MNI ASIA OPEN: Dovish Fed Speak, Heavy Data, Stocks Near Highs

EXECUTIVE SUMMARY

- MNI US TSYS: FDIC Votes To Relax SLR, In Line With June Proposals

- MNI US: White House Puts Healthcare Plan On Ice After Resistance From House GOP

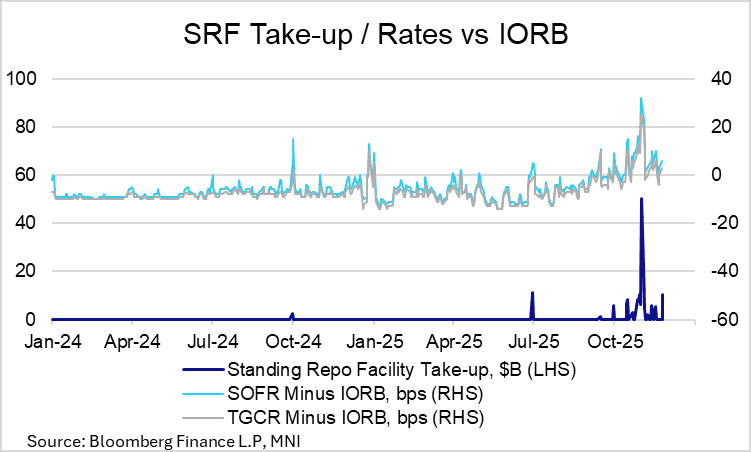

- MNI US TSYS/OVERNIGHT REPO: AM SRF Take-up At $10.6bln; Several Potential Drivers

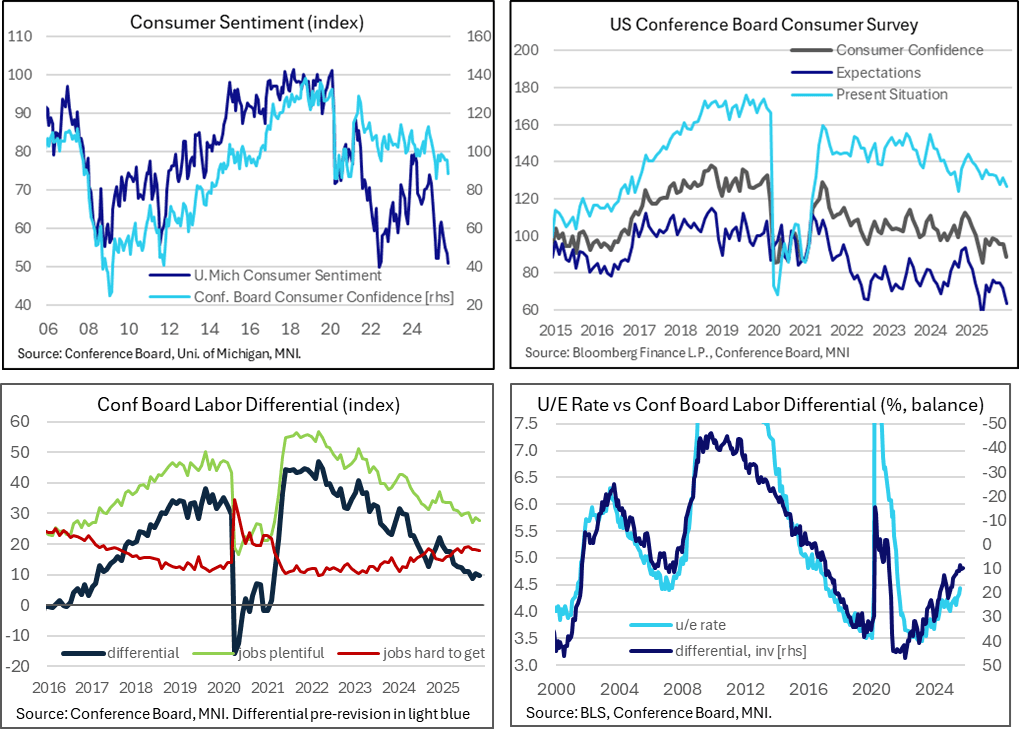

- MNI US DATA: Consumer Confidence Slips Although Labor Concerns At Least Stabilize

