MNI ASIA OPEN: Early Risk Appetite Wanes, Focus on Wed FOMC

EXECUTIVE SUMMARY

- MNI SECURITY: US Moves Assets To MidEast, Iran Asks Trump For Ceasefire - Reuters

- MNI US: Senate Finance Committee Expected To Released Final Portion Of OBBB Today

- MNI IRAN: Risk Sentiment Improves as Iran Reportedly Approach Ceasefire Mediators

- MNI US DATA: Poor Activity, But Much-Improved Outlook In Empire Manufacturing Survey

US

MNI SECURITY: US Moves Assets To MidEast, Iran Asks Trump For Ceasefire - Reuters

Reuters reports that Iran has requested that Qatar, Saudi Arabia, and Oman ask US President Donald Trump to apply pressure on Israel to agree to an 'immediate ceasefire', per two Iranian and three regional sources. According to Reuters, "in return, Iran to offer flexibility in nuclear negotiations with US."

NEWS

MNI US: Senate Finance Committee Expected To Released Final Portion Of OBBB Today

The Senate Finance Committee is expected to release some, or all, of the legislative text of its portion of the ‘One Big Beautiful’ reconciliation bill today, covering the thorniest issues in the package. Committee Chair Mike Crapo (R-ID) will update Senate Republicans on the text at around 17:30 ET 22:30 BST. Observers are watching how the Senate handles SALT, phasing out the IRA tax credits, and work requirements and provider taxes for Medicaid. Any major changes to the House-passed package could set up another confrontation in the House and risk ping-ponging the legislation between the two chambers.

MNI IRAN: Risk Sentiment Improves as Iran Reportedly Approach Ceasefire Mediators

Iran have reportedly approached Qatar, Saudi Arabia and Oman to ask President Trump to press Israel to agree an imminent ceasefire, according to Reuters sources. In return, Iran are reportedly offering flexibility in nuclear negotiations with the US. Markets holding, and building, on their risk-on moves as these Iran headlines cross - equities remain favoured with the e-mini S&P still higher by ~75 points to show above the Thursday high.

MNI IRAN: Tasnim-Tehran Uses Hypersonic Missiles In Latest Strikes On Israel

Semi-official Iranian outlet Tasnim reports that the Islamic Revolutionary Guards Corps (IRGC) Aerospace Force is using hypersonic missiles in its attacks on Israel. Tasnim claims that "In this morning's operation, several images were recorded of hypersonic missiles hitting targets in Tel Aviv and Haifa, showing that these missiles easily passed through Israel's anti-ballistic defense systems and hit the target. [These missiles] are equipped with a solid-fuel spherical engine warhead with a movable nozzle and the ability to maneuver and change course."

US TSYS

MNI US TSYS: Early Risk-On Evaporates, Stocks Just Don't Know it Yet

- Treasuries retreated from midday highs as early risk-on tone over easing geopol-tension hopes in turn retreated as Iran and Israel continued to trade missiles. Weaker Treasury futures are back near opening levels with the Sep'25 10Y contract at 110-15.5 (-4) vs. 110-26 overnight high - compares to early Friday high of 111-05 (111-13 overnight high).

- Earlier focus on key resistance and recent high at 111-14+, a Fibonacci retracement and the Jun 5 high. Clearance of this hurdle would be bullish and highlight a stronger reversal. Technical support below at 109-28 (Low Jun 6 / 11).

- Stocks firmer but off early highs, SPX eminis tapped highest levels since last Wednesday: 6055.25 (+76.0) with Financials and IT sectors leading gainers in early trade.

- Despite the breadth of moves, markets rather quiet ahead of Wednesday's FOMC annc. Projected rate cut pricing has cooled vs. morning levels (*) as follows: Jun'25 at 0.0bp, Jul'25 at -3.1bp (-4.1bp), Sep'25 at -17.4bp (-18.4bp), Oct'25 at -30.6bp (-34.9bp), Dec'25 at -46.4bp (-46.9bp).

- Busy Wednesday: addition to FOMC, markets see weekly/continuing claims, house starts/build permits & 3 bill auctions ahead Thursday's Juneteenth holiday. Cash Treasury and stock exchanges are closed Thursday, along with open outcry pits in Chicago but equity and debt futures will be open for an abbreviated trading session.

