MNI ASIA MARKETS ANALYSIS: Trade Tensions Wreaking Havoc

HIGHLIGHTS

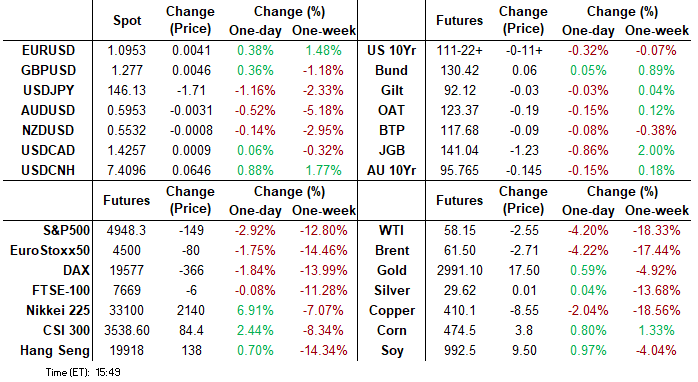

- Treasuries continued to retreat to lows for the week early Tuesday (10Y yield climbed to 4.2582% highs) - early risk-on as stocks rebounded on hopes of progress on US tariff negotiations.

- Tone shifted by midmorning - Tsys climbed back to near steady as stocks reversed huge gains (SPX near 4965.0 vs. 5305.25 high) as the WH confirmed 104% added tariff on China went into effect at noon.

- While stocks extended late session lows, Tsys mostly retreated - except for the short end as curves twisted to new highs (2s10s tapped 55.157 - steepest since mid-February 2022.).

MNI US TSYS: Trade Tensions Reverse Early Stock Gains, Curves Twist to New Highs

- Treasuries look to finish mostly weaker late Tuesday - off lows as tariff headlines continued to rattle markets, curves twisting to the steepest levels in over three years (2s10s tap 55.157 high) while stocks failed to hold onto midmorning gains (SPX emins slipped below 5,000 to 4,988.0 low after marking a session high of 5305.25 at midmorning).

- Treasury futures climbing off lows after Trump officials confirmed 104% added tariff on China went into effect at noon, WH press sec Leavitt adds additional tariff to be collected starting tomorrow.

- Heavy short end buying partially swap-tied as spreads narrowed sharply, projected rate cut pricing rebounded vs. morning's levels - back to pricing in a full point by year end. Current levels vs. early morning (*) as follows: May'25 at -14bp (-8.2bp), Jun'25 at -38.2bp (-28.3bp), Jul'25 at -61.6bp (-49.1bp), Sep'25 -79.3bp (-65.7bp).

- Initial equity optimism boosting the higher beta currencies in G10, before a sharp souring of sentiment prompted a significant turnaround for the likes of AUD & NZD. Overall, the dollar index remains close to unchanged, with a lot of the focus remaining on the JPY and CHF crosses, given they remain a strong barometer for global risk sentiment.

- Focus turns to March FOMC minute release at 1400ET tomorrow, CPI Thursday. PPI Friday morning. Reminder, banks kick off the latest earnings cycle this Friday with Bank of New York Mellon, Wells Fargo & Co, JPMorgan Chase and Morgan Stanley reporting.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00898 to 4.29181 (-0.02803/wk)

- 3M +0.00263 to 4.21022 (-0.04876/wk)

- 6M +0.02251 to 4.03528 (-0.09024/wk)

- 12M +0.06547 to 3.77353 (-0.08990/Wk)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.33% (-0.02), volume: $2.630T

- Broad General Collateral Rate (BGCR): 4.31% (-0.02), volume: $1.029T

- Tri-Party General Collateral Rate (TCR): 4.31% (-0.02), volume: $997B

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $93B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $266B

FED Reverse Repo Operation

RRP usage bounces to $156.911B this afternoon from $148.146B on Monday. Usage had surged to the highest level since December 31, 2024 last Monday, March 31: $399.167B. Compares to $58.770B (lowest level since mid-April 2021) on February 14. The number of counterparties at 34.

US SOFR/TREASURY OPTION SUMMARY

Mixed SOFR & Treasury option flow remained mixed, accounts finding it hard to find momentum as tariff headlines continued to drive volatile underlying futures moves, curves twisting to new highs (2s10s tapped 55.157 high). Projected rate cuts through mid-2025 have rebounded vs. morning's levels - back to pricing in a full point by year end. Current levels vs. early morning (*) as follows: May'25 at -14bp (-8.2bp), Jun'25 at -38.2bp (-28.3bp), Jul'25 at -61.6bp (-49.1bp), Sep'25 -79.3bp (-65.7bp).

