MNI ASIA MARKETS ANALYSIS: Will Trade Breakthrough Last

HIGHLIGHTS

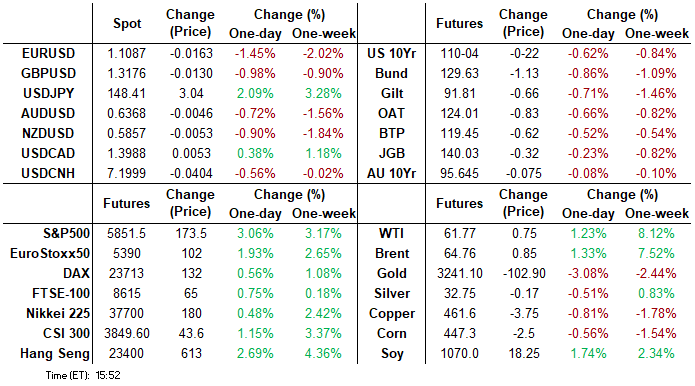

- Treasuries look to finish broadly weaker/off lows US/China agree to a significant reduction in tariffs for 90 days.

- In line with bear curve flattening, projected rate cut pricing retreats from this morning levels (*) as follows: Jun'25 at -2.0bp (-2.8bp), Jul'25 at -10.8bp vs. (-13.1bp), Sep'25 -27.0bp (-29.3bp), Oct'25 -40.3bp (-42.6bp).

- Stocks surged to the highest levels since prior to the "Liberation Day" tariff announcement on April 2.

- The greenback remains the strongest currency in G10 to start the week, following the US and China agreeing to pause their retaliatory reciprocal tariffs.

MNI US TSYS: US/China 90-Day Tariff Pause, Rate Cut Pricing Retreats

- Treasuries gapped lower in early London trade, stocks surged (DJIA +1103 at 42,352) to the pre-Liberation Day levels (April 2) after the US and China agreeing to pause their retaliatory reciprocal tariffs for 90 days.

- After a collective sigh of relief, Treasuries traded sideways, near session lows for much of the session, Jun'25 10Y futures -20.5 at 110-05.5 after the close (110-01.5 low/110-19.5 high) on heavy volumes (TYM>1.880M).

- The next support to watch is 110-01+, a Fibonacci retracement point. Clearance of this level would strengthen a bearish theme and expose a key support at 109-08, the Apr 24 low.

- Curves bear flattening while projected rate cut pricing retreats from this morning levels (*) as follows: Jun'25 at -2.0bp (-2.8bp), Jul'25 at -10.8bp vs. (-13.1bp), Sep'25 -27.0bp (-29.3bp), Oct'25 -40.3bp (-42.6bp).

- Aside from some Fed speakers, tomorrow's focus is on April CPI figures at 0830ET.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.28% (-0.01), volume: $2.479T

- Broad General Collateral Rate (BGCR): 4.27% (-0.01), volume: $1.071T

- Tri-Party General Collateral Rate (TCR): 4.27% (-0.01), volume: $1.035T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $107B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $295B

FED Reverse Repo Operation

RRP usage inches up to $147.505B this afternoon from $142.272B Friday, total number of counterparties at 34. Usage had fallen to $54.772B last Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

Option desks reported heavy option volumes on mixed trade Monday as markets adjust to US/China 90 day tariff reduction headlines (kicked off around 0300ET). Curves bear flattening while projected rate cut pricing retreats from this morning levels (*) as follows: Jun'25 at -2.0bp (-2.8bp), Jul'25 at -10.8bp vs. (-13.1bp), Sep'25 -27.0bp (-29.3bp), Oct'25 -40.3bp (-42.6bp).

