MNI ASIA MARKETS ANALYSIS: USD Holds Early Drop

MNI (NEW YORK) -

HIGHLIGHTS:

- Cross-US asset weakness highlighted by USD maintaining early drop

- Treasury curve lightly bear steepens as ISM Manufacturing data flags stagflationary risks

- Upcoming event risk includes RBA minutes, Swiss and Eurozone inflation data, and US JOLTS job openings

US TSYS: Light Bear Steepening To Start The Week

Treasuries gave back some of Friday's month end gains on Monday, with the cash curve lightly bear steepening.

- Yields ticked up at the open from Friday's multi-week lows, with a prevailing negative tone on US assets (weaker USD and equities) following Friday's post-close announcement by President Trump that the administration would double steel and aluminum tariffs.

- Most of the session's data was on the soft side of expectations if somewhat stagflationary, with May's ISM manufacturing below-expected (with weak sub-components, albeit prices paid in-line), and construction spending contracting again in April.

- But reaction was muted and yields would head to session highs and stay there after Atlanta Fed GDPNow for Q2 was upgraded to 4.6% (from 3.8%) and equities turned positive into the cash close. Fed speakers (Logan, Goolsbee, Powell) likewise saw no discernable reaction.

- Yields were set to close near the highs: the 2-Yr yield is up 4.3bps at 3.9407%, 5-Yr is up 5.4bps at 4.0156%, 10-Yr is up 5.9bps at 4.4596%, and 30-Yr is up 6.3bps at 4.9935%.

- Sep 10-Yr futures (TY) are down 8.5/32 at 110-15.5 (L: 110-13.5 / H: 110-30), having fallen just through Friday's lows in orderly fashion.

- Tuesday's calendar includes factory orders and JOLTS data, with an appearance by Fed's Cook among other speakers, while the week's focus is Friday's employment report for May.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

US TSYS/OVERNIGHT REPO: SOFR Ticks Up, Month-End Pressures To Spill Over Monday

Secured rates picked up again Friday, with SOFR up 2bp to 4.35%. That's the highest since the start of the month, with the rise at both ends of May reflecting month-end dynamics. Upside pressure is expected to persist Monday before subsiding over the rest of the week.

- Fed funds were unchanged as usual.

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.35%, 0.02%, $2641B

* Broad General Collateral Rate (BGCR): 4.34%, 0.02%, $1049B

* Tri-Party General Collateral Rate (TGCR): 4.34%, 0.02%, $1013Bd

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.33%, no change, volume: $105B

* Daily Overnight Bank Funding Rate: 4.33%, no change, volume: $228B

US TSYS/OVERNIGHT REPO: Reverse Repo Takeup More Than Reverses Month-End Jump

Overnight reverse repo takeup fell $180B Monday, the biggest drop since the start of the year ($233B on Jan 2) and more than reversing Friday's $150B jump.

- The latest level of $135.8B represents an 11-session low.

- A sharp drop-off in takeup was expected due to month-end dynamics reversing. Indeed the latest level is within the roughly $125-175B range seen in most of late April through the start of last week.

BONDS: EGBs-GILTS CASH CLOSE: Light Bear Steepening To Open Week

European curves lightly bear steepened to open the week.

- Core FI opened the week on the back foot, hitting the session's highs in mid-morning trade as weekend news was digested including Ukranian attacks on Russian military equipment and the US's announcement that it would raise tariffs on aluminium and steel to 50%.

- Also adding to the early bearish tone were EU bond suppply and Spanish manufacturing PMI coming in above expected.

- But yields would pare their rises over most of the rest of the session, as equities stabilized and US desks came in.

- In futures, rolling activity was heavy, with most Eurex contracts now around 40% through the Jun/Sep roll.

- Gilts mildly outperformed Bunds; periphery/semi-core EGB spreads traded mixed, closing off the early session wides.

- Tuesday brings Eurozone flash inflation and BOE appearances at the Parliamentary Treasury Committee, with the week's focus remaining on Thursday's ECB decision.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.3bps at 1.789%, 5-Yr is up 1.9bps at 2.083%, 10-Yr is up 2.4bps at 2.524%, and 30-Yr is up 3.2bps at 3.012%.

- UK: The 2-Yr yield is up 0.6bps at 4.029%, 5-Yr is up 1.9bps at 4.163%, 10-Yr is up 2bps at 4.667%, and 30-Yr is up 3.8bps at 5.41%.

- Italian BTP spread down 0.4bps at 97.6bps / French OAT unchanged at 66.4bps

OPTIONS: German Package, Sonia Condors Monday

Monday's Europe rates/bond options flow included:

- Bond Futures Package:

- DUU5 107.30p, sold at 21.5 in 6.75k

- DUU5 107.20p, sold at 17.5 in 6.75k.

- UBU5 119.00p, sold at 280 in 500.

vs - RXU5 130.00p, bought for 115 in 2k.

