MNI ASIA MARKETS ANALYSIS: Trump Wants Fed Majority

HIGHLIGHTS

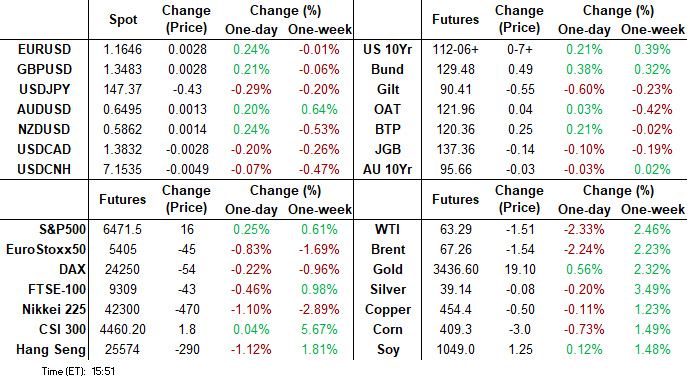

- Treasuries drifted higher in 2s-10s Tuesday, curves twisting steeper (2s10s +2.75 at 57.695) with bonds weaker all day, the US$ and stocks holding narrow range on rather quiet late summer trade.

- Markets continued to digest Trump's unprecedented "firing" of Fed Gov Cook late Monday, projected rate cuts rising as Trump works toward a majority on the Fed Board in the near term.

- Treasury futures had pared gains briefly after higher than expected Durable/Cap Goods Orders, Philadelphia Fed Non-Mfg Activity declines.

US TSYS

MNI US TSYS: Fed Board Majority Goal Sees Tsy Curves Twist Steeper

- Treasuries look to finish mixed Tuesday, curves twisting steeper (2s10s +2.75 at 57.695; 5s30s +6.248 at 116.532) with 2s-10s near late session highs vs. weaker Bonds.

- Markets continued to digest Trump's unprecedented "firing" of Fed Gov Cook late Monday, projected rate cuts rising as Trump works toward a majority on the Fed Board in the near term. The Fed responded that Fed Govs can only be removed "for cause" while Cook moves to challenge the decision in court.

- The dollar dips slightly as President Trump appears to suggest in a cabinet meeting press conference that the administration could nominate Stephen Miran to "fired" Governor Cook's Board position (expiring in 2038), instead of ex-Gov Kugler's vacant spot (whose term ends in January before requiring renewal).

- Treasury futures had pared gains briefly after higher than expected Durable/Cap Goods Orders, Philadelphia Fed Non-Mfg Activity declines. Headline durable goods orders bested expectations at -2.8% M/M (-3.8% expected, -9.4% prior), weighed down once again by the extremely volatile nondefense aircraft orders category (-33% M/M, after -53% prior).

- Meanwhile, core shipments continued to hum along, rising by a 27-month high 0.7% M/M (0.2% expected, 0.4% prior rev from 0.3%).

- Heavy futures volumes (Sep'25 5s &10s near 3.5-4M) tied to Sep-Dec rolling ahead of Friday's "first notice" when Dec'25 will take the lead quarterly position. Light data ahead on Wednesday with MBA Mortgage Applications.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.37% (+0.01), volume: $2.825T

- Broad General Collateral Rate (BGCR): 4.35% (+0.00), volume: $1.153T

- Tri-Party General Collateral Rate (TCR): 4.35% (+0.00), volume: $1.121T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $113B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $236B

