MNI ASIA OPEN: Eyes On CPI

MNI (NEW YORK) -

EXECUTIVE SUMMARY

- TARIFFS: Trump Extends China Tariff Deadline By 90 Days: CNBC

- Bessent Expands Fed Chair Search to Bowman, Jefferson and Logan (BBG)

- MNI US CPI Preview: High Early Bar To September Fed Hold

- MNI UK Labour Market Data Preview: August 2025 Release

- MNI: Greek 2026 New Issuance Lower End Of EUR8-10 Bln-Source

NEWS

TARIFFS: Trump Extends China Tariff Deadline By 90 Days: CNBC

CNBC reports (link): "President Donald Trump has signed an executive order that will prevent U.S. tariffs on Chinese goods from snapping back to near-embargo levels for another 90 days, a White House official told CNBC on Monday." There is limited market reaction to the news as it had been flagged by administration officials (including Commerce Secretary Lutnick last week) with Trump noting this morning that while "we'll see what happens" re an extension, "the relationship is very good with President Xi and myself".

FED - Bessent Expands Fed Chair Search to Bowman, Jefferson and Logan (Bloomberg)

The Federal Reserve’s two vice chairs, Michelle Bowman and Philip Jefferson, and Dallas Fed President Lorie Logan are under consideration to serve as chair of the central bank when the position opens next year, according to two administration officials. Treasury Secretary Scott Bessent, who is running the search, will interview additional candidates in the coming weeks, said the officials, who were granted anonymity to speak candidly about the process. The president is expected to make his final announcement this fall, they said.

MNI US CPI Preview: High Early Bar To September Fed Hold

The CPI report for July is released on Tuesday Aug 12, at 0830ET. Consensus sees core CPI inflation at a seasonally adjusted 0.3% M/M in June and unrounded analyst estimates broadly echo this with a median 0.32% M/M. It would mark a further acceleration from 0.23% M/M in June and 0.13% M/M in May for its fastest pace since January, with the latest firming seen coming from core goods inflation doubling to 0.4% M/M.

MNI UK Labour Market Data Preview: August 2025 Release

With a continually softening labour market a necessity for another quarterly cut in November, Tuesday’s report will be keenly watched by the market. Unlike last month’s release there is no obvious smoking gun to watch out for as the revision to the flash payrolls print for June has returned the focus back to the wider report. Our primary focus therefore will return to private regular average earnings which are expected at 4.8%Y/Y in the 3-months to June based on the MNI median and Bloomberg consensus (vs 4.88% prior).

MNI: Greek 2026 New Issuance Lower End Of EUR8-10 Bln-Source

Greece’s funding plans for 2026 will probably include EUR 8-10 billion of new issuance, with the lower end of the range more likely, a source from the Greek treasury told MNI, adding that this year the country has already raised EUR7.5 billion of the target of EUR8 billion.

MNI BRIEF: Unanchored Expectations Need Vigilance-BCB Galipolo

Central Bank of Brazil governor Gabriel Galipolo said Monday that unanchored expectations demand "vigilance" and will require maintaining interest rates at a very restrictive level for a prolonged period, adding that monetary policy transmission channels are functioning effectively.

MNI INTERVIEW: BCB To Hold Rates Until Q1 2026 - Le Grazie

The Central Bank of Brazil is likely to hold its interest rate until at least the first quarter of 2026, before beginning an easing cycle, possibly at its April meeting, former Deputy Governor for Monetary Policy Reinaldo Le Grazie told MNI.

UKRAINE: Elysee Confirms 'Coalition Of The Willing' Meeting Ahead Of Putin-Trump

The Elysee Palace confirms that French President Emmanuel Macron, German Chancellor Friedrich Merz and UK PM Sir Keir Starmer will hold a meeting of the 'Coalition of the Willing' ahead of the planned meeting between presidents Vladimir Putin and Donald Trump on 15 August. The Elysee notes that the meeting of the 'Coalition of the Willing' comes on the same day as those in other formats taking place.

US TSYS: Leaning Bull Flatter Ahead Of CPI

The Treasury curve leaned bull flatter Monday ahead of Tuesday's CPI release.

- With no key data or Fed speakers on Monday's schedule, and looming CPI being the week's most impactful release, trading was relatively subdued and focused more on geopolitical developments.

- That included anticipation of the Trump-Putin meeting later this week per the Ukraine conflict, and the China tariff truce which was due to expire Tuesday (but per CNBC has been extended by 90 days as widely expected).

- In contrast to last week's reports which drew a small but notable reaction (namely firming the USD), there was little reaction to a Bloomberg report that current FOMC members Vice Chair for Supervision Bowman, Vice Chair Jefferson, and Dallas Fed's Logan are in the running to succeed current Fed Chair Powell.

- Indeed Bowman's comments over the weekend re eyeing 3 rate cuts by year-end were largely taken in stride as she's been a vocal (and dissenting) dove in recent months.