SOFR Options:

-20,000 SFRZ5 96.75/97.25 call spds

+15,000 0QK5 96.25 puts, 0.5 ref 96.55

+6,000 0QK5 96.81/96.87/96.93/97.00 call condors, 0.25 ref 96.53

+5,000 SFRU5 95.68/95.81/96.00 2x3x1 put flys, 0.25 ref 95.97

+5,000 SFRU5 95.68/95.75 put spds, 8.75 ref 95.97

2,500 SFRV5 96.25/96.50/96.75/97.00 call condors ref 96.235

Block, 4,000 SFRK5 95.75/95.81 call spds, 0.50 ref 95.715

Block, 3,000 0QM5 97.00/97.37 call spds, 2.0 ref 96.53

2,500 SFRZ5 95.75/95.87 put spds vs. 96.37/96.50 call spds ref 96.22

20,000 0QU5 97.25/97.75 call spds ref 96.555

4,000 SFRM5 95.62/95.68 put spds ref 95.71

1,500 2QK5 96.00/96.25 2x3 put spds

2,500 0QM5 96.56/97.06/97.56 call flys ref 96.495

4,000 SFRZ5 96.75/97.00/97.50/97.75 call condors ref 96.21 to -.205

2,500 0QU5 95.50/95.75/96.00/96.12 broken put condors ref 95.57

Block, 3,000 0QM5 96.25 puts, 4.5 ref 96.51

over 14,000 SFRU5 96.25/96.75 call spds ref 95.975

4,000 SFRZ5 95.68/95.81 put spds ref 96.215

Block 3,000 SFRM5 95.75/95.87 2x1 put spds ref 95.715

Over 18,750 SFRK5 95.75 puts, 4.0 last ref 95.71

3,000 0QN5 97.12/97.37 call spds ref 96.595

13,000 SFRZ5 97.00/98.00 call spds, 8.0 ref 96.22

Block/screen, 11,000 SFRQ5 95.75/95.81/95.87/95.93 put condors, 1.25 ref 95.985 to -.98

2,000 SFRQ5 96.50/96.75 vs. SFRZ5 97.00/97.50 call spd spd

3,000 SFRM5 95.68/95.81 put spds ref 95.71

2,000 SFRK5 95.75/95.87 2x1 put spds ref 95.71

1,500 SFRU5 96.00/96.12/96.25/96.37 call condors, ref 95.98

1,500 SFRH6 97.50/97.75/98.00/98.25 call condors ref 96.425

1,500 SFRK5 95.50/95.62/95.75 put flys ref 95.715

2,000 SFRM5 95.68/95.75 put spds ref 95.715

Treasury Options:

4,700 USN5 109/112 put spds, 44 ref 113-13

2,500 FVM5 107/107.75 put spds, 19ref 107-21.5

3,500 TYM5 110.5 puts, 47

over 5,000 FVM5 107.25 puts, 14 last

over 3,500 FVM5 107.5/109 strangles, 25 ref

5,600 TYM5 110.75/112 call spds ref 110-03.5

over 8,500 wk5 FV 109/110 call spds ref 107-21 to -20.5

over 13,000 Wed wkly TY 109.5/109.75 put spds ref 110-08.5 to -06.5

3,000 Wed wkly TY 110.75 puts, 26 ref 110-09

4,100 FVM5 107.5/109 strangles ref 107-20.5

over 12,200 TYN5 109 puts, 24-27 ref 110-13

MNI BONDS: EGBs-GILTS CASH CLOSE: Bear Flattening On Sino-US Trade Truce

European curves bear flattened Monday, with periphery / semi-core EGBs outperforming.

- A tentative trade war truce between China and the US saw Bund and Gilt yields gap higher at the start-of-week reopen as equities soared in relief.

- Bear steepening was the order of the day, as ECB/BOE rate cuts were priced out, pressuring the short end.

- Elsewhere, headlines from the BOE Watchers' conference were prevalent following last week's 3-way split (ultimately 5-4 in favour of a 25bp cut).

- Lombardelli called the decision to cut 25bp "finely balanced"; Greene said she would still have voted for a 25bp cut if she knew about the US and UK/China trade developments; Taylor, who had voted for a 50bp cut, noted that he could reconsider support for lower rates if "there was a surprising amount of progress on the international trade war situation".

- Bunds underperformed Gilts. Periphery / semi-core spreads narrowed by around 2bp across the board.

