MNI ASIA MARKETS ANALYSIS: Volatile Session, Mixed Labor Data

HIGHLIGHTS

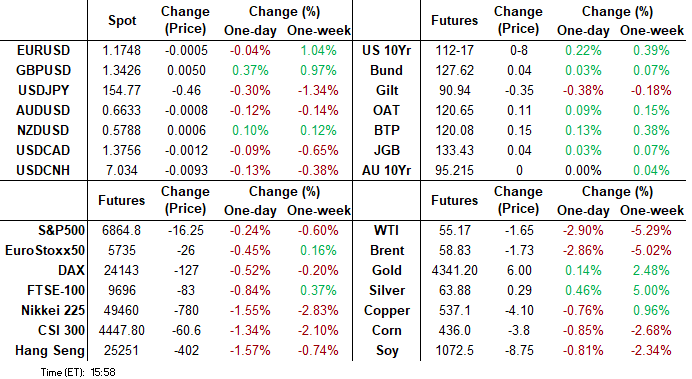

- Treasuries look to finish moderately higher, off post data highs as focus turned away from the 4.6% unemployment rate with possible assistance from that heavy -105k in Oct NFP.

- Rounding and already known higher survey error saw Treasuries extended lows soon after, 10Y yield rising to 4.1939% high while the 2s10s curve climbed to new/near 4Y high of 69.086 - only to retreat to 66.624 after the bell.

- Retail sales growth was flat in October after rising 0.1% prior, a little softer than the expected 0.1% gain - but core sales were significantly stronger than expected, implying strong retail momentum at the start of Q4.

- US dollar index pullback to 97.87, the lowest level since October 03. However, the slightly messy release and associated uncertainty surrounding DOGE deferred resignations saw the Greenback rebound to 98.15.

US TSYS

MNI US TSYS: Back Near Highs After Rejecting Post-NFP Gap Bid

- Treasuries look to finish moderately higher, off post data highs as focus turned away from this morning's 4.6% unemployment rate with possible assistance from that heavy -105k in Oct NFP.

- Rounding and already known higher survey error saw Treasuries extend lows soon after, 10Y yield rising to 4.1939% high while the 2s10s curve climbed to new/near 4Y high of 69.086 - only to retreat to 66.624 after the bell.

- Retail sales growth was flat in October after rising 0.1% prior, a little softer than the expected 0.1% gain - core sales were significantly stronger than expected, implying strong retail momentum at the start of Q4.

- TYH6 currently trades 112-17 (+8) vs. 112-06 low / 112-22.5 high. Curves mildly flatter: 2s10s -.045 at 66.624 after climbing to new - near 4Y high of 69.086 this morning.

- US dollar index pullback to 97.87, the lowest level since October 03. However, the slightly messy release and associated uncertainty surrounding DOGE deferred resignations saw the Greenback rebound to 98.15.

- No Fed speakers during the session, Chicago Fed Pre Goolsbee will appear on CNN at 1600ET. Focus on Wednesday: several regional Fed economic measures, Fed speakers (Waller, Williams, Bostic) and $13B 20Y Bond re-open (912810UQ9).

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.75% (+0.08), volume: $3.270T

- Broad General Collateral Rate (BGCR): 3.73% (+0.08), volume: $1.315T

- Tri-Party General Collateral Rate (TCR): 3.73% (+0.08), volume: $1.288T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $97B

- Daily Overnight Bank Funding Rate: 3.64% (+0.00), volume: $167B

FED Reverse Repo Operation:

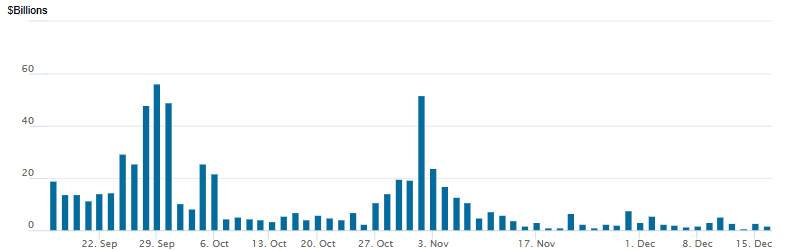

RRP usage recedes to $1.554B with counterparties falling to 2 this afternoon, vs. Monday's $2.601B. Compares to last Thursday's $0.838B (lowest level since mid-March 2021); this years highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury option flow continued to revolve around downside put trade Wednesday. Projected rate cut pricing gains some momentum vs. early morning levels (*): Jan'26 steady at -6.1bp, Mar'26 at -15.2bp (-14.3bp), Apr'26 at -21.6bp (-20.8bp), Jun'26 at -36.1bp (-34.2bp).