- OEU5 117.75p, bought for 64.5 in 4k.

- ERM5 97.87p, bought for 0.25 in 6k.

- SFIU5 96.00/95.90/95.60p ladder, bought for 3.5 in 4k.

- SFIZ5 96.25/96.35/96.45/96.55c condor, bought for 2 in 5k.

- SFIZ5 95.90/95.80/95.70/95.60p condor, bought for 1.75 in 8.88k.

US 10YR FUTURE TECHS: (U5) Pierces Key Resistance

- RES 4: 112-04+ High May 2

- RES 3: 111-25 High May 7

- RES 2: 111-05+ High May 9

- RES 1: 110-30 High May 30 and today’s intraday high

- PRICE: 110-17 @ 16:51 BST Jun 2

- SUP 1: 109-26/12+ Low May 29 / 22 and the bear trigger

- SUP 2: 109-09+ Low Apr 11 and key support

- SUP 3: 109-00 Round number support

- SUP 4: 108-25+ 0.764 proj of the Apr 7 - 11 - May 1 price swing

A bear cycle in Treasury futures remains in play for now, and recent short-term gains still appear corrective. However, the contract has breached an important resistance at 110-23, the May 16 high. A clear break of this level would undermine a bearish theme and highlight a stronger reversal, exposing 111-05+, the May 9 high. On the downside, a reversal lower would refocus attention on the bear trigger at 109-12+.

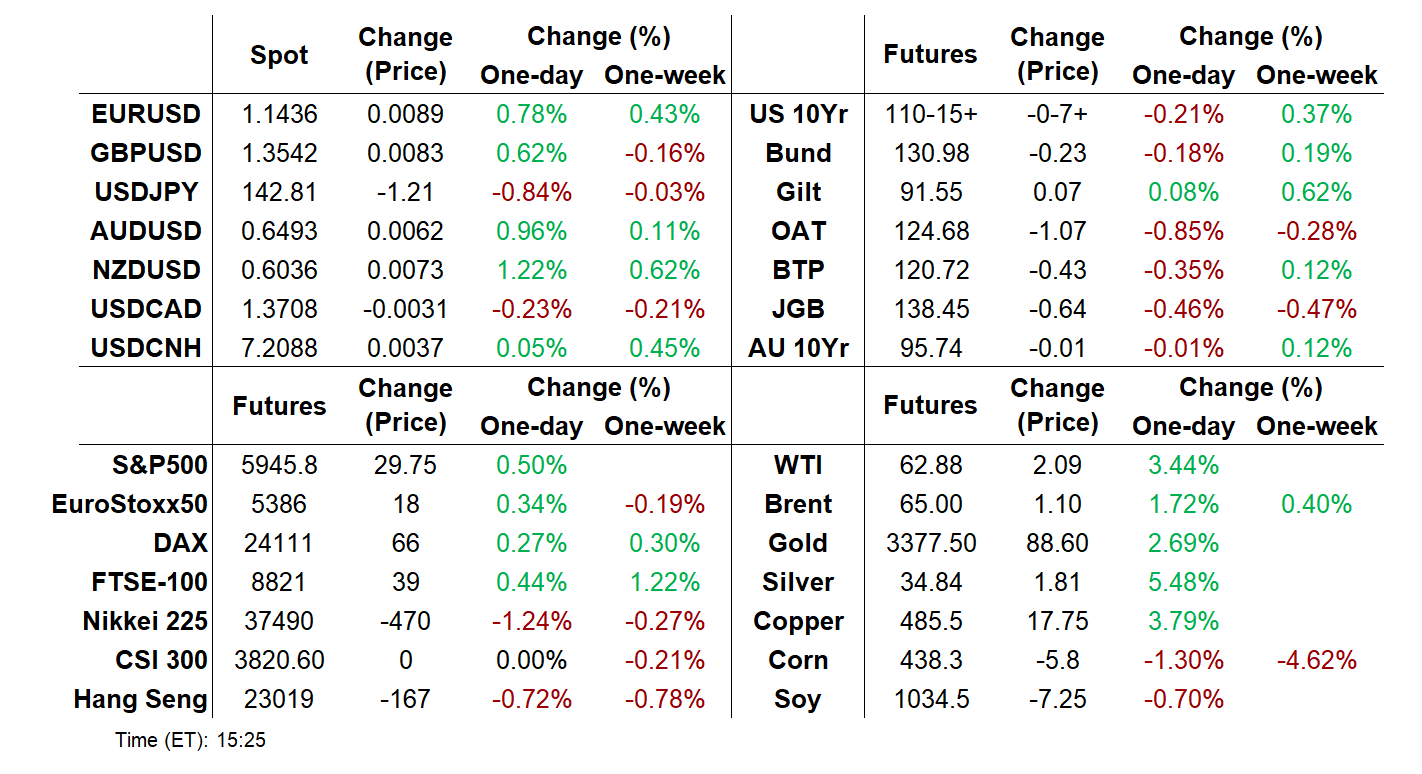

FOREX: US Dollar Weakness Prevails, AUD & NZD Outperform

- The US dollar lost ground on Monday as markets assess the latest geopolitical concerns regarding the Russia/Ukraine conflict and tariff related developments between the US and China. The prevailing trend of greenback weakness has resumed, placing the USD Index at the lowest level for a month and narrowing the gap with the bear trigger at 97.92. The formation of a bearish engulfing daily candle on Thursday last week adds to the S/T downside focus.

