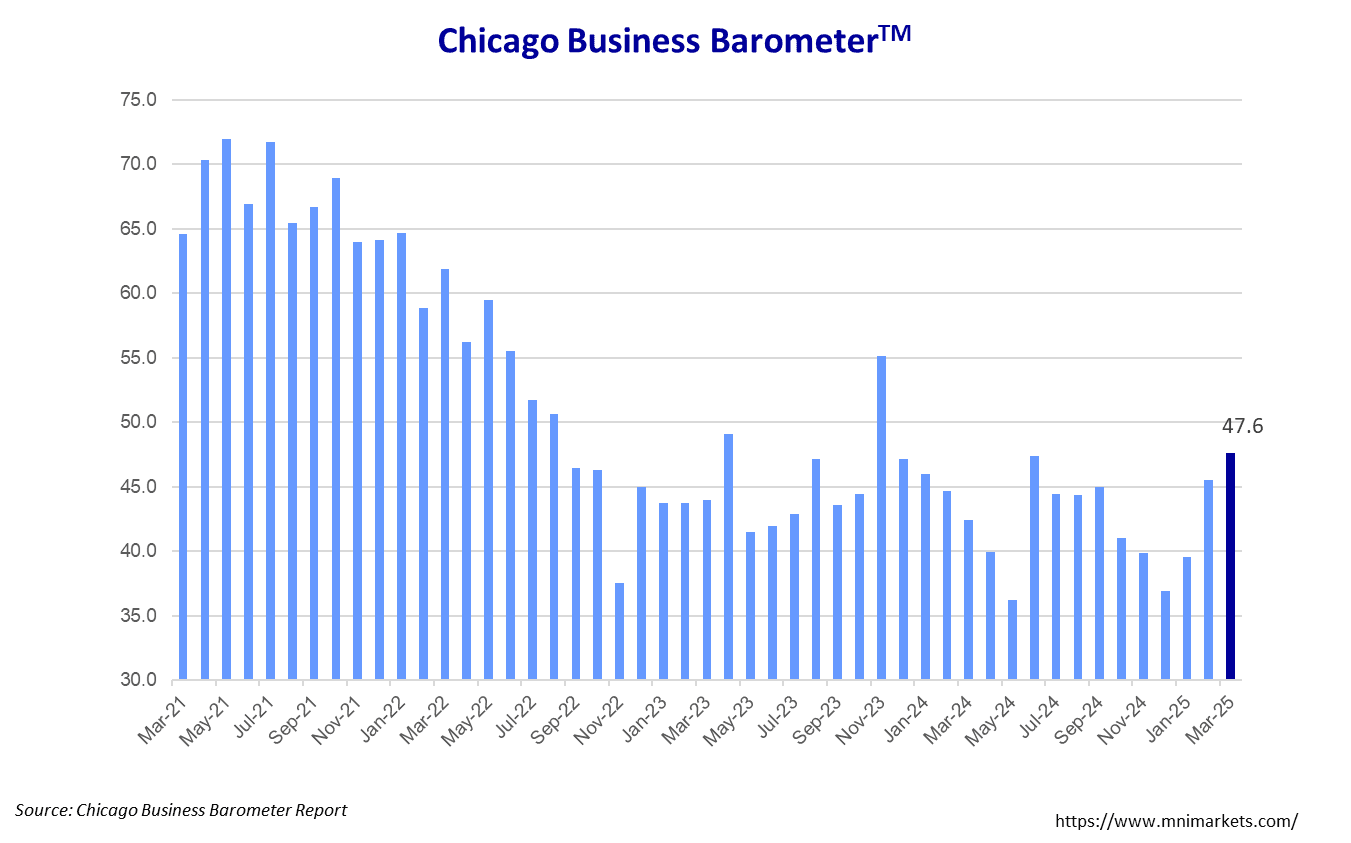

- MNI US DATA: Chicago Business Barometer™ - Advances to 47.6 in March

US

MNI US: MNI POLITICAL RISK - Markets Brace For 'Liberation Day' Tariffs

- President Donald Trump has two Executive Order signing ceremonies on his agenda today. Multiple reports suggest that Trump may be pressing his team to devise an aggressive 'Liberation Day' tariff plan that applies to more countries than anticipated.

