MNI ASIA OPEN: Budget Bill Passes Senate, Back to House

EXECUTIVE SUMMARY

- MNI US: Senate Passes 'Big Beautiful Bill' After Marathon Vote-A-Rama

- MNI FED: Powell: "Really Can't Say" If July Too Soon To Seriously Consider Cut

- MNI US DATA: ISM Manufacturing Sees Solid Production But Soft New Orders And Jobs

- MNI US DATA: Another JOLTS Report Ruling Out Sharper Labor Deterioration

US

MNI FED: Powell: "Really Can't Say" If July Too Soon To Seriously Consider Cut

Fed Chair Powell speaking on an ECB forum panel asked if July is too soon to seriously consider a rate cut and he certainly doesn't categorially rule it out, even if it's couched in typical central bank-speak: "Yeah, I really can't say - it's going to depend on the data. And we are going meeting by meeting. I mentioned, you know, how I'm thinking about that, but I wouldn't take any meeting off the table or put it directly on the table, it's going to depend on how the data evolve."

NEWS

MNI US: Senate Passes 'Big Beautiful Bill' After Marathon Vote-A-Rama

The United States Senate has passed the GOP's 'One Big Beautiful Bill' in a 50-50 vote, with Vice President JD Vance casting the tie-breaking vote. The vote came after over 26 hours of debate and amendment in a so-called vote-a-rama. The bill now passes to the House of Representatives, where the House Rules Committee will meet to craft rules on the package. The Rules committee hearing is likely to take place in around an hour, providing an immediate temperature check on the conservative reaction to the Senate-passed package.

MNI TARIFFS: FT-EU Toughens Stance On Donald Trump’s Tariffs As Deadline Looms

The FT reports "European capitals have hardened their position in trade talks with Donald Trump, insisting the US drops its tariffs on the EU immediately as part of any framework deal before the looming deadline on July 9." European Trade Commissioner Maros Sefcovic travels to Washington, D.C., today ahead of the latest round of talks with Commerce Secretary Howard Lutnick and USTR Jamieson Greer on 3 July. Comes as Brussels treads the fine line of avoiding a major escalation in trade tensions with the US that could see 50% tariffs imposed on EU exports to the US, while also standing up for its own industries.

US TSYS

MNI US TSYS: Late Japan, India Trade Deal Comments Rattle Markets Briefly

- Treasuries look to finish weaker but off lows - drawing some buy interest after Pre Trump commented on trade deals with Japan and India.

- Bloomberg headlines: "DOUBT WE'LL HAVE DEAL WITH JAPAN" , "ON JULY 9 DEADLINE: NOT THINKING ABOUT EXTENDING" while "SUGGESTS JAPAN COULD PAY 30% OR 35% TARIFF".

- Nikkei spun it a little differently: "US TO HANDLE JAPAN LATER IN TARIFF TALKS, PRIORITIZING INDIA".

- Tsy Sep'25 10Y futures trade -7.5 at 111-28.5 after the bell vs. 111-22.5 low, 10Y yield +.0176 at 4.2456%. Curves remain flatter: 2s10s -3.167 at 47.299, 5s30s -3.900 at 93.654.

- The bull cycle in Treasury futures remains intact, however prices reversed hard off highs into the Tuesday close. As such, the contract has failed on the approach to the next important resistance at 112-15, the 61.8% retracement of the Apr 7 - 11 steep sell-off. Note that the uptrend is overbought, a pullback would unwind this position. First key support to watch is 111-05+, the 20-day EMA.

- Stocks dipped (SPX emini -3.75 at 6250.0) as did US$ slightly after climbing off morning lows into midday high (BBDXY: 1185.43 low / 1191.23 high).

- Looking ahead: Wednesday data focus on MBA Mortgage Applications at 0700ET, Challenger Job Cuts at 0730 followed by ADP Employment Change at 0815ET. No Fed scheduled Fed speakers. Thursday is a heavy data day with NFP added due to Independence Day holiday closure on Friday.

