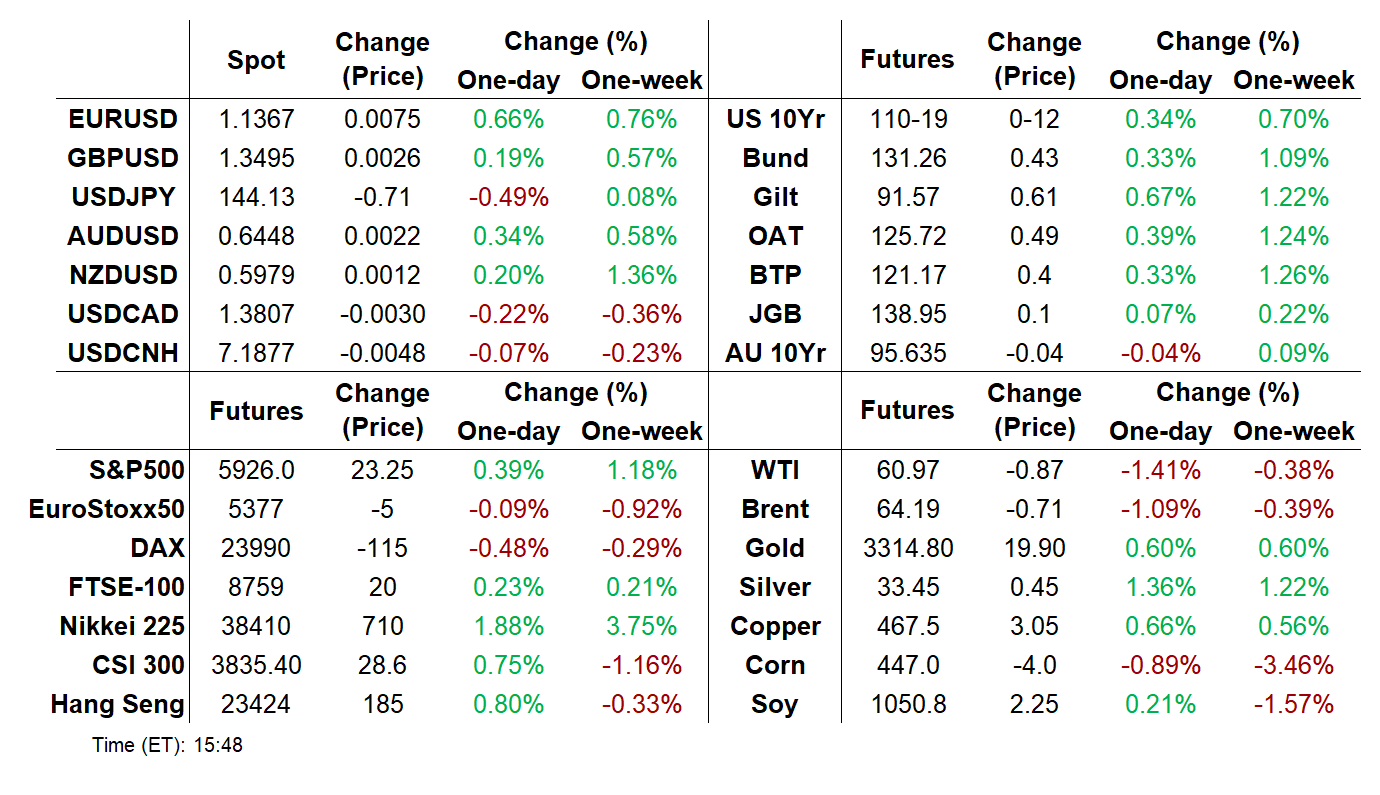

MNI ASIA MARKETS ANALYSIS: Yields And USD Fade Tariff Block

MNI (NEW YORK) -

HIGHLIGHTS:

- Core Bonds Strengthen And Equities Fade Into Month-End Amid Legal Fights Over Trump Tariffs

- US Dollar Reverses Steadily Lower, EURUSD Re-Approaches 1.14

- Friday's Calendar Includes National Euro Inflation And US PCE Data, And MNI Chicago PMI

US TSYS: Belly Outperforms Amid Legal Wrangling Over Tariffs

Treasuries reversed early weakness to finish stronger Thursday, with the belly outperforming on the curve.

- Treasuries were on the back foot early as risk assets gained following late Wednesday's court ruling that blocked implementation of most of the White House's tariffs.

- But the initial reaction faded as markets assessed whether the legal decision would have a lasting effect, and indeed, in late afternoon trade an appeals court allowed the tariffs to remain in effect at least temporarily.

