MNI ASIA MARKETS ANALYSIS: Tsy Curves Twist Steeper Late

HIGHLIGHTS

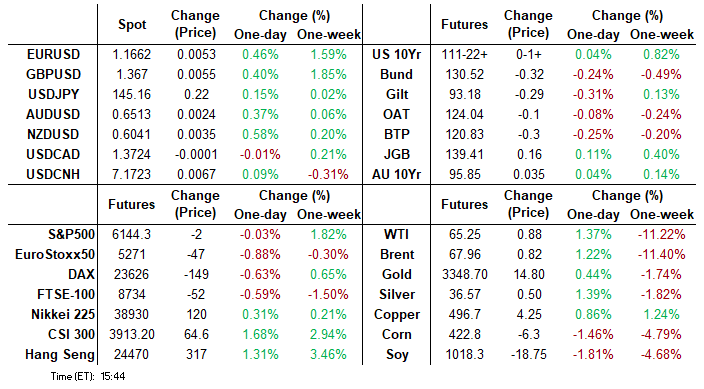

- Treasuries climbed off midmorning lows, curves twisted steeper by the close (2s10s +4.186 at 50.911) late support after Fed SLR proposal to ease rules for large banks.

- After clinging to near steady at midday, the dollar index withdrew in the second half, nearing the prior session's 1W low (BBDXY -2.29 at 1199.24).

- Heavy data tomorrow: weekly claims, GDP, Personal Consumption, Pending Home Sales, followed by several scheduled Fed speakers.

US TSYS

MNI US TSYS: Treasury Curves Twist Steeper, Fed SLR Proposal Eases Bank Rules

- Treasury futures gradually climbed off midmorning lows after the bell, curves twisting steeper (2s10s +4.186 at 50.911) after the Fed SLR proposal to ease rules for large banks.

- Projected rate cut pricing gains slightly vs. early morning levels (*): Jul'25 at -6.2bp (-5.2bp), Sep'25 at -27.1bp (-25.8bp), Oct'25 at -42.7bp (-41.2bp), Dec'25 at -60.9bp (-59.7bp).

- Near the top end of a narrow session range, the Tsy Sep'25 10Y contract trades +2 at 111-23 (111-11.5L / 111-24H), volume just over 1.1M, 10Y yield -.0078 at 4.2867%. Key resistance remains above the intraday high of 111-24 at 111-30/31.5 (76.4% of May 1-22 downleg / 1.0% 10-dma envelope.)

- New home sales fell to an 18-month low in May, with the 13.7% M/M drop to 623k (seasonally-adjusted, annual rate) adding to evidence that overall US housing market activity is deteriorating.

- Cross asset: stocks flat to mixed (SPX eminis +1.75 at 6148.0; DJIA -101.5 at 42987.5, Nasdaq +48.77 at 19961.30), crude firmer after two day rout (WTI +.75 at 65.12), Gold firmer (+10.34 at 3334.01). After clinging to near steady at midday, the dollar index withdrew in the second half, nearing the prior session's 1W low (BBDXY -2.29 at 1199.24). Despite yesterday’s pullback, EURJPY has recovered strongly on Wednesday, rising 0.55% and back above 169.25.

- Heavy data tomorrow: weekly claims, GDP, Personal Consumption, Pending Home Sales, followed by several scheduled Fed speakers.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.30% (+0.01), volume: $2.733T

- Broad General Collateral Rate (BGCR): 4.28% (+0.01), volume: $1.088T

- Tri-Party General Collateral Rate (TCR): 4.28% (+0.01), volume: $1.066T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $115B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $293B

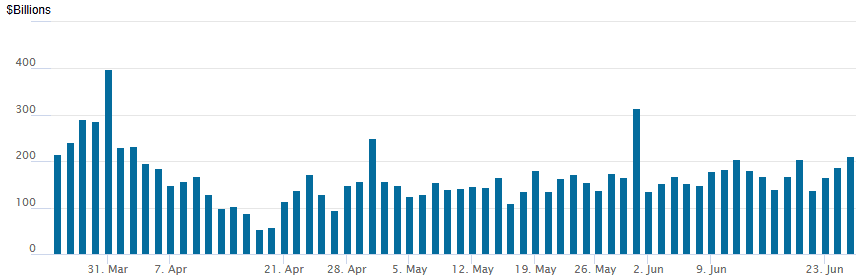

FED Reverse Repo Operation

RRP usage rises to $210.879B this afternoon from $187.367B yesterday, total number of counterparties at 35. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options trade remained relatively mixed compared to better upside SOFR calls the last couple sessions. Underlying futures off lows, curves twisting steeper (2s10s +4.186 at 50.911) while projected rate cut pricing gains slightly vs. early morning levels (*): Jul'25 at -6.2bp (-5.2bp), Sep'25 at -27.1bp (-25.8bp), Oct'25 at -42.7bp (-41.2bp), Dec'25 at -60.9bp (-59.7bp).

