MNI ASIA MARKETS ANALYSIS: Tsys Rebound Late, Focus on Powell

HIGHLIGHTS

- Treasuries rebound late Monday after unwinding last Friday's risk off support following Trump's threat to impose more tariffs on China, light volumes due to Columbus day holiday.

- Focus Tuesday shifts to the return in earnest for US markets and the upcoming beginning of earnings season in the US. Financials are the early focus, with most major Wall Street names set to report.

- Philly Fed Paulson sees easing through year-end in line with the September SEP median - in other words, two more cuts by year-end.

US TSYS

MNI US TSYS: Tsys Rebound Late, 2s-10s Leading on Subdued Holiday Trade

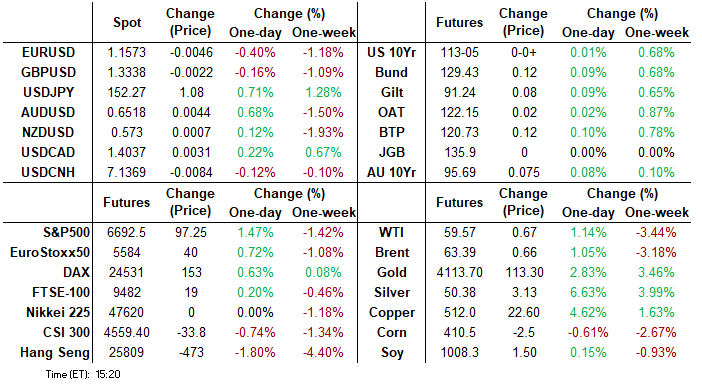

- Treasury look to settle mixed, bonds weaker on very light volumes (TYZ5 670k) due to the Columbus Day holiday. The Dec'25 10Y contract currently trades at 113-05.5 (+1) - rebounding late with no obvious headline of Block-driven support.

- Normal Globex trade hours, stocks open - recovering approximately half of Friday's rout: the DJIA trades up 575.86 points (1.27%) at 46,057.31, S&P E-Minis up 98 points (1.49%) at 6,693, Nasdaq up 467.7 points (2.1%) at 22,674.98.

- No data, but Philly Fed Pres Anna Paulson (non-2025 FOMC voter, votes in 2026) said in a speech Monday that with rates "modestly restrictive now", she sees easing through year-end in line with the September SEP median - in other words, two more cuts by year-end. That's in line with MNI's assumption of her view.

- More Fed speakers tomorrow with focus on Chairman Powell's economic outlook keynote address at the NABE Annual Meeting at 1220ET.

REFERENCE RATES (Not updated due to Columbus Day holiday, levels below from prior session)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.13% (+0.01), volume: $2.923T

- Broad General Collateral Rate (BGCR): 4.10% (+0.01), volume: $1.148T

- Tri-Party General Collateral Rate (TCR): 4.10% (+0.01), volume: $1.120T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.10% (+0.00), volume: $84B

- Daily Overnight Bank Funding Rate: 4.10% (+0.00), volume: $174B

FED Reverse Repo Operation

No RRP usage reported Monday due to the Columbus Day holiday, usage had extended to new low of $4.124B (lowest level since early April 2021) with 10 counterparties last Friday. Compares to this year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR and Treasury option flow remained rather light Monday, cash closed due to Columbus Day holiday. Underlying futures are mixed, short end mildly firmer while projected rate cut pricing rises vs. late Friday levels (*): Oct'25 at -24.7bp (-24.2bp), Dec'25 at -48.1bp (-47.9bp), Jan'26 at -61.0bp (-60.2bp), Mar'26 at -73.5bp (-72.3bp).