- Equities faded from their highs, with Treasuries getting a boost from soft data in the form of downward revisions to Q1 consumption in GDP, and surprisingly weak jobless claims data. Month-end dynamics may have played a factor as well.

- There was a small but notable downtick in short-end rates after the White House said President Trump told Powell in a private meeting today that the Fed Chair was making a "mistake" by not cutting rates.

- The bond rally extended in the afternoon after the third strong Treasury auction of the week, with 7Y Note seeing the joint-highest trade-through since August 2022 (2.9bp), and record-low primary dealer takedown.

- Partly as a result, the curve belly outperformed on the day (7Y yields dropped 5.8bp). Latest levels: The 2-Yr yield is down 4.7bps at 3.9427%, 5-Yr is down 5.7bps at 4.0052%, 10-Yr is down 4.9bps at 4.4279%, and 30-Yr is down 5.1bps at 4.9244%.

- Sep US 10Y futures (TY) up 12.5/32 at 110-20.5 (L: 109-26 / H: 110-23.5), briefly testing key near-term resistance at 110-23, the May 16 high.

- Friday's calendar is busy data-wise: we get the April PCE report, April trade data, MNI Chicago PMI, and May's final UMichigan consumer survey.

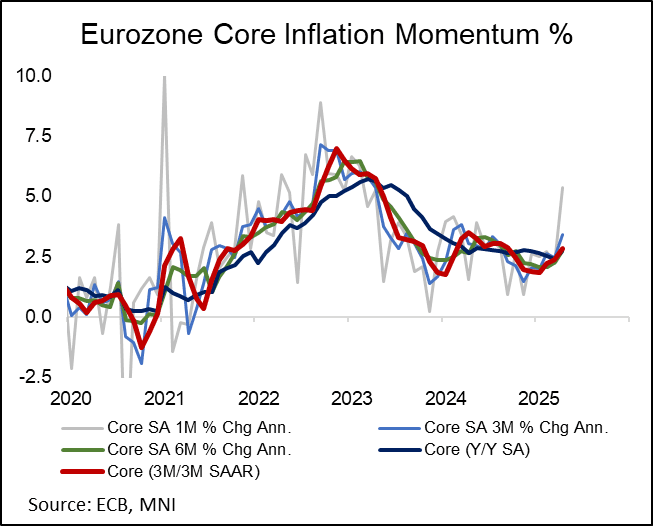

MNI Eurozone May HICP Preview: Unwinding of Easter Effect Key

DOWNLOAD FULL PDF HERE: May2025EZCPIPreview.pdf

- Tariff developments remain the centre of market attention, but the Eurozone May flash inflation round will still be in focus to determine to what extent the April acceleration in services inflation was temporary.

- The details of the April reading pointed to a substantial “Easter effect” for travel-sensitive services such as airfares, and already released French and Belgian data point to an unwind of these dynamics.

- The French data was notably soft, printing at 0.6% Y/Y (vs 0.9% cons and prior), and added downside risks to MNI’s current consensus for the Eurozone, which stands at 2.0% for headline (vs 2.2% prior) and 2.5% for core (vs 2.7% prior).

- In the near-term, the combination of tariff-related downside growth risks and easing wage pressures are expected to weigh on core inflation, but there remains some uncertainty around the medium-term impacts, particularly amongst Governing Council hawks.

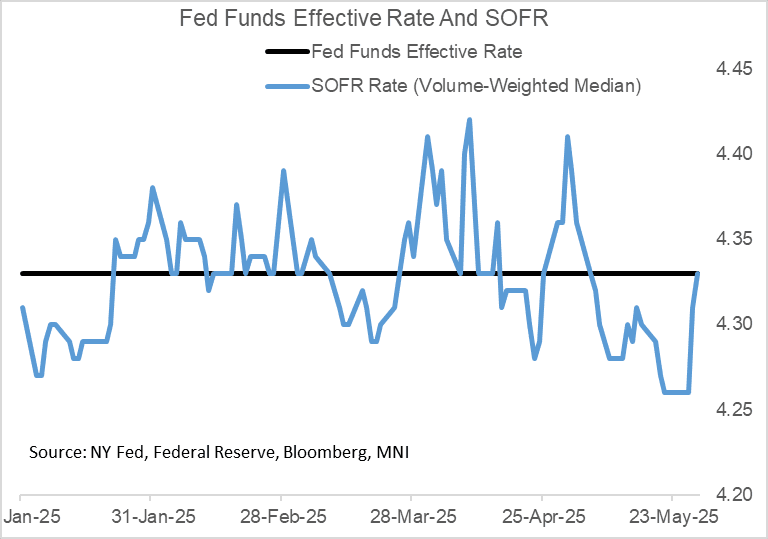

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

US TSYS/OVERNIGHT REPO: Secured Rates Continue To Tick Up With Month-End Ahead

Secured rates rose for a 2nd consecutive session Wednesday, with SOFR up 2bp to 4.33%, adding to the 5bp rise prior.