- Tuesday's agenda includes UK labour market data - MNI's preview is here. We also get US CPI data.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 12.8bps at 1.913%, 5-Yr is up 12.3bps at 2.222%, 10-Yr is up 8.6bps at 2.648%, and 30-Yr is up 6.2bps at 3.081%.

- UK: The 2-Yr yield is up 9.2bps at 4%, 5-Yr is up 9.9bps at 4.126%, 10-Yr is up 7.6bps at 4.643%, and 30-Yr is up 4.5bps at 5.391%.

- Italian BTP spread down 1.8bps at 102.9bps / French OAT down 2.3bps at 68.1bps

MNI OPTIONS: Busy Euribor Trade Includes Continued Call Condor Closeout

Monday's Europe rates/bond options flow included:

- RXN5 133.50c, bought for 14.5 in 4k

- ERM5 97.875/98.00/98.125/98.25 call condor, sold out at 7.25 in 8k (continuing closing out from prior sessions)

- ERU5 98.125/98.1875/98.3125/98.375 condor vs 97.9375/97.8125 put spread, paper sells for 0.25 in 9k (sells the condor)

- ERU5 98.50/98.37/98.25/98.00p condor sold at -1.75 and -2 (receive) in 16.5k

- ERZ5 98.50/98.25ps 1x2 bought the 1 for 1 in 20k

- ERH6 99.12/99.37cs, bought for 1.25 in 10k

MNI FOREX: USD Consolidates Impressive Advance Following US/China Tariff Reprieve

- Despite a less volatile US session, the greenback remains the strongest currency in G10 to start the week, following the US and China agreeing to pause their retaliatory reciprocal tariffs that had been the cause of much trepidation in global financial markets. The news has helped the ICE USD index extend its recovery, rising an impressive 1.35% on the session, while EURUSD slips back below 1.11 to fresh one-month lows for the pair.

- The Japanese Yen is the poorest performing currency amid the significant boost to risk sentiment across global equity markets and the hawkish repricing in core fixed income providing an additional headwind for the low yielders.

- USDJPY is currently up 2.05% as we approach the APAC crossover, exacerbated by a clean break of 50-day EMA resistance that had capped the price action last week. Earlier highs were registered at 148.59, breaching a short-term pivot point at 148.18, which provided the initial resistance point on the chart. Further strength would place the focus on the daily highs from around the ‘liberation day’ announcement at 149.28 and 150.49.

- In similar vein, USDCHF has risen 1.5%, marginally outperforming the DXY. Topside momentum has been underpinned by a break back above the key 0.8333 level, the 2023 low and prior breakdown point. The move substantially narrowed the gap to an important resistance for USDCHF, which stands at 0.8485, the 50-day EMA. A break of this average would signal scope for a recovery towards 0.8578, the April 10 high, while the ‘liberation day’ breakdown level remains much further out at 0.8758.

- Higher beta pairs have relatively outperformed given the risk backdrop, with the Canadian dollar the least impacted on Monday. In similar vein, Latin American currencies and the South African rand have had only moderate adjustments given the ties to China optimism are offsetting the broader rally for the greenback.

- All focus turns to Tuesday’s US CPI report on Tuesday. Labour market data from the UK and German ZEW figures are scheduled during the European morning.

MNI OPTIONS: Expiries for May13 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1145-50(E1.0bln), $1.1290-00(E727mln), $1.1325(E600mln), $1.1355-60(E1.1bln), $1.1370-75(E1.8bln), $1.1415-20(E1.3bln), $1.1450(E1.1bln)

- USD/JPY: Y143.00($1.5bln), Y146.75(E567mln), Y151.00($1.2bln)

- GBP/USD: $1.3200(Gbp599mln)

- EUR/GBP: Gbp0.8695(E580mln)

- AUD/USD: $0.6545(A$811mln)

- USD/CAD: C$1.3875-85($1.2bln)

- USD/CNY: Cny7.2500($519mln)

MNI US STOCKS: Late Equities Roundup: IT, Consumer Stocks Outperforming

- Stocks remain well bid in late Monday trade - highest levels since prior to the "Liberation Day" tariff announcement on April 2. Stocks surged higher around 0300ET Monday morning after wires reported sweeping 90-day US/China tariff reductions stemming from negotiations in Switzerland over the weekend.