SOFR Options

3,000 SFRZ5 97.00/97.50/98.00 call flys ref 97.025

+6,000 SFRZ5 96.18/96.31/96.50/96.62 call condors, 8.0 ref 96.36

+10,000 SFRZ5 96.56/96.75 call spds, 1.5 ref 96.36

-4,000 SFRM6 96.82/97.25 call spds, 10.0 ref 96.80

-1,500 0QX5 97.00 straddles, 22 ref 97.005

+5,000 SFRZ5 96.12/96.25/96.31 put trees, 0.75 ref 96.36

Block, 8,000 SFRH6 97.12/97.25 call spds, 1.0 vs. 96.565/0.04%

1,500 SFRH6 97.00/97.50/97.75 broken call trees

over 5,000 SFRZ5 97.00 calls outright ref 96.36 to -.635

1,800 0QZ5 97.18 calls, 9.0 ref 97.00

over 7,875 SFRZ5 96.50/97.00 1x2 call spds ref 96.36

2,000 SFRZ5 96.12/96.25 put spds ref 96.355

2,100 SFRZ5 96.25/96.31/96.50/96.56 call condors ref 96.355

1,500 SFRZ5 96.31/96.50 call spds ref 96.35

Treasury Options:

2,000 TYX5 111.5/112/112.25/112.75 put condors, 5 net ref 113-00.5

2,000 TUZ5 103.87/104.37/104.5/104.87 put condors ref 104-10.88

2,500 TUZ5 104.62 calls, 6 ref 104-10.75

3,000 FVX5 108.75/109 2x1 put spds, 11 ref 113-02.5

1,100 TYX5 112/112.5/113/113.5 put condors ref 113-01.5

1,500 TYX5 114/115 call spds ref 113-02

over 4,500 TYX5 113.5 calls, 16 ref 113-01.5

1,000 USX5 117/117.5/118 call flys ref 117-24

2,600 TYX5 112.5 puts, 13 ref 112-31.5

1,600 TYX5 109.5 puts, 1 ref 112-31.5

over 8,300 TYZ5 112.5 puts, ref 113-00

MNI BONDS: EGBs-GILTS CASH CLOSE: Bond Bid Holds Despite Equity Bounce

Periphery/semi-core EGBs outperformed Monday amid a broader fall in yields.

- Core yields ticked higher in early trade, with Friday's late fall triggered by escalation in US-China trade tensions fading after conciliatory tones over the weekend.

- From there, core FI regained ground and bid despite an equity recovery, with global price action thinned by North American holidays. Periphery/semi-core EGB spreads tightened on the day.

- Friday's news after the cash close that French President Macron had reappointed Lecornu as PM may have curtailed further OAT/Bund compression but OATs closed Monday roughly in line with peer credits.

- BOE's Greene noted a case for higher-for-longer rates and skipping a cut, in line with prior remarks.

- German instruments outperformed UK counterparts out through the 10Y segment, with Gilts stronger in the long-end.

- Tuesday's highlight is UK labour market data - MNI's preview Hidden PDF. We also get the German ZEW survey and appearances by BOE's Bailey and Taylor, and ECB''s Makhlouf, Kocher and Villeroy.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.5bps at 1.944%, 5-Yr is down 1.9bps at 2.217%, 10-Yr is down 0.8bps at 2.636%, and 30-Yr is down 0.1bps at 3.224%.

- UK: The 2-Yr yield is down 0.8bps at 3.95%, 5-Yr is down 1.7bps at 4.101%, 10-Yr is down 1.7bps at 4.658%, and 30-Yr is down 0.9bps at 5.463%.

- Italian BTP spread down 2bps at 79.8bps / Spanish down 0.9bps at 54.4bps

MNI EGB OPTIONS: Very Busy Opening To The Week, Upside Lean In Rates Continues

Monday's Europe rates/bond options flow included:

- DUX5 107.10c, sold at 5.5 in 3k (suggest closing)

- RX (17th Oct) 128.00p with 127.50p, bought the strip for 2.25 in 9k

- RXX5 130c, bought for 16 up to 18.5 in close to 10k

- RXX5 130.00/132.00 cs vs RXX5 127.50/126.50/125.50/123.00 broken p condor, bought back the cs for 12 in 7.25k

- RXZ5 128.50/127.50/127.00 broken p fly, bought for 18 in 3k

- ERZ5 98.0625 call vs 97.9375 put combo. Paper pays 0.75 for the call in 5k (vs 97.98 spot, 46% delta)