- An extension of dollar weakness was seen following a below-expectation ISM manufacturing print, however, the subsequent stabilisation for equity markets allowed the DXY (-0.50%) to moderately recover from its worst levels.

- Despite the initial pessimistic tone for broader risk sentiment, AUD, NZD and NOK are the best performing currencies to start the week. AUDUSD received support in the low 0.6400s last week keeping bullish trend signals intact. A continuation higher would open 0.6550, a Fibonacci retracement, and the November 25 high. Above here, the key medium-term focus is on the US election related highs at 0.6688.

- In similar vein, a 1% rise during today’s session has prompted NZDUSD to return to an important zone of resistance between 0.6025/40. A close at current levels would be the highest since the US election, signalling scope for a more protracted recovery towards 0.6168, the 76.4% retracement of the Sep ’24 – Apr ’25 selloff.

- USDJPY extended its pullback from last Thursday’s 146.28 high, and spot now trades back below 143.00. A continuation lower would expose 142.12, the May 27 low. Clearance of this level would resume the bear leg and signal scope for a move towards a key medium-term pivot around the 140.00 mark.

- RBA minutes kick off Tuesday’s economic calendar, before Swiss and Eurozone inflation data. JOLTS job openings will headline the US session. Bank of Japan Governor Ueda is due to speak at the Research Institute of Japan, in Tokyo.

OPTIONS: Larger FX Option Pipeline

- EUR/USD: Jun04 $1.1400-05(E1.0bln); Jun05 $1.1050(E5.9bln), $1.1300(E2.3bln), $1.1400(E2.2bln), $1.1415-25(E1.5bln), $1.1500(E1.5bln); Jun06 $1.1500(E1.0bln)

- USD/JPY: Jun05 Y142.00($1.1bln), Y143.00-05($1.1bln)

- AUD/USD: Jun04 $0.6435-55(A$1.5bln);

- USD/CAD: Jun04 C$1.3735-50($1.2bln)

EQUITY TECHS: E-MINI S&P: (M5) Bullish Theme

- RES 4: 6124.00 High Feb 24

- RES 3: 6080.75 High Feb 26

- RES 2: 6057.00 High Mar 3

- RES 1: 6008.00 High May 29

- PRICE: 5895.00 @ 14:14 BST Jun 2

- SUP 1: 5825.39/5749.04 20- and 50-day EMA values

- SUP 2: 5596.00 Low May 7

- SUP 3: 5455.50 Low Apr 30

- SUP 4: 5355.25 Low Apr 24

The trend condition in S&P E-Minis remains bullish. Last Thursday’s initial gains delivered a print above 5993.50, the May 20 high and a bull trigger. The break highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. 6000.00 has been pierced, an extension would open 6057.00 next, the Mar 3 high. Key support lies at 5742.22, the 50-day EMA. A clear break of this average is required to highlight a reversal.

DATA/EVENTS CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 03/06/2025 | 0130/1130 | Business Indicators | ||

| 03/06/2025 | 0130/1130 | Balance of Payments: Current Account | ||

| 03/06/2025 | 0145/0945 | ** | S&P Global Final China Manufacturing PMI | |

| 03/06/2025 | 0630/0830 | *** | CPI | |

| 03/06/2025 | 0700/0300 | * | Turkey CPI | |

| 03/06/2025 | 0900/1100 | *** | HICP (p) | |

| 03/06/2025 | 0900/1100 | ** | Unemployment | |

| 03/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 03/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 03/06/2025 | 0915/1015 | BOE Bailey, Breeden, Dhingra, Mann At TSC | ||

| 03/06/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 03/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 03/06/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/06/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 03/06/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 03/06/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/06/2025 | 1645/1245 | Chicago Fed's Austan Goolsbee | ||

| 03/06/2025 | 1700/1300 | Fed Governor Lisa Cook | ||

| 03/06/2025 | 1930/1530 | Dallas Fed's Lorie Logan | ||

| 04/06/2025 | 2300/0900 | * | S&P Global Final Australia Services PMI | |

| 04/06/2025 | 2300/0900 | ** | S&P Global Final Australia Composite PMI | |

| 04/06/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 04/06/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 04/06/2025 | 0130/1130 | *** | Quarterly GDP |