- Implied Fed funds were unchanged through year-end, still eyeing 57bp of cuts. Tsy yields traded within Friday's ranges overall, with volumes light (725k TYU5 contracts traded through 3:45ET)

- As noted, Friday sees a busier schedule including CPI - MNI's preview is here. Consensus sees core CPI inflation at 0.3% M/M and unrounded analyst estimates broadly echo this with a median 0.32% M/M. We also hear from Fed's Barkin (non-2025 voter) and Schmid (2025 voter, hawk) after CPI, with other data including the NFIB small business survey and the Federal budget statement.

- Latest levels: The 2-Yr yield is down 0.4bps at 3.758%, 5-Yr is down 0.7bps at 3.8242%, 10-Yr is down 1.2bps at 4.2713%, and 30-Yr is down 0.9bps at 4.8403%. Sep 10-Yr futures (TY) up 1.5/32 at 111-28 (L: 111-25 / H: 112-0-)

OVERNIGHT DATA

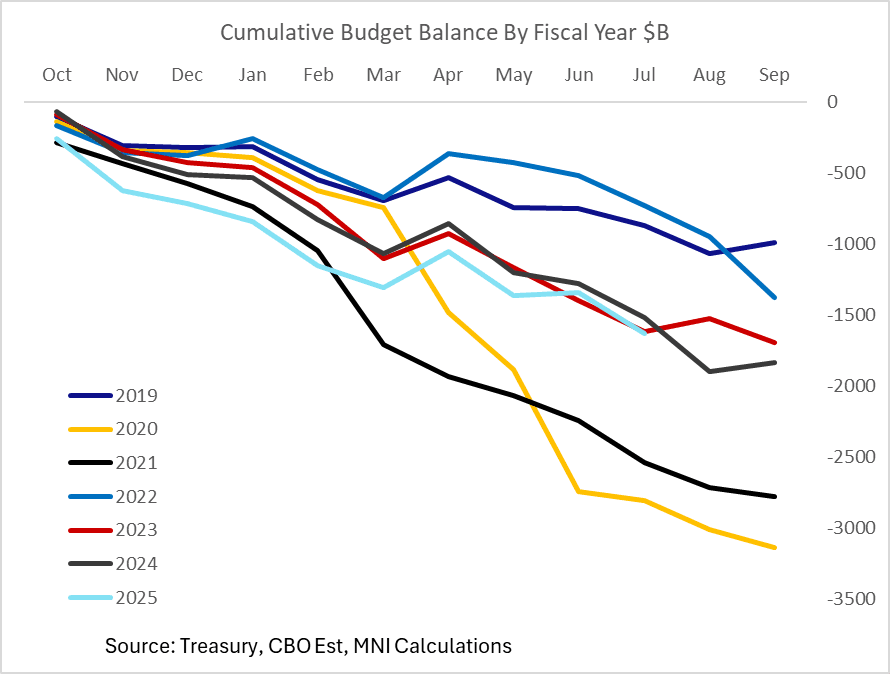

US FISCAL: CBO Estimates $289B Deficit In July

Treasury's monthly fiscal statement for July is expected to be published Tuesday (1400ET), but the Congressional Budget Office has already produced its usually pretty accurate estimate.

- The CBO estimates a $289B deficit was recorded in July, on $628B in spending (up 9% Y/Y) and $339B in receipts (up 3%). Notably in the latter column, customs duties rose $18B (252% Y/Y).

- If correct, the FY2025 cumulative deficit is running at about $1.626T with two months to go in the year, vs $1.517T in the same period of FY2024.

- That's a $109B increase, but accounting for timing changes (which increased FY2023 outlays, benefiting the FY2024 picture), the deficit this year would have been just $37B larger at this point.

- That's a 2% increase but compares to an anticipated 3+% Y/Y nominal increase in GDP in Q3 (Fiscal Q4).

- At the start of 2025, CBO estimated a $1.9T deficit this fiscal year; that's still in play with August typically seeing a large deficit ahead of a better outturn in September in part on tax receipts, though looks a little on the high side at this point. CBO will publish the Monthly Budget Review with its final projection next month.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

US TSYS/OVERNIGHT REPO: Secured Rates Steady, Could Pick Up Later This Week

Secured rates were steady Friday, with SOFR remaining at 4.35%.

- Rates are expected to print the same or perhaps slightly lower Monday. However pressure could pick up later in the week on Treasury auction settlements. These include $55B in net cash raised by bills on Tuesday and a further $42B on Thursday, followed by $35B in coupon settlements Friday.

- The effective Fed funds rate remains steady at 4.33%.

