MNI ASIA MARKETS ANALYSIS: Tsys Near Post-Jobs Highs

HIGHLIGHTS

- Treasuries looked to finish moderately higher Monday, still off last Friday's post-employment data highs, stocks firmer on a nascent risk-on week opener.

- Stocks gained, Nasdaq marked new all time high around 21,885.0 as semiconductor makers and consumer discretionary shares outperformed.

- Weaker-than-expected US employment data continues to keep the risks tilted towards the weaker dollar narrative, emphasised by the USD index spending today’s US session consolidating close to six-week lows.

- Generally slow start to next week - focus on PPI and CPI this Wednesday-Thursday respectively.

US TSYS

MNI US TSYS: Treasuries Drift Higher Ahead Midweek PPI/CPI Data

- Treasuries look to finish moderately higher after a flat open Monday, back near Friday's post NFP highs, stocks gaining as well as rate cut pricing into year end gathers momentum.

- Currently, the Dec'25 10Y contract trades +4.5 at 113-17 vs. -19 high, curves bull flatten: 2s10s -1.392 at 54.905, 5s30s -5.675 at 111.680. Projected rate cuts firmer vs. morning (*) levels: Sep'25 at -28.7bp (-28.4bp), Oct'25 at -49.6bp (-48.2bp), Dec'25 at -71.4bp (-70.6bp), Jan'26 at -85.1bp (-87.7bp).

- Slow start to the week regarding data, main focus is on PPI and CPI this Wednesday-Thursday respectively.

- The New York Fed's Survey of Consumer Expectations leaned in a stag-flationary direction in August, showing both an uptick in short-term inflation expectations and increasing pessimism on the labor market front.

- Starting with the closely-watched inflation expectations, the survey saw a rise in the 1Y median to a 3-month high 3.20% from 3.09% prior. The 3Y median was steady at 3.00% for a 4th consecutive month, but the 5Y median ticked up to a 6-month high 2.93% (2.88% prior).

- Weaker-than-expected US employment data continues to keep the risks tilted towards the weaker dollar narrative, emphasised by the USD index spending today’s US session consolidating close to six-week lows.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.42% (+0.01), volume: $2.847T

- Broad General Collateral Rate (BGCR): 4.40% (+0.02), volume: $1.161T

- Tri-Party General Collateral Rate (TCR): 4.40% (+0.02), volume: $1.127T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $116\B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $225B

FED Reverse Repo Operation

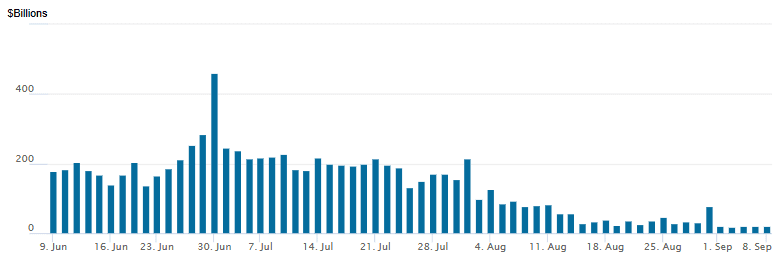

RRP usage slips to $19.416B with 20 counterparties this afternoon from $20.997B last Friday. Compares to $17.923B on Wednesday, Sep 3 - the lowest levels since early April 2021. This year's high usage of $460.731B occurred on June 30.

US SOFR/TREASURY OPTION SUMMARY

Heavier SOFR & Treasury options trade occurred Monday, two-way calls with some chunky unwinds fading the continued support in underlying rates. Underlying futures firmer but still off last Friday's post-employment data highs. Projected rate cuts firmer vs. morning (*) levels: Sep'25 at -28.7bp (-28.4bp), Oct'25 at -49.6bp (-48.2bp), Dec'25 at -71.4bp (-70.6bp), Jan'26 at -85.1bp (-87.7bp).