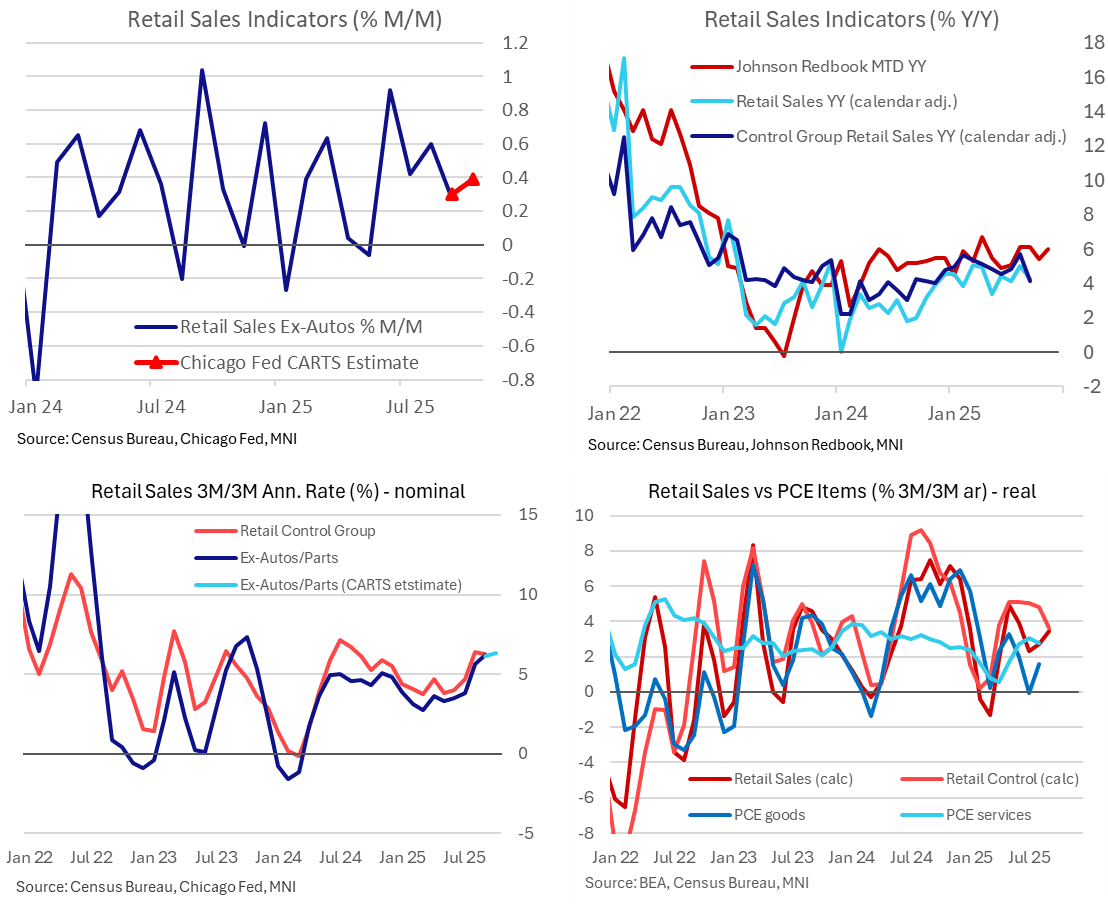

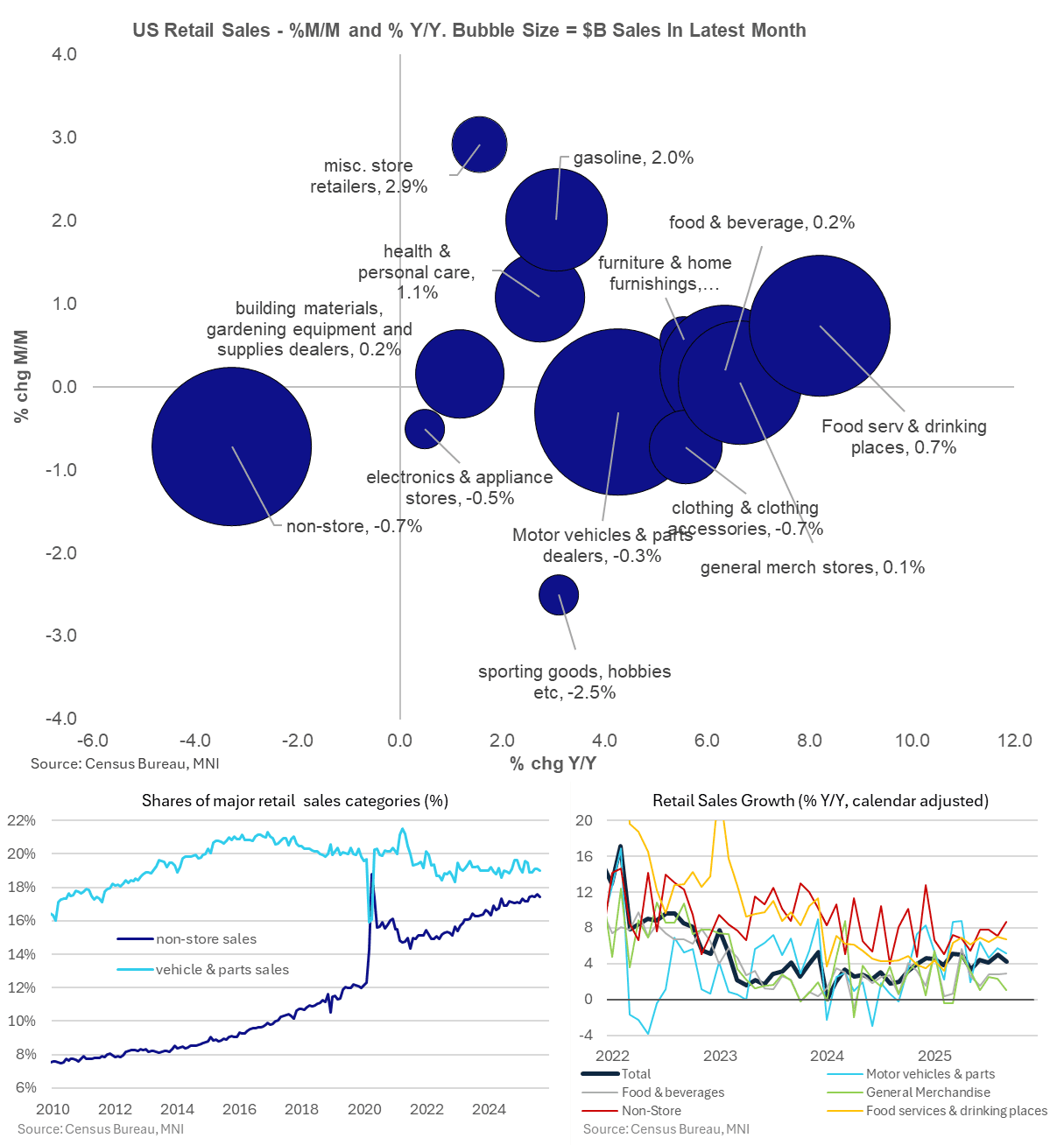

- MNI US DATA: Retail Sales Disappoint In Eventual September Release

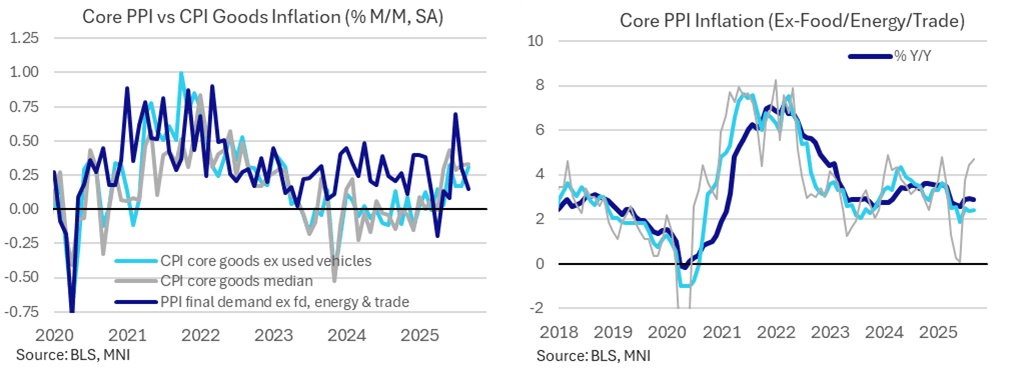

- MNI US DATA: Core PPI Inflation Underwhelms In September

NEWS

MNI US: White House Puts Healthcare Plan On Ice After Resistance From House GOP

The White House has paused plans to roll out a healthcare proposal to address the imminent Obamacare subsidy cliff, which will see around 22 million Americans' insurance premiums rise in the new year without an Affordable Care Act extension. Reports over the weekend suggested that the White House was set to unveil a two-year extension of Obamacare subsidies with income caps to get conservatives onside. The plan was aimed at preventing a midterm rout for the GOP, with core parts of the Republican base expected to be hit with premium hikes.

