MNI ASIA MARKETS ANALYSIS: Tsy Ylds Rise W/US$ Ahead FOMC

HIGHLIGHTS

- Treasuries are holding modestly weaker levels late Monday, narrow ranges since unwinding overnight support, focus on Wednesday's FOMC policy annc - not to mention Friday's employment data for July.

- Two-way positioning also noted in SOFR & Treasury options as derivatives desks adjusted to marginal gains in projected rate cuts by year end.

- EUR sank sharply against all others in G10 Monday, swiftly reversing the opening bid on the back of the EU-US trade deal headlines.

US TSYS

US TSYS: Holding Weaker Levels/Narrow Ranges Ahead Wednesday's FOMC

- Treasuries are holding modestly weaker levels/narrow ranges since midmorning, curves bear steepening (2s10s +2.376 at 48.412) ahead of Wednesday's widely expected steady FOMC rate announcement.

- It’s virtually unanimous that there will be two dissents in favor of a cut at this meeting, with Gov Waller widely expected to do so and Gov Bowman also likely (among analysts who expressed an opinion on this).

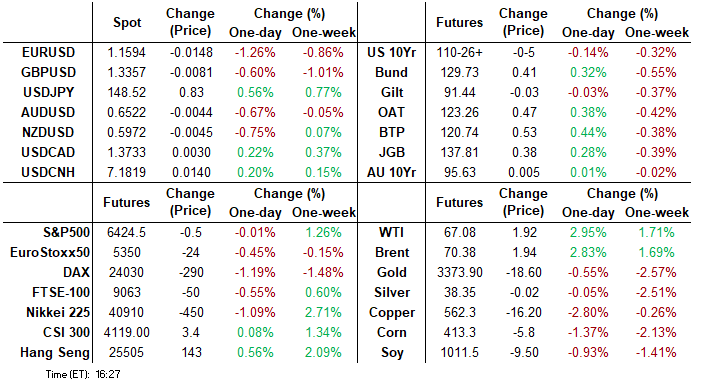

- Projected rate cut pricing gained slightly vs. early morning (*) levels: Jul'25 at -0.8bp (-0.05bp), Sep'25 at -17.4bp (-16.7bp), Oct'25 at -28.2bp (-27.6bp), Dec'25 at -44.5bp (-43.6bp). Year end projection well off early July level of appr -65.0bp.

- Currently, the Sep'25 10Y contract trades -5 at 110-26.5 (110-24.5 low). Key support to watch is 110-08+, the Jul 14 and 16 low. Clearance of this support would reinstate a bearish theme. First support is at 110-19+, the Jul 24 low.

- EUR sank sharply against all others in G10 Monday, swiftly reversing the opening bid on the back of the EU-US trade deal headlines. Bbg's US$ index looks to finish near late session highs: BBDXY +9.42 at 1209.99.

- Stock earnings resume after the close with the following reporting: Woodward Inc, Whirlpool Corp, Waste Management, Brown & Brown, Cadence Design Systems, Beyond Inc, Universal Health Services, Nucor Corp, Welltower Inc and The Western Union Co.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.36% (+0.06), volume: $2.766T

- Broad General Collateral Rate (BGCR): 4.35% (+0.06), volume: $1.144T

- Tri-Party General Collateral Rate (TCR): 4.35% (+0.06), volume: $1.110T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $114B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $266B

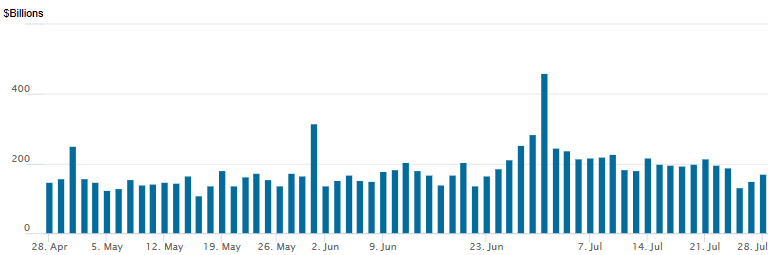

FED Reverse Repo Operation

RRP usage rises to $170.463B this afternoon from $150.509B last Friday, total number of counterparties at 42. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to July 1: $460.731B highest usage since December 31.

