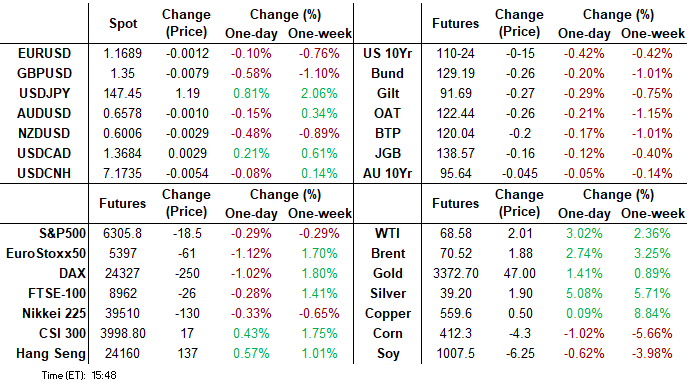

MNI ASIA MARKETS ANALYSIS: Yields Gain Ahead Next Wks June CPI

HIGHLIGHTS

- Early overnight support in Treasuries after Trump calls for 35% tariff on Canadian goods (and the hint of a "major statement" about Russia on Monday) gradually faded through the NY session.

- Next week's June CPI is the highlight of next week's US data slate, with MNI's early roundup of analyst expectations showing an anticipated acceleration in the main measures of inflation.

- The USD index extended its cautious recovery from last week’s cycle lows to ~1.5%, off its best levels, the DXY is threatening a close above 20-day EMA resistance which would mark a bullish development.

US TSYS

MNI US TSYS: Tsys Hug Lows, Curves Bear Steepen, Focus on Next Week's CPI

- Treasuries look to finish weaker late Friday, curves bear steepening with the short end outperforming despite large late session selling in Sep'25 SOFR futures.

- Tariff headlines buoyed Treasuries briefly overnight -- gaining after Pres Trump announced a 35% tariff on Canada starting August 1, while considering 15%-20% tariffs on most other trading partners. Support for Treasuries gradually faded as exact tariff details still to be annc'd (whether USMC trade exemptions will still apply). Rates ignored Trump to make a "major statement" on Russia Monday while stocks retreated.

- Currently, Sep'25 10Y futures trade -14.5 at 110-24.5 vs. 110-22.5 low (10Y yld tapped 4.4253% high), breaching the 50-day EMA, at 110-31+. This undermines a recent bull theme and exposes 110-17 next, a Fibonacci retracement point and a key support. Resistance to watch is at 111-28, the Jul 3 high.

- Curves rebound from Thursday's lows, 2s10s +4.826 at 52.384, 5s30s +4.263 at 97.617. Projected rate cut pricing consolidated slightly vs morning (*) levels: Jul'25 at -1.2bp (-1.7bp), Sep'25 at -17bp (-17.8bp), Oct'25 at -31.7bp (-32.7bp), Dec'25 at -49.6bp (-50.9bp).

- Data limited to Federal Budget Balance - U.S. government posted a USD27 billion budget surplus for June, up USD98 billion from a year earlier, reflecting strong tax receipts and collections of import duties. Focus on next week's CPI, PPI, Retail Sales and UofM inflation/sentiment data.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.31% (-0.01), volume: $2.735T

- Broad General Collateral Rate (BGCR): 4.30% (-0.01), volume: $1.123T

- Tri-Party General Collateral Rate (TCR): 4.30% (-0.01), volume: $1.098T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $106B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $284B

FED Reverse Repo Operation:

RRP usage slipped to $181.637B this afternoon from $183.339B yesterday, total number of counterparties at 37. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to yesterday's (July 1) $460.731B highest usage since December 31.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury option flow shifted to upside calls in the second half Friday. Fading underlying futures - near lows, curves unwinding yesterday's flattening (2s10s +4.587 at 52.145) despite some large late day selling in Sep'25 SOFR futures at 95.865 (-0.020). Projected rate cut pricing consolidated slightly vs morning (*) levels: Jul'25 at -1.2bp (-1.7bp), Sep'25 at -17bp (-17.8bp), Oct'25 at -31.7bp (-32.7bp), Dec'25 at -49.6bp (-50.9bp).