MNI US TSYS: FDIC Votes To Relax SLR, In Line With June Proposals

"US regulators moved to relax capital requirements that lenders have said limit their ability to act as intermediaries in the Treasuries market during times of stress" Bbg. No material reaction in US swap spreads at first glance. Spreads are up to 1bp wider on the session (10-year at -42bps, just shy of last week's multi-month high). It was known that the FDIC were meeting today, so there may have been some speculation/pre-positioning in swap spreads on anticipation of an SLR announcement.

Bloomberg: KEVIN HASSETT SEEN AS FRONTRUNNER IN TRUMP FED CHAIR SEARCH

Bloomberg: China Asks Airlines to Extend Japan Flight Cuts Until March 2026 - The Chinese government has instructed the country’s airlines to reduce the number of flights to Japan through March 2026, according to people familiar with the matter, signaling Beijing is braced for a protracted spat between the two nations.

US TSYS

MNI US TSYS: Tsys Gaining on Dovish Fed Speak, Tepid UK/Russia Peace Deal Support

- Treasuries see-sawed higher Tuesday, near early session highs after a moderately volatile first half. TYZ5 +7.5 at 113-19.5 after the bell vs. 113-24 high; 10Y yld slipped below 4% to 3.9865% low briefly - lowest since late October.

- Treasuries extended highs, stocks rallied but quickly reversed after ABC headlines that Ukraine has agreed with the United States on the terms of a potential peace deal with Russia. The peace plan, which will be presented to Russia when Ukraine signs off, has been heavily modified from the 28-point peace plan that was leaked over the weekend. The alterations to the initial proposal, which leaned heavily towards Russian priorities, has led to scepticism that Russia will agree to the basic terms.

- Treasuries extending highs yet again as Fed Gov Miran sticks to dovish script on Fox Business - that current policy is holding economy back, calling for large rate cuts. Headlines reiterating that Kevin Hassett is deemed a frontrunner in search for the next Fed Chair role have prompted a dovish shift in the front-end of the curve, further weighing on the greenback.

- Heavy data day: The delayed retail sales report for September was softer than expected, with control group sales slipping -0.1% M/M for their first (nominal) decline since April;

- Core PPI inflation was softer than expected back in September even if it was partly offset by a revision even further back in July. It broadly chimes with underlying core goods CPI inflation, with a peak for post-tariff M/M inflation pressures having come earlier in the summer (June for our median estimate on the CPI side, July for core PPI). PPI final demand inflation was in line with expectations in September at 0.31% M/M after -0.14% M/M, although core inflation surprised softer.

- The Conference Board consumer survey for November saw a sharper decline in consumer confidence whilst expectations remained below a recessionary threshold for a tenth consecutive month. Consumer confidence was notably weaker than expected in November at 88.7 (cons 93.3) after a slightly upward revised 95.5 (initial 94.6) in October, hitting its lowest since April and before that early 2021.

OVERNIGHT DATA

MNI US TSYS/OVERNIGHT REPO: AM SRF Take-up At $10.6bln; Several Potential Drivers

Take-up at this morning's NY Fed Standing Repo Facility operation jumped to $10.6bln, the highest level since the period of funding market pressure around October month-end (where total SRF usage was $50bln across the two daily operations). This suggests we may see further upside in secured rates today, after a 3bp increase in SOFR and TGCR yesterday. The SOFR/IORB spread is now at 6bps, a five session high. There are a few factors that may be feeding into the latest developments in funding markets and SRF take-up:

- Early month-end dynamics amid the Thanksgiving holiday later this week.

- Net $14bln of US bill settlements on Nov 25, with an additional $52bln of net coupon/bill settlements due on Friday and $84bln of net coupon settlements due on Dec 1.

- Removal of GSE cash that had been parked in the market since mid-month.

