MNI ASIA OPEN: Beige Book Caps Soft Midweek Data

EXECUTIVE SUMMARY

- MNI FED: Beige Book: Economic Activity Declining Slightly

- MNI BOC: Holds Key Rate at 2.75%, Signals Potential Cut Amid Tariff Threat

- MNI BOC: Gov Macklem: Likelihood Of "Extreme" Trade War Scenario Has Come Down

- MNI US: CBO Determines Tariffs Would Shrink Deficits And Economy, Increase Inflation

- MNI US DATA: ADP Far Softer Than Expected But Still Solid Job-Changer Pay Growth

US/CANADA

MNI FED: Beige Book: Economic Activity Declining Slightly

The June 4 Beige Book reported that "economic activity has declined slightly since the previous report". Uncertainty was a key theme, with manufacturing activity and household consumption showing signs of weakness. Overall the outlook remained "slightly pessimistic and uncertain". Note responses were collected up to May 23, so it's unclear the degree to which this reflects developments such as the US-China trade war de-escalation on May 12.

MNI FED: Beige Book: Tariffs Increasing Price Pressures

The Beige Book suggested rising tariff-related inflationary pressures, with all 12 Fed Districts indicating that higher tariff rates were putting upward pressure on both input and output prices. Additionally, contacts appeared to suggest future price increases could be "substantial". Overall, "Prices have increased at a moderate pace since the previous report."

NEWS

MNI US: CBO Determines Tariffs Would Shrink Deficits And Economy, Increase Inflation

The Congressional Budget Office has noted in a letter to Senate Democrats that tariffs enacted by President Donald Trump would reduce deficits, reduce the size of the economy, and increase inflation. The CBO "estimates that the increase in collections of tariffs would reduce primary deficits by $2.5 trillion. That estimate accounts for how flows of U.S. imports and exports would adjust in response to the tariffs imposed as of May 13, 2025."

MNI US: Lawler Threatens To Tank Big Beautiful Bill If Senate Changes SALT Cap

Rep Mike Lawler (R-NY) warned in a statement on X that SALT Republicans could torpedo the 'Big Beautiful Bill' in the House, if the Senate changes the $40,000 State and Local Tax (SALT) deduction in the House-passed version of the bill. Lawler said: "Let’s be clear — no SALT, no deal... If the Senate changes the negotiated number of $40,000 — it will derail final passage of the bill."

MNI BOC: Holds Key Rate at 2.75%, Signals Potential Cut Amid Tariff Threat

Bank of Canada kept benchmark interest rate 2.75% Wednesday, in line with majority of economist expectations. Second consecutive decision to hold signaled potential cut if economy weakens and inflation contained. "On balance, members thought there could be a need for a reduction in the policy rate if the economy weakens in the face of continued US tariffs and uncertainty, and cost pressures on inflation are contained," Governor Macklem said. "At this decision there was a clear consensus to hold policy unchanged as we gain more information."

MNI BOC: Gov Macklem: Likelihood Of "Extreme" Trade War Scenario Has Come Down

Asked about how the economy is playing out relative to the two forecast scenarios in the April MPR, Gov Macklem says: "We're somewhere between the two scenarios, but it's still a moving target. And you know, we'll we'll have to see where things go....since April, the likelihood of scenario two, which is a pretty extreme, protracted, severe trade war - the likelihood of that does appear to have come down somewhat... I hope the situation becomes clear and we can go back to a more usual forecast, or at least a central scenario with with some some risks, but that's really going to depend on on how things play out."

US TSYS

MNI US TSYS: Holding Near Highs After Soft ADP, ISM Services Data

- Treasuries look to finish near midday highs Wednesday, projected rate cuts through year end back above 50bp again after this morning's soft ADP private payroll and ISM Services data.

- The Sep'25 10Y contract trades +22 at 111-04.5 vs. 111-07 high, testing resistance at 111-05.5 (High May 9)

- The ISM services report for May showed a painful combination of another increase in prices paid (highest since late 2022) and new orders slumping (lowest since late 2022); the overall index hit its lowest (and first sub-50 reading) since Jun 2024.

- ADP employment increased just 37k (sa, cons 114k) in May after a marginally downward revised 60k (initial 62k) in April. Consensus currently stands at 120k for Friday's private payrolls release.

- Later in the session, the June 4 Beige Book reported that "economic activity has declined slightly since the previous report" while suggesting rising tariff-related inflationary pressures.