SOFR Options:

+10,000 TYV5 113/115 call spds, 15 ref 110-25.5

+5,000 SFRU5 95.75/96.00/96.25 call trees, 9.0 ref 95.87

-1,500 0QQ5 96.50/96.75 strangles, 14.75 ref 96.735

+2,000 SFRU5 96.00/96.12/96.18 broken call flys, 1.0 ref 95.87

+2,000 SFRZ5 96.12 straddles, 36 ref 96.195/0.05%

+1,000 SFRU5 95.87/95.93/96.00/96.12 broken call condors, 1.25

over 5,000 SFRN5 95.87 straddles ref 95.87

3,000 SFRQ5 95.81 puts, ref 95.87

1,000 0QZ5 97.25/98.00 call spds ref 96.785

2,000 SFRU5 96.12/96.18 call spds, .75 ref 95.895/0.04%

+3,000 SFRQ5 96.00/96.06/96.12/96.18 call condors, 0.5 ref 95.865

2,000 SFRM5 95.81/95.87/95.93 put trees, 5.5

Treasury Options:

5,000 USQ5 118 calls, 3 ref 113-00

3,000 USQ5 113.5/115/117broken call flys, 19 ref 113-01

+10,000 FVQ 109 calls, 4

+10,000 TYV5 113/115 call spds, 15

1,500 FVQ5 107.75/108.5 3x1 put spds, 4 net/1-leg over ref 108-04.75

6,000 TUU5 104/104.5 call spds ref 103-20.38

+7,500 TYU5 111 straddles, 138 ref 110-28, appr 5.3% implied vol

4,000 TYV5 113.5/114.5 call spds ref 110-26.5

+17,000 FVQ5 107.75 puts 5.5-6

-3,000 TYQ5 111 straddles, 51

+1,500 USQ5 110 puts, 5 ref 113-13/0.06%

+2,500 USQ5 119 calls, 2

over 5,600 TYQ5 110.5 puts, ref 110-29, part tied to 111 put on 2x1 ratio

+10,300 TYU5 109.5/110.5 put spds vs. 112.5 calls, 2 net ref 110-30.5

+2,500 Wednesday wkly US 115 calls, 9

4,000 Wednesday wkly 10Y 111.75/112 call spds, 3 ref 111-09.5 to -08.5 (exp 7/16)

+2,500 TYQ5 114.25 calls, 1

+2,000 TYU5 111.5 calls, 42 vs. 111-05.5/0.42%

MNI BONDS: EGBs-GILTS CASH CLOSE: Week Closes With Notable Bear Steepening

Weakness across core FI Friday cemented a bear steepening move for the week as a whole.

- For yet another session this week, there were few overt macro / headline drivers of weakness, with the broader theme of fiscal concerns continuing to weigh on Bunds and Gilts alike.

- After the US overnight announced 35% tariffs on Canada, there was expectation of the EU rate being revealed Friday, though market participants appeared to largely shrug this off.

- Gilts saw little market reaction to softer-than-expected May GDP data, with upward revisions dulling any dovish impulse.

- ECB's Schnabel was typically hawkish, noting that the bar for another cut is very high.

- Both the German and UK curves bear steepened. 10Y Bund saw its highest daily close since March 31, with 30Y since 2011.

- For the week as a whole, both the UK and German curves bear steepened: for the UK, 2Y +0.4bp, 10Y +6.8bp; Germany underperformed: 2Y +8.4bp, 10Y +11.8bp.

- Fitch is scheduled to review Germany's rating after Friday's close (AAA; Outlook Stable). Next week's European calendar highlights are UK-centric, with CPI and labour market data and BOE's Bailey delivering the Mansion House speech.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1bps at 1.9%, 5-Yr is up 1.5bps at 2.288%, 10-Yr is up 2bps at 2.725%, and 30-Yr is up 2.4bps at 3.227%.