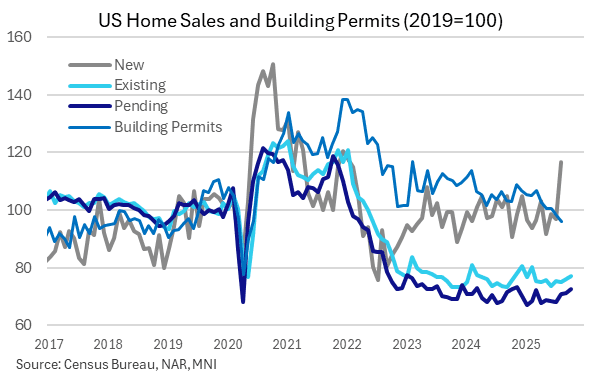

MNI US DATA: Pending Home Sales Offer Some Cautious Optimism

Pending home sales increased nearly 2% M/M in October to offer some near-term optimism for existing home sales but from a clearly low base. Pending home sales were stronger than expected in October, rising 1.9% M/M (cons 0.2) after a slightly upward revised 0.1% M/M in September (initial 0.0).

MNI US DATA: Consumer Confidence Slips Although Labor Concerns At Least Stabilize

The Conference Board consumer survey for November saw a sharper decline in consumer confidence whilst expectations remained below a recessionary threshold for a tenth consecutive month. Consumer confidence was notably weaker than expected in November at 88.7 (cons 93.3) after a slightly upward revised 95.5 (initial 94.6) in October, hitting its lowest since April and before that early 2021.

MNI US DATA: Core PPI Inflation Underwhelms In September

Core PPI inflation was softer than expected back in September even if it was partly offset by a revision even further back in July. It broadly chimes with underlying core goods CPI inflation, with a peak for post-tariff M/M inflation pressures having come earlier in the summer (June for our median estimate on the CPI side, July for core PPI). PPI final demand inflation was in line with expectations in September at 0.31% M/M after -0.14% M/M, although core inflation surprised softer.

MNI US DATA: Retail Sales Disappoint In Eventual September Release

The delayed retail sales report for September was softer than expected, with control group sales slipping -0.1% M/M for their first (nominal) decline since April. We estimate a reasonably large decline in retail sale volumes in September, and whilst prior strength sees still solid growth in Q3 as a whole, it sees weak momentum heading into Q4. Retail sales disappointed in September as they only increased 0.16% M/M (cons 0.4) after an essentially unrevised 0.60% M/M in August that formed a string of strong prints since June.

MNI US DATA: Retail Sales Details See Rare Pullback In Non-Store Category

The details of the September retail sales report point to sizeable drags from large categories along with at best mixed implications for those typically more indicative of discretionary spending. Reverting to the details within the September retail sales report, a drag from the large non-store category helped explain surprise weakness in the headline categories (overall retail sales 0.16% M/M vs cons 0.4 after 0.60%, control group -0.09% cons 0.3 after 0.57%).

- Specifically, non-store sales, which were worth 17.4% of retail sales in September, fell -0.7% after 1.6% M/M to drag -0.13pps from overall retail sales on the month.

- The second largest drag then came from motor vehicle sales, equally large at 17.5% of sales, which fell -0.3% after 0.6% M/M to drag -0.04pps. These are excluded from the control group although auto parts sales, which are included within the control group and are worth 1.5% of overall sales, also fell -1.2% after 1.1% M/M.

- Helping explain the relative gap between overall sales and the control group, gasoline sales (excluded from the control group) increased 2.0% M/M after 0.4% for a fourth consecutive monthly increase. It added 0.14pps to overall retail sales growth.

- Elsewhere, there were mixed signs of discretionary spending: food services & drinking places saw another solid increase of 0.7% after 1.0% M/M but sporting goods & hobbies slid -2.5% after 1.0% M/M. Clothing-related sales also fell back with -0.7% M/M although that’s after a particularly strong run after six months averaging 1.0% M/M since March.

