MNI ASIA MARKETS ANALYSIS:Chip Makers, Media Cos Rattle Stocks

HIGHLIGHTS

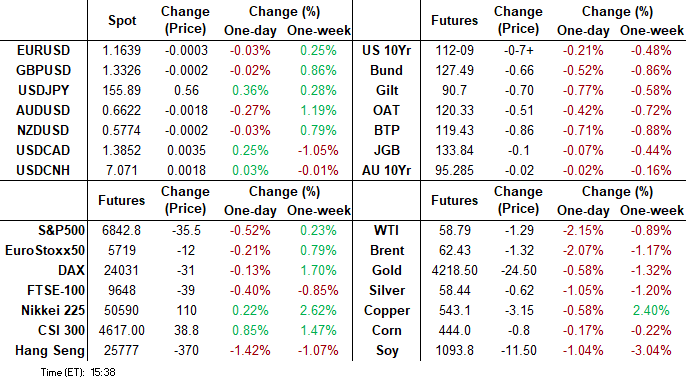

- Treasuries extended midmorning lows, less headline than flow driven with heavy selling pushed TYH6 back to Oct 7 lows.

- Stocks retreat partially tied to a decline in projected rate cut pricing after what may prove to be a contentious FOMC meeting Wednesday (25bp rate cut still largely expected but with a hawkish guidance).

- A round of hawkish communique from ECB’s Schnabel provided the initial selling impetus for German bonds today, extending on the theme seen last week.

US TSYS

MNI US TSYS: Yields Rise Ahead Expected Contentious FOMC Wednesday

- Treasuries remain under moderate pressure late Monday, near the mid-range for the day by the bell: Mar'26 10Y contract trades -8 at 112-08.5, 10Y yield +.0351 at 4.1702%.

- Treasury had extended lows at midmorning (TYH6 112-02.5 September 25 lows), more flow driven on heavier volumes, rather than headline at least in the first half.

- Treasuries rebound off lows after NY Fed Consumer Sentiment Survey recedes to 3.20% from November's 3.24%. A strong Tsy 3Y auction, drawing 3.614% high yield vs. 3.622% WI, contributed to the bounce off session lows.

- The main focus is on Wednesday's FOMC decision, widely expected to deliver a third consecutive 25bp cut after NY Fed Williams’ uncharacteristic guidance following the delayed September payrolls report. Potentially contentious meeting with many FOMC members preferring to have paused.

- The dot plot distribution will be watched keenly whilst we expect the economic projections to show an upward revision for GDP growth and downward revision for core PCE inflation.

- The FOMC will also see two months of JOLTS data on the first day of their two-day meeting otherwise must wait until the following week for NFP (Dec 16) and CPI (Dec 18) reports for November.

- Tuesday Data Calendar: ADP Weekly, Redbook and JOLTS for Sep/Oct; Treasury auctions include $39B 10Y note reopen.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.93% (+0.01), volume: $3.221T

- Broad General Collateral Rate (BGCR): 3.90% (+0.03), volume: $1.321T

- Tri-Party General Collateral Rate (TCR): 3.90% (+0.03), volume: $1.295T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.89% (+0.00), volume: $88B

- Daily Overnight Bank Funding Rate: 3.89% (+0.00), volume: $167B

FED Reverse Repo Operation

RRP usage inches up to $1.703B with 6 counterparties this afternoon from $1.485B Friday. Compares to Tuesday November 18: $0.905B - lowest level since mid-March 2021; this years highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

FI desks reported mixed SOFR & Treasury options with some position adjustments ahead of Wed's FOMC policy annc, anticipating a hawkish cut. Underlying futures moderately lower/off lows, curves mixed (2s10s +1.420 at 58.689, 5s30s -1.600 at 106.174). Projected rate cut pricing near steady vs this morning's levels (*): Dec'25 at -24.7bp (-24.9bp), Jan'26 at -31.4bp (-31.0bp), Mar'26 at -38.3bp (-38.7bp), Apr'26 at -44.4bp (-45b).

