MNI ASIA MARKETS ANALYSIS: Tsys Track Bunds, US$ Retreat

HIGHLIGHTS

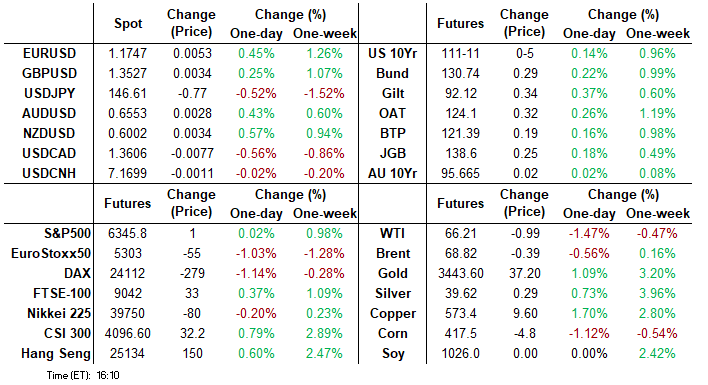

- Treasuries look to finish near moderate session highs Tuesday, 10s back to early July 10 levels, the US$ retreating to lows over the same period.

- Philadelphia Fed's Nonmanufacturing Business Outlook Survey continued to show improvement in July, though cost pressures remained elevated. Otherwise data proved muted.

- Pres Trump announced trade deals with Indonesia and the Philippines, the latter levied a 19% tariff vs. the pre-Liberation Day level of 2.5%.

US TSYS

MNI US TSYS: Tsys Back at July 10 Lvls, Philly Fed Non-Mfg Improves, Costs Elevated

- Treasuries bounced off early Tuesday lows, initially tracking a similar move in German Bunds - before settling into a narrow range near session highs since midmorning.

- The US$ resumed its weakening trend on Tuesday, extending the pullback from last week’s highs to ~1.6% in recent trade, further eroding the cautious recovery that had been seen across the first half of July.

- Tsy Sep'25 10Y futures are +7 at 111-13 after the bell vs. -14.5 high, briefly through resistance at 111-13+, the Jul 10 high. A clear break of this hurdle would highlight a stronger reversal. Key support lies at 110-08+, the low on Jul 14 and 16. A move through this support would reinstate the recent bearish theme.

- The Philadelphia Fed's Nonmanufacturing Business Outlook Survey continued to show improvement in July, though cost pressures remained elevated. The regional current general activity index rose to a 6-month high -10.3 from -25.0 prior. This was the 3rd consecutive improvement since bottoming at -42.7 in April amid tariff policy concerns.

- The Johnson Redbook Retail Sales Index continues to post solid gains, rising 5.1% Y/Y in the week ending Jul 19, fairly steady compared with 5.2% the prior week.

- Look ahead: Wednesday's data limited to MBA Mortgage Applications at 0700ET, Existing Home Sales follow at 1000ET.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.28% (-0.02), volume: $2.688T

- Broad General Collateral Rate (BGCR): 4.27% (-0.02), volume: $1.104T

- Tri-Party General Collateral Rate (TCR): 4.27% (-0.02), volume: $1.077T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $108B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $280B

FED Reverse Repo Operation

RRP usage retreats to $196.374B this afternoon from $213.666B yesterday, total number of counterparties at 34. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to July 1: $460.731B highest usage since December 31.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options segued to downside puts, put spds since midmorning - fading the rebound in underlying futures. Projected rate cut pricing gains slightly vs. early morning (*) levels: Jul'25 at -1.2bp, Sep'25 at -16.1bp (-14.9bp), Oct'25 at -28.7bp (-27.7bp), Dec'25 at -46.2bp (-44.5bp).

SOFR Options:

Block, -5,000 SFRH6/0QH6 98.00 call spd 2.5 net, short March over

-5,000 SFRU5 95.75/95.87/96.00 iron flys, 10 vs. 95.82/0.08%

+3,000 2QU5 96.62 puts, 8.5 vs. 96.77/0.32%

-2,500 SFRV5 96.31 calls, 8.0 ref 96.12

15,000 SFRU5 95.81 put vs. SFRZ5 95.87 puts, cab net

Block, +15,000 SFRU5 95.75 put vs 95.81/95.87 call spd, 0.025

+10,000 SFRU5 95.87/96.12 call spds vs. 95.62/95.75 put spds, 1.0 net

-10,000 SFRU5 95.68/95.81 put spds 5.62/splits

-3,000 SFRU5 95.68/95.87 put spds, 9.0 vs. 95.84/0.46%

5,300 SFRZ5 96.00/96.25 strangles

Block/screen, 9,000 SFRV5 96.12/96.18/96.31/96.44 broken call condors, 0.5 vs. 96.06/0.05%

2,000 SFRU5 95.81/95.87/96.00/96.06 call condors ref 95.83

+4,000 SFRZ5 96.12/96.37/96.62 call flys, 3.5 ref 96.10

Treasury Options:

3,500 TYQ5/TYU5 111 call spds

2,150 FVQ5 108.5/109.25 call spds 11.5

3,500 USZ5 124/125 call spds ref 113-16

5,000 TUU5 104/104.5 call spds ref 103-24.25

over 15,500 TYQ5 111.5/112 1x2 call spds, 3 ref 111-12.5

3,370 TYQ5 111.25/112.25 strangles vs. TYU5 111.5 straddle

+23,000 TYU5 112 calls, 27 vs. 111-07/0.31%

5,340 TYQ5 111.5/112 1x3 call spds ref 111-05.5

20,300 TYU5 112 calls, 23 ref 111-02.5

-2,500 TYQ5 110.5/111 put spds, 8 ref 111-01.5

+3,700 TYU5 112.5 calls, 20 vs. 111-11/0.23% (-20k overnight)

1,000 USU5 93/135 strangle ref 113-01

+3,000 TYU5 107 puts, 3 vs. 111-00/0.15%

+5,000 TYU5 109.5/110.5 put spd vs. 112.5 calls, 0.0 net

+3,000 TYQ5 111.5/112

-20,000 TYU5 112.5 calls, 17 early overnight ref 111-04

MNI BONDS: EGBs-GILTS CASH CLOSE: Bull Flattening Move Continues

The bull flattening move in EGBs and Gilts continued for a second session Tuesday.

- Once again, there was no single trigger for the bullish move in global core FI which overall looked like a continuation move from Monday's constructive session.

- Some pointed to the rally in Treasuries as spilling over into the European space. The biggest move of the day coincided with US Treasury Secretary Bessent's suggestion that there was no reason for Fed Chair Powell to leave office before the end of his term in 2026, helping US long-end yields lower.

- In data, UK public sector net borrowing was higher than expected, while the ECB's Q2 Bank Lending Survey saw credit demand from firms pick up but overall momentum remaining weak.

- As noted, both the UK and German curves bull flattened on the day, with Gilts slightly outperforming.

- Periphery / semi-core EGB spreads were mixed, with BTPs underperforming and OATs outperforming.

- Wednesday's calendar includes Eurozone consumer confidence data but the week's focus remains the ECB decision Thursday.

- MNI's ECB preview has been published (PDF here) - alongside the expected hold, this week’s communication is expected to be as non-committal as possible, maintaining flexibility and buying time for a fresh forecast round in time for the Sep 11 meeting. The balance of risks will be important in determining any market reaction.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.2bps at 1.812%, 5-Yr is down 1.6bps at 2.152%, 10-Yr is down 2.3bps at 2.59%, and 30-Yr is down 2.2bps at 3.117%.

- UK: The 2-Yr yield is down 2.7bps at 3.842%, 5-Yr is down 3.8bps at 3.997%, 10-Yr is down 3.4bps at 4.569%, and 30-Yr is down 2.8bps at 5.4%.

- Italian BTP spread up 0.7bps at 84.4bps / French OAT down 0.3bps at 67.6bps

MNI OPTIONS: Lean Toward Put Structures Amid Rate Declines Tuesday

Tuesday's Europe rates/bond options flow included:

- DUU5 107.20 puts, bought for 8 in 6k

- RXZ5 127.00/125.50 put spread, paper pays 35 in 5k

- ERZ5 98.25/98.375/98.50/98.625 call condor, paper sells for 2.5 in 3.75k

- SFIZ5 96.35/96.50/97.00 call ladder sold at 3.5 in 4k

- SFIF6 96.25/96.00 1x2 put spread, bought for 2.75 in 8k

MNI FOREX: Broad USD Weakness Extending, USDJPY Approaches 146.00

- After consolidating the Monday selloff overnight, the USD index (-0.52%) has resumed its weakening trend on Tuesday, extending the pullback from last week’s highs to ~1.6% in recent trade, further eroding the cautious recovery that had been seen across the first half of July. An extension lower for US yields appears to be assisting the move, helped by Treasury Secretary Bessent providing a more optimistic tone regarding Powell’s short-term future as the Fed Chair.

- Outside of the scandies, gains have been led by the Japanese Yen and Swiss Franc in G10, helping USDJPY extend its post upper house election pullback. USDJPY downside momentum built through initial support of 146.92 (Jul 16 low), printing down to a session low of 146.31. Short-term pivot support to monitor next is 145.85, the 50-day EMA.

- Bessent’s mention of Japan talks going “very well” and that the election may be the impetus to getting a deal done will have also provided tailwinds for the yen. His comments follow Japan’s chief trade negotiator meeting with the US Commerce Secretary on Monday ahead of the looming August 01 deadline.

- Elsewhere, advances for the likes of GBP, AUD, NZD and CAD have all mirrored the adjustment for the DXY. For EURUSD, spot has traded back above 1.1750, narrowing the gap back to cycle highs at 1.1829, the Jul 1 high and the bull trigger.

