MNI ASIA OPEN: Chip Stocks Surge, Trump Tours Saudi Arabia

EXECUTIVE SUMMARY

- MNI MIDEAST: White House Claims 'Largest Defence Sales Deal In History'

- MNI UKRAINE: RTRS-US' Witkoff & Kellogg Head To Turkey w/Putin Attendance Unclear

- MNI US: WaPo-White House Looks To Strike Chips & Minerals Deal On Middle East Trip

- MNI US DATA: Little To Suggest Major PCE-CPI Gap From Report Components

- MNI US DATA: Mixed Evidence Of Tariff Impact On April Goods CPI

NEWS

MNI MIDEAST: White House Claims 'Largest Defence Sales Deal In History'

The White House has released a factsheet following the slew of deals signed between President Donald Trump and Saudi Crown Prince Mohammed bin Salman, claiming the agreements add up to USD600B of Saudi investment in the US, including a USD142B deal for military equipment in what the Trump administration calls the "largest defense sales agreement in history". Reuters reports the two sides have also discussed the potential Saudi purchase of US F-35 jets.

MNI UKRAINE: RTRS-US' Witkoff & Kellogg Head To Turkey w/Putin Attendance Unclear

Reuters reports that, according to its sources, US Middle East envoy Steve Witkoff and Ukraine/Russia envoy Keith Kellogg will travel to Istanbul, Turkey on 15 May as part of the potential talks between Russia and Ukraine on reaching a peace settlement. Earlier, Ukrainian President Volodymyr Zelenskyy confirmed that he will be in Istanbul to meet with Turkish President Recep Tayyip Erdogan. It remains unclear whether Russian President Vladimir Putin, or indeed any Russian government figures, will be in attendance.

MNI US: JCT Tax Bill Score Provides GOP Breathing Room For Reconcilliation Markup

The nonpartisan Joint Committee on Taxation has issued a positive assessment of the revenue implications of the House Republican tax bill. The House Ways and Means Committee is scheduled to mark up the bill today as part of President Donald Trump's 'One Big Beautiful' Bill to legislate his domestic agenda. The JCT scores that the Ways and Means tax bill adds $3.7 trillion to the deficit over 10 years. That is well within the $4 trillion allocated to Ways and Means by the budget resolution adopted by Congress last month.

MNI US: WaPo-White House Looks To Strike Chips & Minerals Deal On Middle East Trip

The Washington Post reports that the Trump White House is set to authorise the sale of advanced AI chips to Middle Eastern firms connected to the Saudi and Emirati gov'ts as part of an effort to bolster AI development in the region as a bulwark against China. The report claims that the deals could be finalised during President Donald Trump's ongoing visit to the region. Speculation of the deal first appeared in NYT. The article also claims that the US has "also approved a memorandum of understanding worth $9 billion between a U.S. company and Saudi partners to mine and process critical minerals used in advanced manufacturing, energy and defense,".

MNI RUSSIA: Kremlin Refuses To Confirm If Putin Will Attend Turkey Talks w/Ukraine

Kremlin spox Dmitry Peskov says to reporters that a Russian delegation is preparing for talks in Turkey later this week. Peskov does not expand on the proposal/demand from Ukrainian President Volodymyr Zelenskyy that President Vladimir Putin attend the talks in person. Says "We will announce who will represent Russia at talks in Turkey when Putin sees fit to announce it." Earlier this morning, reports claimed that, according to a senior Ukrainian official, Zelenskyy would not meet with other members of the Russian delegation, only Putin. On 12 May, Zelenskyy criticised Putin's "strange silence" over whether he would attend.

US TSYS

MNI US TSYS: Rates Quickly Reject Early Highs After Slight CPI Miss

- Treasuries look to finish near late Tuesday session lows - holding a relatively narrow range through the second half. Tsys had extend highs after slighly lower than expected CPI inflation measures.

- There is little in this report alone to suggest a meaningful gap between CPI and PCE - in other words, the slight downside miss in core CPI doesn't carry a major re-interpretation for PCE via the components. Note April core PCE consensus was 0.24% M/M coming into today, and while this may dip slightly we doubt forecasts will be radically changed (core CPI came in at 0.22% M/M).