US SOFR/TREASURY OPTION SUMMARY

Option desks reported decent SOFR & Treasury option volume Monday, mixed/two-way flow ahead of Wednesday's FOMC rate announcement. Despite weaker underlying futures - projected rate cut pricing gained slightly vs. early morning (*) levels: Jul'25 at -0.8bp (-0.05bp), Sep'25 at -17.4bp (-16.7bp), Oct'25 at -28.2bp (-27.6bp), Dec'25 at -44.5bp (-43.6bp). Year end projection well off early July level of appr -65.0bp

SOFR Options:

+3,000 0QU5 96.62 straddles, 28.0 red 96.665

-30,000 SFRU5 95.37/95.62/95.75 put flys 9.0 vs. 95.83/0.46%

-20,000 SFRZ5 95.25/95.62/96.12 call flys, 6.5

-2,000 0QZ5 96.75 straddles 31.0 over 0QH6 97.12 calls ref 96.75/0.35%

+60,000 SFRV5 96.18/96.43 call spds 4.5 vs. 96.07

-2,000 0QZ5 96.25/96.50/96.75 put trees, 6.5 ref 96.76/0.05%

+2,000 SFRZ5 96.50/0QZ5 97.31 call spds 2.0

+8,000 0QZ5 95.87/96.12/96.37 put flys, 3.0 ref 96.74

-2,000 SFRV5 95.87/96.37 strangles, 8.0 ref 96.065

over +20,000 SFRZ5 95.56/95.68 put spds, 1.0 ref 96.065

+1,000 SFRZ5 96.00/SFRH6 96.25 straddle spds, 15.5

2,000 SFRU6 96.62/97.25 2x1 put spds

2,000 SFRQ5 95.87/96.00/96.12 call flys ref 95.825

Block/screen, 4,000 SFRU5 95.81/95.87/95.93 put flys, 0.75 ref

2,000 SFRH6 96.81/97.06 call spds ref 96.295

3,000 SFRU5 96.75/97.62 strangles ref 96.675

1,000 SFRU5 96.75/97.37 2x1 put spds vs. 97.00/97.62 1x2 call spds

6,000 0QZ5 95.87/96.12/96.37 put flys, 3.0

+1,000 SFRQ5 95.875/96.00/96.12 call flys, 1.5 vs. 95.845/0.10%

+1,000 SFRU5 95.875/96.00/96.12 call flys, 2.75 vs. 95.855/0.08%

Treasury Options:

-5,000 TYU5 111 straddles, 118 appr iv 5.47% (exp 8/22)

+16,000 wk1 US 102.5 puts, 1

4,000 USU5 115/117/118 broken call flys

over 4,600 TYU5 110 puts, 20

over 4,900 TYU5 111 calls, 37

over 4,600 TYV5 109.5 puts, 31 ref 111-01

3,000 TYU5 106.25 puts, 1

+5,000 wk1 TY 111 puts, 22

+5,000 wk1 TY 111 calls, 26

+4,850 TUU5 103.625/104.25 call spds, 7.5-8

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Underperform Bunds After EU-US Trade Pact

EGBs outperformed Gilts Monday as the implications of the EU-US trade pact agreed over the weekend were digested.

- Yields headed lower in early trade on the growth concerns implied by an increased tariff on EU exports to the US and the diminished prospects for EU retaliation on US imports, but the rest of the session saw a pronounced divergence between Gilts and Bunds.

- An MNI Policy sources piece ("MNI SOURCES: Markets Overplaying ECB's Hawkish Shift") boosted EGBs, led by the short end.

- German yields spiked briefly on defence spending headlines, but the move faded as there was nothing new (previously reported in June).

- The German curve bull steepened, with the UK's bear flattening.

- Periphery/semi-core EGB spreads were mostly lower.