- Currently, the DJIA trades up 1099.95 points (2.67%) at 42351.12, S&P E-Minis up 174 points (3.06%) at 5852.75, Nasdaq up 741.2 points (4.1%) at 18670.52.

- Information Technology and Consumer Discretionary sectors continued to outperform in late trade, chip makers underpinning the Tech sector with Zebra Technologies +12.21%, Monolithic Power +12.07%, Microchip Technology +11.71%, ON Semiconductor +9.88%, Lam Research +9.29% and Applied Materials +8.60%.

- Broadline retailers, clothing and auto related stocks supported the Discretionary sector with Williams-Sonoma +8.57%, Amazon.com +7.96% and Best Buy +5.71%; Lululemon Athletica +7.77%, NIKE +6.81%; Tesla +6.41%, Aptiv +7.68%

- Consumer Staples and Utilities continued to underperform in late trade, food & tobacco shares weighed on the former: Altria Group -3.55%, Philip Morris -2.58%, Hershey -2.12% and Coca-Cola -1.87%. Meanwhile, gas providers weighed on the Utility sector: Alliant Energy -3.51%, Exelon -3.47%, Consolidated Edison -3.30%, Xcel Energy -3.24% and Duke Energy -3.15%.

MNI EQUITY TECHS: E-MINI S&P: (M5) Northbound

- RES 4: 6000.00 Round number resistance

- RES 3: 5938.25 High Mar 4

- RES 2: 5896.25 76.4% retracement of the Feb 19 - Apr 7 bear leg

- RES 1: 5865.75 Intraday high

- PRICE: 5855.00 @ 1505 ET May 12

- SUP 1: 5628.71/ 5571.80 50- and 20-day EMA values

- SUP 2: 5455.50 Low Apr 30

- SUP 3: 5355.25 Low Apr 24

- SUP 4: 5127.25 Low Apr 21 and a key support

A bullish trend condition in S&P E-Minis remains intact and today’s strong start to this week’s session reinforces bullish conditions. The contract has pierced an important resistance at 5837.25, the Mar 25 high and a bull trigger. This strengthens the current bullish theme, paving the way for a continuation near-term. Sights are on 5896.25, a Fibonacci retracement. Initial firm support to watch lies at 5628.71, the 50-day EMA.

COMMODITIES

MNI AMERICAS OIL: WTI crude has risen back to late-April levels

May 12 - Americas End-of-Day Oil Summary: WTI crude has risen back to late-April levels amid lower US-China tariffs after negotiations this weekend.

- The US and China released a joint statement agreeing to lower tariffs for 90 days.145% US levies on China will be reduced to 30%, while 125% Chinese tariffs on US goods will drop to 10%.

- US-China tariff cuts likely to revive some trade between the US and China, and support China’s oil demand, Platts reports.

- The US and Iran talks this weekend were “encouraging” and “difficult but useful.” Further talks on Iran’s nuclear program were agreed and likely to meet again in a week.

- Ukraine's Volodymyr Zelenskiy is set to meet with Vladimir Putin in Istanbul on May 15 for direct negotiations.

- WTI June futures were up 1.6% at $61.95

- WTI July futures were up 1.6% at $61.57

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 13/05/2025 | 0600/0700 | *** | Labour Market Survey | |

| 13/05/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 13/05/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 13/05/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 13/05/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 13/05/2025 | - | *** | Money Supply | |

| 13/05/2025 | - | *** | New Loans | |

| 13/05/2025 | - | *** | Social Financing | |

| 13/05/2025 | - | ECB's De Guindos At ECOFIN Meeting | ||

| 13/05/2025 | 1230/0830 | *** | CPI | |

| 13/05/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 13/05/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 14/05/2025 | 0130/1130 | *** | Quarterly wage price index |