MNI ASIA MARKETS ANALYSIS: Tech Lifts Indexes to New Highs

HIGHLIGHTS

- Early Treasury support evaporated after comments from Fed Bostic: sees little reason for additional rate cuts "for now", labor market "not in crisis", Tsy futures look to finish near late session lows.

- New Fed Governor Miran unsurprisingly argues for significantly lower policy interest rates (2-2.5% "ballpark) in his first prepared remarks since being appointed to the Board, calling current rates "very restrictive".

- FX trading with a subdued tone amid a lighter economic calendar to start the week, with central bank speakers providing little to boost volatility, USD index tracks around 0.25% lower on Monday.

- Tech and railroad deals (Nvidia $100B investment into OpenAI; Kazakhstan intent to purchase $4B in locomotive and rail equipment), helped push equities to new record highs yet again.

US TSYS

MNI US TSYS: Fed Speakers: Difference of Opinions

- Treasuries reversed early support after comments from Fed Bostic: sees little reason for additional rate cuts "for now", labor market "not in crisis": "forecasting is really hard these days and so I still have one cut down for the year. So that would be it."

- StL Fed Musalem: "I believe there is limited room for easing further without policy becoming overly accommodative, and we should tread cautiously," Musalem said in prepared remarks for an event at the Brookings Institution.

- Conversely, new Fed Governor Miran (Mr. Low Dot) unsurprisingly argues for significantly lower policy interest rates (2-2.5% "ballpark) in his first prepared remarks since being appointed to the Board, calling current rates "very restrictive".

- Projected rate cut pricing cooled slightly vs. early morning levels (*): Oct'25 at -22.3bp (-22.9bp), Dec'25 at -43.1bp (-44.6bp), Jan'26 at -54.1bp (-56.2bp), Mar'26 at -66bp (-69.1bp).

- Currently, the Dec'25 10Y trades -2.5 at 112-21.5 (yld 4.1467% +.0193) vs. 112-21.5 low, modest volumes (TYZ5 1.03M); technical resistance well above at 113-29 (High Sep 11 and the bull trigger); Support at 112-15+ (High Aug 5 and 14). Curves mixed: 2s10s -1.430 at 53.948, 5s30s +0.067 at 106.406.

- Look ahead to Tuesday's session: S&P Global flash PMIs, Current Account Balance and regional Fed data. Fed Chair Powell speaks about the economy at 1235ET after Bowman's outlook (0900ET) and Bostic podcast (1000ET).

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.14% (+0.00), volume: $2.881T

- Broad General Collateral Rate (BGCR): 4.11% (+0.00), volume: $1.148T

- Tri-Party General Collateral Rate (TCR): 4.11% (+0.00), volume: $1.118T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.08% (+0.00), volume: $95B

- Daily Overnight Bank Funding Rate: 4.08% (+0.00), volume: $191B

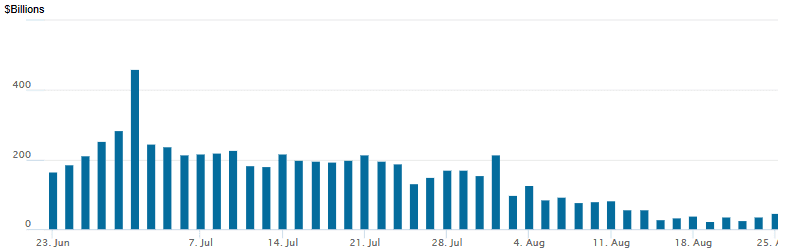

FED Reverse Repo Operation

RRP usage drifts up to $14.173B with 15 counterparties this afternoon from $11.363B Friday - lowest levels since early April 2021. Compared to this year's high usage of $460.731B occurred on June 30.