SOFR Options:

+2,000 SFRH7/SFRM7 99.00/99.75 call spd strip, 8.5

Block, -7,000 SFRV5 95.75/96.00/96.12 broken put trees, 4.25

+8,000 SFRZ5 95.37 puts, 0.5

-2,500 SFRU5 95.75/95.93/96.12 call flys, 5.5 ref 95.96

2,000 0QN5/0QQ5 96.50/96.75/97.12 broken call fly spd

+10,000 0QV5 97.43/98.00 call spds, 5.5

-10,000 SFRZ5 95.37/95.62 put spds, 0.5

2,000 0QU5 96.00/97.00 2x3 call spds ref 96.815

Block, 2,500 2QN5 96.68/96.93/97.18 call flys, 0.75 ref 96.775

2,500 0QN5 97.12/97.18 call spds vs. 96.12/96.37 put spds ref 96.82

2,000 SFRH6 98.50 calls, 2.5

2,000 SFRZ5 95.68/SFRU6 96.12 put spds

+2,000 SFRQ5 95.93/96.06 call spds, 4.0 vs. 95.965/0.17%

3,200 SFRU5 95.62/95.75 put spds, 2.5 ref 95.96

Treasury Options:

4,000 USQ5 103/106/108 2x1x1 broken put trees

-5,000 TYQ5 111.5 straddles 131-130 ref 111-16

-8,000 TYQ5 110.25/112.75 strangles, 36 ref 111-16

+10,000 TYQ5 108.5 puts, 4

-5,000 TYU5 115.5 calls, 10

8,500 TUQ5 105/106.5 1x2 call spds ref 103-27.75

+1,700 TYQ5 108/109.5 2x1 put spds, 3 ref 111-19.5

+5,000 TYU5 107/108 put spds, 4 ref 111-14/0.04%

+1,500 TYQ5 112.5/114.5 call spds, 21 vs. 111-21/0.23%

1,370 wk4 TU 103.62/103.75/103.87/104 call condors, exp 6/27

4,300 TYQ5 113 calls ref 111-23.5

3,000 TYQ5 111.5 calls

MNI BONDS: EGBs-GILTS CASH CLOSE: Twist Steepening After Early Rally Fades

European curves lightly twist steepened Wednesday.

- Yields looked headed lower in early trade, with no clear headline driver though seemingly continuing the bullish global bond move from Tuesday's close.

- The rally lost steam however, and yields steadily edged higher throughout the session from around 9am London time.

- Various factors contributing to the reversal included a soft 15Y Gilt auction as well as some fiscal headlines surrounding European countries increasing defence spending amid the NATO summit, and related US threats to increase tariffs on Spain.

- Gilts outperformed Bunds, with twist steepening in both the UK and German curves.

- Periphery/semi-core EGB performance was mixed, with OATs leading gains.

- Thursday's schedule includes appearances by BOE's Bailey and Breeden and ECB's Schnabel, Guidos and Lagarde, along with German GfK consumer confidence and UK CPI data.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.8bps at 1.843%, 5-Yr is up 1.1bps at 2.142%, 10-Yr is up 2.2bps at 2.565%, and 30-Yr is up 2.6bps at 3.052%.

- UK: The 2-Yr yield is down 1.6bps at 3.856%, 5-Yr is down 1.2bps at 3.979%, 10-Yr is up 0.8bps at 4.481%, and 30-Yr is up 2.3bps at 5.231%.