FED Reverse Repo Operation

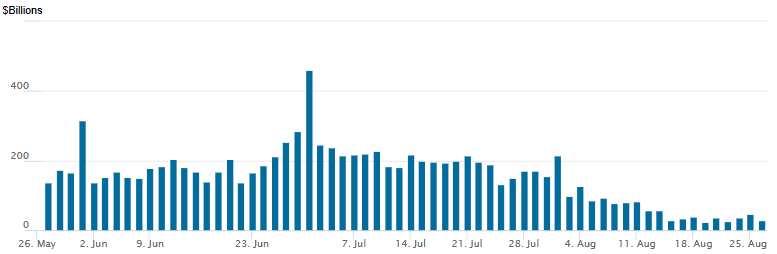

RRP usage retreats to $28.574B this afternoon from $47.567B yesterday -- compares to $22.344B on Tuesday, Aug 19 - lowest since April 5, 2021. Total number of counterparties at 16. This year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options seeing mixed/two-way flow carry over from overnight, lighter volumes so far as markets continue to digest the unprecedented firing of Fed Gov Cook by Pres Trump. Underlying futures mixed, curves twist steeper with short end outperforming weaker bonds. Projected rate cuts gain slightly vs. late Monday (*) levels: Sep'25 at -21.6bp (-20.8bp), Oct'25 at -33.6bp (-33.2bp), Dec'25 at -53.9bp (-52.9bp), Jan'26 at -67.6bp (-65.6bp).

SOFR Options:

+6,000 SFRZ6 96.50/97.50 call over risk reversals, 4.5

-10,000 SFRX5 96.00 puts, 0.5 over 96.31/96.43 call spds ref 96.215

+4,000 0QV5 95.62 puts. 1.5 vs. 96.96/0.10%

+3,000 SFRZ5 96.00/96.12/96.25/96.37 call condors, 4.25 ref 96.21

+1,000 SFRZ5 96.25 straddles, 29.75-30.0 ref 96.21

+5,000 SFRV5 96.06/96.12/96.18 call flys, 1.0 vs. 96.19/0.05%

4,000 SFRU5 95.68/96.25 strangle, 0.5 ref 95.8825

2,500 SFRU5 96.00/96.12 call spds, 0.75

Treasury Options:

+2,500 USV5 118 calls, 13 vs.113-28 to -25/0.06%

-2,000 TYV5 112/113.5 1x2 call spds, 15 vs. 111-28.5 to -29/0.14%

-6,000 FVV5 108.25/108.75 put spds, 9.5 vs. 109-03.5/0.16%

+2,500 TYZ5 111.5 puts, 63 vs. 111-26/0.44%

+2,000 TYV5 110/112 put 2x1 put spds, 31 vs. 111-30/0.32%

-1,000 USV5 112.5 puts, 56 vs. 114-23/0.36%

-2,000 TYV5 110/114 call over risk reversals, 3 vs. 112-00/0.30%

MNI BONDS: EGBs-GILTS CASH CLOSE: OAT/Bund Spread Continues To Widen On Politics

OATs remained under pressure Tuesday as political risk concerns remained prevalent.

- The OAT/Bund spread widening initiated Monday by PM Bayrou's call for a confidence on his own government (to be held Sep 8) continued, with speculation that President Macron could have to call another set of legislative elections.

- French yields actually closed lower on the day, but the 10Y yield touched its highest level (3.534%) since March before recovering. 10Y OAT/Bund closed at 77.3bp, the widest since April 11 and up over 7bp this week.

- Elsewhere, French consumer confidence came in on the weak side, while BOE's Mann in a speech appeared to rule out any further rate cuts in the short-term.

- The German curve bull steepened, with the UK's bear steepening (the underperformance in cash being due to a catch-up from bank holiday market closure). Periphery EGB spreads widened modestly.

- Wednesday's schedule is on the light side, with German GfK consumer confidence and UK CBI Sales data, with main focus remaining on flash August Eurozone inflation later in the week.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 3.7bps at 1.938%, 5-Yr is down 4.7bps at 2.268%, 10-Yr is down 3.4bps at 2.723%, and 30-Yr is down 1.2bps at 3.32%.

- UK: The 2-Yr yield is up 2.4bps at 3.968%, 5-Yr is up 3.8bps at 4.139%, 10-Yr is up 4.7bps at 4.74%, and 30-Yr is up 6bps at 5.608%.