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.35%, no change, $2817B

* Broad General Collateral Rate (BGCR): 4.33%, no change, $1169B

* Tri-Party General Collateral Rate (TGCR): 4.33%, no change, $1139B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.33%, no change, volume: $115B

* Daily Overnight Bank Funding Rate: 4.33%, no change, volume: $262B

US TSYS/OVERNIGHT REPO: ON RRP Takeup Remains Below $100B

Takeup of the Fed's overnight reverse repo facility ticked up by around $2B to $82.2B Monday, the second consecutive daily increase but the 5th day in 6 below the $100B mark.

- ON RRP takeup has averaged $91B in the first 7 sessions of August, compared with $225B over the first 7 sessions in July.

- Helping reduce appetite for ON RRP is the rise in bill issuance since the debt limit was lifted in early July - a dynamic that is expected to keep a lid on the facility for the foreseeable future (outside of spikes typically seen at month-/quarter-end).

BONDS: EGBs-GILTS CASH CLOSE: Gilts Outperform Ahead Of Labour Data

Gilts outperformed Bunds Monday ahead of key UK labour market data.

- The session low for yields was set in early trade, with some focus on the potential disinflationary implications of a resolution to the Russia-Ukraine conflict ahead of a Trump-Putin meeting scheduled for end-week.

- That said, the pullback in yields looked corrective in nature, coming after Friday's rise and amid limited macro / data / headline news flow. Yields crept up for most of the remainder of the session.

- That left the German curve relatively unchanged on the day, though Gilts benefited in part from a KPMG-REC report on jobs suggesting weak labour market dynamics / restrained wage growth.

- Periphery/semi-core EGB spreads closed mixed, with Spain outperforming and Greece underperforming. MNI published an exclusive on Greek issuance ("Greek 2026 New Issuance Lower End Of EUR8-10 Bln-Source").

- Tuesday's scheduled highlight is the UK labour market report. MNI's preview is here (PDF): primary focus is on private regular average earnings which are expected at 4.8%Y/Y in the 3-months to June.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.8bps at 1.964%, 5-Yr is up 0.6bps at 2.289%, 10-Yr is up 0.6bps at 2.696%, and 30-Yr is up 2bps at 3.226%.

- UK: The 2-Yr yield is down 3.6bps at 3.863%, 5-Yr is down 3.6bps at 4.001%, 10-Yr is down 3.6bps at 4.565%, and 30-Yr is down 3.6bps at 5.392%.

- Spanish bond spread down 0.3bps at 56.4bps / Greek up 1.1bps at 65.3bps

FOREX: USD on More Solid Footing into July CPI Print

- The dollar finished the Monday session stronger, rising against most others in G10 in a relief rally and clear out of positioning ahead of the Tuesday US CPI print. The USD's move higher seemingly came in isolation, with the front-end of the US curve and core equity markets proving resilient to the edge higher in the greenback. Resultantly, strength in the USD Monday was likely an extended phase of position-squaring after the soft NFP print earlier this month (USD Index still 1.4% below pre-NFP levels), and ahead of tomorrow's CPI print - the next data input for the September FOMC decision.

- In addition, outside of the EUR, USD gains seemingly have less conviction: GBP/USD has reversed lower after a failed test on the 50-dma of 1.3502, and further weakness here will open 1.3398 support (23.6% retracement for the upleg off the 1.3142 low) ahead of the more notable level at 1.3310. Below here, the bounce will look to have concluded, and a further fade becomes more likely. Tomorrow's wages and unemployment numbers could prove key this week.

- The sole currency to outperform the greenback was NOK. Strength here persisted through Monday, helping EURNOK push through initial support at 11.9326 (23.6% retracement of the upleg off the late July low). The slightly stronger-than-expected July inflation report set the tone for NOK Monday: although CPI-ATE inflation was actually in line with Norges Bank's June MPR projections at 3.1% Y/Y, measures of inflation momentum suggest underlying price pressures remain a little persistent. This should push back against the need for firmer guidance towards a September cut at Thursday's Norges Bank decision.

- Near-term focus shifts to the RBA rate decision at which the bank are seen trimming rates by a further 25bps to 3.60%. The German ZEW survey then crosses ahead of the July US CPI print.

DATA/EVENTS CALENDAR

| Date | ET | Impact | Period | Release | Prior | Consensus | |

| 12/08/2025 | 0600 | ** | Jul | NFIB Small Business Index | 98.6 | 98.9 | |

| 12/08/2025 | 0830 | *** | Jul | - Core [Ex Food and Energy] y/y (1dp) | -- | -- | % |

| 12/08/2025 | 0830 | *** | Jul | - Core [Ex Food and Energy] m/m (1 dp) | -- | -- | % |

| 12/08/2025 | 0855 | ** | 09-Aug | Redbook Retail Sales y/y (month) | 5.4 | -- | % |

| 12/08/2025 | 0855 | ** | 09-Aug | Redbook Retail Sales y/y (week) | 6.5 | -- | % |

| 12/08/2025 | 1400 | ** | Jul | Treasury Budget Balance | 27.0 | -150 | USD (b) |