- That brings SOFR back up to the level of effective Fed funds for the first time since May 5.

- Secured rates rates could be temporarily subdued today by $29B in net Treasury bill paydowns. However, upside pressures are likely to persist toward week-end exacerbated by Friday's month-end dynamics and $46B in Treasury net new cash raised via coupon auction settlements.

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.33%, 0.02%, $2605B

* Broad General Collateral Rate (BGCR): 4.32%, 0.02%, $1049B

* Tri-Party General Collateral Rate (TGCR): 4.32%, 0.02%, $1020B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.33%, no change, volume: $108B

* Daily Overnight Bank Funding Rate: 4.33%, no change, volume: $282B

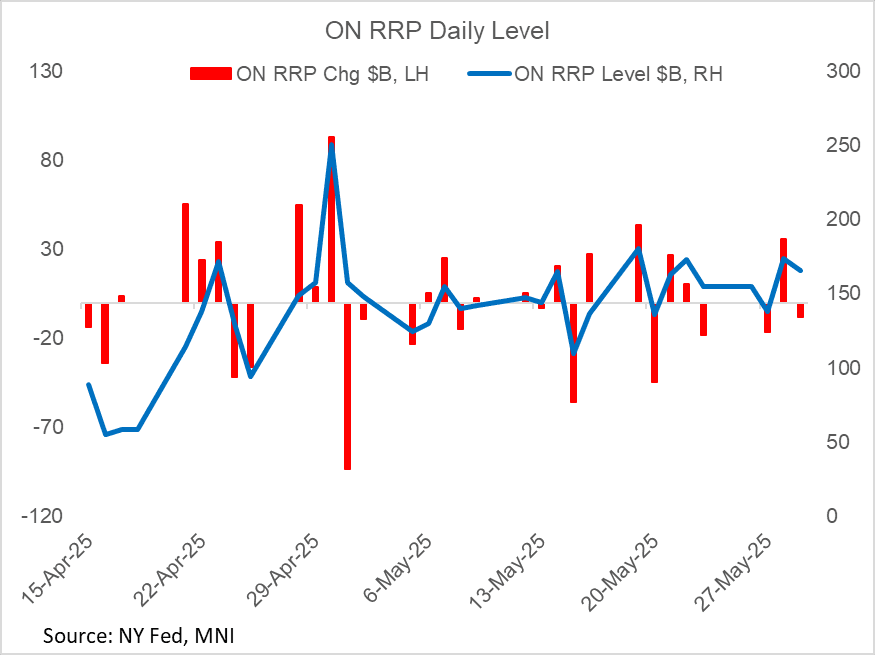

US TSYS/OVERNIGHT REPO: Overnight Reverse Repo Takeup Pared, May Rebound Friday

Overnight reverse repo (ON RRP) takeup dipped $8.0B to $165.7B Thursday. Even so, it remains elevated, with Wednesday's total having been the 2nd highest total of the month.

- As we noted following yesterday's $36B jump, ON RRP takeup isn't expected to rise much more (ie remaining below $200B), with the likely exception of month-end dynamics Friday.

EGBs-GILTS CASH CLOSE: Rallying Into Month-End

European core FI recovered from early weakness to close stronger Thursday.

- Core instruments were under some pressure in an early risk-on move, after a surprise US court decision overnight striking down (at least temporarily) the bulk of the White House's previously-announced tariffs.

- But Bunds and Gilts rallied almost continuously throughout the rest of the session.

- Multiple factors drove the rally: softer-than-expected US GDP and jobless claims data in the early European afternoon; softening equities as the impact of the US tariff court order was reconsidered; and, potentially, month-end dynamics helping boost core instruments led by Treasuries.

- UK yields fell around 8bp across the curve, outperforming bull flattening German instruments.

- Periphery / semi-core EGBs traded mixed but basically flat on the day vs Bunds; OATs outperformed.

- Friday brings flash May inflation data from Spain, Italy and Germany - MNI’s preview is here. We also hear from ECB's Muller, Panetta and Vujcic.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.8bps at 1.769%, 5-Yr is down 3.9bps at 2.068%, 10-Yr is down 4.6bps at 2.508%, and 30-Yr is down 4.4bps at 2.987%.