- Trump’s trade advisor, Peter Navarro, said tariffs could net the Treasury Department $600 billion a year for a decade. Trump is reportedly considering letting income taxes on the “very highest earners” rise in return for cutting taxes on tips.

- Trump is considering applying secondary tariffs on countries that buy Russian oil if he determines Russian President Vladimir Putin is attaching unreasonable demands to ceasefire negotiations.

- The Senate is expected to vote on Tuesday on a Democratic resolution to undo Trump’s tariffs on Canadian goods. Senate Republicans are expected to begin procedural votes on a compromise budget resolution as soon as Wednesday.

NEWS

MNI TARIFFS: Japan, China, ROK Signal Closer Cooperation Ahead Of US Tariffs

Reuters reporting, per Chinese state media, that China, Japan, and South Korea have reached “consensus" that the three will "jointly respond to the US tariffs.” All three have lobbied the Trump administration for exceptions from Trump's metals and auto tariffs without success.

- The report notes that Tokyo and Seoul are, “seeking to import semiconductor raw materials from China," and China is "interested in purchasing chip products from Japan, South Korea”.Finbarr Bermingham at SCMP cautions that while the joint statement mentions cooperation on export controls and chips, "There's no detail on there about a joint response to Trump's reciprocal tariffs."

- The Korean Economic Daily noted yesterday that a meeting of trade ministers, “marked the first time that the economic ministers of the three countries sat down to discuss policy cooperation since December 2019 in Beijing."

MNI EU-RUSSIA: G5 Plus: Willing To Put More Pressure On Russia, Inc. New Sanctions

A meeting of foreign ministers from the so-called 'G5+' group (France, Germany, Italy, Poland, UK, Spain and the EU, more commonly known as the Weimar+ group) has taken place in the Spanish capital, Madrid. The post-meeting comments have sought to maintain a hard-line stance against Russia and in support of Kyiv, but it remains to be seen whether these European countries will have any notable impact on the future of peace talks given the US' preference for direct conversations with Russia. G5 Plus: "We are willing to exert more pressure on Russia, including new sanctions."

MNI US: Senate Republicans Aim To Adopt Compromise Budget Resolution This Week

Senate Republicans are expected to begin procedural work on a compromise budget resolution to underpin President Donald Trump’s reconciliation agenda as soon as Wednesday. The Senate could follow with a ‘vote-a-rama’ on Thursday, allowing the Senate to adopt a budget by Friday and synch up with the House to unlock reconciliation - the process to pass Trump's agenda along party lines.

MNI FRANCE: Le Pen Barred From Running In 2027 Election

After being found guilty of embezzlement, far-right Rassemblement National (National Rally, RN) figurehead Marine Le Pen has been declared immediately ineligible to run for public office. The ban is for five years, upending the 2027 presidential election in which she was the early frontrunner. Le Pen left the courtroom before her full sentence was read out (she was also fined EUR100k and sentenced to four years in prison (two suspended) that can be served with an ankle monitor). There will undoubtedly be an appeal, but following a constitutional court ruling earlier in the month, Le Pen will remain barred from running for office during the appeal. As such, unless her appeal is successful and swift, the RN will have to find another candidate to run in the 2027 presidential election.

MNI US TSYS: Month End Rebalancing Tempered Early Tariff Positioning

- Treasuries look to finish mildly higher - well off early morning highs as month/quarter end rebalancing flow tempered Monday morning's risk-off support ahead of Wednesday's US tariff deadline.

- Multiple reports suggest that Trump may be pressing his team to devise an aggressive 'Liberation Day' tariff plan that applies to more countries than anticipated. Stocks opened broadly weaker, but have been consolidating since midmorning amid month end positioning trade desks said.

- Little react to to slightly higher than expected Chicago PMI data, the barometer advancing 2.1 points to 47.6 in March. This is the third consecutive monthly gain, taking the index to its highest level since November 2023, though it remains in contractionary territory for the sixteenth successive month.

- Little new from late session Fed speakers Williams and Barkin: "need an open mind how long tariff impacts last" Williams said, while "to cut rates, got to have confidence on inflation".