- UK: The 2-Yr yield is unchanged at 3.856%, 5-Yr is up 1.7bps at 4.043%, 10-Yr is up 2.7bps at 4.622%, and 30-Yr is up 2.7bps at 5.433%.

- Italian BTP spread down 0.8bps at 84.6bps / French OAT down 0.6bps at 68.8bps

MNI EGB OPTIONS: Busier Session To End The Week Sees Downside Lean In Euro Rates

Friday's Europe rates/bond options flow included:

- RXQ5 129p, bought for 46.5 in 10k vs 4.6k at 129.18

- ERQ5 98.125/98.1875/98.25/98.3125c condor, sold at 1 in 3.8k

- ERU5 98.1875/98.125/98.0625/98.00 put condor 14K sold at 0.5 all day

- ERU5 98.1875/98.3125cs 1x2, bought for 1.5 in 5k

- ERU5 98.12/98.25/98.37 call fly 10K given at 3.25.

- ERU5 98.0625/98.00/97.9375 1x3x2 put fly paper paid 1 on 5K

- ERH6 98.25/98.125ps, bought for 6.5 in 30k

- SFIZ5 97.15/97.40cs, bought for half in 2k

MNI FOREX: USDCAD Completes Round Trip Following Stellar Employment Report

- The USD index is rising once again on Friday, extending its cautious recovery from last week’s cycle lows to ~1.5%. Although off its best levels, the DXY is threatening a close above 20-day EMA resistance which would mark a bullish development.

- The Canadian dollar has been a focus in G10 today following President Trump’s latest letter to Prime Minister Mark Carney and the announcement that Canada will face a 35% tariff on exports to the United States starting August 1. This prompted a rapid spike for USDCAD during APAC hours, from levels around 1.3655 to an intra-day peak of 1.3731.

- However, a reversal lower was then accelerated following a positive set of June employment data in Canada. Despite the composition of job gains being heavily tilted towards part-time, the lower-than-expected unemployment rate (6.9% vs 7.1% expected) has seen a notable repricing of July easing expectations, which worked in favour of the Canadian dollar.

- As such, USDCAD eroded the entirety of the Trump letter rally from overnight to print a fresh session low by 1 pip at 1.3652. On the downside, sights remain on key support at 1.3540, the Jun 16 low. Clearance of this level would resume the technical downtrend.

- GBP remains weaker following this morning's second consecutive month of negative growth in May, with fiscal concerns also remaining a headwind for the pound. For GBPUSD, spot broke to fresh weekly lows below the 1.35 handle, to then test key 50-day EMA support which intersects today at 1.3481. Below here, a key trendline drawn from the January lows comes in just above the 1.34 mark.

- Higher core yields today also worked in favour of USDJPY (+0.75%), which extends the week’s advance to 2% as we approach the close. The latest bullish wave has seen the pair narrow the gap to 148.03, the Jun 23 high.

- Chinese trade and activity data are early data highlights next week, while US CPI dominates the global calendar.

MNI OPTIONS: Expiries for Jul11 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500(E2.1bln), $1.1550(E581mln), $1.1700(E1.4bln), $1.1770(E2.4bln), $1.1825-40(E1.8bln)

- USD/JPY: Y146.30($649mln), Y146.75-90($667mln)

- AUD/USD: $0.6550-60(A$580mln)

- USD/CAD: C$1.3625-45($ C$1.3700-15($1.1bln)

MNI US STOCKS: Late Equities Roundup: Paring Shorts Ahead the Weekend

- Stocks trade mildly weaker late Friday, off session lows with the Nasdaq outperforming. Currently, the DJIA trades down 252.85 points (-0.57%) at 44398.79, S&P E-Minis down 14.75 points (-0.23%) at 6309.75, Nasdaq down 10.2 points (0%) at 20620.63.

- SPX eminis and Nasdaq indexes had retreated from the prior sessions all-time highs early Friday, eminis near flat for the week -- retreating late Thursday evening after Pres Trump called for 35% tariff on Canadian goods to commence August 1. Weaker price action was relatively contained, however, as exact tariff details still to be announced (whether USMC trade exemptions will still apply).