OVERNIGHT DATA

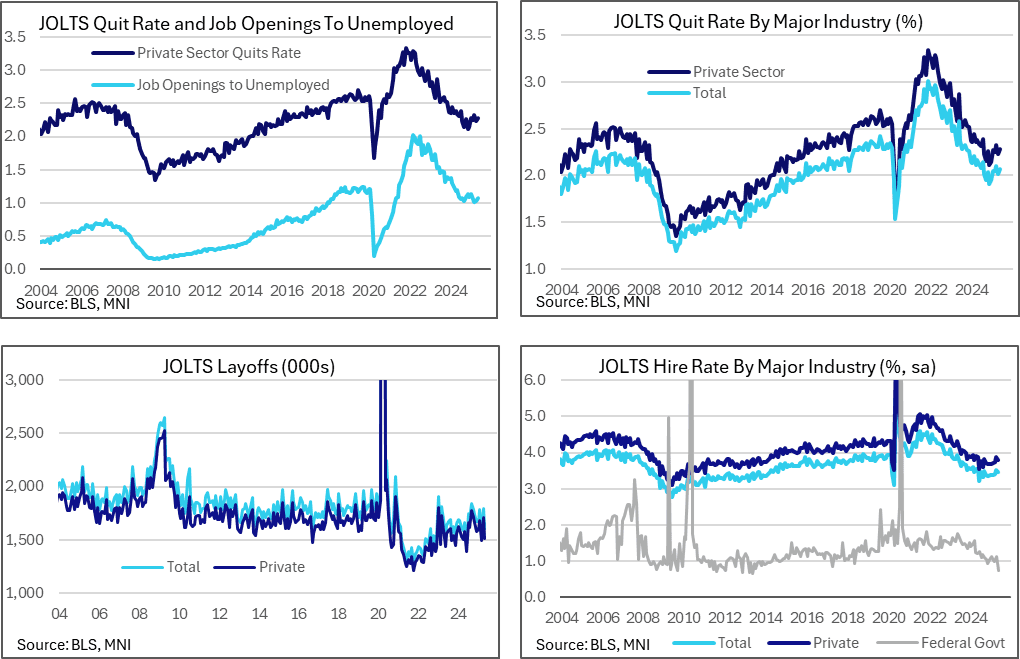

MNI US DATA: Another JOLTS Report Ruling Out Sharper Labor Deterioration

The JOLTS report for May saw stronger than expected job openings whilst quit and hiring rates plus the level of layoffs all pointed to broad stabilization in the labor market rather than showing signs of further moderation. Previous DOGE efforts on reducing the size of federal government appear to have a larger impact than in recent months although it doesn’t move the broader needle.

- Job openings increased to 7,769k (sa, cons 7,300k) in May from a near unrevised 7,395k (initial 7,391k) in April.

- The ratio of openings to unemployed increased to 1.07 from an unrevised 1.03, slightly up from the recent low of 1.02 in March. It represented continued recent stability rather than any further moderation, having averaged 1.07 since Jun 2024. For context, it averaged 1.2 in 2019 and 1.0 in 2017-18.

- The quit rate meanwhile nudged up to 2.06% from a slightly upward revised 2.02% (initial 2.00) having for now appeared to have stabilized around the 1.9-2% level since Aug 2024.

- These are still relatively subdued levels though, having averaged 2.3% in 2019 and 2.2% in 2017-18.