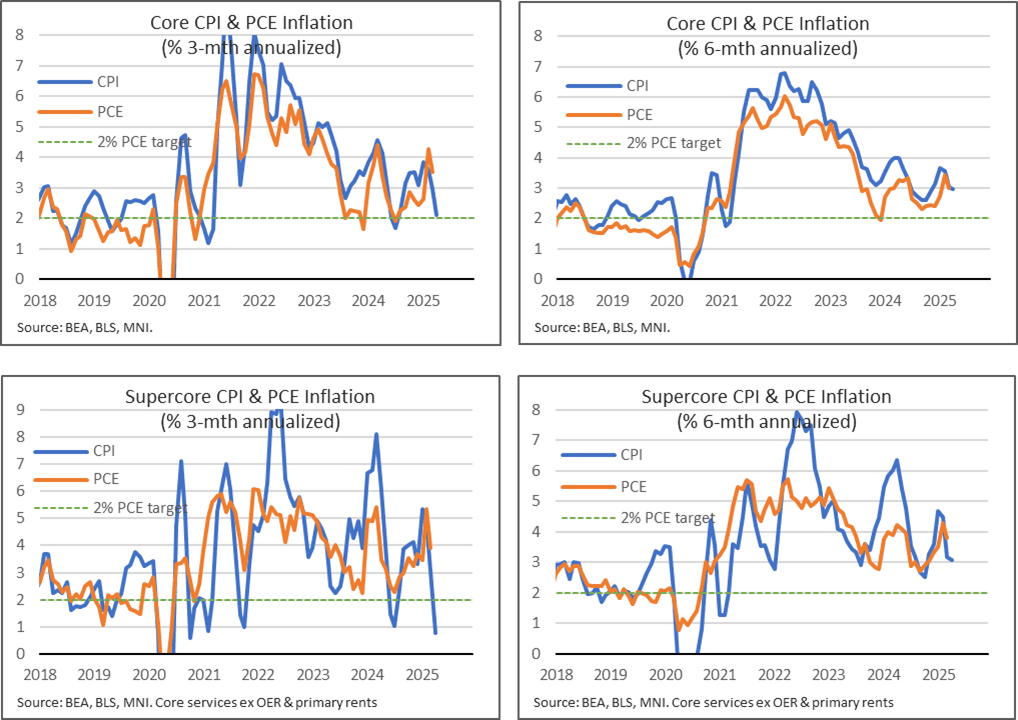

- As for broader trends, the core CPI six-month rate held at 3.0% annualized for a second month in April having moderated from 3.7% in January, although it’s still a fourth consecutive month above the Y/Y.

- Treasury Jun'25 10Y futures currently trades at 109-31.5 (-5.5) -- breaching support at 110-01+, a Fibonacci retracement point as well as yesterday’s low. Clearance here strengthens a bearish theme and exposes a key support at 109-08, the Apr 24 low.

- Curves bear steepened, 2s10s +1.515 at 46.949, 5s30s +1.966 at 81.118.

- The greenback has weakened on Tuesday, eroding a solid portion of the prior session advance. Amid the continued bid for major equity indices, the US dollar traded in a more typical manner with risk, weakening against most G10 peers and in particular against the likes of AUD and NZD.

OVERNIGHT DATA

MNI US DATA: CPI Core & Supercore Latest Trends

As for broader trends, the core CPI six-month rate held at 3.0% annualized for a second month in April having moderated from 3.7% in January, although it’s still a fourth consecutive month above the Y/Y.