- Health Care sector shares reversed the prior session gains with pharmaceuticals leading decliners in late trade: Molina Healthcare -3.58%, Gilead Sciences -3.98%, Bristol-Myers Squibb -3.36% and Centene -2.92%.

- Materials and Financial sectors also underperformed, laggers included: Albemarle -3.82%, Dow Inc -2.33% and Freeport-McMoRan -2.29%; financial services stocks included Mastercard -2.84%, Visa -1.87% and Corpay Inc -2.58%.

- Reminder, banks and financial stocks report earning next week Tuesday: Blackrock, JPMorgan Chase & Co, Wells Fargo & Co, Bank of New York Mellon, State Street Corp and Citigroup.

- On the positive side, Energy and Information Technology sectors outperformed, Energy sector buoyed by Halliburton +3.14%, Baker Hughes +1.98%, Schlumberger +1.36% and Diamondback Energy +1.15%. Meanwhile, semiconductor stocks supported IT: Advanced Micro Devices +1.9%, NVIDIA +1.19%, Micron Tech +1.10% and Lam Research +0.91%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Trend Needle Points North

- RES 4: 6402.44 1.382 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6381.00 1.764 proj of the Apr 7 - 10 - 21 price swing

- RES 2: 6356.12 1.236 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6335.50 High Jul 10

- PRICE: 6307.00 @ 1530 ET Jul 11

- SUP 1: 6246.25 Low Jul 7

- SUP 2: 6190.81/6044.35 20- and 50-day EMA values

- SUP 3: 5811.50 Low May 23

- SUP 4: 5645.75 Low May 7

The trend condition in S&P E-Minis remains bullish and short-term weakness is considered corrective. Resistance at 6128.75, the Jun 11 high, has recently been breached. The break confirmed a resumption of the uptrend that started Apr 7. This was followed by a breach of key resistance and a bull trigger at 6277.50, the Feb 21 high. Sights are on 6356.12, a Fibonacci projection. Key support is at the 50-day EMA, at 6044.35.

MNI AMERICAS OIL: WTI crude futures are set for a net gain on the week

July 11 - Americas End-of-Day Oil Summary: WTI crude futures are set for a net gain on the week with support today from signs that Trump is planning to ramp up pressure on Russia. Markets are meanwhile weighing the impact of US tariffs on demand and potential for future increase in OPEC+ output.

- IEA has revised the global oil demand growth forecasts lower for both 2025 and 2026 with the slowest growth this year since 2020, according to the July Oil Market Report.

- President Donald Trump said he planned to make a "major statement" on Russia and expects the Senate to pass a tougher Russia sanctions bill, Bloomberg said. The US has reached an agreement to send more weapons to Ukraine via NATO, he said.

- OPEC+ is discussing a pause in further supply rises from October, delegates told Bloomberg. after a tentative plan to complete the revival of a 2.2mb/d supply in September.

- The Baker Hughes rig count was down the 11th consecutive week, down by two to 537. Oil rigs fell by one to 424, the lowest since September 2021.

- WTI Aug futures were up 2.8% at $68.45

- WTI Sep futures were up 2.5% at $67.03

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 14/07/2025 | 0600/0800 | *** | Final Inflation Report | |

| 14/07/2025 | - | *** | Trade | |

| 14/07/2025 | - | *** | Money Supply | |

| 14/07/2025 | - | *** | New Loans | |

| 14/07/2025 | - | *** | Social Financing | |

| 14/07/2025 | 1230/0830 | ** | Wholesale Trade | |

| 14/07/2025 | 1500/1700 | ECB Cipollone At EU Parliament | ||

| 14/07/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 14/07/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 15/07/2025 | 2301/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 15/07/2025 | 0200/1000 | *** | GDP | |

| 15/07/2025 | 0200/1000 | *** | Fixed-Asset Investment | |

| 15/07/2025 | 0200/1000 | *** | Retail Sales | |

| 15/07/2025 | 0200/1000 | *** | Industrial Output | |

| 15/07/2025 | 0200/1000 | ** | Surveyed Unemployment Rate M/M |