- Off session lows, the Greenback nevertheless reversed the prior session gains after data set a negative tone for the US dollar on Wednesday. USDJPY sits 0.85% lower on the session, having had a punchy 165 pip turnaround from the overnight highs.

- Focus turns to Thursday's weekly jobless claims, trade balance and unit labor costs.

OVERNIGHT DATA

MNI US DATA: ISM Services Prices Paid vs New Order Gap Ratchets Wider Again

The ISM services report for May showed a painful combination of another increase in prices paid (highest since late 2022) and new orders slumping (lowest since late 2022). One of the few positive areas was an improvement in employment. The overall index hit its lowest (and first sub-50 reading) since Jun 2024. Whilst it’s only just sub-50, such readings are rare having now only seen four months below the breakeven line since mid-2020.

- ISM services: 49.9 (cons 52.0, 60 responses) in May after 51.6 in April – lowest since Jun 2024.

- New orders: 46.4 (cons 51.6, 4 responses) in May after 52.3 in April – lowest since Dec 2022.

- New export orders only fell 0.1pt to 48.5 vs the 5.9pt slide in overall new orders.

- Prices paid: 68.7 (cons 65.1, 6 responses) in May after 65.1 in April – highest since Nov 2022.

- Employment: 50.7 (cons 49.0, 4 responses) in May after 49.0 in April – highest since Feb 2025.

MNI US DATA: ADP Far Softer Than Expected But Still Solid Job-Changer Pay Growth

The ADP employment and pay insights report for May showed a further significant miss, with the slowest monthly pace of hiring since March 2023. Weakness was widespread and whilst familiar NFP correlation concerns remain, the ADP data points to a clearly softening trend. That said, job changer pay growth saw a second month at 7.0% Y/Y for its strongest since Aug 2024, something we wouldn’t expect to see amidst a sharper cooling in the labor market.

- ADP employment increased just 37k (sa, cons 114k) in May after a marginally downward revised 60k (initial 62k) in April. Consensus currently stands at 120k for Friday's private payrolls release. ADP has undershot private payrolls in each of the prior three months, by a large 107k in Apr, 23k in Mar and 23k in Feb (all according to latest vintages). That said, despite the weak correlation with payrolls, ADP data has appeared to recently have a smoother trend and it's pointing in a quickly moderating direction.

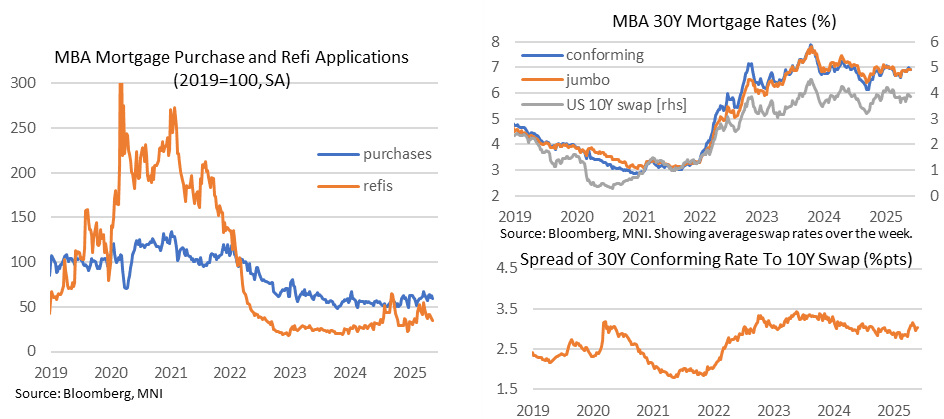

MNI US DATA: Mortgage Applications Dip Despite Modest Rate Relief

MBA composite applications dipped -3.9% last week (sa) for a third consecutive weekly decline. Unusually, it was led by new purchases (-4.4% admittedly after 2.7%) whilst refis fell further (-3.5% after -7.1%).