- Tsy Jun'25 10Y futures trades 111-10.5 (+4) -- well off initial technical resistance of 111-22.5 (today's intraday high) -- next resistance above at 112-01 (High Mar 4 and a bull trigger), curves mildly flatter: 2s10s -1.269 at 32.276, 5s30s -2.300 at 62.471.

- Cross asset: Stocks near highs (SPX eminis at 5650.0 vs. 5533.75 low), Gold making new highs over 3122.0, Bbg US$ index climbing higher at 1274.25 (+2.38).

OVERNIGHT DATA

MNI US DATA: Chicago Business Barometer™ - Advances to 47.6 in March

The Chicago Business Barometer™, produced with MNI advanced 2.1 points to 47.6 in March. This is the third consecutive monthly gain, taking the index to its highest level since November 2023, though it remains in contractionary territory for the sixteenth successive month.

- The increase was largely driven by a rise in Production, with smaller increases in Employment, Order Backlogs and New Orders also contributing whilst Supplier Deliveries declined.

- Production increased 8.8 points to 55.5, to the highest since December 2023, taking it into expansionary territory for the first time since June 2024.

- New Orders saw a minor 0.4 point rise, with the subindex last higher than this in November 2023.

- Employment lifted 0.9 points to 37.2, only a marginal improvement from January 2025 which had recorded the lowest level since June 2020.

- Order Backlogs progressed by 0.7 points, remaining the highest since September 2024.

- Supplier Deliveries dipped 2.0 points.

- Inventories fell 6.5 points to the lowest level since March 2020.

- Prices Paid edged down a marginal 0.4 points to 76.7, keeping the reading the second highest print since August 2022. No respondents reported lower prices for the second consecutive month.

MNI US DATA: Uncertainty (And Prices) Still Rising In Texas Manufacturing Sector

The Dallas Fed's Texas Manufacturing Outlook Survey for March was mixed, with sentiment worsening but current activity seemingly solid. As with the other regional Fed manufacturing surveys for March, readings have retreated sharply from the post-November election highs as uncertainty over tariffs and the demand outlook in general have set in, while inflation looks to be picking up sharply.

- The most closely-watched indicator in the Dallas Fed survey, the general business activity index, unexpectedly retreated further to an 8-month low -16.3, (-5.0 expected, -8.3 prior). However the Dallas Fed highlights that the production index rose 15 points to 6.0, effectively meaning factory activity rose in March after falling in February.

- This divergence potentially reflects activity front-running tariffs even as the outlook deteriorates.

- New orders ticked 3.6 points higher to -0.1, well below the January multi-year high of 7.7 but appearing to be off the lows.

- The outlook for production six months ahead dipped 0.7pp to 27.6, a fresh 10-month low but essentially steady after plummeting 16.5 points in February.

- And "outlook uncertainty" rose 7 points to 36.2, highest since Oct 2022.

- Worryingly from an inflation perspective, prices paid hit a fresh high 37.7 (up 2.7 points, highest since mid-2022), with prices received dipping slightly to 6.3. While expected prices paid/received pulled back slightly, these were off 2022 highs and remain elevated on a historical basis.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 409.44 points (0.98%) at 41998.04

S&P E-Mini Future up 24.75 points (0.44%) at 5649

Nasdaq down 67 points (-0.4%) at 17259.21

US 10-Yr yield is down 2.5 bps at 4.2244%

US Jun 10-Yr futures are up 4/32 at 111-10.5

EURUSD down 0.0011 (-0.1%) at 1.0817

USDJPY up 0.17 (0.11%) at 150.01

WTI Crude Oil (front-month) up $2.19 (3.16%) at $71.57

Gold is up $37.51 (1.22%) at $3122.55

European bourses closing levels:

EuroStoxx 50 down 83.01 points (-1.56%) at 5248.39

FTSE 100 down 76.04 points (-0.88%) at 8582.81

German DAX down 298.03 points (-1.33%) at 22163.49

French CAC 40 down 125.37 points (-1.58%) at 7790.71

US TREASURY FUTURES CLOSE

3M10Y -2.968, -7.711 (L: -14.209 / H: -4.451)

2Y10Y -0.859, 32.686(L: 31.828 / H: 35.286)