- Tuesday's calendar includes UK money supply/consumer credit data, ECB CPI expectations, and Spanish retail sales.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 3bps at 1.918%, 5-Yr is down 3.1bps at 2.267%, 10-Yr is down 2.9bps at 2.689%, and 30-Yr is down 1.1bps at 3.196%.

- UK: The 2-Yr yield is up 2.2bps at 3.906%, 5-Yr is up 1.7bps at 4.075%, 10-Yr is up 1.2bps at 4.647%, and 30-Yr is up 0.5bps at 5.454%.

- Italian BTP spread down 1.7bps at 81.7bps / Spanish down 1.1bps at 58.5bps

MNI OPTIONS: Condors, Ladders, And Spreads Monday

Monday's Europe rates/bond options flow included:

- DUU5 107.10/107.20/107.30/107.40c condor, bought for 2.5 in 3k.

- ERU5 98.06/98.00 put spread sold at 4.75 in 7k

- ERZ5 98.37/98.75cs, bought for 1.5 in 5k

- SFIX5 96.15/96.10/96.05p ladder, bought for flat in 5k (ref 96.30)

MNI FOREX: EUR Seals Worst Session of the Year as Markets See Flaws in EU-US Deal

- EUR sank sharply against all others in G10 Monday, swiftly reversing the opening bid on the back of the EU-US trade deal headlines. The scale of Monday's reversal signals the markets' surprise at the terms of the EU-US trade deal. The 15% export tariff, minimal industry carve-outs and reduction of many tariffs to zero for EU-bound US products have opened the deal up for criticism - particularly in France. This leaves risks to growth larger than the ECB had anticipated, even as the worst case scenario has been avoided.

- Resultantly, cracked through first support with very little difficulty, nearing the 50-dma as the next key level at 1.1564.

- Spillover sales helped trigger GBP and CHF weakness, both of which hit multi-week lows. In GBP/USD, spot is now through the bear trigger at 1.3365, the Jul 16 low, has been cleared. This confirms a resumption of the downleg that started Jul 1. Monday’s moves open 1.3335 initially, the May 20 low. Note that a break of 1.3365 would also confirm a breach of the trendline drawn from the Jan 13 low - cancelling a false break scenario.

- Oil prices fared very well. Both WTI and Brent crude futures rose over 2.5% intraday on the back of Trump cutting the imposed deadline on Russia to halt fighting in Ukraine down to 10-12 days from 50 days previously. This brings forward the threat of secondary sanctions on Russian trade partners - and could further cut off the international energy market from Russian supply. Compounding the market move, Russia proceeded with an export ban on gasoline to ensure domestic supply.

- Firmer oil prices helped contain losses for CAD, NOK against the USD - helping NOK/SEK rally back above the 100-dma in the process.

- Focus Tuesday shifts to ECB inflation expectations data, advance trade balance data, wholesale inventories numbers for June. Meanwhile, the JOLTS jobs openings data will be watched carefully for clues ahead of Friday's NFP print. Central bank speak remains quiet as the Fed remain inside their pre-decision media blackout period.

MNI OPTIONS: Expiries for Jul29 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1425-30(E607mln), $1.1500(E629mln), $1.1540-50(E830mln), $1.1600(E772mln), $1.1650(E1.7bln), $1.1700-20(E1.5bln), $1.1725-45(E2.1bln)

- USD/JPY: Y145.00($1.3bln), Y146.65-70($1.0bln), Y147.50-55($1.1bln), Y147.85-00($757mln)

- EUR/JPY: Y172.50(E706mln)

- AUD/USD: $0.6530-50(A$736mln), $0.6600(A$968mln)

- USD/CAD: C$1.3770($540mln)

MNI US STOCKS: Late Equities Roundup: Tech Stocks Help Nasdaq Outperform Monday

- The tech heavy Nasdaq index is outperforming mildly weaker S&P eminis and the DJIA late Monday, narrow ranges as markets await the next rate announcement by the FOMC this Wednesday.