US SOFR/TREASURY OPTION SUMMARY

Large Tsy 10Y call buying highlight of Monday's FI option trade. Underlying futures mildly weaker, near late session lows. Projected rate cut pricing cooled slightly vs. early morning levels (*): Oct'25 at -22.3bp (-22.9bp), Dec'25 at -43.1bp (-44.6bp), Jan'26 at -54.1bp (-56.2bp), Mar'26 at -66bp (-69.1bp).

SOFR Options:

-3,000 0QZ5 97.37 calls, 5.0 vs. 96.985/0.18%

+17,000 SFRV5 96.31 calls, 5.5 vs. 96.33/0.56% (adds to +5k earlier at 5.0)

-6,000 SFRV5 96.31 calls, 5 vs. 96.33/0.62%

2,000 SFRZ5 96.00/96.12/96.25 put flys, 2.5

3,000 SFRV5 96.37/96.73/96.50 call trees, 0.75 ref 96.37

1,250 SFRZ5 96.37/96.50 call spds vs. 96.12/96.25 put spds ref 96.345

1,000 SFRV5 96.37/96.43 call spds vs. 0QV5 97.00/97.06 call spds

2,750 SFRH6 95.86/96.06/96.25 put flys, ref 96.57

3,000 SFRZ5 95.62/95.75 2x1 put spds ref 96.345

Treasury Options:

over -7,500 TYX5 113.5/114.5/115.5 1x3x2 call flys, 2 net on the package (total volume on the 114.5 call over 40k)

over +155,000 TYV5 114 calls, 31-33 ref 112-27 to -24.5

8,197 USV5 117 calls, 13

3,000 TYV5/Wed wkly TY 112 put spd on a 1x2 put spds

1,500 FVV5 109/109.25 2x1 put spds ref 109-16.5

1,800 TYZ5 113 straddles vs. TYX5 112/114 strangles (1x3 ratio)

2,400 TYX5 110.5 puts ref 112-26

3,800 TYZ5 113 calls ref 112-26.5 to -25.5

2,000 FVV5 109.5 calls, 8.5 ref 109-14.25

1,000 USV5 114.5/115.5 2x3 put spds ref 116-08

2,000 TYV5 112.25 puts, 5 ref 112-23

MNI BONDS: EGBs-GILTS CASH CLOSE: Mixed Curves Ahead Of PMIs

European yields were little changed Monday, with longer-end Gilts slightly outperforming their German counterparts.

- Yields opened the session a little higher coming in from the weekend, carrying on from a bond-bearish tone late last week, but gradually descended to session lows by mid-day London time with few immediate macro/headline movers in evidence.

- 10Y Gilt yields briefly hit a post-Sept 4 high (4.724%) but otherwise trade was largely within last week's ranges.

- Comments from BOE's Pill and Bailey didn't prove impactful. MNI's Macro team noted however that all seven of the non-dissenting MPC members are due to make public appearances before the end of September.

- On the day, the UK curve bull flattened, with Germany's twist steepening.

- Periphery/semi-core EGB spreads widened slightly. BTP spreads were a little wider, despite Friday's one-notch rating upgrade to Italy from Fitch; France's were little changed following Friday's one-notch downgrade from Morningstar DBRS.

- Tuesday's schedule includes flash September PMIs, and another appearance by BOE's Pill.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.5bps at 2.018%, 5-Yr is down 0.6bps at 2.32%, 10-Yr is unchanged at 2.748%, and 30-Yr is up 2bps at 3.357%.

- UK: The 2-Yr yield is down 0.2bps at 3.98%, 5-Yr is down 0.2bps at 4.13%, 10-Yr is down 0.3bps at 4.712%, and 30-Yr is down 1.1bps at 5.548%.

