MNI ASIA MARKETS ANALYSIS: Tsy Ylds Gain Ahead July Minutes

HIGHLIGHTS

- Treasury yields gained slightly after a lower Monday open, limited data ahead of Wednesday's July FOMC minutes release and Jackson Hole symposium on Friday.

- Curves reversed mild early steepening, projected rate cut pricing cools on the day, Sep meeting under -25bp at -20.1bp.

- The US dollar has traded with a constructive tone on Monday, initially assisted by softer sentiment for major equity benchmarks.

US TSYS

MNI US TSYS: Holding Mildly Lower, Focus on July FOMC Minutes, Economic Summit

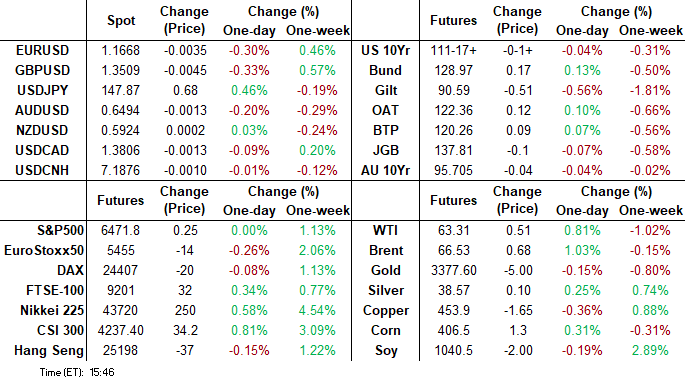

- Still weaker after the bell, Treasury futures are off late morning lows, curves mildly steeper (2s10s +0.281 at 56.614; 5s30s +.479 at 108.512) while projected rate cut pricing retreats slightly vs. early morning levels (*): Sep'25 at -20.9bp (-21.2bp), Oct'25 at -33.6bp (-34.6bp), Dec'25 at -52.9bp (-54.6bp), Jan'26 at -64.1bp (-65.6bp).

- Tsy Sep'25 10Y contract trades -1.5 at 111-17.5 (111-13.5L / 111-27H), volume just over 1.1M -- a fair portion of which driven by Sep/Dec quarterly roll. Key support is 110-08+, the low on Jul 15 and 16. Prices faded into the Monday close, however first support is yet to be tested at 110-23+, the Aug 1 low.

- Limited data: August's NAHB/Wells Fargo Housing Market report showed little improvement in the homebuilding sector, with present sales weakening modestly and selling prospects steady/moderately better. The headline index fell 1 point to 32 - reverting back to June's level which is around post-2022 lows.

- The NY Fed's survey of regional services firms' business leaders showed a deterioration in activity and forward-looking sentiment in August, with inflation pressures remaining prevalent. The current general activity index fell for the first time since March, to -11.7 from -9.3 prior

- Cross asset: stocks flat to mildly weaker (SPX eminis -0.75 at 6470.75; DJIA -30.02 at 44916.1, Nasdaq +4.96 at 21627.75), crude firmer (WTI +.53 at 63.33), Gold weaker (-3.94 at 3332.25). USD index now 0.3% higher on the session as we approach the APAC crossover. Although there has been a flurry of initial headlines from the Trump/Zelenskyy meeting at the White House, few concrete details have been provided regarding the war.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.36% (+0.02), volume: $2.821T

- Broad General Collateral Rate (BGCR): 4.34% (+0.02), volume: $1.163T

- Tri-Party General Collateral Rate (TCR): 4.34% (+0.02), volume: $1.146T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $112B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $240B

FED Reverse Repo Operation

RRP usage inches up to $38.240B this afternoon from $33.757B Friday, total number of counterparties at 19. Compares to last Thursday's lowest usage of the year at $28.818B on Wednesday, April 16 -- in turn the lowest level since April 2021.

US SOFR/TREASURY OPTION SUMMARY

With few exceptions (26k FVU5 put fly) Monday's option flow revolved around upside SOFR & Tsy calls, the latter likely consolidating ahead of Friday's Sep expiry. Projected rate cut pricing cooled slightly vs. morning (*) levels: Sep'25 at -20.9bp (-21.2bp), Oct'25 at -33.6bp (-34.6bp), Dec'25 at -52.9bp (-54.6bp), Jan'26 at -64.1bp (-65.6bp).