Core CPI (SA)

- % M/M: 0.237 in Apr'25 after 0.057 in Mar'25

- % 3mth ar: 2.1 in Apr'25 after 3 in Mar'25

- % 6mth ar: 3 in Apr'25 after 3 in Mar'25

- % Y/Y (NSA): 2.78% in Apr’25 after 2.79% in Mar’25

CPI Core Services Non-Housing (SA)

- % M/M: 0.209 in Apr'25 after -0.241 in Mar'25

- % 3mth ar: 0.8 in Apr'25 after 3.1 in Mar'25

- % 6mth ar: 3.1 in Apr'25 after 3.2 in Mar'25

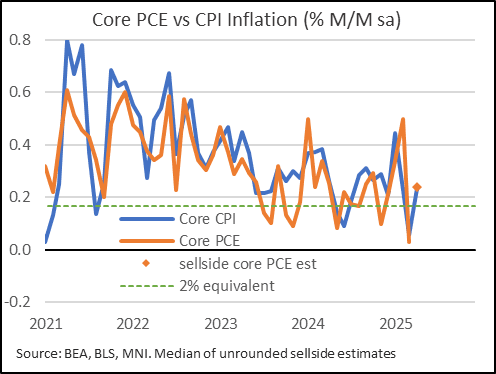

MNI US DATA: Little To Suggest Major PCE-CPI Gap From Report Components

There is little in this report alone to suggest a meaningful gap between CPI and PCE - in other words, the slight downside miss in core CPI doesn't carry a major re-interpretation for PCE via the components. Note April core PCE consensus was 0.24% M/M coming into today, and while this may dip slightly we doubt forecasts will be radically changed (core CPI came in at 0.22% M/M).

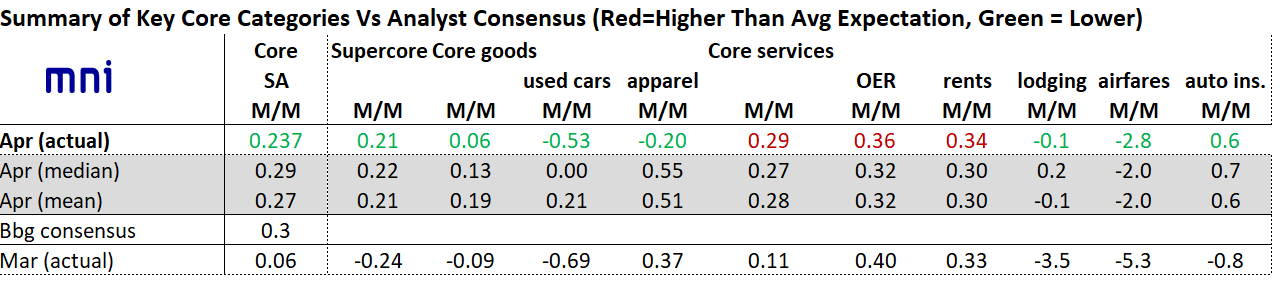

- For the usual suspects: as noted, airfares (taken from PPI for PCE) were a little softer than expected, but basically in line - and in the same camp, auto insurance rebounded more or less as expected (again, this is taken from PPI for PCE).

- CPI medical care services were if anything stronger than expected, rising 0.5% M/M for a second consecutive month, equaling March's rise which was the biggest since September 2024 - with higher professional and dental care inflation offset by slower hospital care inflation.

- On a side note on services: communications fell by 0.4% M/M, the softest in 5 months after being a stronger-than-expected contributor in the earlier months of the year.

MNI US DATA: Mixed Evidence Of Tariff Impact On April Goods CPI

While April was widely considered to be too early to see significant impacts from tariff-induced pickups in inflation, the evidence looking through the report is mixed. The biggest hint of a tariff-induced pickup is that core goods ex-used cars CPI posted the strongest unrounded rate of inflation (0.15% M/M) since March 2023. Category-by-category though, it was less clear.

MNI US DATA: Slightly Lower-Than-Expected Core Goods Prices, Mostly In-Line Services

The slightly soft core CPI reading vs consensus (0.24% M/M vs 0.29% MNI Median, 0.06% prior) came amid an undershoot on core goods prices (and a slightly above but basically in-line core services reading. See table for key components.