- UK: The 2-Yr yield is down 8bps at 3.995%, 5-Yr is down 7.8bps at 4.128%, 10-Yr is down 7.9bps at 4.648%, and 30-Yr is down 8.4bps at 5.396%.

- Italian BTP spread unchanged at 98.1bps /French down 0.6bps at 66.7bps

FOREX: US Dollar Reverses Steadily Lower, EURUSD Re-Approaches 1.14

- Following the greenback’s powerful gap higher on the overnight news that the US trade court ruling against Trump’s tariffs, the dollar has since reversed steadily lower across Thursday’s trading session, and the USD index is currently 0.6% lower as we approach the APAC crossover.

- Outperforming in G10 has been the Euro, with EURUSD hugging the day’s highs at typing and re-approaching the 1.14 handle, despite registering earlier lows at 1.1210. On the upside, a break of 1.1419, the May 26 high, would be a bullish development and bolster the underlying trend for the pair.

- EURGBP prices reversed higher Thursday, bouncing sharply off a fresh pullback low. Despite the phase of strength, the cross is still yet to meaningfully challenge the next resistance: the 50-day EMA at 0.8444. Clearance here opens potential for a stronger reversal toward 0.8541.

- USDJPY has been grinding lower, with the reversal lower for major equity benchmarks adding specific weight to the pair. Spot has slipped back below 144.00 in late US trade, having reversed ~230 pips from the APAC highs at 146.28. The initial rally resulted in a breach of the 50-day EMA, at 145.64, however the failure to close above opens scope for near-term weakness. Support to watch is 142.12, the May 27 low. A break would resume the recent bear leg.

- In emerging markets, the South African rand has traded to a fresh 5-month high, as a 25bp rate cut from the SARB was easily shrugged off. SARB Governor Kganyago said a lower inflation target would lead to structurally lower interest rates as the economy recalibrates to a lower-inflation, higher-growth environment. Support is seen at 17.6191, the December low.

- Focus Friday turns to the US Core PCE Report for April. Elsewhere, German & Spanish CPI and Canada GDP are also scheduled.

EUROPE OPTIONS: Some Downside Seen In Bund, Mixed In Euribor Thursday

Thursday's Europe rates/bond options flow included:

- OEN5 119.25/120.25cs, bought for 4 in 3k.

- RXN5 129.50/128.50ps, bought for 15 in 4k.

- ERM5 98.00/98.125 cs bought for 2 in 15k

- ERZ5 98.00/97.9375ps, bought for 1.25 in 3k.

FX OPTIONS: Expiries for May30 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1200-05(E530mln), $1.1250(E914mln), $1.1340-50(E945mln), $1.1475(E648mln)

- USD/JPY: Y140.00($2.8bln) Y143.00($3.4bln)

- AUD/USD: $0.6400-10(A$504mln), $0.6500(A$541mln)

- USD/CAD: C$1.3900($755mln), C$1.4500($1.3bln)

DATA/EVENTS CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 30/05/2025 | 0600/0800 | *** | GDP | |

| 30/05/2025 | 0600/0800 | ** | Import/Export Prices | |

| 30/05/2025 | 0600/0800 | ** | Retail Sales | |

| 30/05/2025 | 0630/0730 | DMO to release FQ2 (Jul-Sep) issuance ops calendar | ||

| 30/05/2025 | 0700/0900 | *** | HICP (p) | |

| 30/05/2025 | 0700/0900 | ** | KOF Economic Barometer | |

| 30/05/2025 | 0800/1000 | ** | M3 | |

| 30/05/2025 | 0800/1000 | *** | GDP (f) | |

| 30/05/2025 | 0800/1000 | *** | Bavaria CPI | |

| 30/05/2025 | 0800/1000 | *** | North Rhine Westphalia CPI | |

| 30/05/2025 | 0800/1000 | *** | Baden Wuerttemberg CPI | |

| 30/05/2025 | 0900/1100 | *** | HICP (p) | |

| 30/05/2025 | 1000/1200 | ** | PPI | |

| 30/05/2025 | 1200/1400 | *** | HICP (p) | |

| 30/05/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 30/05/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 30/05/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 30/05/2025 | 1230/0830 | *** | GDP - Canadian Economic Accounts | |

| 30/05/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 30/05/2025 | 1230/0830 | *** | CA GDP by Industry and GDP Canadian Economic Accounts Combined | |

| 30/05/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 30/05/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 30/05/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 30/05/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 30/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 30/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 30/05/2025 | 2045/1645 | San Francisco Fed's Mary Daly | ||

| 31/05/2025 | 0130/0930 | *** | CFLP Manufacturing PMI | |

| 31/05/2025 | 0130/0930 | ** | CFLP Non-Manufacturing PMI |