SOFR Options:

Block/screen over +145,000 SFRU5 96.50 calls, 3.0-3.25

2,000 SFRU5 95.68/95.75/95.81/95.87 put condors ref 95.9025

1,500 0QH6 97.12/97.25 call spds ref 96.93

1,775 SFRM6 97.00/97.25 call spds ref 96.67

5,000 SFRU5 95.75/95.81 put spds

1,500 SFRU5 96.12 calls, ref 95.9025

1,200 SFRZ5 96.25/96.37/96.50/96.62 call condors

2,000 SFRZ5 95.87/96.00/96.12 call flys, ref 96.22

Block/screen, +21,000 SFRU5 96.00/96.12/96.25 call flys, 0.75 ref 95.90

Treasury Options: (Sep'25 options expire Friday)

-26,968 FVU5 107.5/108.25/109 put flys, 21.5 ref 108-20.5

+40,000 TYU5 112.5 calls, 2, total volume over 52,700

4,000 FVU5 107.75/108/108.5 2x3x1 put flys

+30,000 FVU5 109.25 calls, 2

1,650 FVX 110.25/FVZ5 110 call spds

3,000 wk5 TU 104.12/104.37/104.62 call flys ref 104-02.5

MNI BONDS: EGBs-GILTS CASH CLOSE: Bunds Regain Ground But Gilt Sell-Off Continues

Gilts underperformed global peers to start the week.

- After strengthening in preliminary trade, in a partial reversal of Friday's sell-off, EGB and Gilt yields bottomed around 9am London time and moved steadily higher for most of the rest of the session.

- The Gilt sell-off in late afternoon stood out. While there was no particular identifiable trigger, a Guardian report that the government was considering adjustments to property taxes served as a reminder of UK fiscal woes which will be increasingly focused upon ahead of the Autumn budget.

- Additionally, anticipation of Wednesday's UK CPI report may have dampened sentiment.

- 10Y Gilt yields hit the highest levels since May, with futures piercing support at Friday's lows.

- The UK curve bear steepened, in contrast to the rally across the German curve. Periphery / semi-core EGB spreads closed little changed.

- Tuesday's fairly thin schedule includes Eurozone current account data. There will also be attention paid to a video conference of EU member state leaders (1300CET) to discuss the US-Ukraine situation.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.4bps at 1.959%, 5-Yr is down 2.1bps at 2.319%, 10-Yr is down 2.5bps at 2.763%, and 30-Yr is down 1.2bps at 3.338%.

- UK: The 2-Yr yield is up 3.2bps at 3.965%, 5-Yr is up 3.3bps at 4.123%, 10-Yr is up 4.2bps at 4.738%, and 30-Yr is up 4.7bps at 5.611%.

- Italian BTP spread down 0.8bps at 79.3bps / French OAT up 0.3bps at 68.4bps

MNI OPTIONS: Large Euribor Put Spread Sales, Outright Call Buying Stand Out Monday

Monday's Europe rates/bond options flow included:

- DUU5 107.00/107.10/107.20 call fly paper paid 3.00-3.25 on 4.5K

- OEU5 117.50/117.25ps 1x2, traded for -10 in 4k

- RXU5 127 puts, paper pays 2.0 in 3.625k

- ERZ5 98.50 calls paper paid 0.75 on another 10K

- 0RU5 98.25/00 2x3.5 put spread 2K given at 27.0 (4K x 7K)

- SFIX5 96.20/96.15/96.05 put ladder Vs. SFIZ5 96.00 puts paper paid 0.75 for the put ladder on 2.25K

- SFIZ5 96.40/96.65/96.90 call fly, sold for 1.25 in 2k (suggested liquidation)

- SFIH6 96.60/70 call spread vs. 96.25/15 put spread paper paid -1.50 (vs. 34) for the call spread on 5K

MNI FOREX: US Dollar Edges Higher amid Trump/Zelenskyy White House Meeting

- The US dollar has traded with a constructive tone on Monday, initially assisted by softer sentiment for major equity benchmarks, and US yields turning higher across the US session then providing further support. The USD index now 0.3% higher on the session as we approach the APAC crossover. Although there has been a flurry of initial headlines from the Trump/Zelenskyy meeting at the White House, few concrete details have been provided regarding the war, with President Trump stating there is a possibility something could come out of Russia talks.

- The uptick for US yields provided a supportive backdrop for USDJPY, which briefly rose to an intra-day high of 147.99, which marks a post US PPI high for the pair. Above here, firm resistance to watch is at 148.52, the Aug 12 high, of which a breach would be viewed as a S/T bull signal.

- In similar vein, the likes of EUR and GBP have also traded with an offered tone. For EURUSD, while moves have remained shallow, spot has been consistently grinding towards last Thursday's pullback low at 1.1631, while firm support is seen at 1.1583, the 50-day EMA.