- In core goods (0.06% M/M vs 0.13% median, -0.09% prior), used cars (-0.5% vs 0.0% median, -0.7% prior) and apparel (-0.2% vs +0..6% median, 0.4% prior) both were softer than expected. New vehicle inflation was basically the same as March (0.0% vs 0.1% prior).

- In core services (0.29% M/M vs 0.27% median, 0.11% prior), OER and Rents were very slightly higher than expected as noted earlier. Offsetting that were lodging (-0.1% vs 0.2% median, though rebounding from -3.5% prior) and airfares (-2.8% vs -2.0% median, also up from -5.3% prior).

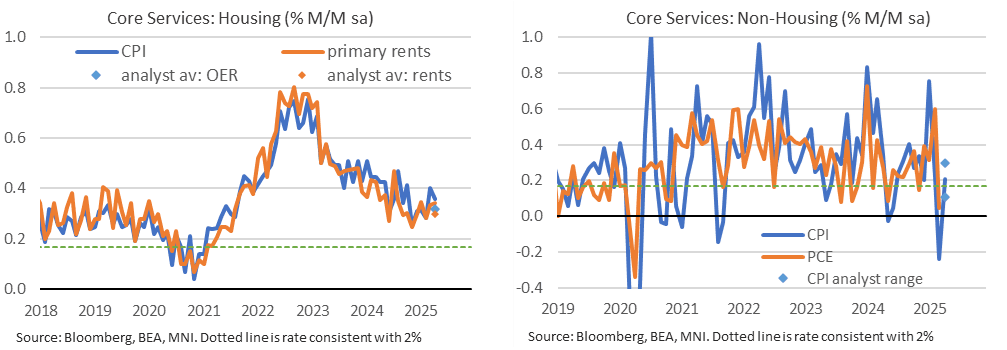

MNI US DATA: Rental Inflation Surprises A Little Stronger, Supercore In Line

Rental inflation was stronger than expected again this month, although OER only just rounded to 0.4% M/M.

- OER: 0.36% M/M vs analyst average 0.32% (range 0.28-0.40) in April vs 0.40% in March and 0.28% in Feb.

- Primary rents: 0.34% M/M vs analyst average 0.30% (range 0.28-0.32) in April vs 0.33% in March and 0.28% in Feb.

The supercore print at 0.21% M/M was exactly in line with a consensus we had seen across four estimates.

- Core services excl OER & primary rents ('supercore'): 0.209% M/M after -0.241%. Latest 3mth av of 0.061%

- Core services excl all shelter: 0.151% M/M after -0.069%. Latest 3mth av of 0.114%

- Limited analyst estimates for ex OER & rents had averaged 0.21% M/M, ranging from 0.11 to 0.30

MNI US DATA: Redbook Continues To Suggest Retail Momentum Going Into May

Johnson Redbook retail sales were up 5.8% Y/Y in the month through to May 10 (compared with retailers' target of a 5.4% gain), with sales in the most recent week likewise up 5.8% Y/Y. Once again we have a solid piece of "hard" retail sales data in recent months in contrast with sharp drops in survey-based consumer confidence indicators.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 159.48 points (-0.38%) at 42248.54

S&P E-Mini Future up 55.75 points (0.95%) at 5920.75

Nasdaq up 342.4 points (1.8%) at 19049.75

US 10-Yr yield is up 2 bps at 4.4907%

US Jun 10-Yr futures are down 5.5/32 at 109-31.5

EURUSD up 0.0103 (0.93%) at 1.119

USDJPY down 1.02 (-0.69%) at 147.45

WTI Crude Oil (front-month) up $1.78 (2.87%) at $63.73

Gold is up $13.65 (0.42%) at $3249.68

European bourses closing levels:

EuroStoxx 50 up 23.85 points (0.44%) at 5416.21

FTSE 100 down 2.06 points (-0.02%) at 8602.92

German DAX up 72.02 points (0.31%) at 23638.56

French CAC 40 up 23.73 points (0.3%) at 7873.83

US TREASURY FUTURES CLOSE

3M10Y +2.757, 10.126 (L: 0.934 / H: 12.091)

2Y10Y +1.539, 46.973 (L: 43.974 / H: 48.918)