SOFR Options:

Block, 5,000 SFRH6 96.37/96.43/96.50/96.68 broken call condors, 1.0 net

-6,000 SFRM6 96.31/96.56/96.81 put flys, 8.0

Block, +10,000 SFRZ6 97.00/98.00 call spds, 17.0 vs. 96.88/0.32%

-8,500 0QZ6 96.62/96.75 put spds, 0.5 ref 96.75

-2,000 SFRF6 96.56/96.68 call spds, 1.75 ref 96.48

-5,000 SFRH6 96.75/96.87 call spds, 1.0 ref 96.505

+3,000 SFRG6 96.50/96.62/96.75 call flys, 2.25

+2,500 SFRH6 96.25/96.31/6.37/96.43 1x1x2x2 put condor 3.0 vs. 96.48

-3,000 SFRH6 96.50/96.62 call spds 3.25 vs. 96.68/0.17%

4,500 SFRH6 96.56/96.68 call spds ref 96.47

+2,000 SFRH6 96.37 puts, 3.75 vs. 96.46/0.30%

+4,200 SFRF6 96.25/96.43/96.50 broken put flys, 0.25 ref 96.47

+2,000 SFRG6 96.50/96.62 call spds, 3.0 ref 96.47

+4,000 SFRF6 96.37 puts, 1.25

+6,000 SFRU 96.37/96.81 2x3 put spds, 3.0-3.25 ref 96.835 to -.83

1,800 SFRF6 96.50 puts vs. 96.50/96.62 call spds ref 96.48

2,690 SFRU6 96.37/96.81/97.25 2x3x1 put flys ref 96.84

Treasury Options:

+67,185 USF6 108 puts at cab-7 ***

1,250 FVG6 108.75/109.25 5x4 put spd

1,800 TYG6 112/113 strangles, 50 ref 112-16

10,000 FVF6 109.5 calls, 7.5

4,000 TYG6 111/112 2x1 put spds, 7 net ref 112-11.5

Block, +28,000 TYH6 110 puts, 11 vs. -15,000 TYG6 111 puts, 9

+20,000 TYH6 110.5 puts, 15 ref 112-16.5

5,000 TYF6 113/113.5 1x2 call spds ref 112-11

6,000 TYG6 111/112/113 2x3x1 put flys ref 112-12.5

+12,000 Weds Wkly 10Y 112 puts, 6-7

-8,000 TYG6/TYH6 112.5 straddle spd, 33 vs. 112-09.5

over 6,400 TYF6 113 calls, 9-10

7,000 TUH6 103.5/104/104.12/104.37 broken put condors, 2.5 vs. 104-09.75/0.04%

+1,200 USF6 116.5 puts, 150 ref 114-30

-3,000 TYF6 112.75 calls, 14-15 ref 112-12 to -13 /0.34%

+2,000 TYF6 111.25 puts, 4

+2,100 TYG6 111.5 puts, 21

-1,065 FVG6 108/109 put spds, 16.5 ref 109-08/0.27%

Expire today:

over 19,000 Tue Wkly 10Y 112 puts ref 112-12.5

over 15,000 Tue Wkly 1112.25 puts, 10-11

MNI US TSY OPTIONS: Patently Absurd Low-Delta 30Y Puts Trading Again

- *** +67,185 USF6 108 puts at cab-7, new position with open interest of 4,024 coming into the session. The Mar'26 options expire in 10 days - the Friday after Christmas.

- Precedent: On Wednesday, December 3: paper bought 84,361 wk2 30Y 106 puts trade on screen at cab-7

- The 10 handle out-of-the-money option expired last Friday, December 12 - after the FOMC's widely anticipated third consecutive 25bp rate cut last Wednesday.

- Most likely a hedge vs some short term balance sheet risk that corresponded to a rise in 30Y yield to (rough) appr 5.48% from 4.73% yield at the time of trade.

MNI EGB BONDS: EGBs-GILTS CASH CLOSE: Gilts Underperform On UK PMIs, Wage Growth

EGB yields dipped Tuesday amid mixed global labor market and activity data, but Gilts weakened.

- Slightly weaker-than-expected Eurozone December flash PMIs had little impact on core EGBs. In the UK however Gilts were kept on the back foot amid a firm PMI print and labour market data that showed higher-than-expected earnings growth.

- The delayed US nonfarm payrolls report was initially seen as weak due to a sizeable unemployment rate rise, but the move fully reversed in part due to strong US retail sales alongside, and saw Gilts and Bunds yields hit session highs.

- Yields were content to come off of the lows into the cash close, ahead of Wednesday's UK CPI release and Thursday's ECB / BoE decisions.