- Relative levels for context: composite applications at 48% of 2019 averages (lowest since late April), new purchases at 60% (lowest since late April) and refis at 35% (lowest since Feb). The decline came despite the 30Y conforming mortgage rate falling 6bps to 6.92%, to reverse the prior week’s increase to what had been its highest since January.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 62.33 points (-0.15%) at 42448.07

S&P E-Mini Future up 2.5 points (0.04%) at 5982.25

Nasdaq up 73.8 points (0.4%) at 19468.53

US 10-Yr yield is down 9.3 bps at 4.3611%

US Sep 10-Yr futures are up 21.5/32 at 111-4

EURUSD up 0.0041 (0.36%) at 1.1414

USDJPY down 1.09 (-0.76%) at 142.88

WTI Crude Oil (front-month) down $0.63 (-0.99%) at $62.80

Gold is up $20.2 (0.6%) at $3373.66

European bourses closing levels:

EuroStoxx 50 up 29.45 points (0.55%) at 5405.15

FTSE 100 up 14.27 points (0.16%) at 8801.29

German DAX up 184.86 points (0.77%) at 24276.48

French CAC 40 up 40.83 points (0.53%) at 7804.67

US TREASURY FUTURES CLOSE

3M10Y -10.252, 0.783 (L: -0.591 / H: 11.045)

2Y10Y -1.016, 48.839 (L: 47.685 / H: 50.629)

2Y30Y -1.491, 101.094 (L: 99.5 / H: 102.998)

5Y30Y -0.683, 95.162 (L: 93.524 / H: 96.772)

Current futures levels:

Sep 2-Yr futures up 5.625/32 at 103-25.375 (L: 103-18.75 / H: 103-26.125)

Sep 5-Yr futures up 13.75/32 at 108-12.75 (L: 107-28.75 / H: 108-14.5)

Sep 10-Yr futures up 21/32 at 111-3.5 (L: 110-12 / H: 111-07)

Sep 30-Yr futures up 1-14/32 at 113-17 (L: 111-29 / H: 113-25)

Sep Ultra futures up 1-26/32 at 116-27 (L: 114-27 / H: 117-06)

MNI US 10YR FUTURE TECHS: (U5) Testing Resistance

- RES 4: 112-04+ High May 2

- RES 3: 111-25 High May 7

- RES 2: 111-07 Intraday high

- RES 1: 111-05.5 High May 9

- PRICE: 111-04+ @ 1550 ET Jun 4

- SUP 1: 109-26/12+ Low May 29 / 22 and the bear trigger

- SUP 2: 109-09+ Low Apr 11 and key support

- SUP 3: 109-00 Round number support

- SUP 4: 108-25+ 0.764 proj of the Apr 7 - 11 - May 1 price swing

Treasury futures are holding on to the bulk of their recent gains. A dominant bear cycle remains in play for now, and recent gains still appear corrective. However, the contract has breached an important resistance at 110-23, the May 16 high. A clear breach of this level would undermine a bear theme and highlight a stronger reversal, exposing 111-05+, May 9 high. For bears, a resumption of weakness would refocus attention on 109-12+, May 22 low.

SOFR FUTURES CLOSE

Jun 25 +0.008 at 95.695

Sep 25 +0.045 at 95.950

Dec 25 +0.080 at 96.235

Mar 26 +0.095 at 96.460

Red Pack (Jun 26-Mar 27) +0.095 to +0.105

Green Pack (Jun 27-Mar 28) +0.090 to +0.090

Blue Pack (Jun 28-Mar 29) +0.085 to +0.085

Gold Pack (Jun 29-Mar 30) +0.085 to +0.090

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.32% (-0.03), volume: $2.711T

- Broad General Collateral Rate (BGCR): 4.30% (-0.02), volume: $1.082T

- Tri-Party General Collateral Rate (TCR): 4.30% (-0.02), volume: $1.045T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $120B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $297B

FED Reverse Repo Operation

RRP usage rises to $168.882B this afternoon from $153.177B yesterday, total number of counterparties at 45. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

MNI PIPELINE: Corporate Bond Roundup: $2.75B Brazil 2Pt Launched

$13.4B to price Wednesday

- Date $MM Issuer (Priced *, Launch #)

- 06/04 $2.75B #Brazil $1.5B +5Y 5.68%, $1.25B 2035 tap 6.73%

- 06/04 $2.5B *British Colombia 10Y SOFR+95

- 06/04 $2B *IDA (Int Development Assn) 5Y SOFR+46

- 06/04 $1.75B #Macquarie $750M 3Y +50, $1B 3Y SOFR+74

- 06/04 $1.5B #Targa Resources $750M 5Y +100, $750M +10Y +133

- 06/04 $1.25B #RBC 60NC5 6.75%

- 06/04 $1B #Cemex PerpNC5 7.2%

- 06/04 $650M #Gerdau Trade 10Y +140

MNI BONDS: EGBs-GILTS CASH CLOSE: German Curve Twist Flattens Pre-ECB

European curves flattened Wednesday, with Gilts outperforming Bunds.