SOFR Options

Block, 20,000 SFRH6 97.00 calls, 11.0 vs. 96.65/0.28%

+40,000 SFRZ5 96.06/96.18 put spds, 2.5

-8,000 SFRZ5 96.00/96.12/96.25/96.37 put condors, 4 ref 96.385

-20,000 0QU6 97.00/97.50/98.00/98.50 1x1x2x2 call condors, 8.5

5,000 SFRZ5 96.56/96.68/96.81 call flys ref 96.385

Block, 7,000 SFRX5 96.37/96.50 call spds (4.25) vs. 5,000 SFRZ5 96.56/96.68/96.81 call flys (0.75)

Block, 5,000 SFRZ5 95.75/95.87/96.00 put flys ref 96.37

+10,000 SFRZ5 96.50/96.75 call spds 1.0 over 96.12 puts vs. 96.37/0.38%

+8,000 SFRV5 96.31/96.37 call spds, 3.25 ref 96.37

Update, 10,000 SFRV5/SFRZ5 96.50/96.62 call spd spd

-8,000 SFRZ5 96.18/96.73 1x2 call spds 3.75

Block, 5,000 SFRU5 96.00/96.12 call spds 1.25 over 95.93 puts

+4,000 SFRX5 96.37/96.50/96.62 call flys, 2.25

+2,000 SFRX5 96.25/96.37/96.62 broken call flys, 0.25

+2,000 SFRZ5 96.56/96.68 call spds, 2.0

-2,500 SFRH6 96.50/97.00 call spds vs. 96.62/0.25%

4,000 SFRU5 95.75/95.87/96.00 put flys, 2.5 ref 95.99

Block, +5,000 SFRZ5 95.87 puts, 0.5

4,100 0QU5/2QU5 97.00 call spds, 1.5 net

2,000 SFRZ5 96.00/96.06/96.25/96.31 call condors, 2.0

2,000 SFRU5 96.00/96.12 call spds vs. 95.93 put, 1.0 net ref 95.99

1,000 SFRV5 96.43/96.68 call spds vs. 0QV5 97.25/97.50 call spd spd

over -34,700 (pieces) SFRU5 95.87 calls, 11

2,000 0QZ5 97.25/97.37 call spds, 3.5 vs 97.075/0.10%

Treasury Options:

10,000 TYZ5 116 calls, 21 ref 113-18.5

+13,000 TYX5 110/111/112 put flys, 6.0

1,800 TYV5 113.5 straddles, 103

-10,000 TYV5 112.75/113.25/113.5/114 iron condors (wings x2), 13 net cr

2,500 TYV5 111.5 puts vs. 115.25/115.75 call spds ref 113-12.5

-1,250 TYV5 113/114 1x2 call spds, 7

-3,000 FVX5 108.75 puts, 8.5

2,300 FVX 109.75 straddles, 107-107.5

+1,500 TYX5 113 straddles 148 ref 113-13.5

-1,600 TYV5 112/114.75 strangles, 16 ref 113-11.5

1,500 USV5 115/116.5 put spds ref 116-13

-1,250 TYV5 112/115 strangles, 16 ref 113-11

+2,000 FVV5 110/110.5 1x2 call spds, 0.5

MNI BONDS: EGBs-GILTS CASH CLOSE: OATs Shrug Off French Gov't Collapse

EGBs and Gilts resumed the rally that began late last week, with bull flattening seen across curves Monday.

- Core instruments got off to a steady start, largely looking through weekend Japanese political headlines (JGB curve twist steepened overnight after LDP leader Ishiba resigned).

- But the recent rally (helped by Friday's weak US employment data) soon resumed, with limited data / macro headlines to get in the way. 10Y Gilt yields fell to the lowest since Aug 14; Bund Aug 8.

- After the cash close, French PM Bayrou lost a confidence vote in parliament that triggered his resignation, with President Macron now set to name his replacement within days.