OVERNIGHT DATA

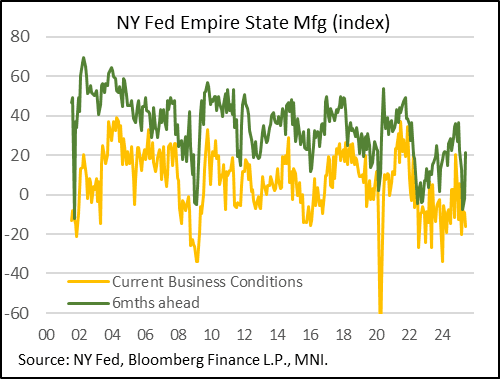

MNI US DATA: Poor Activity, But Much-Improved Outlook In Empire Manufacturing Survey

The NY Fed's Empire Manufacturing survey unexpectedly saw the headline General Business Conditions index worsen in June, to a 3-month low -16.0 (-6.0 expected) vs -9.2 in April.

- This was a surprise as the Empire survey is conducted early in the month, and May's deterioration (-8.1 to -9.2) had been seen as not reflective of the May 12 US-China tentative tariff deal which saw sentiment improve in other surveys conducted later in the month.

- New orders pulled back sharply, from a positive 7.0 reading in May, to -14.2, a 3-month low, with shipments also declining. We also note higher delivery times and lower inventory levels, with the Supply Availability index ticking up to -8.3 from -11.4 but still suggestive of worsening supply availability.

- That said, this was a very mixed report as there was some notable improvement in other subindices. Most notably, the 6-month-ahead reading jumped to 21.2 (-2.0 prior), a 4-month high. And employment rose to the first positive reading (4.7, from -5.1 prior) since January, and the best level outright since December 2022, suggesting some hiring in the month.

- Even within the 6-month outlook, results were extremely mixed: "New orders and shipments are expected to increase, and firms expect supply availability to be only slightly worse in the months ahead. Capital spending plans remained soft." Indeed capex plans were the weakest since 2020.

- There is probably more noise in this report than signal, given how mixed these readings are (and how volatile the survey is even in normal times).

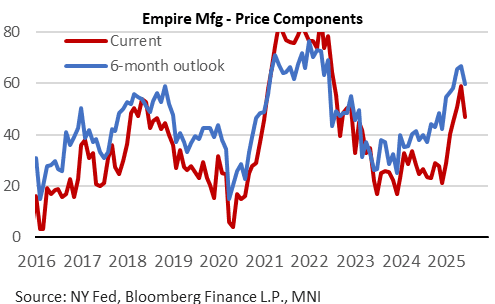

- One largely clear finding though was that inflation components in the survey eased from multi-year highs in May: prices paid fell to 46.8 from 59.0, with 6-month expectations falling to 59.6 from 66.7, suggesting that the worst of the perceived price pressures may be over.

MNI CANADA DATA: May Housing Starts -0.2%, Toronto YOY Starts -22%

- Seasonally adjusted monthly starts -0.2% in May to 279,510 units, Canada Mortgage and Housing Corp. says Monday.

- Six-month trend was also little changed +0.8% in May to 243,407 units.

- Toronto May YOY housing starts -22% and Vancouver -10%, both due to lower multi-unit starts. Montreal +11% YOY boosted by multi-units.

- “Growth in actual starts activity in May was once again driven by increases of single-detached homes and purpose-built rentals in Québec and the Prairie provinces. By contrast, weak condominium market conditions in Toronto and Vancouver have contributed to significant declines in overall housing starts in these regions,’’ said Tania Bourassa-Ochoa, CMHC’s Deputy Chief Economist.

- Government has pledged to double the pace of homebuilding to address supply squeeze; most economists note a lack of workers to achieve that goal.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 258.65 points (0.61%) at 42458.18

S&P E-Mini Future up 51 points (0.85%) at 6082

Nasdaq up 276 points (1.4%) at 19683.61

US 10-Yr yield is up 5.2 bps at 4.4502%

US Sep 10-Yr futures are down 3.5/32 at 110-16

EURUSD up 0.0021 (0.18%) at 1.1569

USDJPY up 0.55 (0.38%) at 144.62

WTI Crude Oil (front-month) down $1.78 (-2.44%) at $71.20

Gold is down $46.9 (-1.37%) at $3385.71

European bourses closing levels:

EuroStoxx 50 up 49.1 points (0.93%) at 5339.57

FTSE 100 up 24.59 points (0.28%) at 8875.22

German DAX up 182.89 points (0.78%) at 23699.12

French CAC 40 up 57.56 points (0.75%) at 7742.24

US TREASURY FUTURES CLOSE

3M10Y +5.981, 9.18 (L: 0.291 / H: 9.716)

2Y10Y +3.468, 48.376 (L: 44.674 / H: 48.761)

2Y30Y +4.356, 98.772 (L: 93.74 / H: 99.285)

5Y30Y +3.058, 92.118 (L: 88.333 / H: 92.489)

Current futures levels:

Sep 2-Yr futures down 0.75/32 at 103-18.75 (L: 103-17 / H: 103-21)

Sep 5-Yr futures down 1.5/32 at 107-29.75 (L: 107-25.75 / H: 108-03.25)

Sep 10-Yr futures down 4/32 at 110-15.5 (L: 110-10.5 / H: 110-26)

Sep 30-Yr futures down 18/32 at 112-22 (L: 112-18 / H: 113-20)

Sep Ultra futures down 24/32 at 115-21 (L: 115-15 / H: 116-26)

MNI US 10YR FUTURE TECHS: (U5) Resistance Remains Intact For Now

- RES 4: 111-30 76.4% retracement of the May 1 - 22 downleg

- RES 3: 111-21 1.0% 10-dma envelope

- RES 2: 111-14+ High Jun 5 & 61.8% of the May 1 - 22 downleg

- RES 1: 111-13 High Jun 13

- PRICE: 110-18+ @ 11:01 BST Jun 16

- SUP 1: 109-28 Low Jun 6 / 11

- SUP 2: 109-12+ Low May 22 and the bear trigger

- SUP 3: 109-09+ Low Apr 11 and key support

- SUP 4: 108-25+ 0.764 proj of the Apr 7 - 11 - May 1 price swing

Treasury futures remain below key resistance and its recent high at 111-14+, a Fibonacci retracement and the Jun 5 high. Clearance of this hurdle would be bullish and highlight a stronger reversal. This would open 111-30, a Fibonacci retracement. On the downside, support to watch lies at 109-28, the Jun 6 / 11 low. Clearance of this level would be bearish and open the bear trigger at 109-12+, May 22 low.

SOFR FUTURES CLOSE

Jun 25 -0.020 at 95.668

Sep 25 -0.040 at 95.865

Dec 25 -0.035 at 96.115

Mar 26 -0.030 at 96.325

Red Pack (Jun 26-Mar 27) -0.01 to +0.005

Green Pack (Jun 27-Mar 28) -0.01 to steady

Blue Pack (Jun 28-Mar 29) -0.015 to -0.01

Gold Pack (Jun 29-Mar 30) -0.03 to -0.02

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.28% (+0.00), volume: $2.644T

- Broad General Collateral Rate (BGCR): 4.27% (+0.00), volume: $1.089T

- Tri-Party General Collateral Rate (TCR): 4.27% (+0.00), volume: $1.062T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $110B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $296B

FED Reverse Repo Operation

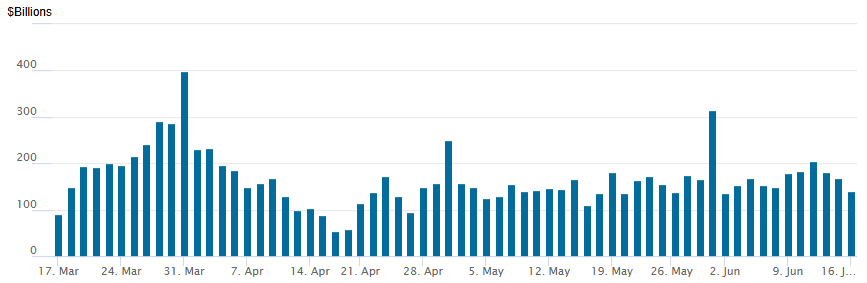

RRP usage retreats to $140.759B this afternoon from $168.645B Friday, total number of counterparties at 26. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

MNI PIPELINE: Corporate Bond Update: $3.5B EOG 4Pt Launched

- Date $MM Issuer (Priced *, Launch #)