SOFR Options:

-20,000 0QH6 97.25/97.50 call spds, 2.25 ref 96.79

Block, -10,000 0QZ5 96.75 puts, 2.0 vs. 96.80/0.28%

+2,000 SFR5 96.18 puts, 1.0

2,000 SFRZ6 96.31/96.43/96.56 call flys ref 96.265

14,000 SFRZ6 96.87/97.37 call spds 0.5 over 96.50 puts

1,100 SFRG6 96.25/96.37/96.43/96.50 broken put condors

6,700 SFRZ5 96.50/96.87/97.37 broken call trees ref 96.83

+3,000 SFRZ5 96.18/96.25/96.31 put flys, 2.5 ref 99.265

Block, +4,300 SFRH6 96.18/96.43/96.56 broken put flys, 0.0 ref 96.43

-5,250 SFRZ5 96.31/96.37 call spds, 0.25 net ref 96.265

Blocks +6,000 0QH6 96.12/96.25/96.37 put flys, 0.5

+3,370 SFRZ6 99.00/100/101 call flys, 2 vs. 96.89/0.05%

1,785 SFRZ5 96.31/96.37 call spds ref 96.265

1,350 0QZ5 96.62/96.87/97.00/97.12 broken put condors ref 96.835

-10,000 0QF6 96.93/97.06 call spds, 3 ref 96.85

Treasury Options:

11,187 TYG6 110.5/112.5 3x2 put spds, 109 net ref 112-10

30,000 TYF6 112.75/113.5 call spds, 11 net vs. 112-07 to -07.5

8,000 wk2 TY/TYF6 112 put spds

+6,000 TYH6 112 straddles, 2-00 vs. 112-07.5/0.06%

Block, 10,160 USG6/USH6 111 put spds 19 net, Mar'26 over ref 115-01

2,900 TYF6 113/113.5/114.5 broken call flys

4,000 TYF6 113/113.5 1x2 call spds, 1 net 2-leg over ref 112-13 to -13.5

4,400 FVF6 108.5/110.25 strangle vs. FVG6 108.25/110.25 strangle

over 4,000 TYH6 110 puts, 14

2,000 TYF6 110/111.5 put spds ref 112-13

2,000 TYF6 110.5/112 put spds ref 112-13

over 39,800 TYF6 112 puts, 17-20

5,650 TUH6 104 puts, 9

1,500 TYF6 113 straddles

+2,000 TYF6 112/113 2x5 call spds 10

+4,000 TYF6 111.5 puts, 9 vs. 112-16/0.18%, total volume over 10k

+1,500 TYH6 113.5 calls vs. TYG6 114 calls, 20 net (Mar over)

-20,000 TYF6 112/112.5 put spds vs. 114.5 calls, 11 net ref 112-15

+1,600 FVF6 108.25/108.75 put spds, 6.5 vs. 109-06.25

+5,000 TYF6 111.25/112.25 put spds vs. 113.5/114.5 call spds 12 net ref 112-115

over 7,100 wk2 TY 112.5 puts, 14 exp Fri

+2,130 TYH6 110/111/112 put flys, 9 ref 112-18

MNI FOREX: JPY and CHF Underperform as Core Yields Shift Higher

- Despite the correlation breakdown between rates and the Japanese yen in recent months, higher core yields on Monday have weighed on the low yielders, with JPY and CHF underperforming the G10 basket. A round of hawkish communique from ECB’s Schnabel provided the initial selling impetus for bonds today, extending on the theme seen last week.

- Both USDJPY and USDCHF have risen around 0.35%, assisting the USD index to further recover from last weeks pullback lows as we approach this week’s Fed decision, where market pricing leans heavily towards the FOMC cutting rates by 25bps.

- The bounce for USDJPY was also assisted by a magnitude-7.6 earthquake that struck off the northeast coast, prompting urgent evacuation warnings for coastal areas of northern Japan. These dynamics boosted USDJPY from its overnight 154.91 lows to a session high of 155.99. Last week’s deep retracement for USDJPY has allowed an overbought condition to unwind, and today’s bounce underpins the underlying bullish theme for the pair.

- The more constructive dollar backdrop prompted the likes of CAD and AUD to scale back from recent highs, although both currencies continue to exhibit short-term bullish signals as both RBA and BOC decisions are awaited over the next two sessions.

- Schnabel’s initial Euro boost was very short-lived, as EURUSD faded from1.1672 session highs and sits close to 1.1630 as we approach the NY crossover. Last week’s breach of meaningful 1.1656 resistance has failed to garner much topside momentum, as the tepid optimism surrounding Russia/Ukraine peace talks might be dissipating. Zelenskiy said negotiators discussing a US-brokered peace initiative remain divided over territory amid Trump’s disappointment, and polymarket still assigns a <50% probability of a ceasefire in 2026.

- The RBA meeting highlights Tuesday’s calendar, before US weekly ADP and September JOLTS data are scheduled. BOJ’s Ueda and RBNZ’s Breman are scheduled to speak.