SOFR Options:

-10,000 0QN5 97.25/97.50/97.75 call flys vs 0QZ5 97.25/97.50 call spds, 2.25-2.0

+10,000 0QM5 97.00/97.50 call spds 9-9.5 ref 96.745

Block/screen/pit, 50,000 SFRM5 95.75 puts, 2.75 vs. 96.00/0.12%

-5,000 2QK5 96.31 puts, 5.0 vs. 96.675/0.20%

-3,000 0QZ5 96.75 straddles, 83.5-83.0 ref 96.765

-10,000 SFRZ5 98.00/98.50/99.00 call flys, 1.0 ref 96.545

5,000 SFRU5/0QU5 96.37 put spds

Block/screen, -50,000 SFRM5 96.50/97.25 call spds 5.0-4.5 ref 96.015

4,550 SFRU5 95.75 puts, 2.75 ref 96.355

1,250 SFRM5 95.68/95.75/95.81 put trees ref 96.025

Block, 1,125 SFRU6 96.00/0QU5 96.62 3x2 put spd, 20.0 net/front Sep over

1,000 SFRK5 95.75/95.87/96.00 2x3x1 put flys

2,000 SFRM5 95.81/95.87/95.93 put flys ref 96.025

3,000 SFRM5 96.00/96.12 call spds ref 96.038

2,000 SFRU5 95.25/95.62/95.75/95.81 broken put condors ref 96.39 to -.37

2,000 SFRM5 96.50/97.00 1x2 call spds

Block/screen, 9,500 SFRU5 95.62/95.81 put spds ref 96.40

1,000 SFRM5 95.81/95.87/95.93 put flys ref 96.055

10,000 SFRN5 97.00/98.00 call spds vs. 0QN5 97.50/98.00 call spd spd

Treasury Options:

16,250 TYK5 113/114 call spds 10 ref 111-19

5,000 TYM5 113.5/114.5 call spds, 14 ref 111-22.5

1,750 FVK5 108.75/110 1x3 call spds, 3.5

1,500 TUK5 103/103.5 3x2 put spds, 7 net ref 103-24.25 to -23.88

1,500 TYK5 104 calls, 9.5 ref 103-26.12

3,600 TUK5 104.12 calls, 8 ref 103-26.38

2,500 TYM5 112/113/114/115 call condors

6,700 USM5 112/114 put spds, 31 ref 116-23

4,800 TYM5 113 calls, 46 ref 111-21.5

3,000 TYK5 110/110.5 put spds ref 110-22

6,300 TYK5 110 puts, 14 ref 111-21

8,500 TYK5 113.5/115 call spds ref 112-05.5

1,500 TYK5 112.5/114 1x2 call spds ref 112-02

1,200 FVM5 107/107.5 put spds

3,000 TYK 111.25 puts, 32 ref 112-01

Block, 4,000 TYK5 112.25 puts 61 vs. 112-03/0.52%

over 5,700 TYM5 114.5 calls, 33 last

over 5,100 TYM5 108.5 puts, 13 last

2,000 TYM5 113.5/115.5 call spds ref 111-31

MNI OPTIONS: Large Euribor Call Fly Sale, Schatz Put Spread Buy Tuesday

Tuesday's Europe rates/bond options flow included:

- DUK5 106.70/106.50ps, bought for 1.5 in ~11.9k

- OEK5 118/117 put spread, bought for 19.5 in 4.5k

- RXK5 130.50/134.00cs sold at 74.5 in 3k

- ERK5 97.6875/97.8125ps, bought for 1.75 in 2k

- ERU5 99.25/95.62/100.00c fly, sold at 0.25 in 15k

- SFIK5 96.30/96.40cs, bought for 0.75 in 8k

MNI FOREX: Sharp Swings for AUD Persist amid China Tariff Turmoil

- Today’s session was categorised by a tale of two halves, with initial equity optimism boosting the higher beta currencies in G10, before a sharp souring of sentiment prompted a significant turnaround for the likes of AUD & NZD. Overall, the dollar index remains close to unchanged, with a lot of the focus remaining on the JPY and CHF crosses, given they remain a strong barometer for global risk sentiment.

- Specifically for AUDUSD, the most recent turn lower for equities has certainly sapped the overnight enthusiasm, prompting the pair to almost entirely erode the prior 1.5% advance. The turnaround for risk was exacerbated by the USTR's Greer stating that tariff exemptions will not come through in the near-term, and late confirmation that 104% tariffs on China would be implemented from April 09.

- Earlier 0.6085 highs fell short of initial resistance, which stands at 0.6127, and technical conditions remain firmly in bearish territory. Yesterday’s low print of 0.5933 matched closely with an initial technical support, the 1.764 projection of the Sep 30 - Nov 6/7 price swing. This will remain the key short-term mark on the downside.

- USDJPY is also substantially off the overnight highs, located at 148.12. The pair maintains a bearish tone following last week’s sharp sell-off and the Monday recovery is - for now - considered corrective. A resumption of the downtrend and a break of Friday’s 144.56 low would signal scope for an extension towards 144.13, a Fibonacci retracement point.

- Amid the deterioration of the US/China trade relationship, USDCNH has been pushing fresh record highs today, at 7.3930 at typing. Market moves follow the push higher for the USD/CNY midpoint fix overnight - at 7.2038, the CFETS fix was the highest since Sept'23 and not far off the highest fix on record from late 2022 at 7.2555.

- Calendar focus turns to the RBNZ decision on Wednesday, before the market’s attention shifts to US inflation data, scheduled on Thursday.