- ERZ5 98.25c bought for 0.5 in 7.5k

- ERH6 98.25c sold at 2.5 in 8k vs 2RH6 97.93c bought for 9.5 in 8k

- ERM6 98.375/98.625 1x1.5 call spread, paper pays up to 1.5 in 5k

- ERU6 98.12/98.37/98.50 broken c fly, bought for 5.25 up to 5.5 in 5k

- 0RH6 98.3125c, sold at 4 in 6k

- 2RZ5 98.00c, bought for 4.5 in 13k total

- SFIZ5 96.10/96.00ps 1x2 vs 96.15/96.25cs, bought the ps for 0.25 in 4k

- SFIG6 96.35/96.55cs vs SFIZ5 96.20c, bought the cs for 1 in 5k

MNI FOREX: JPY Weakness Persists, GBP Resilience to be Tested With Jobs Print

- The early Monday JPY fade persisted through the London close, prompting JPY to comfortably underperform all others in G10. USD/JPY is back above 152.00, but a further rally above 152.64 will be needed to erase the sell-off triggered by Trump's threats to raise tariffs on China on Friday. Politics remains a key driver of the currency, with opposition parties set to meet tomorrow to discuss the collapse of the governing coalition last week. These meetings could help determine whether Takaichi goes ahead with a minority government, or looks to bring forward elections.

- Focus Tuesday shifts to the return in earnest for US markets and the upcoming beginning of earnings season in the US. Financials are the early focus, with most major Wall Street names set to report. 7.4% of the index are set to report between now and Friday, and this quarter’s earnings will be the first to fully reflect the signs of passthrough of tariffs, making those with high exposure to international trade a particular focus.

- Final German CPI data for September is expected to come in unrevised, while the UK jobs data and numerous MPC appearances take focus for GBP. Into the MPC speeches and the run of UK data, GBP/USD is off last week's lows, but inside the Friday range. This leaves the 1.3262 low as key support this week, a break below which exposes the 200-dma of 1.3178 and levels last seen at the beginning of August. It remains difficult to see a protracted GBP/USD sell-off absent a move in the USD however, and with an October Fed rate cut fully priced, there may be limits on how much further the greenback

can rally from here. - Lastly, AUD is stronger against the broader G10 complex, buoyed by both the stronger risk sentiment as a result of Trump's moderation in language toward China, as well as the continued surge in gold prices, which put the price through to record highs once again. The 0.6560 50-day EMA marks the next upside level, which would go further in erasing last week's sell-off. This comes after Friday's support breaks undermined a recent bullish theme, potentially signaling scope for a deeper retracement towards key support at 0.6415, the Aug 21 and 22 low.

MNI OPTIONS: Expiries for Oct14 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1450(E537mln), $1.1500(E848mln), $1.1600(E663mln), $1.1650(E636mln)

- USD/JPY: Y151.50($691mln), Y152.00($751mln)

- AUD/USD: $0.6500(A$1.0bln), $0.6580-00(A$1.2bln)

- USD/CAD: C$1.4000-10($598mln)

MNI US STOCKS: Late Equities Roundup: IT & Materials Sector Remains in Lead

- Stocks well bid late Monday, but still recovering only about half of Friday's sell-off, prices are back near the top end of the day's range after some sporadic profit taking ahead midday. Overall trade was relatively subdued due to the Columbus Day holiday.

- Currently, the DJIA trades up 575.86 points (1.27%) at 46,057.31, S&P E-Minis up 98 points (1.49%) at 6,693, Nasdaq up 467.7 points (2.1%) at 22,674.98.

- Information Technology and Materials sector shares continued to lead the rally, semiconductor makers outperforming: ON Semiconductor Corp +10.47%, Broadcom Inc +9.76% after reports of an accelerated AI chip deal with OpenAI, Monolithic Power Systems +9.25%, Microchip Technology +6.97% and HP Inc +6.58%.

- Materials sector gainers included Albemarle Corp +8.25% apparently on a short squeeze tied to lithium mining, Freeport-McMoRan +5.16%, Newmont Corp +4.72%, Dow Inc +4.02% and DuPont de Nemours +3.65%.