- 06/16 $4B Hungary $1.5B +5Y +145, $1B +10Y +175, $1.5B +30Y +195

- 06/16 $3.5B #EOG $500M 3Y +50, $1.25B 7Y +80, $1.25B +10Y +90, $500M 30Y +100

- 06/16 $2.25B #Enbridge $400M 3Y +67, $600M 5Y +87, $900M 10Y +112, $350M tap 04/05/54 +122

- 06/16 $700M Unisys 5.5NC2.5 10.5%a

- 06/16 $500M #Atmos Energy 10Y +80

- 06/16 $500M #Kimco Realty +10Y +92

- 06/16 $Benchmark EIB 7Y SOFR+53a

- 06/16 $Benchmark America Movil +7Y +110a

- 06/16 $Benchmark IBK 3Y SOFR+58a, 5Y +45a

- 06/16 $Benchmark Islamic Development Bank Sukuk 5Y SOFR+58a

MNI BONDS: EGBs-GILTS CASH CLOSE: Bull Steeper On Another Geopolitically Heavy Day

European yields fell across curves Monday in a bull steepening move.

- Yields rose early in the session, with safe havens shrugging off weekend escalation of Middle East tensions, taking more of a cue from associated higher oil prices.

- But the day's highs were hit relatively early and yields descended from there. Iran-Israel headlines dominated in a data-thin session, with bond gains notably on a WSJ report that Iran was seeking to end hostilities.

- Italian final HICP was revised lower. The Eurozone hourly labour cost index moderated in Q1, but less than initially estimated.

- Both the German and UK curves bull steepened, with Gilts outperforming.

- Periphery/semi-core EGB spreads tightened, with BTPs and OATs outperforming.

- Tuesday's calendar includes the ZEW Survey for June and Spanish labour market data, with speaking appearances by ECB's Villeroy and Centeno.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.5bps at 1.841%, 5-Yr is down 1.6bps at 2.12%, 10-Yr is down 0.8bps at 2.527%, and 30-Yr is down 0.1bps at 2.986%.

- UK: The 2-Yr yield is down 3.4bps at 3.906%, 5-Yr is down 2.4bps at 4.04%, 10-Yr is down 1.7bps at 4.533%, and 30-Yr is down 0.6bps at 5.254%.

- Italian BTP spread down 2.1bps at 92.8bps / French OAT down 2bps at 70.2bps

MNI FOREX: AUD and NZD Outperforming Amid Firmer Risk Sentiment

- The US dollar is underperforming on Monday, as more benign price action across the energy and equity markets is conveying a more stable risk backdrop. WTI and Brent crude futures are roughly 7% off the earlier highs, while the e-mini S&P 500 tracks around 1% in the green to start the week.

- As such, the likes of AUD and NZD have been key beneficiaries within G10, largely mirroring the price action for the major equity benchmarks. AUDUSD has been testing an important resistance point at 0.6550, the Nov 25 high, and a close at current levels would be he highest in 7 months, potentially signalling scope for a stronger recovery to the US election related highs at 0.6688.

- The EUR has also recovered, briefly rising to a session high of 1.1615. The rally has moderated as we approach the APAC crossover as spot deals close to 1.1580 at typing. Sights remain on 1.1696 next, a Fibonacci projection, as the technical uptrend remains firmly in place. Relative underperformance for the safe havens has elevated EURJPY to the highest level since July last year. A positive close today for the cross would be 8 consecutive winning sessions, with sights now on a couple of daily highs at the 168.00 mark.

- USDJPY stands a touch higher Monday, but still managed to establish a 110 pip range on the session, keeping attention on the pair high as we approach tomorrow’s BOJ decision and press conference. 145.46 and 142.12 appear the key short-term parameters for the pair.

- Elsewhere on Tuesday, German ZEW figures are scheduled, before US retail sales and import price data are due.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 17/06/2025 | 0600/0800 | ** | Unemployment | |

| 17/06/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 17/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 17/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 17/06/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/06/2025 | 1230/0830 | *** | Retail Sales | |

| 17/06/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 17/06/2025 | 1230/0830 | *** | Retail Sales | |

| 17/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 17/06/2025 | 1315/0915 | *** | Industrial Production | |

| 17/06/2025 | 1400/1000 | * | Business Inventories | |

| 17/06/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 17/06/2025 | 1400/1000 | * | Business Inventories | |

| 17/06/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 5 Year Note | |

| 18/06/2025 | 2350/0850 | * | Machinery orders |