MNI OPTIONS: Expiries for Dec09 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1585-90(E1.7bln), $1.1600(E755mln), $1.1675(E784mln), $1.1760(E1.3bln)

- EUR/GBP: Gbp0.8785-92(E530mln)

- AUD/USD: $0.6330-35(A$1.2bln)

MNI US STOCKS: Late Equities Roundup: Chip Makers And Broadcast Entertainment Making Waves

- Stocks are extending late Monday lows as headlines regarding a takeover bid by Paramount Skydance of Warner Bros Discovery continued to make the rounds. Currently, the DJIA trades down 257.36 points (-0.54%) at 47695.75, S&P E-Mini Futures down 32.75 points (-0.48%) at 6844.75, Nasdaq down 82.5 points (-0.4%) at 23493.44.

- Senator Warren called the hostile bid a "five alarm antitrust fire" after Fortune reported Jared Kushner’s "fully owned private equity firm, Affinity Partners, as one of four outside financing partners backing the offer, alongside the sovereign wealth funds of Saudi Arabia, Abu Dhabi, and Qatar."

- Stocks were paring losses just prior to the Paramount headlines after Semafor reported the US Department of Commerce will ease export restrictions of NVIDIA GPUs to China.

- Weaker stocks were also partially tied to a decline in projected rate cut pricing after what may prove to be a contentious FOMC meeting (25bp rate cut still largely expected but with a hawkish guidance).

- Communication Services and Consumer Discretionary sector shares led late session declines: Netflix declined -3.89% after Pres Trump expressed concern over a $72B take over bid for Warner Bros was announced late last week), while T-Mobile US declined -2.52%, Alphabet -2.56% and Comcast -2.33%.

- Conversely, Paramount Skydance surged +7.33% and Warner Bros Discovery +3.36% (not the same as WB) after the former announced a $108.4B hostile takeover bid for WBD.

- Meanwhile, Lululemon Athletica -4.89%, Tesla -4.22%, DR Horton -3.05%, Royal Caribbean Cruises -2.92% and Ralph Lauren -4.19% weighed on the Discretionary sector.

- On the positive side, Information Technology and Industrials sector shares outperformed in the first half:

- Hewlett Packard Enterprise +2.64%, ON Semiconductor +2.50%, Lam Research +2.46% and Broadcom +2.35%.

- Huntington Ingalls Industries +2.65%, Lockheed Martin +2.28%, Boeing +1.96% and EMCOR Group +1.20%.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Bullish Cycle Intact

- RES 4: 7000.00 Psychological round number

- RES 3: 6953.75 High Oct 30 and bull trigger

- RES 2: 6918.50 High Oct 31

- RES 1: 6905.00 High Dec 5

- PRICE: 6842.50 @ 14:28 ET Dec 8

- SUP 1: 6797.09 20-day EMA

- SUP 2: 6749.07 50-day EMA

- SUP 3: 6674.50 Low Nov 25

- SUP 4: 6525.00 Low Nov 21 and a key support

A bullish theme in S&P E-Minis is intact. Price remains above the 20- and 50- day EMAs. Note that recent gains signal the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would highlight potential for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low. First support is at 6797.09, the 20-day EMA.

COMMODITIES

MNI Oil End of Day Summary: WTI Falls

WTI has fallen today, unwinding gains seen late last week, but still within the range seen in recent weeks as the market weighs an expected US Fed rate cut this week alongside geopolitical developments.

- WTI JAN 26 down 2% at 58.87$/bbl

- US President Trump said that he was disappointed with how Ukraine’s President Zelenskyy has treated the latest US proposal and accused him of not reading it.

- The US and Ukraine agreed on a “framework for security arrangements” with “necessary deterrence capabilities to sustain a lasting peace”, according to the US State Department.

- West Qurna 2 oilfield output has been reduced by around 300k b/d to nearly 150k b/d, sources told Argus, after a leak at a storage depot.

- CPC will not return to full export capacity until at least Dec. 11, after a Ukrainian drone attack damaged SPM-2 on Nov. 29: Reuters.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 09/12/2025 | 0700/0800 | ** | Trade Balance | |

| 09/12/2025 | 1000/1000 | * | Index Linked Gilt Outright Auction Result | |

| 09/12/2025 | 1100/0600 | ** | NFIB Small Business Optimism Index | |

| 09/12/2025 | - | FOMC Meetings with S.E.P. | ||

| 09/12/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 09/12/2025 | 1415/1415 | BOE Lombardelli, Ramsden, Dhingra, Mann at TSC | ||

| 09/12/2025 | 1500/1000 | *** | JOLTS jobs opening level | |

| 09/12/2025 | 1500/1000 | *** | JOLTS quits Rate | |

| 09/12/2025 | 1700/1200 | *** | USDA Crop Estimates - WASDE | |

| 09/12/2025 | 1800/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 09/12/2025 | - | Bank of Canada Meeting | ||

| 10/12/2025 | 0130/0930 | *** | CPI | |

| 10/12/2025 | 0130/0930 | *** | Producer Price Index |