- Italian BTP spread down 0.6bps at 91.3bps / French OAT down 1.6bps at 69.6bps

MNI EGB OPTIONS: Dovish Euribor Skew Persists, With Sonia Activity Picking Up

Wednesday's Europe rates/bond options flow included:

- ERQ5 98.1875/98.3125/98.4375 call fly 8K sold down to 1

- ERZ5 98.25c vs 2RZ5 98.0625c, bought the front for -1 in 15k

- ERZ5 98.125/98.25/98.375c fly x2 with ERZ5 98.375/98.50/98.625c fly vs 0RV5 98.0625p x1, bought the Flies strip for -0.5 in 8k

- ERZ5 98.375/98.50/98.625 call fly paper paid 1.5 on 5K.

- ERH6 98.125/98.25/98.50/98.625 c condor vs 97.9375p, bought for 1 in 5k

- SFIU5 95.90/96.00/96.15/96.25c condor, sold at 6.25 in 10.5k

- SFIU5 96.20/96.40 1x2 call spread paper paid 1.25 on 3K

- SFIX5 96.60/96.70cs, bought for 1.5 in 8k

- SFIZ5 96.10/96.25/96.40/96.55c condor, bought for 6 up to 6.25 in 30k

MNI FOREX: JPY Weakness Stands Out in Relatively Subdued Session

- After clinging to near steady at midday, the dollar index withdrew in the second half, nearing the prior session's 1W low (BBDXY -2.29 at 1199.24).

- Despite yesterday’s pullback, EURJPY has recovered strongly on Wednesday, rising 0.55% and back above 169.25. The rally from the June lows totals ~4%, with Monday’s cycle highs immediately coming back into focus at 169.71. Price action continues to erode the steep declines seen in July last year, bolstering the technically bullish theme. Scope is seen for a climb towards 170.47, a key Fibonacci retracement point.

- Australian monthly CPI came in lower-than-expected, potentially calling into question the RBA's next decision on rates. Despite this, AUDUSD has firmed off the lows and is holding the bulk of the recovery off Monday's 0.6373. This price actions favours this week's weakness as a false break below the bottom-end of the multi-month trend channel, and a reversion higher here would make 0.6552, the June 16 high and bull trigger, the primary upside target.

- USDCHF remains just above cycle lows printed yesterday at 0.8035 after the solid franc outperformance posted from the beginning of the week. Having initially benefited from haven flows on the exchange of fire between Israel and Iran, the CHF has held the rally, keeping a test of 0.8000 on the cards.

- The US data calendar is busier on Thursday, with the 3rd read of Q1 GDP, jobless claims and durable goods figures scheduled. Focus will then turn to Friday’s May PCE report.

MNI OPTIONS: Expiries for Jun26 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E5.1bln), $1.1625(E1.2bln), $1.1640-50(E907mln), $1.1700(E3.2bln)

- USD/JPY: Y142.00($1.3bln), Y143.00($1.4bln), Y147.00($782mln)

- AUD/USD: $0.6500(A$2.4bln)

- NZD/USD: $0.6040(N$522mln)

- USD/CAD: C$1.3715-35($1.7bln), C$1.3800($2.0bln)

MNI US STOCKS: Late Equities Roundup: Chip-Makers Buoy Tech Sector

- Stocks continue to scale off early Wednesday highs, the tech-heavy Nasdaq still outperforming in late trade. Currently, the DJIA trades down 167.8 points (-0.39%) at 42921.04, S&P E-Minis down 7 points (-0.11%) at 6139.25, Nasdaq up 22.6 points (0.1%) at 19935.0.

- Information Technology and Communication Services sectors continued to outperform in the second half, semiconductor makers supporting the tech sector: Super Micro Computer +7.89%, NVIDIA +3.96% and Advanced Micro Devices +3.24%.

- Interactive media and entertainment shares supported the Communication Services sector: Alphabet +2.18%, News Corp +0.65% and Fox +0.55%.

- Meanwhile, Consumer Discretionary and Consumer Staples sectors underperformed late, auto-makers and travel stocks weighing on the former: Tesla -5.10%, Caesars Entertainment -4.05%, Norwegian Cruise Line Holdings -2.42% CarMax -2.30% and Ford Motor -2.28%.