MNI OPTIONS: Expiries for Apr09 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0880(E1.2bln), $1.0900-05(E1.4bln), $1.0950(E551mln)

- USD/JPY: Y147.00($716mln), Y147.40-50($1.2bln)

- EUR/JPY: Y162.75-90(E719mln)

- AUD/USD: $0.5975(A$650mln)

- USD/CAD: C$1.4100($571mln)

MNI US STOCKS: Late Equities Roundup: Materials & Energy Lead Late Sell-off

- Stocks continue to retreat from midmorning highs, the DJIA, SPX emini and Nasdaq are in the red. Currently, the DJIA trades down 20.13 points (-0.05%) at 37943.95 (39,426.60 high), S&P E-Minis down 32 points (-0.63%) at 5064.75 (5,305.25 high), Nasdaq down 159 points (-1%) at 15443.37 (16,316.16 high). This morning's strong risk-on tone started to evaporate after the White House confirmed the 104% tariff on China went into effect at noon.

- Materials and Energy sectors continued to underperform in late trade: Albemarle Corp -10.57%, LyondellBasell Industries -4.98%, Dow Inc -4.32% and PPG Industries -4.03% weighed on the Materials sector.

- The Energy sector was weighed by oil and gas shares under pressure as crude prices fell in late trade (WTI -1.47 at 59.23 -- 4Y lows): APA Corp -5.21%, Occidental Petroleum -5.14%, Devon Energy -4.54%, Diamondback Energy -2.59% and EOG Resources -2.51%.

- Financials and Utility sectors outperformed in late trade, insurance names buoyed Financials: Everest Group +2.89%, Progressive Corp +2.51%, Arch Capital Group +2.27% and W R Berkley +2.21%.

- Meanwhile, alternative energy providers supported the Utility sector: Constellation Energy +3.24%, Atmos Energy +1.43%, Vistra +1.09% and Public Service Enterprise +0.93%.

- Reminder, banks kick off the latest earnings cycle this Friday with Bank of New York Mellon, Wells Fargo & Co, JPMorgan Chase and Morgan Stanley reporting.

MNI EQUITY TECHS: E-MINI S&P: (M5) Gains Appear Corrective

- RES 4: 5797.02 50-day EMA

- RES 3: 5610.64 20-day EMA

- RES 2: 5435.00 High Apr 4

- RES 1: 5286.50 High Apr 7

- PRICE: 4960.00 @ 1539 ET Apr 9

- SUP 1: 4832.00 Low Apr 7

- SUP 2: 4760.88 1.618 proj of the Feb 19 - Mar 13 - 25 price swing

- SUP 3: 4663.75 1.764 proj of the Feb 19 - Mar 13 - 25 price swing

- 7SUP 4: 4519.84 61.8% retracement of the Oc ‘22 - Feb ‘25 bull cycle

S&P E-Minis continues to trade in a volatile manner. A bearish theme remains intact and the latest fresh cycle lows, strengthen current conditions. Scope is seen for an extension towards the 4800.00 handle next. Moving average studies are in a bear-mode position, highlighting a dominant downtrend. Initial firm resistance is seen at 5610.64, the 20-day EMA. Short-term gains are for now, considered corrective

MNI COMMODITIES: WTI Falls Further, Copper Declines Amid US-China Trade Tensions

- WTI has returned to losses after the White House Press Secretary confirmed imposition of 104% tariffs on Chinese imports, offsetting concerns of a shutdown on the Keystone pipeline.

- WTI May 25 is down by 2.3% at $59.3/bbl.

- A bearish theme in WTI futures remains intact following the recent impulsive sell-off. The move down has resulted in the breach of a number of important support levels, with sights on $57.79 next, a Fibonacci projection.

- Meanwhile, spot gold has erased earlier gains amid the renewed tariff threat, with the yellow metal currently unchanged at $2,983/oz.

- The trend condition in gold remains bullish and the recent pullback from record highs appears to be corrective. The next key support to watch lies at $2,946.9, the 50-day EMA. The bull trigger is $3,167.8, the Apr 3 high.

- Copper has also erased earlier gains as fears of a prolonged US-China trade spat mount, with the red metal now 1.3% lower on the session at $413/lb.

- Trade war fears rose as USTR Greer stated that tariff exemptions will not come through in the near-term, coming on top of concerns over a prolonged trade spat between the US and China.

- Copper has now fallen by almost 15% since last week’s tariff announcements, highlighting an acceleration of the current bear cycle.

- Key support at $403.85, the Jan 2 low, has been pierced. A clear break would strengthen a bearish theme and open $392.10, the Aug 7 ‘24 low.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 09/04/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 09/04/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 09/04/2025 | - | Higher Reciprocal Tariffs On Imports | ||

| 09/04/2025 | 1230/1430 | ECB's Cipollone On Macro-Financial Stability Panel | ||

| 09/04/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/04/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 09/04/2025 | 1500/1100 | Richmond Fed's Tom Barkin | ||

| 09/04/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 09/04/2025 | 1800/1400 | *** | FOMC Minutes | |

| 10/04/2025 | 2301/0001 | * | RICS House Prices | |

| 10/04/2025 | 0130/0930 | *** | CPI | |

| 10/04/2025 | 0130/0930 | *** | Producer Price Index |