- On the day, the German curve bull steepened slightly, with the UK's bear steepening. Periphery/semi-core EGB spreads fell modestly.

- Aside from UK CPI (MNI's preview here), German IFO and Eurozone final November inflation data feature Wednesday.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.6bps at 2.134%, 5-Yr is down 1.7bps at 2.452%, 10-Yr is down 0.8bps at 2.845%, and 30-Yr is down 0.6bps at 3.466%.

- UK: The 2-Yr yield is up 1.2bps at 3.766%, 5-Yr is up 1.3bps at 3.96%, 10-Yr is up 2.2bps at 4.518%, and 30-Yr is up 1.9bps at 5.258%.

- Spanish bond spread down 1.2bps at 43.6bps / French OAT down 0.4bps at 70.5bps

MNI EGB OPTIONS: Limited Trade Includes Sonia Upside Buying Between Key UK Data Points

Tuesday's Europe rates/bond options flow included:

- RXG6 126.50/124.50ps, bought for 27.5 in 6k

- ERM6 97.87/97.81ps vs 98.00/98.06cs, bought the ps for flat in 7.5k

- SFIZ6 96.90/97.00cs vs 96.30/96.20ps, bought the cs for half in 3k

MNI FOREX: Dollar Index Ending Volatile Session Lower, GBP Outperforms

- The long-awaited release of the latest US employment report painted a mixed picture of the US labour market, prompting a volatile session for the US dollar. Despite the higher-than-expected headline NFP change of +64k, the -105k adjustment in October certainly dampened the release, while the above consensus unemployment rate at 4.564% contributed to an immediate extension lower for the US dollar.

- This resulted in the dollar index printing fresh pullback lows at 97.87, the lowest level since October 03. However, the slightly messy release and associated uncertainty surrounding DOGE deferred resignations made the initial greenback pessimism short-lived. Indeed, with the heavy central bank calendar ahead and US inflation data due Thursday, momentum quickly stalled and two-way price action within a relatively contained range persisted across the US session.

- With that said, the DXY is holding 0.3% declines on the session as we approach the APAC crossover and GBP has maintained its position at the top of the G10 leaderboard, rising 0.45% to 1.3435.

- Price action was assisted by a strong set of labour market figures in the UK, with firmer-than-expected wage data denting prospects of easy policy through 2026. Cable bridged the gap to 1.3452, the 61.8% retracement of the Sep 17 - Nov 4 bear leg, and clearance of this hurdle would strengthen a bull theme and open 1.3527, the Oct 1 high. UK inflation data is scheduled tomorrow before Thursday’s BOE decision.

- USDJPY has also tracked lower, initially dented overnight by souring equity sentiment across the APAC session, and the overall adjustment lower for US yields confirming the negative bias for the pair. Lows today came within 5 pips of the December 05 low at 154.35, and also narrow the gap to the key 50-day EMA located just above the 154 handle. A clear breach of this average would undermine the bull theme and signal scope for a deeper retracement.

- Elsewhere, EURUSD had a very brief test above 1.1800 before settling closer to 1.1775. US inflation and the ECB decision/press conference will keep the pair in focus as the week progresses. Above here, 1.1848 is a notable chart point, the Sep 18 high.

MNI OPTIONS: Expiries for Dec17 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1700(E1.3bln), $1.1750(E1.5bln), $1.1800(E1.6bln), $1.1850(E624mln)

- USD/JPY: Y154.75($594mln)

- AUD/USD: $0.6590(A$680mln), $0.6650-60(A$875mln)

EQUITIES

MNI US STOCKS: Late Equities Roundup: Nasdaq Leading Soft late Day Recovery

- Stocks held narrowly mixed to weaker late Tuesday, cautiously drifting off second half lows along with Treasuries, Nasdaq outperforming. Stock indexes had reversed early gains to weaker following this morning's data that did little to shift rate guidance expectations after last week's third consecutive 25bp cut.

- Currently, the DJIA trades down 329.66 points (-0.68%) at 48079.6, S&P E-Mini Futures down 29.5 points (-0.43%) at 6851, Nasdaq up 12.6 points (0.1%) at 23068.28.

- Energy, Health Care and Financials sector shares led declines in late trade, oil and gas shares weighing on the former with crude prices broadly lower (WTI currently -1.48 to 55.34, oversupply cited):

- Phillips 66 -5.84%, APA Corp -5.60%, Marathon Petroleum -5.06%, Halliburton -4.33%, Baker Hughes -4.24% and Coterra Energy -3.90%.

- Humana -5.74%, Pfizer -4.60%, Centene Corp -4.46%, Molina Healthcare -3.32% and Bio-Techne Corp -3.22%.