- The dollar’s focus this week will be on the Fed’s Jackson Hole Symposium, which kicks off Thursday and includes the keynote speech by Chair Powell on Friday. Attention will mostly be on any nod to a potential September cut, but a large portion of his comments will touch on the findings from the Fed's policy framework review.

- Canadian CPI is scheduled Tuesday, which will be very closely eyed given stronger-than-expected core price momentum in Q2 and an upside surprise would place the technical focus for USDCAD on both the 20- and 50-day exponential moving average supports, located around 1.3760. A clear break would resume the correction off the early August high at 1.3879, signalling scope for a move back to 1.3576, the Jul 23 low.

MNI FX OPTIONS: Expiries for Aug19 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E731mln), $1.1620-25(E2.3bln), $1.1650-65(E682mln), $1.1700(E1.3bln)

- USD/JPY: Y148.30-35($709mln)

- AUD/USD: $0.6515(A$745mln)

- USD/CAD: C$1.3750-70($646mln)

MNI US STOCKS: Late Equities Roundup: Holding Weaker, DJIA Underperforming

- US Stocks remain mildly weaker, holding narrow ranges late Monday as the week's event risk sidelines investors. Focus is on Wednesday's July FOMC minutes release and the annual economic symposium in Jackson Hole, Wy that officially kicks off Friday morning.

- Currently the DJIA trades down 40.35 points (-0.09%) at 44905.68, S&P E-Minis down 3 points (-0.05%) at 6468.5, Nasdaq down 0.7 points (0%) at 21622.13.

- Consumer Discretionary, Staples and Industrials sectors lead late session gainers, while individual stocks are more varied with IT services leading: Dayforce +28.65%, Paycom Software +3.4%, EPAM Systems +4.31%, Trade Desk +5.41%.

- Other leading stocks included First Solar +10.44%, Enphase Energy +3.93%, Royal Caribbean Cruises +4.61% Lululemon Athletica +3.93% and Axon Enterprises +4.56%.

- Conversely, oil & gas stocks underperformed EQT -4.9%, Coterra Energy -3.06%, Expand Energy -2.02%, Baxter Int -2.13%; followed by large cap tech stocks: Electronic Arts -3.26%, Intel -2.67%, Meta Platforms -2.35% and Palantir Technologies -2.22%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Trend Needle Points North

- RES 4: 6600.00 Round number resistance

- RES 3: 6543.43 2.0% 10-dma envelope

- RES 2: 6523.63 1.764 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6508.75 High Aug 15 and Alltime High

- PRICE: 6469.50 @ 1505ET Aug 18

- SUP 1: 6392.29 20-day EMA

- SUP 2: 6313.25 Low Aug 6

- SUP 3: 6267.88 50-day EMA

- SUP 4: 6239.50 Low Aug 1

The dominant uptrend in S&P E-Minis remains intact and the contract is trading at its recent highs. Moving average studies are in a bull-mode position, highlighting a clear uptrend. A resumption of gains would pave the way for a climb towards 6523.63, a Fibonacci projection. On the downside, supports to watch are; 6392.29, the 20-day EMA, and 6267.88, the 50-day EMA.

COMMODITIES

MNI AMERICAS OIL: US End of Day Oil Summary: Crude Rises

Crude prices have gained ground today, as the market digests how the Trump-Zelenskiy meeting and later the Putin-Trump call will alter the outlook for a peace deal or ceasefire in Ukraine.

- WTI SEP 25 up 1% at 63.41$/bbl

- Trump called security guarantees for Ukraine important for getting a deal done. He also said that a ceasefire is not necessary for a peace deal, a position the Russian side also takes.

- Trump said that he would call Putin after the meeting and if all went well a trilateral meeting would take place. POTUS added that if a trilateral dialogue takes place, “there would be a good chance the war ends.”

- Trump said he would hold off on raising tariffs on China for buying Russian fuel following the talks with Putin.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 19/08/2025 | 0800/1000 | ** | EZ Current Account | |

| 19/08/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 19/08/2025 | 1230/0830 | *** | CPI | |

| 19/08/2025 | 1230/0830 | *** | Housing Starts | |

| 19/08/2025 | 1230/0830 | *** | Housing Starts | |

| 19/08/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 19/08/2025 | 1810/1410 | Fed Vice Chair Michelle Bowman | ||

| 20/08/2025 | - | Reserve Bank of New Zealand Meeting | ||

| 20/08/2025 | 2301/0001 | * | Brightmine pay deals for whole economy | |

| 20/08/2025 | 2350/0850 | * | Machinery orders | |

| 20/08/2025 | 0200/1400 | *** | RBNZ official cash rate decision |