- This chain of events was entirely expected and there was no discernable reaction in OAT futures, indeed French spreads tightened on the day.

- In data, German industrial production was slightly stronger than expected.

- Gilts slightly outperformed Bunds on the day, with both curves bull flattening. Periphery/semi-core EGB spreads tightened, with OATs among the outperformers.

- We get some 2nd tier data Tuesday (including arious national-level Eurozone industrial production figures), with the week's European focus being Thursday's ECB decision - MNI's preview will be published Tuesday.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.3bps at 1.926%, 5-Yr is down 1bps at 2.209%, 10-Yr is down 2bps at 2.642%, and 30-Yr is down 3.3bps at 3.264%.

- UK: The 2-Yr yield is down 0.7bps at 3.903%, 5-Yr is down 2.5bps at 4.023%, 10-Yr is down 4.1bps at 4.605%, and 30-Yr is down 4.5bps at 5.459%.

- Italian BTP spread down 1.3bps at 82.9bps / French OAT spread down 2bps at 76.6bps

MNI EGB OPTIONS: Put Spread Selling In Sonia, Put Strip Buying In Euribor Monday

Monday's Europe rates/bond options flow included:

- ERZ5 97.9375 put, ERZ5 97.875 put, ERH6 97.9375 put and ERM6 97.8125 put (put strip). Paper pays 4.25 for 2k

- ERH6 98.125/25 call spread, paper pays 4.25 for 4k

- SFIM6 97.25 calls, bought for 2.0 in 2.5k

- SFIZ5 96.15/96.05 1x2 put spread, paper sells for 3.0 in 3k

MNI FOREX: JPY Volatility in Focus, USD Index Tilts Weaker

- The Japanese yen was the main focus across G10 currency markets on Monday, following the resignation of PM Ishiba and the associated sharp initial negative reaction at the open. USDJPY gapped higher from last Friday’s close around 147.40, swiftly erasing the post payrolls decline to trade as high as 148.58. Resistance in USDJPY at 148.78, the Aug 22 high, remains intact for now.

- Thatcherite MP Sanae Takaichi is a front-runner among many opinion polls to takeover, having previously made clear her preference for easy monetary policy and a bigger role for fiscal spending - reminiscent of the Abenomics policy set from 2012 - 2020. Markets have subsequently calmed, and USDJPY tracks back towards 147.75 ahead of Tuesday’s APAC crossover.

- Overall, weaker-than-expected US employment data continues to keep the risks tilted towards the weaker dollar narrative, emphasised by the USD index spending today’s US session consolidating close to six-week lows. Associated strength in G10 has been led by the likes of AUD and NZD, while political risks in France may have contained the EURUSD price action somewhat.

- The NZDUSD (+0.65%) rally places a clear focus on 50-day EMA resistance (intersecting today at 0.5921), a breach of which would counter the most recent bearish theme. Furthermore, spot has also closed in on 0.5944, short-term trendline resistance drawn from the July 01 high. Further gains would target the August 13 high at 0.5996.

- Tuesday’s calendar will be centred around the preliminary annual payrolls benchmark revision, which is widely expected to imply large downward revisions to nonfarm payrolls growth through the twelve months to March 2025. SNB Chairman Schlegel will also participate in a fireside chat titled "Future-proofing central banks" at the BIS Innovation Summit, in Basel.

- Focus this week remains on the US inflation picture, with PPI and CPI prints due on Wednesday and Thursday respectively.

MNI FX OPTIONS: Expiries for Sep09 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1530-50(E1.2bln), $1.1600(E519mln), $1.1650-70(E1.0bln), $1.1685-05(E2.3bln), $1.1750(E835mln), $1.1790-00(E1.2bln), $1.1885-90(E994mln)

- USD/JPY: Y145.85-00($1.4bln), Y150.00($1.1bln)

- GBP/USD: $1.3595-20(Gbp1.0bln)

MNI US STOCKS: Late Equities Roundup: Nasdaq Climbs to New Record Highs

- The tech-heavy Nasdaq index continued to outperform Monday, drifting near new record highs in late trade, the DJIA and SPX eminis drifting near steady to mildly mixed.