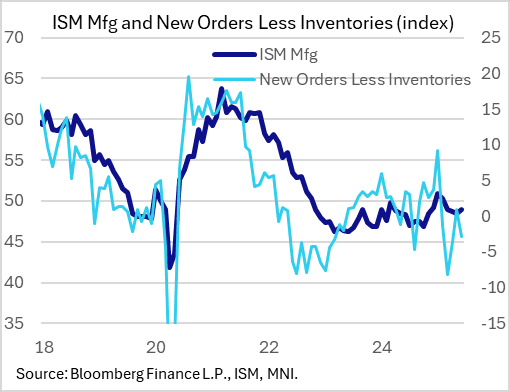

MNI US DATA: ISM Manufacturing Sees Solid Production But Soft New Orders And Jobs

The ISM Manufacturing index improved a little more than expected in June, rising to 49.0 (48.5 prior, 48.8 expected) for the first increase in 4 months albeit still in contractionary territory amid heightened trade policy uncertainty. A rebuilding of inventories as well as stronger production led the increase.

- This was a very mixed report in terms of activity. While production picked up sharply, by 4.9 points to a 4-month high 50.3, new orders fell 1.2 points to 46.4 for a 3-month low, and employment fell 1.8 points to 45.0, a 4-month low. Consensus had anticipated an improvement in both new orders and employment. Per the ISM, "The mixed indicators in output suggest companies still being cautious in their hiring even with an increase in production."

- Inventories rose 2.5 points to 49.2, backlogs fell 2.8 points to 44.3, while supplier delivery times fell 1.9 points to 54.2. Sizeable improvements were seen on the trade front, albeit from weak levels: export orders were up 6.2 points to 46.3, with imports up 7.5 points to 47.4, both 4-month highs.

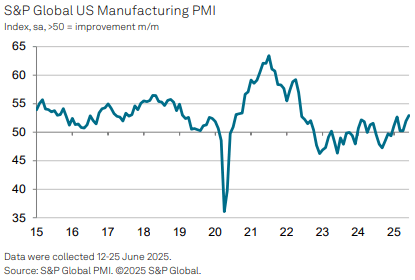

MNI US DATA: Mfg PMI Revised Higher In June Final, Uptrend In Prices Remains

The S&P Global manufacturing PMI was stronger than initially thought in June at 52.9 (flash and consensus 52.0) after 52.0 in May. It leaves it at its highest since May 2022. The improvement relative to the flash came as output charge inflation was marked down a touch, now seen at its highest since Sep 2022 vs Jul 2022 in the flash release, although an upward trend is still clear.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 473.93 points (1.07%) at 44570.06

S&P E-Mini Future up 4.75 points (0.08%) at 6258.5

Nasdaq down 130.5 points (-0.6%) at 20239.2

US 10-Yr yield is up 2.3 bps at 4.2514%

US Sep 10-Yr futures are down 9/32 at 111-27

EURUSD down 0.0001 (-0.01%) at 1.1786

USDJPY down 0.26 (-0.18%) at 143.77

WTI Crude Oil (front-month) up $0.56 (0.86%) at $65.67

Gold is up $35.79 (1.08%) at $3338.96

European bourses closing levels:

EuroStoxx 50 down 20.81 points (-0.39%) at 5282.43

FTSE 100 up 24.37 points (0.28%) at 8785.33

German DAX down 236.32 points (-0.99%) at 23673.29

French CAC 40 down 3.32 points (-0.04%) at 7662.59

US TREASURY FUTURES CLOSE

3M10Y -0.294, -7.902 (L: -16.082 / H: -6.009)

2Y10Y -3.402, 47.064 (L: 46.023 / H: 50.856)

2Y30Y -5.544, 99.557 (L: 98.771 / H: 105.299)

5Y30Y -3.925, 93.629 (L: 93.233 / H: 97.931)

Current futures levels:

Sep 2-Yr futures down 3.75/32 at 103-28.625 (L: 103-28.125 / H: 104-02)

Sep 5-Yr futures down 7.25/32 at 108-24.75 (L: 108-22.25 / H: 109-05)

Sep 10-Yr futures down 8.5/32 at 111-27.5 (L: 111-22.5 / H: 112-12.5)

Sep 30-Yr futures down 3/32 at 115-12 (L: 114-30 / H: 116-03)