2Y30Y +2, 90.846 (L: 88.021 / H: 94.21)

5Y30Y +1.91, 81.062 (L: 78.174 / H: 84.26)

Current futures levels:

Jun 2-Yr futures down 1.125/32 at 103-9.125 (L: 103-08.75 / H: 103-13.125)

Jun 5-Yr futures down 2.25/32 at 107-16 (L: 107-14.75 / H: 107-26)

Jun 10-Yr futures down 5.5/32 at 109-31.5 (L: 109-30 / H: 110-15)

Jun 30-Yr futures down 23/32 at 112-25 (L: 112-19 / H: 113-23)

Jun Ultra futures down 26/32 at 116-8 (L: 115-27 / H: 117-12)

MNI US 10YR FUTURE TECHS: (M5) Bearish Tone

- RES 4: 112-20+ High May 1 and a bull trigger

- RES 3: 112-01+ High May 2

- RES 2: 111-22 High May 7 and a key near-term resistance

- RES 1: 111-04+ 20-day EMA

- PRICE: 109-31+ @ 1535 ET May 13

- SUP 1: 109-30 Low May 13

- SUP 2: 109-08 Low Apr 24 and key support

- SUP 3: 108-26+ 76.4% retracement of the Jan 13 - Apr 7 bull cycle

- SUP 4: 108-21 Low Feb 19

Treasury futures maintain a softer tone following recent weakness. Support at 110-01+, a Fibonacci retracement point, has broken - as well as yesterday’s low. Clearance here strengthens a bearish theme and exposes a key support at 109-08, the Apr 24 low. Key near-term resistance has been defined at 111-22, the May 7 high. A break of this level is required to signal a potential reversal.

SOFR FUTURES CLOSE

Jun 25 -0.005 at 95.70

Sep 25 -0.035 at 95.930

Dec 25 -0.035 at 96.180

Mar 26 -0.030 at 96.365

Red Pack (Jun 26-Mar 27) -0.02 to -0.015

Green Pack (Jun 27-Mar 28) -0.02 to -0.01

Blue Pack (Jun 28-Mar 29) -0.025 to -0.015

Gold Pack (Jun 29-Mar 30) -0.03 to -0.025

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.28% (+0.00), volume: $2.535T

- Broad General Collateral Rate (BGCR): 4.27% (+0.00), volume: $1.077T

- Tri-Party General Collateral Rate (TCR): 4.27% (+0.00), volume: $1.037T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $105B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $296B

FED Reverse Repo Operation

RRP usage recedes to $144.214B this afternoon from $147.505B yesterday, total number of counterparties at 32. Usage had fallen to $54.772B last Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

PIPELINE: Corporate Bond Update: $10.35B to Price Tuesday

- Date $MM Issuer (Priced *, Launch #)

- 05/13 $2.65B TransDigm 8NC3

- 05/13 $1.75B #National Securities Clearing $750M 2Y +38, $400M 2Y SOFR+57, $600M 5Y +60

- 05/13 $1.5B #Tennessee Valley Authority 10Y +45

- 05/13 $1.2B #Capital Power $700M 3Y +125, $500M 10Y +170

- 05/13 $1B #L'Oreal 10Y +62.5

- 05/13 $1B #Belrose Funding 30Y +185

- 05/13 $600M #Interstate Power & Light 10Y +115

- 05/13 $650M #Baltimore Gas & Electric 10Y +98

- Expected to issue Wednesday:

- 05/13 $1B AIIB WNG 10Y SOFR+65a

MNI BONDS: EGBs-GILTS CASH CLOSE: Selling Resumes, Shrugging Off Benign Data

Tuesday saw further weakness across European bonds, despite seemingly FI-benign data releases.

- Following Monday's sell-off following a de-escalation of the US-China trade war, European core FI remained on the back foot as a risk-on tone persisted in equities.

- Brisk supply on both the corporate and sovereign (Netherlands, Germany, Italy, EU) fronts in Europe weighed on the space.