- Still off Friday's high print of 45770.20, the DJIA trades up 16.01 points (0.04%) at 45415.48, S&P E-Minis up 10.5 points (0.16%) at 6500.0, Nasdaq up 116.7 points (0.5%) at 21816.30 vs. 21885.62 high.

- Information Technology and Consumer Discretionary sector shares led gainers in the first half, semiconductor shares rebounding from better selling last week: Broadcom +2.88%, Palantir Technologies +2.52%, Oracle +2.44%, Adobe +2.13% and IBM +2.03%.

- Consumer Discretionary sector was buoyed by: Wynn Resorts +2.31%, Amazon.com +1.60%, Ulta Beauty +1.49% and Aptiv +1.44%.

- On the flipside, Real Estate and Utility sector shares led decliners in the first half. Investment trust shares weighed on the Real Estate sector with Crown Castle -4.08%, American Tower Corp -3.83%, SBA Communications -3.46% and Weyerhaeuser -2.07%.

- Weighing on the Utility sector in late trade: PG&E -3.08%, American Water Works -2.61%, Edison International -2.11% and Sempra -2.08%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Northbound

- RES 4: 6068.66 2.0% 10-dma envelope

- RES 3: 6600.00 Round number resistance

- RES 2: 6543.75 2.00 proj of the Apr 7 - 10 - 21 price swing

- RES 1: 6541.75 High Sep 5

- PRICE: 6499.00 @ 13:10 BST Sep 8

- SUP 1: 6451.12/6371.75 20-day EMA / Low Sep 2

- SUP 2: 6353.11 50-day EMA

- SUP 3: 6313.25 Low Aug 6

- SUP 4: 6239.50 Low Aug 1 and a key support

A bull cycle in S&P E-Minis remains intact and the latest pullback has once again proved to be a shallow correction. The contract traded to a fresh cycle high last week, breaching the Aug 28 high of 6523.00. This confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Sights are on 6543.75 next, a Fibonacci projection. Initial support to watch is 6447.06, the 20-day EMA.

COMMODITIES

MNI AMERICAS OIL: Americas End of Day Oil Summary: Crude Rises

Crude prices have recovered much of Friday’s losses after a cautious 137k b/d increase in the OPEC output target from October. The risk of more sanctions on Russian crude after a strike on Ukraine is adding upside pressure. At a meeting yesterday, OPEC+ decided to start to unwind the new 1.66mb/d layer of halted oil production, which was scheduled to be in place until end-2026. Unwinding further cuts will depend on “evolving market conditions”.

- The OPEC+ decision to start gradually unwinding the 1.65mb/d cuts reflects the low OECD commercial stocks, according to Goldman Sachs cited by Reuters.

- A preliminary Reuters poll showed on Monday that US crude oil inventories fell by about 3 million barrels in the week to September 5. Analysts estimated distillate inventories decreased by about 1 million barrels last week, while gasoline stocks rose by about 1.2 million barrels. Refinery utilization was estimated to be down 0.9% from 94.3% of total capacity in the previous week.

- WTI Oct futures were up 0.6% at $62.25

- WTI Nov futures were up 0.7% at $61.88

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 09/09/2025 | 0645/0845 | * | Industrial Production | |

| 09/09/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 09/09/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 09/09/2025 | 1150/1350 | SNB's Schlegel at BIS fireside chat | ||

| 09/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 09/09/2025 | 1515/1615 | BOE Breeden Moderates BIS Fireside Chat | ||

| 09/09/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 10/09/2025 | 0130/0930 | *** | CPI | |

| 10/09/2025 | 0130/0930 | *** | Producer Price Index |