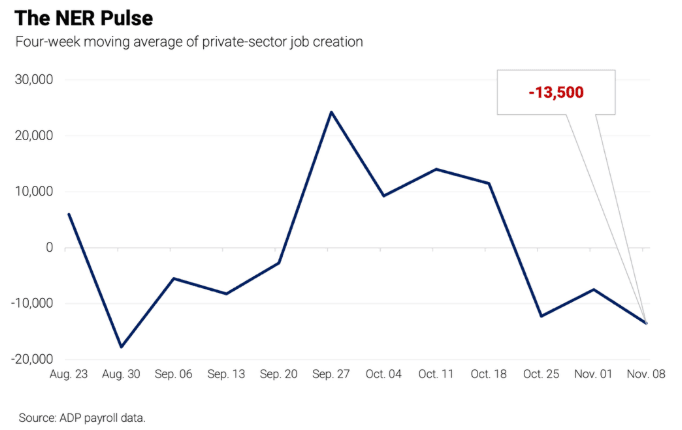

MNI US DATA: Another Weak Weekly ADP Print But Still Waiting Exact Revisions

The weekly ADP reported an average weekly decline of -13.5k in the four weeks to November 8. That’s down from the -2.5k initially reported last week – we can see from the image ADP provides that this was revised to a larger decline but ADP hasn’t updated the excel file that is released along with it.

MNI CANADA DATA: More Signs Of Business Confidence Amid Tariffs, Food Inflation

- StatsCan's quarterly business conditions survey Tues shows 21% of respondents are very optimistic compared with 5% who are very pessimistic. About two-thirds of responses taken in Oct and Nov show strong or some optimism.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 632.61 points (1.36%) at 47086.81

S&P E-Mini Future up 53.75 points (0.8%) at 6775.5

Nasdaq up 116.7 points (0.5%) at 22988.27

US 10-Yr yield is down 1.7 bps at 4.0075%

US Dec 10-Yr futures are up 7.5/32 at 113-19.5

EURUSD up 0.0044 (0.38%) at 1.1566

USDJPY down 0.79 (-0.5%) at 156.08

WTI Crude Oil (front-month) down $0.84 (-1.43%) at $58.00

Gold is down $5.41 (-0.13%) at $4132.47

European bourses closing levels:

EuroStoxx 50 up 45.24 points (0.82%) at 5573.91

FTSE 100 up 74.62 points (0.78%) at 9609.53

German DAX up 225.45 points (0.97%) at 23464.63

French CAC 40 up 66.13 points (0.83%) at 8025.8

US TREASURY FUTURES CLOSE

Curve update:

3M10Y +2.165, 22.291 (L: 17.803 / H: 23.147)

2Y10Y +1.909, 54.276 (L: 51.223 / H: 54.535)

2Y30Y +3.44, 120.297 (L: 114.705 / H: 120.502)

5Y30Y +2.07, 109.721 (L: 105.172 / H: 109.917)

Current futures levels:

Dec 2-Yr futures up 0.875/32 at 104-9.625 (L: 104-07.75 / H: 104-10.25)

Dec 5-Yr futures up 4.75/32 at 109-26 (L: 109-19.5 / H: 109-28.5)

Dec 10-Yr futures up 7.5/32 at 113-19.5 (L: 113-09.5 / H: 113-24)

Dec 30-Yr futures up 8/32 at 117-31 (L: 117-18 / H: 118-14)

Dec Ultra futures up 5/32 at 121-11 (L: 121-00 / H: 122-02)

MNI US 10YR FUTURE TECHS: (H6) Bull Cycle Extends

- RES 4: 114-00 Round number resistance

- RES 3: 113-29+ High Oct 17 and a key resistance

- RES 2: 113-23 High Oct 23

- RES 1: 113-18+ Intraday high

- PRICE: 113-15 @ 16:59 GMT Nov 25

- SUP 1: 113-08/112-27+ Intraday low / 20-day EMA

- SUP 2: 112-24 50-day EMA

- SUP 3: 112-10+ Low Nov 20

- SUP 4: 112-07 Low Nov 5 and a key support

A bullish theme in Treasuries remains intact and today’s gains reinforce current conditions. Last week’s breach of the 112-31 level, an area of congestion since Nov 5, marks an important short-term bullish development. An extension would pave the way for a climb towards 113-29+, the Oct 17 high and a key resistance. On the downside, initial support is at 112-27+, the 20-day EMA. Support at the 50-day EMA, lies at 112-24.