- Conversely, Consumer Staples and Health Care sector shares led declines in the first half: J M Smucker Co -2.93%, Altria Group -2.52%, Monster Beverage -2.43% and Kenvue -2.16%. Pharmaceuticals weighed on the Health Care sector: Humana -2.02%, Eli Lilly & Co -1.31%, Regeneron Pharmaceuticals -1.28% and Edwards Lifesciences -1.27%.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Corrective Pullback

- RES 4: 6850.87 1.618 proj of the Aug 1 - 15 - 20 price swing

- RES 3: 6831.38 2.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6819.25 1.500 proj of the Aug 1 - 15 - 20 price swing

- RES 1: 6705.18/6812.25 20-day EMA / High Sep 9

- PRICE: 6695 @ 1450 ET Oct 13

- SUP 1: 6598.55 50-day EMA

- SUP 2: 6540.25 Low Sep 10 and a key short-term support

- SUP 3: 6506.50 Low Sep 5

- SUP 4: 6427.00 Low Sep 2

A sharp sell-off in S&P E-Minis on Friday is - for now - considered corrective. The contract has found support below the 50-day EMA, currently at 6598.55. Friday’s low of 6940.25 has been defined as a key short-term support. Note that moving average studies remain in a bull-mode position, highlighting a dominant uptrend. The bull trigger is 6812.25, the Sep 9 high. A breach of this hurdle would confirm a resumption of the uptrend.

COMMODITIES

MNI GOLD: Extends All-Time Highs While SocGen Sees $5000/oz Next Year

- Gold today broke to new all-time highs again Monday, with the bullish price action persisting even as equities post a solid recovery off Friday's lows. This continues to point to persistent resilience in gold demand, with the price extending gains since the beginning of September to near 20%.

- While algorithmic and discretionary macro positioning already has been in stretched long territory for a while according to TD Securities, (retail) ETF flows are seen as another recent driver behind bullish price action and would in theory have the potential to expand as the virtuous circle of strong price action is distributed further, reaching broader groups of investors. However, stretched long institutional positioning can add to gold's vulnerability to a potential correction.

- Société Générale today revised upwards their Q426 gold price forecast to $5000/oz from a previous $4,318/oz, seeing "ETF flows remaining strong [and] central bank buying expected to be resilient".

- From a technical perspective, the move higher maintains the price sequence of higher highs and higher lows. Sights are on $4113.5, a Fibonacci projection point. Note that the trend is in overbought territory. A move down would be considered corrective and would allow the overbought set-up to unwind. Support to watch is $3836.5, 20-day EMA.

- The Gold-Silver Ratio meanwhile sits close to cycle lows Monday, pushing below the 80.0 handle for the first time since July 2024. Desks point towards speculative ETF demand underpinning recent gains in silver, which resulted in a move above a major resistance area around the $49.00-$50.00 region, strengthening a bull theme and paving the way for a climb towards $52.00 next. Support for silver to watch lies at $46.204, the 20-day EMA.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 14/10/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 14/10/2025 | 0600/0800 | *** | Germany CPI (f) | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - Payrolls & Claimants | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - Payrolls & Claimants | |

| 14/10/2025 | 0600/0800 | *** | Germany CPI (f) | |

| 14/10/2025 | 0750/0950 | ECB Cipollone Speech on Digital Euro | ||

| 14/10/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 14/10/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 14/10/2025 | - | *** | Money Supply | |

| 14/10/2025 | - | *** | New Loans | |

| 14/10/2025 | - | *** | Social Financing | |

| 14/10/2025 | - | ECB Lagarde and Cipollone at G20 Meeting | ||

| 14/10/2025 | 1200/1300 | BOE Taylor Remarks and Fireside Chat at University of Cambridge | ||

| 14/10/2025 | 1230/0830 | * | Building Permits | |

| 14/10/2025 | 1245/0845 | Fed Governor Michelle Bowman | ||

| 14/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 14/10/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 14/10/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 14/10/2025 | 1610/1210 | BOC Sr Deputy Rogers fireside talk in Vancouver | ||

| 14/10/2025 | 1620/1220 | Fed Chair Jerome Powell | ||

| 14/10/2025 | 1700/1800 | BOE Bailey Fireside Chat at Institute of International Finance | ||

| 14/10/2025 | 1925/1525 | Fed Governor Christopher Waller | ||

| 14/10/2025 | 1930/1530 | Boston Fed's Susan Collins | ||

| 15/10/2025 | 0130/0930 | *** | CPI | |

| 15/10/2025 | 0130/0930 | *** | Producer Price Index | |

| 15/10/2025 | 0430/1330 | ** | Industrial Production |