- The Gilt front-end/belly outperformed, with the latest labour market report bringing a downside surprise on the wage front (and little in market-moving commentary by BOE's Pill). And in the most closely-watched release of the day globally, US CPI came in softer than expected.

- In the end, the data didn't hold sway, with cross-asset moves in a lower USD and higher equities after the US CPI release instead dragging Bunds and Gilts to/near session lows by the cash close.

- The German and UK curves both bear steepened, with the UK belly/short end outperforming overall as noted.

- Spreads tightened modestly on the EGB periphery/semi-core, with BTPs leading gains.

- Wednesday's calendar includes some final April HICP readings, while we also get multiple ECB speakers including Villeroy and Holzmann.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 2.3bps at 1.936%, 5-Yr is up 2.3bps at 2.245%, 10-Yr is up 3.2bps at 2.68%, and 30-Yr is up 4.5bps at 3.126%.

- UK: The 2-Yr yield is down 2bps at 3.98%, 5-Yr is up 0.5bps at 4.131%, 10-Yr is up 2.7bps at 4.67%, and 30-Yr is up 3.6bps at 5.427%.

- Italian BTP spread down 1.1bps at 101.8bps / Spanish down 0.7bps at 61.9bps

FOREX: AUDUSD Surges Amid Equity Rally/Soft US CPI

- Following the softer-than-expected US CPI, the greenback has weakened on Tuesday, eroding a solid portion of the prior session advance. Amid the continued bid for major equity indices, the US dollar traded in a more typical manner with risk, weakening against most G10 peers and in particular against the likes of AUD and NZD.

- NZDUSD (+1.4%) has risen back above a short-term pivot at 0.5900, and trades within close proximity of Monday’s highs at 0.5941. The pair has made multiple attempts above the 0.60 handle in recent weeks, but has failed to breach the US election related highs at 0.6038. This will remain a key barrier to a more protracted recovery.

- For AUDUSD (+1.60%), Monday’s move down is considered corrective and spot currently stands at the best levels of the week. This keeps trend conditions firmly in bullish territory, and further strength would open 0.6528, the Nov 29 ‘24 high.

- The likes of EURUSD and GBPUSD are also notably higher, though gains are just under the 1% mark. From a trend perspective, recent EURUSD weakness appears corrective as key signals remain bullish. The 50-day EMA has been pierced but today’s reversal higher keeps this support level intact. A resumption of strength would place the topside focus on 1.1381, the May 2 - 6 high. Clearance of this level would signal the end of the correction. Various sell-side analysts had flagged that levels between 1.10/11 should offer an attractive entry point for dip buyers.

- The risk-on theme sees the Japanese yen underperform, with USDJPY only half a percent lower today, holding on to the bulk of the surge through the 50-day EMA on Monday, as easing trade tensions between the US & China spur renewed optimism for the pair.

- Australia Wage Price Index data and China new loans figures will be highlights on the Wednesday calendar, before the focus turns to Thursday’s release of US retail sales and PPI.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 14/05/2025 | 0600/0800 | *** | Final Inflation Report | |

| 14/05/2025 | 0600/0800 | *** | HICP (f) | |

| 14/05/2025 | 0700/0900 | *** | HICP (f) | |

| 14/05/2025 | 0715/0815 | BOE Breeden At ISDA Conference | ||

| 14/05/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 14/05/2025 | 0915/0515 | Fed Governor Christopher Waller | ||

| 14/05/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 14/05/2025 | - | *** | Money Supply | |

| 14/05/2025 | - | *** | New Loans | |

| 14/05/2025 | - | *** | Social Financing | |

| 14/05/2025 | 1230/0830 | * | Building Permits | |

| 14/05/2025 | 1240/1440 | ECB's Cipollone On Liquidity Issues Panel | ||

| 14/05/2025 | 1310/0910 | Fed Vice Chair Philip Jefferson | ||

| 14/05/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 14/05/2025 | 2140/1740 | San Francisco Fed's Mary Daly | ||

| 15/05/2025 | 0130/1130 | *** | Labor Force Survey |