MNI ASIA MARKETS ANALYSIS: Tsys Rise, Shutdown Day 19

HIGHLIGHTS

- Treasuries drift near moderate late session highs after the close, modest volumes as the US Gov enters shutdown day 19, no data & the Federal Reserve in policy blackout through October 30.

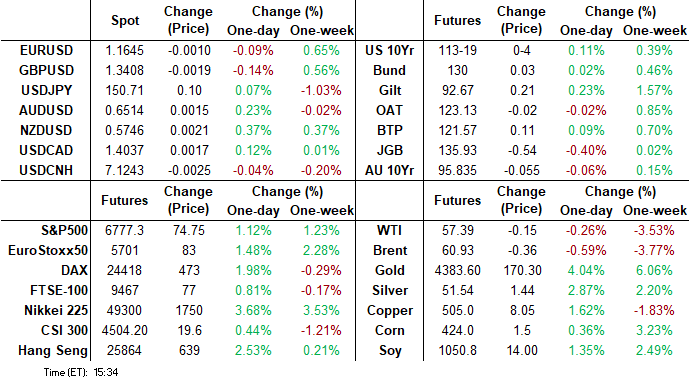

- The USD index trades a touch firmer Monday, extending the bounce from Friday’s lows by around 0.1% to 98.60

- Information Technology, Communication Services and Industrials sector shares lead advances late Monday - indexes remain off record highs from earlier in the month, however.

- President Trump $20bn currency swap line between the BCRA and US Treasury today.

- Core CPI inflation is mostly expected to moderate from the 0.35% in August although it would be a third consecutive strong month after the 0.32% in July as well.

US TSYS

MNI US TSYS: Treasuries Inch Higher As US Enters Shutdown Day 19

- Treasuries extended the top end of the range late Monday on relatively modest volumes (TYZ5 just over 1M) as the US Gov enters shutdown day 19, no data & the Federal Reserve in policy blackout through October 30.

- The Dec'25 10Y futures contract trades +4 at 113-19, 113-10.5 low / 113-20 high. MA studies are in a bull-mode position and this set-up continues to highlight a dominant uptrend. Sights are on 114-10, the Apr 7 high (cont) and the next key resistance.

- Speaking at a bilateral meeting with Australian PM Anthony Albanese, US President Donald Trump confirms that he intends to meet Chinese President Xi Jinping in South Korea during the Asia Pacific Economic Cooperation annual summit at the end of the month.

- Expected corporate earnings announcements after the close include: Cleveland-Cliffs, Crown Holdings, Steel Dynamics, AGNC Investment Corp and Zions Bancorp - the regional bank in the spotlight last week after it "disclosed a $50 million charge-off for a loan underwritten by its wholly-owned subsidiary, California Bank & Trust," Bbg reported.

- Looking ahead, UK fiscal data will be published ahead of Canada CPI on Tuesday, while markets will remain focused on Friday’s US inflation data. An early look at analyst unrounded core CPI estimates for Friday’s delayed September release sees a median estimate of 0.30% M/M, with a reasonably wide range of 0.25-0.36% M/M.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.18% (-0.12), volume: $3.022T

- Broad General Collateral Rate (BGCR): 4.16% (-0.09), volume: $1.180T

- Tri-Party General Collateral Rate (TCR): 4.16% (-0.09), volume: $1.145T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.11% (+0.00), volume: $79B

- Daily Overnight Bank Funding Rate: 4.11% (+0.00), volume: $169B

FED Reverse Repo Operation

RRP usage rebounds to $5.931B with 9 counterparties this afternoon from $4.102B Friday. Compares to $3,516B on Tuesday, Oct 13 (lowest level since early April 2021) & this year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

Rather modest SOFR/Treasury option volumes to report Monday, as the US Gov enters shutdown day 19. No data and the Fed in policy blackout. Underlying futures modestly higher (TYZ5 113-19 +4) while US$ index pares modest gains in late trade. Projected rate cut pricing cools slightly vs. late Friday levels (*): Oct'25 at -24.7bp (-25.3bp), Dec'25 at -50bp (-50.9bp), Jan'26 at -63.7bp (-64.8bp), Mar'26 at -77bp (-77.9bp).

SOFR Options:

3,200 SFRM6 96.25/96.62/97.00 vall flys ref 96.87

2,000 SFRH6 96.37 puts, 4.0

over +12,500 SFRZ5 96.12 puts, 0.5 ref 96.365/0.05%

+2,500 SFRX5 96.75/96.87 call spds, cab

-4,000 SFRZ5 96.25/96.37 call spds, 8.5

+2,000 SFRM6 96.25/96.37 put spds, 2.0 ref 96.87

1,600 SFRH6 96.31/96.43 put spds

1,500 SFRM6 96.25/96.62/97.00 call flys

+8,000 SFRG6 96.68/96.81/96.87/97.00 call condors, 1.75 ref 96.625 to -.63

Treasury Options:

1,560 USX5 116.5/117/118 broken put flys ref 118-24

6,000 TUZ5 104.25 puts, ref 104-13.75

9,000 TYZ5 113.5/114.5 call spds, 6 ref

10,000 TYZ5 113.5/114.5 2x1 call spds vs. TYZ 112.5 puts

Update, total -6,000 TYF6 113.5 straddles, 163-200 vs. 113-09 to -13.5/0.06%

2,000 TYX5 114/115.5 call spds, 5 ref 113-16

2,500 FVF6 110/111.5 call spds ref 1109-27.5

over 5,000 TYX5 113.5/118 call spds on ratio

over 5,000 FVX5 109.5 puts, 5.5 last

5,900 TYX5 113 puts, 7-8 ref 113-13.5/0.08%

-5,000 TUZ 104.75 calls, 5 ref 104-13

+3,000 TYH6 107.5/109 put spds, 6

3,000 TYF6 110/112 put spds, 23 vs. 113-11/0.20%

MNI EGBS: BTP/Bund Spread Near Session Lows, Growth Data Key To Further Narrowing

The 10-year BTP/Bund spread trades close to session lows of ~78.5bps, benefiting from the latest extension higher in global equity futures.

- We highlighted last week that having already tightened by ~35bps this year, the 10-year BTP/Bund spread has struggled to sustainably consolidated below 80bps in recent months.

- Signs of a more resilient domestic growth outlook may be a necessary condition for further narrowing. Although the 2026 draft budget projects the Italian deficit to fall to 2.8% next year, a weak growth trajectory may impede continued improvements in fiscal metrics. Q3 flash GDP is due on October 30.

- Note that EUR 3m10y swaption vol has also moved away from multi-year lows through October, which may be limiting near-term tightening impulses.

- BTP futures are +7 ticks at 121.53, off session lows of 121.58. Initial resistance is Friday’s opening high of 121.94.

- Italy is issuing the new retail-only 7-year Oct-32 BTP Valore this week. Day 1 books are currently E4.9bln. That’s above the E3.7bln raised on the first day of the last BTP Valore issue in May 2024, but currently below the E5.6bln raised on the first day of the BTP Piu issue in February 2025.

MNI FOREX: JPY Volatility on Show, NZD Outperforms on CPI Beat/Equity Rally

- The USD index trades a touch firmer to start the week, extending the bounce from Friday’s lows by around 0.1% to 98.60. China third quarter GDP slowed to 4.7% Y/y, however the print came in marginally above expectations, prompting minimal impact on broader risk sentiment and the greenback. President Trump expressed optimism around US-China trade talks (albeit with clear focus points), keeping major equity benchmarks in the green Monday.

- Despite the broadly contained price adjustments across G10 FX, the Japanese yen has had a volatile session, registering a 92 pip range. Developments regarding Japan's LDP and Ishin parties forming a coalition initially boosted USDJPY to 151.20, before hawkish remarks from BoJ board member Takata and headlines on the BOJ revising the economic growth forecast up assisted a solid reversal to 150.28 session lows. Price has subsequently consolidated close to unchanged levels around 150.75.

- Elsewhere, New Zealand Q3 CPI came in at 1.0% Q/q overnight, one tenth above market expectations. While the data overall was close to RBNZ expectations, NZD does stand 0.40% higher on the session, assisted by the constructive price action for major equity indices late Monday. Despite the bounce for NZDUSD, bearish conditions remain firmly intact, with the pair remaining just 1.15% above cycle lows at 0.5683, 6-month lows for the pair.

- It is also worth noting that EURCHF has fallen 0.25%, further narrowing the gap to a crucial cluster of support between 0.9206-22. Clearance of the lows would place EURCHF at its lowest since the peg removal in 2015.

- In emerging markets, the Colombian peso has significantly underperformed peers following the negative newsflow on US tariff threats against Colombia and weaker-than-expected economic activity data published on Monday. USDCOP has risen 1.5% on the session, extending the bounce from Friday’s cycle lows to around 3.2%.

- Looking ahead, UK fiscal data will be published ahead of Canada CPI on Tuesday, while markets will remain focused on Friday’s US inflation data.

MNI ARGENTINA: Milei Says Swap Line Provides Security, Remains Confident On Election

- Speaking after the signing of the $20bn currency swap line between the BCRA and US Treasury today, President Milei said that the agreement is to provide security and will only be executed when needed. According to a report in La Nacion, Milei said that if the government can’t access the international capital market because of elevated country risk, then it will make payments due next year using the swap line.