- Italian BTP spread up 1.2bps at 79.7bps / Spanish up 0.3bps at 55.1bps

MNI OPTIONS: Week Opens With Bund Put/Call Spread Buying

Monday's Europe rates/bond options flow included:

- RXX5 131/132cs, bought for 4.5 in 3k Total

- RXZ5 128/126ps, bought for 66 in 3.25k

- ERU6 98.125/98.25cs, bought for 3.75 in 5k (ref 98.02)

- 2RX5 97.6875/97.50ps vs 0RX5 97.9375p, bought the ps for half in 5k

- SFIF6 96.45/96.35/96.25/96.05p condor with SFIG6 96.50/96.40/96.25/96.05p condor, bought the strip for 2 in 4.6k

- SFIU6 96.90c, sold at 6.75 in 8k

MNI FOREX: USD Index Eases Off Recovery Highs, SEK Outperforms Ahead of Riksbank

- The USD index tracks around 0.25% lower on Monday, easing from the overnight peak that saw the index print a fresh recovery high at 97.82. Markets are trading with a subdued tone amid a lighter economic calendar to start the week, with central bank speakers providing little to boost volatility.

- The EUR outperforms, rising around 0.35% against the dollar to 1.1785. Large option expiries for EURUSD between the 1.17/18 mark might define the short-term range, following the post-Fed volatility last week that saw the pair reverse from 1.1919 cycle highs. Support to watch is 1.1667. the 50-day EMA.

- Last Thursday’s advance for EURJPY resulted in a breach of 173.97 resistance, the Jul 28 high and bull trigger. The cross has been consolidating above 174.00 for much of the session, bolstering the medium-term uptrend. Sights are on 174.86 next, a Fibonacci projection, before the 2024 highs which reside at 175.43, a key medium-term resistance.

- SEK outperforms the G10 basket Monday, seemingly trading as a high beta Euro with no obvious tailwinds from the equity/risk sentiment or rate differential channels. Focus of course remains on tomorrow's Riksbank decision, which is a very close call between a hold and a 25bp cut.

- For NZDUSD, the sharp reversal from 0.6000 to current spot levels renews the focus on a significant pivot point at 0.5800, which coincides with the 50% retracement of the year’s range. Below 0.5800, 0.5728 and 0.5636 would be the most obvious targets for a deeper selloff.

- Eurozone and US flash PMIs for September and the Riksbank decision highlight Tuesday’s calendar.

- LATAM: Argentinian Peso Continues To Outperform As US Promises Forceful Action

- The Argentinian peso continues to outperform on Monday after the US said it will take “large and forceful” action to support the country. USDARS fell by over 2.5%. Local equities are also up by over 6% and the country’s dollar bonds have rallied sharply, with Argentina '35s up more than 5pts. US Treasury Secretary Bessent said that the US won’t take action until after the meeting between Presidents Trump and Milei tomorrow. He also said that he had spoken with IMF MD Georgieva about Argentina and is satisfied with their positions.

MNI US STOCKS: Late Equities Roundup: AI Center Buildout, Rail Equipment Rally

- Stocks climb to new record highs yet again - due in large part to Information Technology sector shares Monday: Nvidia gaining over 3.60% after announcing it's intent to "invest up to $100B" in Microsoft's OpenAI data center buildout.

- Currently, the DJIA trades up 70.16 points (0.15%) at 46378.86 vs. 46429.02 record high, S&P E-Minis up 26.75 points (0.4%) at 6748.75 vs. 6752.00 record high, Nasdaq up 143.8 points (0.6%) at 22773.72 vs. 22787.95 record high.

- Additional tech sector shares outperforming in the second half include: Teradyne +12.93%, Skyworks Solutions +5.23%, Western Digital +4.63% and Oracle Corp +4.49%.

- Utilities and Industrial sector shares gained in the second half, the former buoyed by Constellation Energy +3.65%, Vistra +3.56%, NRG Energy +3.43% and NiSource +3.32%.

- Industrial sector shares rallied in the second half after President Trump announced Kazakhstan intent to purchase $4B in locomotive and rail equipment: Westinghouse Air Brake Tech +6.23%, EMCOR Group +2.95%, Norfolk Southern Corp +2.72% and GE Vernova Inc +2.66%.