- Bunds softened early, with Eurozone services PMI revised up, the German cabinet approving corporate tax cuts, and equities gaining ground. EGB weakness spilled over into Gilts.

- Afternoon moves in Gilts in particular tracked US Treasuries, which were buoyed by soft ADP private payroll and ISM Services data.

- For the session, the German curve twist flattened, with the UK's bull flattening.

- Periphery/semi-core EGB spreads were little changed; BTPs modestly outperformed.

- The ECB meeting, with an expected 25bp cut, is Thursday's focus - MNI's preview is here.

- We also get BoE DMP survey, and appearances by Greene and Breeden.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.2bps at 1.798%, 5-Yr is up 1.6bps at 2.098%, 10-Yr is up 0.3bps at 2.528%, and 30-Yr is down 1.8bps at 2.999%.

- UK: The 2-Yr yield is down 2.3bps at 4.005%, 5-Yr is down 2.8bps at 4.115%, 10-Yr is down 3.2bps at 4.606%, and 30-Yr is down 4.5bps at 5.322%.

- Italian BTP spread down 0.6bps at 96.4bps / French OAT up 0.3bps at 67.3bps

MNI FOREX: Greenback Sold on Weak US Data, Safe Havens Outperform

- Weaker-than-expected ADP employment data in the US set a negative tone for the US dollar on Wednesday, sentiment that was exacerbated by a soft ISM services print. With an associated move lower for US yields, notorious safe havens such as JPY and CHF are outperforming on Tuesday.

- USDJPY sits 0.85% lower on the session, having had a punchy 165 pip turnaround from the overnight highs. A bear cycle for the pair remains in play and sights remain on the next important support at 142.12, the May 27 low. Clearance of this level would confirm a resumption of the bear leg and open 139.89, the Apr 22 low. In similar vein, USDCHF (-0.76%) has gravitated back below the 0.82 handle, although spot remains just shy of the week’s lows at 0.8157.

- A moderately hawkish lean to the BOC decision is providing an additional tailwind for the Canadian dollar, with communications keeping the door open to a cut but not emphatically (Macklem's opening statement: "We also discussed the path ahead for the policy interest rate. Here, there was more diversity of views.”)

- USDCAD reaches fresh cycle lows below 1.3675, keeping bearish technical conditions firmly intact for the pair. Sights are on 1.3643 next, the Oct 9 low/Sep high. Below here, attention will be on 1.3579, the 1.5 Fibonacci projection of the Feb 3 - 14 - Mar 4 price swing, before the September lows at 1.3420 will garner attention.

- EURUSD regained the 1.14 handle amid the broad dollar weakness, but remains below the week’s best levels ahead of the ECB meeting on Thursday, where a 25bp rate cut is widely expected and forecast revisions will be of particular interest. Attention will then swiftly turn to Friday’s release of US employment data.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 05/06/2025 | 0545/0745 | ** | Unemployment | |

| 05/06/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 05/06/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 05/06/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 05/06/2025 | 0745/0845 | BOE's Greene Opening Remarks at Econdat Conference 2025 | ||

| 05/06/2025 | 0800/1000 | * | Retail Sales | |

| 05/06/2025 | 0830/0930 | Decision Maker Panel data | ||

| 05/06/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 05/06/2025 | 0900/1100 | ** | PPI | |

| 05/06/2025 | 1215/1415 | *** | ECB Deposit Rate | |

| 05/06/2025 | 1215/1415 | *** | ECB Main Refi Rate | |

| 05/06/2025 | 1215/1415 | *** | ECB Marginal Lending Rate | |

| 05/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 05/06/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 05/06/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 05/06/2025 | 1230/0830 | ** | Trade Balance | |

| 05/06/2025 | 1230/0830 | ** | Non-Farm Productivity (f) | |

| 05/06/2025 | 1230/0830 | ** | Trade Balance | |

| 05/06/2025 | 1245/1445 | ECB Press Conference | ||

| 05/06/2025 | 1400/1000 | * | Ivey PMI | |

| 05/06/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 05/06/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 05/06/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 05/06/2025 | 1600/1200 | Fed Governor Adriana Kugler | ||

| 05/06/2025 | 1620/1220 | BOC Deputy Kozicki speech | ||

| 06/06/2025 | 2330/0830 | ** | Household spending |