MNI FX OPTIONS: Expiries for Oct21 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E961mln), $1.1640(E550mln), $1.1700(E941mln), $1.1800(E1.0bln)

- USD/JPY: Y149.90-00($1.4bln)

- GBP/USD: $1.3270(Gbp478mln), $1.3290-00(Gbp850mln)

- AUD/USD: $0.6495-00(A$800mln)

- USD/CNY: Cny7.1075($715mln), Cny7.1400($759mln)

MNI US STOCKS: Late Equities Roundup: Continued Gains, Still Off Record Highs

- US Stocks continue to drift higher late Monday - but remain off record highs from earlier in the month as the US Gov enters shutdown day 19. Currently, the DJIA trades up 531.63 points (1.15%) at 46,720.6 vs record high of 47,034.92 on Oct 3, S&P E-Minid Future up 75.75 points (1.13%) at 6,778.25 vs record high of 6,812.25 on Oct 8, Nasdaq up 337.4 points (1.5%) at 23,017.28 vs. record high of 23,098.98 on Oct 10.

- Information Technology, Communication Services and Industrials sector shares lead advances in late trade, supporting the Tech sector: Super Micro Computer +6.82%, ON Semiconductor +5.54%, Apple +4.49% and Arista Networks +4.05%.

- Communication Services gainers included: Trade Desk +4.74%, Netflix +3.88%, Meta Platforms +2.21% and Live Nation Entertainment +1.83%; while Industrials supported by Jacobs Solutions +5.14%, United Airlines Holdings +3.84%, Delta Air Lines +3.77% and Leidos Holdings +3.30%.

- Conversely, a mix of Consumer Staples and Utilities sector shares underperformed in the first half: Church & Dwight Co -0.99%, Molson Coors Beverage -0.99%, Walmart -0.93% and Altria Group -0.89%, while Constellation Energy -3.67%, Vistra -2.74%, NRG Energy -0.42% and Pinnacle West Capital -0.11%.

- Expected corporate earnings announcements after the close include: Cleveland-Cliffs, Crown Holdings, Steel Dynamics, AGNC Investment Corp and Zions Bancorp - the regional bank in the spotlight last week after it "disclosed a $50 million charge-off for a loan underwritten by its wholly-owned subsidiary, California Bank & Trust," Bbg reported. Western Alliance, the second bank in the hot seat after announcing bad loans/investments last week, announces Tuesday after the close.

- Additional corporate earnings expected this week include: Halliburton, PulteGroup, Lockheed Martin, Northrop Grumman, GM, Netflix, Capital One, Texas Inst, AT&T, Alcoa, American Airlines, Valero, Ford, Intel, General Dynamics, Baker Hughes and Procter & Gamble.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Support Remains Intact

- RES 4: 6850.87 1.618 proj of the Aug 1 - 15 - 20 price swing

- RES 3: 6831.38 2.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6819.25 1.500 proj of the Aug 1 - 15 - 20 price swing

- RES 1: 6783.00/6812.25 Intraday High Oct 20 / High Sep 9 and bull trigger

- PRICE: 6777.75 @ 1443 ET Oct 20

- SUP 1: 6615.80 50-day EMA

- SUP 2: 6540.25 Low Oct 10 and a key short-term support

- SUP 3: 6506.50 Low Sep 5

- SUP 4: 6427.00 Low Sep 2

Recent weakness in S&P E-Minis appears corrective - for now. Price has pierced support at the 50-day EMA, currently at 6615.80, but this support area remains intact - for now. Note that the Oct 10 low of 6540.25 marks the key short-term support. Clearance of this level would undermine a bull theme. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend. The bull trigger is 6812.25, the Oct 9 high.

COMMODITIES

MNI AMERICAS OIL: US OIL: October 20 - Americas End of Day Oil Summary: Crude unch

WTI crude ended mixed but remains above the low of $56.15/bbl from last week after finding some support on Friday from a more positive US-China trade outlook. Concern remains for fundamentals with supply increasing and demand softening.

- US-China trade negotiations continue this week and Trump’s comments signal that there should be an agreement.

- Chinese imports of crude oil from Malaysia fell in September to their lowest level in more than two years, Customs data showed.

- China’s crude oil stockpile flows dropped sharply in September as lower imports and higher refinery processing cut the surplus available for storage, according to Reuters’ Clyde Russell.

- Focus remains on Ukraine-Russia with meetings due to take place including possibly a second meeting between Trump and Putin “within two weeks or so” following a meeting last week.

- WTI Nov futures were down 0.1% at $57.52

- WTI Dec futures were down 0.2% at $57.03

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 21/10/2025 | 0600/0700 | *** | Public Sector Finances | |

| 21/10/2025 | 0700/0900 | ECB Lane at Macroeconomics and Finance Conference | ||

| 21/10/2025 | 0900/1100 | * | government debt | |

| 21/10/2025 | 0900/1100 | * | government deficit | |

| 21/10/2025 | 0900/1000 | BOE Saporta Fireside Chat at Islamic Development Bank | ||

| 21/10/2025 | 1030/1130 | BOE Bailey & Breeden on Private Markets at Financial Services Regulation Committee | ||

| 21/10/2025 | 1100/1300 | ECB Lagarde Keynote at Norges Bank Climate Conference | ||

| 21/10/2025 | 1230/0830 | *** | CPI | |

| 21/10/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 21/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 21/10/2025 | 1915/2015 | BOE Mann Fireside Chat at Lazard |