- Currently, the DJIA trades down 121.95 points (-0.27%) at 44779.7, S&P E-Minis down 10.5 points (-0.16%) at 6414, Nasdaq up 36.3 points (0.2%) at 21145.06.

- A mix of IT, Energy and Consumer Discretionary sector shares led gainers in the second half: Super Micro Computer +7.91%, NIKE +3.91%, Advanced Micro Devices +3.83%, Tesla +3.81%, Diamondback Energy +3.69%, Devon Energy +3.52%, Monolithic Power Systems +3.52%, ON Semiconductor +3.25% and Williams-Sonoma +2.88%.

- On the flipside, Materials, Utilities and Consumer Staples sector share led decliners in late Monday trade: Albemarle -10.35%, Revvity -8.89%, Centene -4.79%, Coinbase Global -3.85%, eBay I-3.48%, Chipotle Mexican Grill -3.21% and Philip Morris International -3.06%.

- Earnings resume after the close with the following reporting: Woodward Inc, Whirlpool Corp, Waste Management, Brown & Brown, Cadence Design Systems, Beyond Inc, Universal Health Services, Nucor Corp, Welltower Inc and The Western Union Co.

MNI EQUITY TECHS: E-MINI S&P: (U5) Bulls Remain In The Driver’s Seat

- RES 4: 6523.63 1.764 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6500.00 Round number resistance

- RES 2: 6477.31 1.618 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6457.75 Intraday high

- PRICE: 6411.00 @ 1507 ET Jul 28

- SUP 1: 6391.50/6302.01 Low Jul 24 / 20-day EMA

- SUP 2: 6241.00 Low Jul 16

- SUP 3: 6153.14 50-day EMA

- SUP 4: 6130.75 Low Jun 25

S&P E-Minis have traded to fresh cycle high today. The climb confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Note that moving average studies are in a bull-mode position highlighting a clear dominant uptrend. Sights are on 6477.31, a Fibonacci projection. Key support is at the 50-day EMA, at 6153.14. Support at the 20-day EMA is at 6302.01.

COMMODITIES

MNI AMERICAS OIL: WTI crude prices have risen after US President Trump announced

July 28 - Americas End-of-Day Oil Summary: WTI crude prices have risen after US President Trump announced a new 10-12 day deadline on Russia to form a peace deal with Ukraine, adding to support from a US-EU trade deal. The near term Brent call volatility has followed the jump in front month future prices in reaction to the increased threat of further US sanctions on Russia.

- The EU reached an agreement with the US for tariffs of 15% except steel & aluminum which still face 50% and aircraft & parts that will have no duty. The EU agreed to buy $750bn of US energy over the remainder of President Trump’s term and invest $600bn in the US.

- Another round of US-China talks took place in Stockholm on Monday with expectations that a tariff truce will be extended, laying the groundwork for a Trump-Xi meeting later this year.

- Trump may be pushing for trade deals ahead of an upcoming Federals appeals court ruling on his authority to use “emergency powers” to impose tariffs, which he could lose, according to trade sources cited by a Fox News reporter.

- WTI Sep futures were up 2.5% at $66.71

- WTI Oct futures were up 2.5% at $65.91

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 29/07/2025 | 0600/0800 | Flash Quarterly GDP Indicator | ||

| 29/07/2025 | 0700/0900 | *** | GDP (p) | |

| 29/07/2025 | 0800/1000 | ** | ECB Consumer Expectations Survey | |

| 29/07/2025 | 0830/0930 | ** | BOE Lending to Individuals | |

| 29/07/2025 | 0830/0930 | ** | BOE M4 | |

| 29/07/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 29/07/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 29/07/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 29/07/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 29/07/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 29/07/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 29/07/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 29/07/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 29/07/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 29/07/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 29/07/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 29/07/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 30/07/2025 | - | Bank of Japan Meeting | ||

| 30/07/2025 | 0130/1130 | *** | CPI inflation | |

| 30/07/2025 | 0130/1130 | *** | CPI Inflation Monthly |