Sep Ultra futures steady at 119-4 (L: 118-19 / H: 120-00)

MNI US 10YR FUTURE TECHS: (U5) Reverses Hard Off Highs

- RES 4: 114-14 High Apr 7 and key resistance

- RES 3: 113-07 76.4% retracement of the Apr 7 - 11 bear leg

- RES 2: 112-23 High May 1 and key resistance

- RES 1: 112-12/15 Intraday high / 61.8% of the Apr 7 - 11 sell-off

- PRICE: 111-23 @ 16:46 BST Jul 1

- SUP 1: 111-22 Low Jun 30

- SUP 2: 111-05+ 20-day EMA

- SUP 3: 110-28+ 50-day EMA

- SUP 4: 110-20 Low Jun 20

The bull cycle in Treasury futures remains intact, however prices reversed hard off highs into the Tuesday close. As such, the contract has failed on the approach to the next important resistance at 112-15, the 61.8% retracement of the Apr 7 - 11 steep sell-off. Clearance of this level would expose 112-23, the May 1 high. Note that the uptrend is overbought, a pullback would unwind this position. First key support to watch is 111-05+, the 20-day EMA.

SOFR FUTURES CLOSE

Sep 25 -0.005 at 95.985

Dec 25 -0.035 at 96.295

Mar 26 -0.060 at 96.540

Jun 26 -0.070 at 96.750

Red Pack (Sep 26-Jun 27) -0.07 to -0.065

Green Pack (Sep 27-Jun 28) -0.065 to -0.05

Blue Pack (Sep 28-Jun 29) -0.05 to -0.035

Gold Pack (Sep 29-Jun 30) -0.035 to -0.02

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.45% (+0.06), volume: $2.946T

- Broad General Collateral Rate (BGCR): 4.39% (+0.02), volume: $1.059T

- Tri-Party General Collateral Rate (TCR): 4.39% (+0.02), volume: $1.038T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $79B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $157B

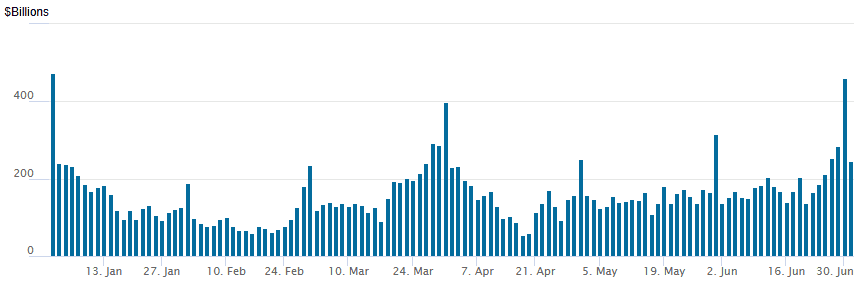

FED Reverse Repo Operation: Sharp Retreat as July Gets Underway

RRP usage retreats to $245.530B this afternoon from $460.731B yesterday (highest since December 31), total number of counterparties falls to 38 from 62. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021.

MNI PIPELINE: Corporate Bond Update: SoftBank Group Rolled to Wednesday

- Date $MM Issuer (Priced *, Launch #)

- 07/01 $750M *Türkiye Vakıflar Bankası 5Y 7.375%

- Rolled to Wednesday:

- 07/01 $Benchmark SoftBank Group 3.75Y 6.75%a, 5.5Y 7.125%a, 7 Y 7.500%a, 10Y 7.875%a (in addition to 3 EUR tranches) Note, SoftBank Corp issued $1B over 2 tranches on Monday.

MNI BONDS: EGBs-GILTS CASH CLOSE: Flattening To Start The Quarter

European yields pulled back Tuesday in a flattening move.

- There was a strong rally in early trade, largely following the cue of US Treasuries as the month/quarter got underway.

- Gains faded by mid-afternoon in Europe, with US data releases showing firmer-than-expected job openings, and still-elevated manufacturing sector prices.