2Y30Y -2.128, 69.336 (L: 68.578 / H: 74.318)

5Y30Y -2.203, 62.568 (L: 62.18 / H: 67.406)

Current futures levels:

Jun 2-Yr futures up 0.75/32 at 103-19.625 (L: 103-17.875 / H: 103-23.375)

Jun 5-Yr futures up 1.5/32 at 108-7.5 (L: 108-03 / H: 108-16.5)

Jun 10-Yr futures up 4.5/32 at 111-11 (L: 111-04 / H: 111-22.5)

Jun 30-Yr futures up 15/32 at 117-18 (L: 117-03 / H: 118-02)

Jun Ultra futures up 27/32 at 122-21 (L: 121-31 / H: 123-09)

MNI US 10YR FUTURE TECHS: (M5) Sights Are On Key Resistance

- RES 4: 112-23+ 1.618 proj of the Jan 13 - Feb 7 - Feb 12 price swing

- RES 3: 112-13 1.500 proj of the Jan 13 - Feb 7 - Feb 12 price swing

- RES 2: 112-01 High Mar 4 and a bull trigger

- RES 1: 111-22+ Intraday high

- PRICE: 111-06 @ 1355 ET Mar 31

- SUP 1: 110-21+ 20-day EMA

- SUP 2: 110-08/06 50-day EMA / Low Mar 27

- SUP 3: 110-00 High Feb 7 and a key support

- SUP 4: 109-18+ Trendline support drawn from the Jan 13 low

Treasury futures are trading higher today, as the contract starts the week on a bullish note. This marks an extension of the recovery from last week’s low of 110-06+ (Mar 27). Attention is on key resistance at 112-01, the Mar 4 high. A break of this level would confirm a resumption of the uptrend that started Jan 13, and open 112-13, a Fibonacci projection. Initial support to watch is 110-21+, the 20-day EMA.

SOFR FUTURES CLOSE

Jun 25 -0.015 at 95.920

Sep 25 +0.005 at 96.20

Dec 25 +0.010 at 96.385

Mar 26 +0.010 at 96.505

Red Pack (Jun 26-Mar 27) steadysteady0 to +0.010

Green Pack (Jun 27-Mar 28) steadysteady0 to +0.015

Blue Pack (Jun 28-Mar 29) +0.020 to +0.035

Gold Pack (Jun 29-Mar 30) +0.035 to +0.050

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00127 to 4.32365 (+0.00354/wk)

- 3M -0.00156 to 4.29761 (-0.00022/wk)

- 6M -0.00099 to 4.21561 (+0.01095/wk)

- 12M -0.00594 to 4.05286 (+0.02948/wk)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.34% (-0.02), volume: $2.440T

- Broad General Collateral Rate (BGCR): 4.34% (-0.01), volume: $946B

- Tri-Party General Collateral Rate (TCR): 4.33% (-0.01), volume: $915B

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $112B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $286B

FED Reverse Repo Operation

RRP usage surges to highest level since December 31, 2024: just under $400B to $399.167B this afternoon from $286.575B Friday. Compares to $58.770B (lowest level since mid-April 2021) on February 14. The number of counterparties at jumps to 66 from 45.

MNI PIPELINE: Corporate Bond Update: Issuers Sidelined Ahead April 2 Tariff Deadline

- Date $MM Issuer (Priced *, Launch #)

- 03/31 $Benchmark Japan Tobacco +3Y, +5Y, +10Y investor calls

- 03/31 $Benchmark Gold Fields 10Y investor calls

- 03/31 $Benchmark Caf perpNC5.5 investor calls

- Expected Tuesday:

- 04/01 $Benchmark Kommunalbanken Norway 4Y SOFR+41a

- 04/01 $Benchmark NRW Bank 5Y SOFR+49a

- 03/31 $Benchmark DBJ 5Y SOFR+62a

MNI BONDS: EGBs-GILTS CASH CLOSE: Core Short-Ends Underperform

Bunds underperformed Gilts Monday as an early flight to safety reversed.

- Core FI started strong, as risk aversion picked up following weekend reports that the US could impose more onerous tariffs this week than had been hoped.