- Italian BTP spread down 0.5bps at 83.3bps / French OAT up 5.1bps at 77.3bps

MNI OPTIONS: Mixed Post-UK Holiday Trade In Sonia Call Structures

Tuesday's Europe rates/bond options flow included:

- DUV5 107.30/107.50cs 1x2, bought for 1 in 1k

- ERH6 98.06/97.93ps 1x2, bought the 1 for 3.5 in 10k

- SFIV5 96.10/96.20/96.30c fly, sold at 2.75 in 3k

- SFIZ5 96.20/96.30/96.40/96.50c condor vs 96.05p, sold at flat down to -0.25 in 6k

- SFIU6 96.90c bought for 9 up to 9.25 in 4k (ref 96.39)

- 0NZ5 96.60/97.00/97.40c fly, bought for 5 in 2.5k

MNI FOREX: USD Index Consolidates Moderate Weakness After Trump-Cook Inspired Vol

- Headlines surrounding the uncertain future for Fed Governor Lisa Cook inspired some sharp two-way flows for the dollar early Tuesday, with the initial dip finding solid demand. Second-tier US data in the form of durable goods and consumer confidence beat expectations, however, a weaker labour differential and the stable session for equities has allowed the greenback to consolidate at moderately weaker levels on the session.

- USDJPY’s intra-day range has been contained within 147.00-148.00, comfortably within the short-term parameters established following Powell’s Jackson Hole remarks. Clearance of the bear trigger at 146.21 (Aug 14 low) would reinstate a downtrend, however, a resumption of gains would instead open 149.12, 61.8% of the Aug 1 - 14 bear leg.

- Despite a 0.3% bounce today, EURUSD remains lower on the week as political uncertainty has ratcheted up following French Prime Minister Francois Bayrou’s plan to call a confidence vote. The trend set-up in EURUSD remains bullish and short-term weakness is for now considered corrective. Support at the 50-day EMA remains intact, at 1.1597. A clear break of it would signal scope for a deeper retracement and potentially expose key support at 1.1392, the Aug 1 low.

- Ahead of the UK Budget (likely late October/early November), vols are recovering off seasonal lows: EUR/GBP 3m implied vols have recovered the entirety of the early August dip - with EUR, USD vols also improving.

- The 30-min candle chart shows EUR/GBP testing the nascent uptrend drawn off the late May lows of 0.8356. The level, today at 0.8624-0.8627, has been tested, and a break below could mark a resumption of the fade off 0.8769, opening 0.8508 in the short-term.

- Australia July CPI headlines a quiet schedule on Wednesday, before the market turns its attention to US GDP & PCE later in the week, as well as Eurozone inflation prints.

MNI OPTIONS: Expiries for Aug27 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550-60(E1.8bln), $1.1620-30(E1.5bln), $1.1650(E2.1bln), $1.1665(E954mln), $1.1700-10(E1.5bln), $1.1750(E1.3bln), $1.1800(E2.0bln)

- USD/JPY: Y147.00($633mln), Y147.20-25($910mln), Y147.40-50($805mln) Y147.90-05($3.2bln)

- GBP/USD: $1.3350-60(Gbp1.8bln), $1.3484-85(Gbp672mln), $1.3515-25(Gbp903mln), $1.3570-75(Gbp1.1bln)

- AUD/USD: $0.6515-25(A$1.3bln), C$1.3915-25($840mln)

- USD/CAD: C$1.3680-90($1.2bln)

- USD/CNY: Cny7.1669($766mln)

MNI US STOCKS: Drifting Mildly Higher, Dog Days Settle In

- Stocks have inched mildly higher late Tuesday, top end of narrow session ranges on quiet late summer trade. Currently, the DJIA trades up 35.31 points (0.08%) at 45319.15, S&P E-Mini Future up 10 points (0.15%) at 6465.25, Nasdaq up 40.4 points (0.2%) at 21489.94.