SOFR FUTURES CLOSE

Current White pack (Dec 25-Sep 26):

Dec 25 +0.008 at 96.263

Mar 26 steady00 at 96.460

Jun 26 +0.015 at 96.725

Sep 26 +0.025 at 96.910

Red Pack (Dec 26-Sep 27) +0.030 to +0.035

Green Pack (Dec 27-Sep 28) +0.035 to +0.035

Blue Pack (Dec 28-Sep 29) +0.030 to +0.030

Gold Pack (Dec 29-Sep 30) +0.030 to +0.030

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.96% (+0.03), volume: $3.232T

- Broad General Collateral Rate (BGCR): 3.93% (+0.03), volume: $1.288T

- Tri-Party General Collateral Rate (TCR): 3.93% (+0.03), volume: $1.260T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.88% (+0.00), volume: $73B

- Daily Overnight Bank Funding Rate: 3.88% (+0.00), volume: $159B

FED Reverse Repo Operation

RRP usage at $2.314B with 8 counterparties this afternoon from $1.077B Monday. Compares to last Tuesday's $0.905B - lowest level since mid-March 2021; this years highest excess liquidity measure: $460.731B on June 30.

MNI FOREX: Hassett Headlines Bolster Softer USD Backdrop, UK Budget Awaited

- Tuesday’s FX session was characterised by waning optimism for the dollar, prompting the USD index to recede further from last week’s cycle highs, now tracking comfortably back below the 100.00 mark. Headlines reiterating that Kevin Hassett is deemed a frontrunner in search for the next Fed Chair role have prompted a dovish shift in the front-end of the curve, further weighing on the greenback.

- Additionally, tepid optimism relating to the Russia/Ukraine peace deal have helped boost major equity indices, while also providing notable support to the Euro. As such, EURUSD has risen to 1.1580, narrowing the gap to a key short-term resistance at 1.1656, the Nov 13 high and reversal trigger.

- It is GBP that has stood out as the best performing currency in G10. We noted earlier that potential positioning dynamics could help exacerbate a potential GBP squeeze, and this may have been playing out ahead of tomorrow’s UK budget.

- GBPUSD is currently up 0.72% on the session, rallying as high as 1.3201. Today’s move has notably breached a short-term resistance for cable, rising above the 20-day EMA, at 1.3161, signalling scope for a stronger corrective cycle. More meaningful resistance is at the 50-day, intersecting at 1.3265.

- Lower core yields have allowed USDJPY to further erode a portion of the significant recent upswing, with the pair dipping back below 156.00 today. While the USDJPY bullish trend appears well established, the pair had entered overbought territory, and this short-term pullback is considered technically corrective at this juncture. Support to watch is the prior breakout level around 155.00, which closely coincides with 154.76, the 20-day EMA.

- The RBNZ decision highlights the APAC calendar on Wednesday before all focus turns to the UK budget. It is worth noting that there did appear to be some dollar demand heading into 4pm London, and as a reminder, Barclays’ rebalancing model points to strong Dollar buying against all the majors at month-end in November.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 26/11/2025 | 0700/1500 | ** | MNI China Money Market Index (MMI) | |

| 26/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 26/11/2025 | 1200/0700 | ** | Brazil Preliminary CPI | |

| 26/11/2025 | 1230/1230 | Chancellor Reeves to deliver UK Budget | ||

| 26/11/2025 | 1330/0830 | ** | Advance Trade, Advance Business Inventories | |

| 26/11/2025 | 1330/0830 | *** | Jobless Claims | |

| 26/11/2025 | 1330/0830 | ** | Durable Goods New Orders | |

| 26/11/2025 | 1330/0830 | ** | Durable Goods New Orders | |

| 26/11/2025 | 1442/0942 | *** | MNI Chicago PMI | |

| 26/11/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 26/11/2025 | 1530/1530 | DMO to publish consultation agenda | ||

| 26/11/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 26/11/2025 | 1605/1705 | ECB Lane Fireside Chat on Macro Outlook | ||

| 26/11/2025 | 1630/1130 | ** | US Treasury Auction Result for 7 Year Note | |

| 26/11/2025 | 1700/1200 | ** | Natural Gas Stocks | |

| 26/11/2025 | 1700/1800 | ECB Lagarde Acceptance Speech | ||

| 26/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 26/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 26/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 26/11/2025 | 1900/1400 | Fed Beige Book | ||

| 27/11/2025 | 0030/1130 | * | Private New Capex and Expected Expenditure |