- Lagging Consumer Staples shares included: General Mills -4.77%, Conagra Brands -4.24%, Hershey Co -2.59%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Northbound

- RES 4: 6249.00 High Feb 21

- RES 3: 6200.00 1.50 proj of the Apr 7 - 10 - 21 price swing

- RES 2: 6172.50 High Feb 24

- RES 1: 6157.75 Intraday high

- PRICE: 6141.50 @ 1335 BST Jun 25

- SUP 1: 5959.00/5922.67 Low Jun 23 / 50-day EMA

- SUP 2: 5811.50 Low May 23

- SUP 3: 5645.75 Low May 7

- SUP 4: 5500.00 Low Apr 30

The trend condition in S&P E-Minis is unchanged, it remains bullish and this week’s fresh cycle high reinforces current conditions. Short-term resistance and a bull trigger at 6128.75, the Jun 11 high, has been breached. The clear break confirms a resumption of the uptrend that started Apr 7. Sights are on the 6200.00 handle, a Fibonacci projection. Key support remains at the 50-day EMA - at 5922.67. A clear break of it would signal a reversal.

MNI COMMODITIES: Crude Stabilises, Gold Steady, Bullish Outlook For Copper

- Oil markets have stabilised on Wednesday after falling sharply over the previous two days following the de-escalation of the Iran-Israel conflict, with the ceasefire holding so far. This has allowed the geopolitical risk premium to decline.

- WTI Aug 25 is up by 0.9% at $64.9/bbl.

- OPEC meets virtually on July 6 to decide August’s production target. Another increase is likely as the group normalises output, targeting market share and punishing overproducing members.

- For WTI futures, support to watch is at the 50-day EMA, at $64.53, which has been pierced. A clear break of it would signal scope for a deeper retracement, exposing $58.87, the May 30 low.

- On the upside, initial resistance to watch is $71.20, the 50.0% retracement of the Jun 23 - 24 high-low range.

- Meanwhile, spot gold has been rangebound today, with the yellow metal 0.2% higher at $3,330/oz.

- A bullish theme in gold remains intact and the recent pullback is considered corrective - for now. Resistance at $3,435.6, the May 7 high, has recently been pierced. Initial key support to monitor is $3,289.2, the 50-day EMA.

- Elsewhere, copper has risen by 0.7% to $496/lb.

- Yesterday’s gains saw copper pierce $502.70, the Apr 23 high, undermining the recent bearish theme and signalling scope for an extension higher near-term. This has opened $514.43, a Fibonacci retracement.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 26/06/2025 | 0600/0800 | * | GFK Consumer Climate | |

| 26/06/2025 | 0700/0900 | ** | Economic Tendency Indicator | |

| 26/06/2025 | 0830/0930 | BOE Breeden On UK Competetiveness Panel | ||

| 26/06/2025 | 0945/1145 | ECB De Guindos At Deutsch Bank Forum 2025 | ||

| 26/06/2025 | 0945/1045 | BOE Greene Chairs Panel On MonPol Communication | ||

| 26/06/2025 | 1000/1100 | ** | CBI Distributive Trades | |

| 26/06/2025 | 1100/1300 | ECB Schnabel At 'Wirtschaftsrat der CDU' Finanzmarktklausur | ||

| 26/06/2025 | 1100/1200 | BOE Bailey Keynote Speech At BCC Conference | ||

| 26/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 26/06/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 26/06/2025 | 1230/0830 | * | Payroll employment | |

| 26/06/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 26/06/2025 | 1230/0830 | *** | GDP | |

| 26/06/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 26/06/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 26/06/2025 | 1245/0845 | Richmond Fed's Tom Barkin | ||

| 26/06/2025 | 1300/0900 | Cleveland Fed's Beth Hammack | ||

| 26/06/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 26/06/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 26/06/2025 | 1430/1530 | BOE Lombardelli Chairs Panel On Communicating Uncertainty | ||

| 26/06/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 26/06/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 26/06/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 26/06/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 26/06/2025 | 1700/1300 | * | US Treasury Auction Result for Cash Management Bill | |

| 26/06/2025 | 1715/1315 | Fed Governor Michael Barr | ||

| 26/06/2025 | 1830/2030 | ECB Lagarde Opening Speech at Münchner Opernfestspiele | ||

| 26/06/2025 | 1900/1500 | *** | Mexico Interest Rate | |

| 27/06/2025 | 2330/0830 | * | Labor Force Survey | |

| 27/06/2025 | 2330/0830 | ** | Tokyo CPI | |

| 27/06/2025 | 2350/0850 | * | Retail Sales (p) |