- The German curve bull flattened on the day, with the UK's twist flattening. Periphery/semi-core EGB spreads widened slightly, with Greece underperforming.

- In data, Spanish PMI beat expectations but Italy missed. Eurozone June flash inflation metrics came in line with consensus though ECB 1-year and 3-year ahead inflation expectations both eased.

- BoE's Bailey reiterated that the direction of rates continues to be downwards, while ECB's Lagarde repeated that there was no commitment to any particular rate path.

- Wednesday's calendar includes labor market data for Italy, Spain and the Eurozone, and commentary from dovish BoE dissenter Taylor.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.2bps at 1.849%, 5-Yr is down 2.2bps at 2.148%, 10-Yr is down 3.3bps at 2.574%, and 30-Yr is down 4.7bps at 3.053%.

- UK: The 2-Yr yield is up 1bps at 3.827%, 5-Yr is down 1.4bps at 3.936%, 10-Yr is down 3.5bps at 4.454%, and 30-Yr is down 5bps at 5.229%.

- Italian BTP spread up 0.6bps at 87.5bps / Greek up 2.1bps at 71.1bps

MNI FOREX: USD Index Recovers From Trendline Support, US Yields Reverse

- It was a tale of two halves for the greenback on Tuesday as an initial extension of recent weakness USD index weakness to fresh cycle lows saw a solid recovery across the US session. Two key factors were at play here; the reversal higher for US yields from bearish extremes which was assisted by some stronger-than-expected US data and an important technical support holding for the DXY, a trendline drawn across the 2011 and 2021 lows.

- This dynamic prompted most G10 peers to erase early gains and slip into negative territory ahead of the APAC crossover. The Canadian dollar stands out here as an underperformer, falling 0.35% against the greenback. The likes of EURUSD and GBPUSD sit around 50 pips off their respective cycle highs.

- For EURUSD, it is worth flagging some interesting comments from ECB Vice President Luis de Guindos who told Bloomberg that the speed of the euro’s ascent is more worrying than its current level. Furthermore, De Guindos expressed the view that levels above 1.20 would provide a more complicated scenario. This may have helped EURUSD consolidate back below 1.18 today, while appetite for fresh EURUSD positions may be contained by the close proximity to this Thursday's US employment print.

- Yen volatility was notable, with an impressive 142.68-144.08 daily range. While dollar/rate dynamics were a primary driver of the day’s moves, it is worth noting the Q2 Japan Tankan survey painted a resilient picture and improved capex outlook, potentially providing an additional yen tailwind. As such, USDJPY remains 0.26% lower on the session despite the greenback turnaround.

- Wednesday’s data calendar is highlighted by Australian retail sales, Eurozone unemployment releases and US ADP. The focus then turns to US NFP and ISM Services data on Thursday, ahead of the July 04 holiday.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 02/07/2025 | 0800/1000 | ECB de Guindos Chairs Sintra Panel | ||

| 02/07/2025 | 0900/1100 | ** | Unemployment | |

| 02/07/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 02/07/2025 | 0900/1100 | ECB Cipollone Chairs Sintra Panel | ||

| 02/07/2025 | 1030/1230 | ECB Lane Chairs Sintra Panel | ||

| 02/07/2025 | 1030/1130 | BOE Taylor On Panel At Sintra Conference | ||

| 02/07/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 02/07/2025 | 1215/0815 | *** | ADP Employment Report | |

| 02/07/2025 | 1415/1615 | ECB Lagarde Gives Closing Sintra Remarks | ||

| 02/07/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 03/07/2025 | 2300/0900 | * | S&P Global Final Australia Services PMI | |

| 03/07/2025 | 2300/0900 | ** | S&P Global Final Australia Composite PMI | |

| 03/07/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 03/07/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 03/07/2025 | 0130/1130 | ** | Trade Balance | |

| 03/07/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 03/07/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI |