MNI ASIA MARKETS ANALYSIS: Tracking Bunds, Geo-Pol Risk

HIGHLIGHTS

- Treasuries look to finish mixed Friday, curves mildly steeper with short end rates outperforming going into month end.

- Treasuries tracked more abrupt moves in German Bunds & curve steepening, likely tied to Dutch pension fund transition to new contribution system news.

- Modest risk-off after Miami Herald headline annc Pres Trump's decision to launch attacks on Venezuelan military sites "linked to drugs ... at any moment". Trump later denied imminent attacks with reporters on Air Force One.

- The flurry of USD selling ahead of and across the WMR month-end fixing window appears to have stalled the upward momentum for the greenback on Friday.

US TSYS

MNI US TSYS: Early Risk-Off on Venezuela Attack Plans Denied by Pre Trump

- Treasuries look to finish mixed Friday, curves modestly steeper after bonds tracked moves in Bunds earlier in the session: German Bunds retreated, 5s30s curve steepened likely tied to Dutch pension fund transition to new contribution system news.

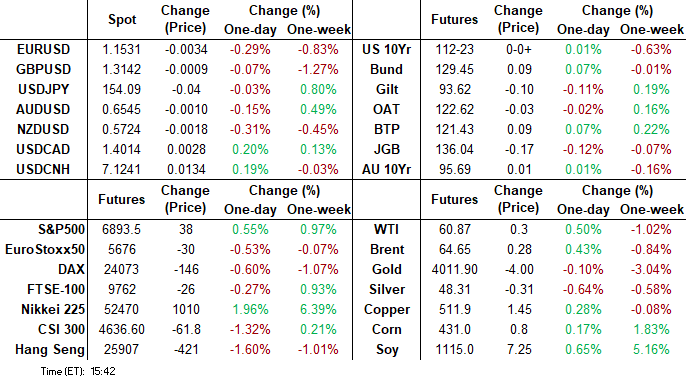

- Currently, the Dec'25 10Y contract trades +.5 at 112-23 (112-17.5 low/-27 high), the contract needs to trade above 113-18+, the Oct 28 high to signal a possible bullish reversal. 10Y yield -.0040 at 4.0930%.

- Earlier risk-off followed Miami Herald headlines announcing Pres Trump's decision to launch attacks on Venezuelan military sites "linked to drugs ... at any moment". Trump later denied imminent attacks when speaking to reporters on Air Force One.

- The flurry of USD selling ahead of and across the WMR month-end fixing window appears to have stalled the upward momentum for the greenback on Friday, with the USD index now settling just above yesterday’s highs around 99.75 as we approach the weekend close.

- Potential month-end portfolio rebalancing another factor for swings in rates & stocks earlier.

- WTI has regained ground in a day where Trump headlines have sparked volatility. The latest rally appears to be driven by news that the Pentagon has greenlit the US providing long-range Tomahawks missiles to Ukraine, which would be a sign of the US taking a harder stance against Russia.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.04% (-0.23), volume: $3.098T

- Broad General Collateral Rate (BGCR): 3.99% (-0.25), volume: $1.170T

- Tri-Party General Collateral Rate (TCR): 3.99% (-0.25), volume: $1.142T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.87% (-0.25), volume: $104B

- Daily Overnight Bank Funding Rate: 3.87% (-0.25), volume: $179B

FED Reverse Repo Operation

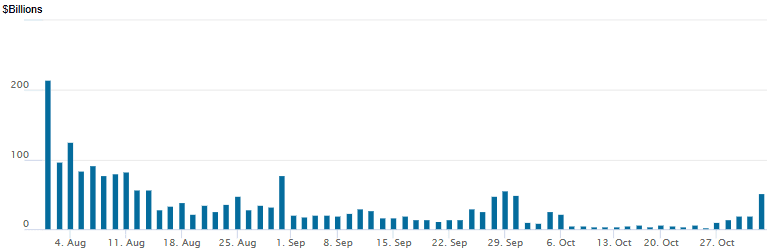

RRP usage climbed to $51.802B with 25 counterparties going into month end, up from $19.166B Thursday. Compares to $2.435B on October 24 (lowest level since mid-March 2021) and the year's highest usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

With a few exceptions, SOFR options saw better put structure trade on net Friday, underlying futures mixed, SOFR Reds (SFRZ6-SFRU7) gaining slightly. Projected rate cut pricing retreat slightly vs. early morning levels (*): Dec'25 at -15.6bp (-18bp), Jan'26 at -23.5bp (-26.5bp), Mar'26 at -32.1bp (-35.1bp), Apr'26 at -38.5bp (-41bp).

SOFR Options:

+20,000 SFRH6 96.37/96.50 put spds, 8.0 vs. 96.415/0.15%

+7,500 0QZ5 97.00/97.25 call spds, 5.0 ref 96.90

+2,000 0QF6 97.50 calls, 2.5 vs. 96.91/0.10%

+20,000 SFRU6 96.25/96.62 vs. 10,000 0QU6 96.62 puts, 1.25-1.50 net

+9,000 SFRH6 96.37/96.50 put spds, 8.0 vs. 96.415/0.15%

-4,000 SFRZ5 95.87/96.00/96.12 call flys, 1.75 ref 96.225

-5,000 SFRX5 96.25/96.37 2x1 put spds, 5.5

+5,000 SFRH6 96.37/96.50 put spds, ref 96.415

-5,000 SFRX5 96.18/96.25 strangles, 4.0 ref 96.225

4,000 2QF6 97.00/97.25/97.50 call flys ref 96.755

Block, 5,000 SFRX5 95.87/96.12 put spds .25 vs. 96.235/0.10%

Block, 5,000 SFRH6 96.06/96.31/96.43 broken put flys 1.0 ref 96.405

over -30,000 SFRZ5 96.25/96.31/96.50/96.56 call condors, 2.75 ref 96.225

+6,000 SFRF6 96.68/96.75 call spds, 0.75

+7,000 SFRX5 96.18 puts, 1.75

3,700 SFRF6 96.06/96.18/96.31 put trees

5,000 SFRZ5 96.25/96.31/96.43/96.50 call condors ref 96.225

6,000 SFRF6 96.68/96.75 call spds ref 96.41

2,000 SFRF6 96.68/96.75/96.87/97.00 call condors ref 96.41

4,500 SFRF6 96.18/96.31 put spds ref 96.41

6,000 SFRM6 96.50/2QM6 96.37 put spds

+7,000 0QZ5 97.00/97.25 call spds, 4.5 ref 96.875

1,500 SFRZ5 96.12/96.25/96.37 put flys ref 96.23

+4,000 SFRZ5 96.00/96.12/96.25/96.37 put condors, 6.25 ref 96.23

Block, +4,000 SFRM6/0QM6 96.50 put spds, 1.0 vs. 96.665/0.10%

+5,000 SFRZ5 96.18/96.31/96.43/96.56 call condors, 2.5 ref 96.23

+4,200 SFRX5 96.18/96.25/96.31 put trees, 3.25 ref 96.225

+5,000 SFRX5 96.00/96.12 put spds, 0.5 ref 96.225

4,500 SFRZ5 96.25/96.31/96.37/96.43 call condors

Treasury Options:

10,000 TYZ5 113.5 calls, 13 ref 112-23.5

4,400 USZ5 116.5/118 put spds,

2,500 USG6 121 calls, 49 bid ref 117-11

+10,000 TUZ5 104 puts, 4.5

2,500 TUZ5 104.37/104.62

1,350 TYZ5 111.5/112.75/114 call flys ref 112-19.5

1,300 USF6 104 puts ref 116-31

-2,000 USZ5 115 puts, 17

+4,000 TYZ5 111.5 puts, 7 ref 112-18.5

MNI OPTIONS: More Subdued Post-ECB Session Includes Sonia Risk Reversal, ER Upside

Friday's Europe rates/bond options flow included:

- ERM6 98.1875/98.25/98.375/98.4375c condor, bought for 0.75 in 10k

- 1x ERM6 97.93/97.75 ps v 1.5x ERH6 97.93/87 ps, bought for 0.875 in 2k (vs 99)

- 0NZ5 96.80/96.50RR 1x1.5, bought the call for -1 in 3k. This was also bought for flat in 9k this Week

MNI FOREX: USD Index Set to Post Highest Weekly Close Since May

- The flurry of USD selling ahead of and across the WMR month-end fixing window appears to have stalled the upward momentum for the greenback on Friday, with the USD index now settling just above yesterday’s highs around 99.75 as we approach the weekend close.

- USD: Three consecutive days of gains sees the DXY ~1.2% off the week’s lows, looking set to post its highest weekly close since May amid the hawkish lean from the Fed and notable weakness for the likes of GBP and NZD.

- GBP: For GBPUSD, the breach of key support at 1.3142 is a meaningful development for the pair. A close below would strengthen current bearish conditions, and refocus attention on 1.3041, the Apr 14 low. UK fiscal developments as we approach the Nov 26 budget will be key in shaping the short-term trajectory for sterling, while next week’s Bank of England meeting should not go overlooked.

- NZD: For NZDUSD, spot trades within 40 pips of cycle lows, located at 0.5683. A move below here would turn the focus to 0.5636, the 76.4% retracement of the year’s range. New Zealand Q3 employment data is scheduled next Wednesday local time.

- JPY: The lack of hawkish signals from the BOJ was enough to boost USDJPY to the highest levels since February, potentially looking to close above 154.00. Thursday’s rally resulted in a breach of key resistance at 153.27, the Oct 10 high, and confirms a resumption of the medium-term uptrend. Sights are on 154.80 next, the Feb 12 high.

MNI OPTIONS: Expiries for Nov3 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1400(E686mln), $1.1450(E772mln), $1.1600(E561mln), $1.1695(E614mln)

- USD/JPY: Y150.00($1.1bln)

- USD/CAD: C$1.3980-85($1.1bln)

MNI US STOCKS: Late Equities Roundup: Recovering From Midday Lows

- Stocks are climbing off midday lows late Friday. Stocks had pared gains following earlier Miami Herald headlines announced Pres Trump's decision to launch attacks on Venezuelan military sites "linked to drugs ... at any moment". Trump later denied imminent attacks when speaking to reporters on Air Force One. Potential month-end portfolio rebalancing could be another factor for stocks reversing earlier gains.

- Currently, the DJIA trades up 47.08 points (0.1%) at 47,568.01, S&P E-Minis up 19.75 points (0.29%) at 6,876.25

Nasdaq up 167.9 points (0.7%) at 23,750.55. - Consumer Discretionary and Energy sector shares continued to outperform: Amazon continued to rally after reporting better than expected earnings late Thursday, currently +10.77%, MGM Resorts Int +3.22%, Tesla +2.70%, Lululemon Athletica +1.85% and Carnival +1.20%.

- Advances in the Energy sector were led by Expand Energy +2.39%, Chevron +2.32%, Targa Resources +2.03% and EQT C+1.43%.

- Meanwhile, a mix of Materials, Utilities, Consumer Staples and Health Care sector shares continued to underperform: Dexcom -12.51%, Monolithic Power Systems -10.81%, Solstice Advanced Materials -7.20%, Erie Indemnity -7.18%, Motorola Solutions -5.15%, Arthur J Gallagher -4.89% and AbbVie -4.80%.

- Of note, the latest earnings cycle is approximately 70% complete with the following expected Monday Morning: ON Semiconductor, Ares Management, Cipher Mining Inc.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Bull Cycle Intact

- RES 4: 7000.00 Psychological round number

- RES 3: 6993.12 3.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6974.04 3.382 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 1: 6953.75 High Oct 30

- PRICE: 6870.50 @ 1455 ET Oct 31

- SUP 1: 6812.25/6787.51 High Oct 9 / 20-day EMA

- SUP 2: 6783.25 50-day EMA

- SUP 3: 6540.25 Low Oct 10 and a key short-term support

- SUP 4: 6506.50 Low Sep 5

The trend condition in S&P E-Minis remains bullish and the latest pullback appears corrective. The fresh cycle high this week confirms a resumption of the primary uptrend and maintains the bullish price sequence of higher highs and higher lows. Sights are on 6974.04 next, a Fibonacci projection point. Initial firm support to watch lies at 6748.48, the 20-day EMA. Key pivot support lies at 6783.25, the 50-day EMA.

MNI COMMODITIES: Crude Edges Higher Ahead Of OPEC+ Meeting, Gold Falls

- WTI has regained ground in a day where Trump headlines have sparked volatility. The latest rally appears to be driven by news that the Pentagon has greenlit the US providing long-range Tomahawks missiles to Ukraine, which would be a sign of the US taking a harder stance against Russia.

- WTI Dec 25 is up by 0.4% at $60.8/bbl.

- Earlier volatility came after reports of US plans to strike military targets in Venezuela were refuted by Trump.

- Aside from that, weak Chinese data added to rising global supply concerns, with another OPEC+ output hike expected this weekend.

- For WTI futures, recent gains appear corrective for now. However, a clear break of resistance at $62.34, the Oct 8 high, would expose key resistance at $65.77, the Sep 26 high.

- First key support and the bear trigger is unchanged at $55.96, the Oct 20 low.

- Meanwhile, spot gold has fallen by 0.5% today to $4,004/oz, as the market continues to assess the truce in the US-China trade war.

- Westpac said that a combination of the hawkish Fed cut, US-China truce and heavy outflows from gold ETFs could result in gold falling back to $3,750.

- A fresh cycle low in gold this week highlights an extension of the bear cycle that started Oct 20. The 20-day EMA has been breached, signalling scope for a test of the 50-day EMA, at $3,859.0.

- Initial resistance is at $4,161.4, the Oct 22 high.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 03/11/2025 | 0700/0200 | * | Turkey CPI | |

| 03/11/2025 | 0730/0830 | *** | CPI | |

| 03/11/2025 | 0815/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 03/11/2025 | 0845/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 03/11/2025 | 0850/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 03/11/2025 | 0855/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 03/11/2025 | 0900/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 03/11/2025 | 0930/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 03/11/2025 | 1200/1300 | ECB Lane Lecture In Dublin | ||

| 03/11/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 03/11/2025 | 1445/0945 | *** | S&P Global Manufacturing Index (final) | |

| 03/11/2025 | 1500/1000 | *** | ISM Manufacturing Index | |

| 03/11/2025 | 1500/1000 | * | Construction Spending | |

| 03/11/2025 | 1500/1000 | * | Construction Spending | |

| 03/11/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 03/11/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 03/11/2025 | 1700/1200 | San Francisco Fed's Mary Daly | ||

| 03/11/2025 | 1830/1330 | BOC Governor fireside chat at The Logic conference | ||

| 03/11/2025 | 1900/1400 | Federal Reserve Governor Lisa Cook | ||

| 04/11/2025 | 0030/0930 | ** | S&P Global Final Japan Manufacturing PMI | |

| 04/11/2025 | 0330/1430 | *** | RBA Rate Decision |