- On the flipside, Consumer Staples and Financial Services sector shares continued to underperform in the second half: Kenvue -6.41%, Archer-Daniels-Midland -4.04%, Keurig Dr Pepper -3.58% and Church & Dwight Co -3.57%. Meanwhile, Coinbase Global -3.26%, Fifth Third Bancorp -2.53%, Regions Financial -2.03% and Citizens Financial -2.02% continued to weigh on the Financial Services sector.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Northbound

- RES 4: 6787.63 1.382 proj of the Aug 1 - 15 - 20 price swing

- RES 3: 6750.50 2.000 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6748.50 1.236 proj of the Aug 1 - 15 - 20 price swing

- RES 1: 6731.50 High Sep 19

- PRICE: 6703.50 @ 14:15 BST Sep 22

- SUP 1: 6602.01 20-day EMA

- SUP 2: 6536.50 Low Sep 8

- SUP 3: 6487.14 50-day EMA

- SUP 4: 6417.25 Low Aug 12

A bull cycle in S&P E-Minis remains intact and the contract traded to a fresh cycle high on Friday. Price has breached the 6700.00 handle and this signals scope for an extension towards 6748.50, a Fibonacci projection point. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend and positive market sentiment. Initial support to watch lies at 6602.01, the 20-day EMA.

COMMODITIES

MNI Americas End of Day Oil Summary: Crude Steady

US OIL: September 22 - Americas End of Day Oil Summary: Crude Steady

WTI crude is relatively steady overall amid Oct expiration, with looming oversupply concerns weighed against supply risks from potential sanctions and strikes on Russian energy infrastructure. Crude remains within the $5/bbl range seen since early August. Resumed weakness could retest $57.71, the May 30 low.

- The EU is considering trade measures to target its remaining Russian oil imports, Bloomberg reported on Saturday citing people familiar with the matter.

- The U.S. has sought to continue pressure on Indian purchases of Russian oil in its latest trade talk efforts sources told Bloomberg on Saturday.

- Strikes were reported at the Saratov and Novokuybyshevsk refineries and an Urals production station in the Samara region.

- Kurdish media are reporting that the Kurdistan Regional Government, Iraq’s Federal Oil Ministry and international oil companies (IOCs) have signed a tripartite agreement which will return oil exports from Kurdistan to Turkey’s Ceyhan port.

- WTI Oct futures were down 0.1% at $62.64

- WTI Nov futures were down 0.2% at $62.28

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 23/09/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 23/09/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 23/09/2025 | 0730/0930 | *** | Riksbank Interest Rate Decison | |

| 23/09/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 23/09/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 23/09/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 23/09/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 23/09/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 23/09/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 23/09/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 23/09/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 23/09/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 23/09/2025 | 0900/1000 | BOE Pill Fireside Chat At Pictet Research Institute Symposium | ||

| 23/09/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 23/09/2025 | 1230/0830 | * | Current Account Balance | |

| 23/09/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 23/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 23/09/2025 | 1300/0900 | Fed Governor Michelle Bowman | ||

| 23/09/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 23/09/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 23/09/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 23/09/2025 | 1400/1000 | *** | NAR existing home sales | |

| 23/09/2025 | 1400/1000 | Atlanta Fed's Raphael Bostic | ||

| 23/09/2025 | 1420/1620 | ECB Cipollone In Bloomberg Fireside Chat | ||

| 23/09/2025 | 1635/1235 | Fed Chair Jay Powell | ||

| 23/09/2025 | 1700/1300 | * | US Treasury Auction Result for 2 Year Note | |

| 23/09/2025 | 1815/1415 | BOC Governor Macklem speech in Saskatoon | ||

| 24/09/2025 | 2301/0001 | * | Brightmine pay deals for whole economy | |

| 24/09/2025 | 0030/0930 | ** | Jibun Bank Flash Japan PMI | |

| 24/09/2025 | 0130/1130 | *** | CPI Inflation Monthly |