- Flash March Euro inflation data were mixed, compared with Friday's below-expected Spanish and French readings: Italy's were above consensus while Germany's (starting with the state-level releases) CPI was broadly in-line.

- The day's rally reversed after a Bloomberg ECB sources piece pointed to increasing appetite among some on the Governing Council for an April rate hold. Cut pricing was pared sharply to around 65% from 85%, impacting EGBs across the curve with Bunds hitting session lows.

- Both the German and UK curves twist flattened on the day.

- Periphery EGB spreads were wider, while French OATs underperformed in semi-core, on a day the RN's Le Pen was deemed ineligible for election.

- Tuesday's schedule includes final March manufacturing PMIs (including the only readings for Spain and Italy), and the flash estimate of March Eurozone HICP. We also hear from multiple central bankers including BOE's Greene, and ECB's Lagarde / Lane.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 2.7bps at 2.047%, 5-Yr is up 1.9bps at 2.339%, 10-Yr is up 1.1bps at 2.738%, and 30-Yr is down 1.2bps at 3.09%.

- UK: The 2-Yr yield is up 0.1bps at 4.196%, 5-Yr is down 1.4bps at 4.284%, 10-Yr is down 1.9bps at 4.675%, and 30-Yr is down 0.6bps at 5.282%.

- Italian BTP spread up 0.7bps at 112.9bps / French OAT up 2bps at 72.5bps

MNI FOREX: AUD and NZD Remain Weakest in G10, USDJPY Has Strong Reversal Higher

- Despite the initial USD Index weakness from the open, weighed by the aggressive move lower for USDJPY, the DXY then edged steadily higher through European trade and into the US session. This has culminated in 0.15% gains for the DXY overall.

- USDJPY had initially been very reactive to the waning sentiment for US equities, and the initial dip lower for US yields. However, a solid recovery for equities and yields climbing back to unchanged prompted an impressive USDJPY reversal, to trade positive on the day around 150.00 as we approach the APAC crossover.

- The broad dollar strength worsened the intra-day performance for AUD (-0.68%) and NZD (-0.77%), which although off worst levels, remain comfortably the weakest in G10. For AUDUSD, we continue to narrow the gap to a key short-term support at 0.6187, the Mar 4 low. Importantly, clearance of this level would reinstate a bearish technical theme for the pair.

- Downside momentum picked up for NZDUSD on a break of a cluster of lows around 0.5710, and the intra-day fall now totals 1.10%. 0.5600 remains a key psychological pivot for the pair, while the medium-term target for the move remains at 0.5512.

- In emerging markets, similar sentiment is being felt by MXN, where intra-day weakness has been unperturbed by the latest bounce for major US equity indices. USDMXN traded to a fresh high of 20.4736 as the tariff deadline nears and investors continue to assess the dovish rhetoric from the Banxico committee.

- The Tuesday economic calendar is busy, with both the RBA decision and Japan’s Tankan survey highlights in APAC. Focus then turns to Eurozone inflation readings, before ISM Manufacturing and JOLTS data headline the US schedule.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 01/04/2025 | 0630/0830 | ** | Retail Sales | |

| 01/04/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 01/04/2025 | 0745/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 01/04/2025 | 0750/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 01/04/2025 | 0755/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 01/04/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 01/04/2025 | 0815/0915 | BoE's Greene on ‘UK MP/macro conjuncture’ | ||

| 01/04/2025 | 0820/1020 | ECB's Cipollone At Croatian National Bank Meeting | ||

| 01/04/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 01/04/2025 | 0900/1100 | *** | HICP (p) | |

| 01/04/2025 | 0900/1100 | ** | Unemployment | |

| 01/04/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 01/04/2025 | 1230/1430 | ECB's Lagarde At AI Conference | ||

| 01/04/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 01/04/2025 | 1300/0900 | Richmond Fed's Tom Barkin | ||

| 01/04/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 01/04/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 01/04/2025 | 1400/1000 | * | Construction Spending | |

| 01/04/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 01/04/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 01/04/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 01/04/2025 | 1530/1130 | * | US Treasury Auction Result for Cash Management Bill | |

| 01/04/2025 | 1630/1830 | ECB's Lane At AI Conference | ||

| 02/04/2025 | 0030/1130 | * | Building Approvals |