- The swift reversal and subsequent resumption of weakness keeps a bearish trend intact for USDCAD. Downside momentum appears to have picked up below some daily lows around 1.3650 today and further declines would refocus attention on key support at 1.3540, the Jun 16 low.

- GBP has relatively underperformed, however, cable has still risen back above the 1.35 handle which further negates the prior bearish technical breaks last week. This dynamic keeps EURGBP trading towards its most recent highs and attention firmly on the April 11 high at 0.8738.

MNI US STOCKS: Late Equities Roundup: Chip Makers & Media Stocks Lead Gainers

- Stocks remain mixed late Tuesday, S&P eminis back near steady vs. weaker Nasdaq index. Currently, the DJIA trades up 142.22 points (0.32%) at 44464.55, S&P E-Minis up 2.5 points (0.04%) at 6347.25, Nasdaq down 65.1 points (-0.3%) at 20909.01.

- Information Technology and Communication Services sector stocks continued to lead the late session declines, semiconductor makers weighing on IT: KLA Corp -4.66%, Lam Research -3.74%, Micron Technology -3.71%, Broadcom Inc -3.33%, Dell Technologies -3.21% and Super Micro Computer -3.03%.

- Interactive media and entertainment shares weighed on the Communications sector: Netflix -2.82%, Meta Platforms -1.21%, TKO Group Holdings -1.06% and Take-Two Interactive Software -0.86%.

- On the positive side, Health Care and Homebuilding sectors led gainers by midday: IQVIA Holdings surged 18.6% higher on strong earnings, Charles River Laboratories +8.49%, Quest Diagnostics +6.40%, Moderna +5.13%, Thermo Fisher Scientific +4.65% and Bio-Techne +4.48%.

- Also on strong earnings: DR Horton +15.93%, PulteGroup +10.68%, NVR Inc +7.37% and Lennar Corp +8.29%. Other leaders included Northrop Grumman +9.15%, Enphase Energy +7.00% and Albemarle +6.73%..

- Earnings expected after today's close: Lockheed Martin Corp, Capital One Financial Corp, Texas Instruments Inc, EQT Corp, CoStar Group Inc, Intuitive Surgical Inc, Enphase Energy Inc, Pegasystems Inc, Range Resources Corp and Baker Hughes Co.

MNI EQUITY TECHS: E-MINI S&P: (U5) Fresh Cycle High

- RES 4: 6439.884 1.500 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6402.44 1.382 proj of the May 23 - Jun 11 - 23 price swing

- RES 2: 6381.50 1.764 proj of the Apr 7 - 10 - 21 price swing

- RES 1: 6374.00 High Jul 21

- PRICE: 6350.00 @ 1502 ET Jul 22

- SUP 1: 6288.25 Low Jul 17

- SUP 2: 6256.07/6111.35 20- and 50-day EMA values

- SUP 3: 5811.50 Low May 23

- SUP 4: 5645.75 Low May 7

S&P E-Minis traded to a fresh cycle high Monday before pulling back. The climb confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Note that moving average studies are in a bull-mode position highlighting a clear dominant uptrend. Sights are on 6381.50, a Fibonacci projection. Key support is at the 50-day EMA, at 6111.35. Support at the 20-day EMA is at 6256.07.

MNI COMMODITIES: Crude Falls, Gold And Copper Extend Gains

- Crude futures continue to drift towards the low end of the trading range seen through much of July. US trade demands and potential retaliation from trading partners continue to weigh on pricing.

- WTI Aug 25 is down by 1.3% at $66.3/bbl.

- With trade negotiations continuing, US Treasury Secretary Bessent said he will meet Chinese counterparts in Stockholm next week for a third round of talks aimed at extending a tariff truce and widening the discussions, potentially to include Beijing’s purchases of oil from Russia and Iran.

- A bearish theme in WTI futures remains intact, with support to watch at $65.76, the 50-day EMA. This average has been pierced, and a clear break of it would expose $58.87, the May 30 low.

- Meanwhile, spot gold has risen by 1.0% to $3,430/oz, building on yesterday’s solid 1.4% rally to take the yellow metal to its highest level since June 16.

- Today’s gains come on the back of further weakness in the US dollar, assisted by an extension lower in US yields, after Bessent provided a more optimistic tone regarding Powell’s short-term future as Fed Chair.

- The move widens the gap with prior resistance at $3,395.1, the June 23 high, which was pierced yesterday, signalling scope for a push towards $3,451.3, the June 16 high.

- Elsewhere, copper has also rallied by 1.4% to $572/lb, its highest level since July 9.

- The move narrows the gap to resistance at $589.55, the July 8 high. Clearance of this level would open $600.00.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 23/07/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 23/07/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 23/07/2025 | 1400/1000 | *** | NAR existing home sales | |

| 23/07/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 23/07/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 23/07/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 23/07/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 24/07/2025 | - | European Central Bank Meeting | ||

| 24/07/2025 | 2300/0900 | *** | Judo Bank Flash Australia PMI | |

| 24/07/2025 | 0030/0930 | ** | Jibun Bank Flash Japan PMI |