- Industrials, Health Care and Information Technology sector shares continued to lead gainers in the second half: Boeing +3.16%, GE Vernova +2.74%, Southwest Airlines +2.40%, Howmet Aerospace +2.39% and General Electric +2.02%.

- The Health Care sector was largely buoyed by pharmaceuticals: Eli Lilly & Co +4.51%, Regeneron Pharmaceuticals +2.10%, Humana Inc +0.96% and UnitedHealth Group +0.91%.

- Leading tech stocks included: Leading tech stocks: QUALCOMM +2.01%, Palantir Technologies +1.82%, Advanced Micro Devices +1.81% and Monolithic Power Systems +1.45%.

- On the flipside, Energy and Communication Services shares underperformed in late trade: Paramount Skydance -4.01%, Charter Communications -2.39%, Fox Corp -1.74% and AT&T -1.46%.

- Energy stocks weighed by a drop in crude prices (WTI -0.77 at 64.03): Halliburton -1.99%, Devon Energy -1.65%, Diamondback Energy -1.49% and ConocoPhillips -1.44%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Trend Needle Points North

- RES 4: 6600.00 Round number resistance

- RES 3: 6572.45 2.0% 10-dma envelope

- RES 2: 6523.63 1.764 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6508.75 High Aug 15 and all-time High

- PRICE: 6465.00 @ 1445 ET Aug 26

- SUP 1: 6362.75 Low Aug 20

- SUP 2: 6313.25 Low Aug 6

- SUP 3: 6304.76 50-day EMA

- SUP 4: 6239.50 Low Aug 1

The dominant uptrend in S&P E-Minis remains intact and last Friday’s rally reinforces current conditions. Moving average studies are in a bull-mode position, highlighting a clear uptrend and positive market sentiment. Attention is on 6508.75, the Aug 15 high and the bull trigger. Clearance of this level would confirm a resumption of the uptrend and open 6523.63, a Fibonacci projection. Support to watch lies at 6304.76, the 50-day EMA.

MNI COMMODITIES: Crude Slides, Gold Rises Amid Threat To Fire Fed Governor Cook

- Crude came under pressure on Tuesday, fully unwinding Monday’s gains, as oil markets remain focussed on Russian oil supply amid laboured peace efforts.

- WTI Oct 25 is down by 2.4% at $63.3/bbl.

- On the bearish side, Trump’s 50% tariffs on India for buying Russian oil come into effect on Wednesday while Indian buying shows signs of resuming.

- Crude arrivals into India will likely increase in September and October, driven by higher inflows of Russian crude, Vortexa reports. This could signal that secondary Russian oil sanctions may do little to dent buying.

- A bear cycle in WTI futures remains intact, with initial support at $61.29, the Aug 13 low, which was recently pierced. A continuation lower would open $57.71, the May 30 low.

- Key short-term resistance has been defined at $69.36, the Jul 30 high.

- Meanwhile, spot gold has risen by 0.5% to $3,384/oz, taking total gains from last week’s low to over 2%.

- The move comes amid a further dip in the US dollar today, following headlines surrounding the uncertain future of Fed Governor Lisa Cook.

- The medium-term trend condition in gold remains bullish and moving average studies remain in a bull-mode position, highlighting a dominant uptrend.

- The sideways direction that has been in place since the April peak appears to be a pause in the uptrend. A continuation of gains would open $3,439.0, the Aug 23 high.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 27/08/2025 | 0600/1400 | ** | MNI China Money Market Index (MMI) | |

| 27/08/2025 | 0600/0800 | * | GFK Consumer Climate | |

| 27/08/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 27/08/2025 | 1000/1100 | ** | CBI Distributive Trades | |

| 27/08/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 27/08/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 27/08/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 27/08/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 27/08/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 28/08/2025 | 0130/1130 | * | Private New Capex and Expected Expenditure |