- Progressive Corp -2.09%, Bank of New York Mellon -2.03%, Aflac -1.93%, Brown & Brown -1.92% and Fiserv -1.91%.

- On the positive side, a mix of Consumer Discretionary/Staples and Technology sector shares continued to lead advances in late trade: Comcast Corp +4.93%, Estee Lauder Cos +3.23%, United Airlines Holdings +3.18%, Sandisk Corp +2.78%, Dell Technologies +2.31%, Zoetis +2.29% and Vistra Corp +2.23%.

MNI EQUITY TECHS: E-MINI S&P: (H6) Corrective Pullback

- RES 4: 7100.00 Round number support

- RES 3: 7048.21 2.0% Upper Bollinger Band

- RES 2: 7014.00 High Oct 30 and the bull trigger

- RES 1: 6932.25/6988.00 High Dec 15 / 12

- PRICE: 6864.50 @ 14:28 GMT Dec 16

- SUP 1: 6830.94 50-day EMA

- SUP 2: 6785.50 50.0% retracement of the Nov 21 - Dec 11 rally

- SUP 3: 6737.71 61.8% retracement of the Nov 21 - Dec 11 rally

- SUP 4: 6684.50 Low Nov 24

A bull cycle in S&P E-Minis remains intact and the latest pullback - for now - is considered corrective. Initial support to watch is 6830.94, the 50-day EMA. A clear break of this average would signal scope for a deeper retracement. Note that the key support and reversal trigger lies at 6583.00, the Nov 21 low. For bulls, a resumption of gains would refocus attention on the key resistance and bull trigger at 7014.00, the Oct 30 high.

MNI COMMODITIES: Crude Extends Losses Amid Oversupply Concerns, Gold Steady

- Crude is extending a recent bearish theme, with WTI briefly sinking below $55 for the first time since Feb 2021, as oversupply concerns remain in focus and the market assesses some positive signs in Ukraine peace talks.

- WTI Jan 26 is down by 2.7% at $55.3/bbl.

- President Trump said a deal to end Russia's war in Ukraine is closer than ever after talks as US negotiators offered more significant security guarantees to Kyiv.

- For WTI futures, moving average studies are in a bear-mode position, highlighting a dominant downtrend.

- A key support and the bear trigger at $55.99, the Oct 20 low, has been breached. Clearance of this level resumes the downtrend and opens $53.53.

- Elsewhere, spot gold is little changed on Tuesday, as the long-awaited US employment report painted a mixed picture of the US labour market, prompting a volatile session for the US dollar.

- Spot gold is currently 0.2% higher on the session at $4,312/oz, just below recent two-month highs.

- A bullish theme in gold remains intact, with attention on key resistance and the bull trigger at $4,381.5, the Oct 20 high, followed by $4,400 round number resistance.

- Meanwhile, copper has fallen by 0.9% to $537/lb today, leaving it 3% below last week’s highs.

- Copper futures remain in a corrective consolidation mode. However, resistance at $550 has been pierced and a clear break would open $588.70 next, the Jul 30 high.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 17/12/2025 | 0700/0700 | *** | Consumer Inflation Report (1dp) | |

| 17/12/2025 | 0700/0700 | *** | Producer Prices | |

| 17/12/2025 | 0700/1500 | ** | MNI China Money Market Index (MMI) | |

| 17/12/2025 | 0700/0700 | *** | Consumer Inflation Report (2dp) | |

| 17/12/2025 | 0900/1000 | *** | IFO Business Climate Index | |

| 17/12/2025 | 1000/1100 | *** | EZ HICP Final | |

| 17/12/2025 | 1000/1100 | *** | EZ HICP Final | |

| 17/12/2025 | 1000/1100 | *** | EZ HICP Final | |

| 17/12/2025 | 1000/1100 | *** | EZ HICP Final (2dp) | |

| 17/12/2025 | 1100/1100 | ** | CBI Industrial Trends | |

| 17/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 17/12/2025 | 1315/0815 | Fed Governor Christopher Waller | ||

| 17/12/2025 | 1330/0830 | * | International Canadian Transaction in Securities | |

| 17/12/2025 | 1405/0905 | New York Fed's John Williams | ||

| 17/12/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 17/12/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 17/12/2025 | 1730/1230 | Atlanta Fed's Raphael Bostic | ||

| 17/12/2025 | 1800/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 18/12/2025 | 2145/1045 | *** | GDP | |

| 18/12/2025 | - | European Central Bank Meeting | ||

| 18/12/2025 | - | NorgesBank Meeting | ||

| 18/12/2025 | - | Bank of Japan Meeting | ||

| 18/12/2025 | - | Riksbank Meeting |