MNI US CPI Preview: High Early Bar To September Fed Hold

Aug-11 15:09By: Chris Harrison and 1 more...

InflationFederal ReserveUS

Hidden PDF

Executive Summary

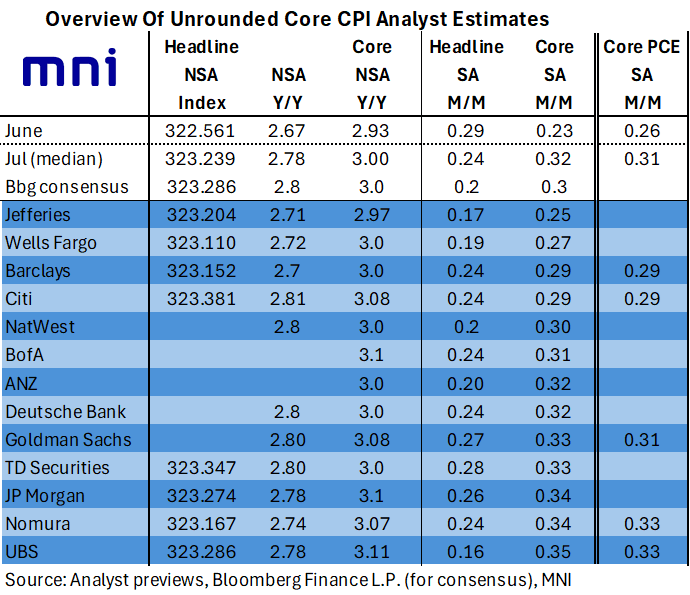

- The CPI report for July is released on Tuesday Aug 12, at 0830ET. Consensus sees core CPI inflation at a seasonally adjusted 0.3% M/M in June and unrounded analyst estimates broadly echo this with a median 0.32% M/M.

- It would mark a further acceleration from 0.23% M/M in June and 0.13% M/M in May for its fastest pace since January, with the latest firming seen coming from core goods inflation doubling to 0.4% M/M.

- Headline CPI meanwhile is seen at 0.2% M/M (MNI median 0.24% M/M) with a gasoline drag.

- This should start to be a better month to assess tariff passthrough, with rough consensus of three months from tariff implementation to consumer price adjustments, but the fall months could see the largest impact.

- The July PPI report isn’t until Thursday, with early tracking of core PCE estimates at 0.31% M/M implying little net impact from PPI details. That would be an acceleration from 0.26% M/M in June.

- Fed Funds futures currently price 22bp of cuts for the next FOMC meeting in September after the huge downward revisions in the July nonfarm payrolls report less than two weeks ago.

- We see more sensitivity to a downside surprise in July CPI, particularly in core goods components seen sensitive to tariffs. That would set up a replay of the 2024 episode in which after holding in July, the FOMC cut 50bp in Sept (a decision which was, going into the meeting, a “close call” vs 25bp) after a July jobs report saw the u/e rate rise by 0.2pp to 4.25%, even as core PCE appeared to stabilize at 2.6/2.7% Y/Y.

- There is however the August round for NFP and CPI reports before then, with both coming after Fed Chair Powell’s Jackson Hole appearance. We also await Trump’s new BLS commissioner pick.

Trending Top

Jun-25 06:23