MNI ASIA MARKETS ANALYSIS: Strong Earnings, Trade Optimism

HIGHLIGHTS

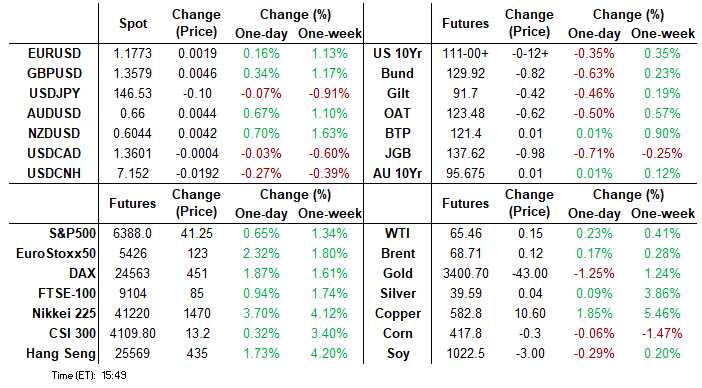

- Treasuries look to finish weaker, through yesterday's lows, general risk-on tone tied to positive earnings and trade deal optimism after Pres Trump announced deal with Japan late Tuesday.

- Financial Times article posited US/EU were closing in on a 15% deal added to the positive sentiment - despite WH advisor Navarro saying to take the FT story with a grain of salt.

- Stocks surged (new record high for SPX eminis at 6393.75), US$ retreated back to early July levels (BBDXY -2.74 at 1193.06).

- Focus turns to Thursday's data: weekly claims, S&P Global US Mfg/Services PMIs and New Home Sales.

US TSYS

MNI US TSYS: Trade Sentiment, Strong Earnings Add to Risk-On Tone

- Treasuries look to finish near session lows Wednesday, improved sentiment tied to trade and better than expected equity earnings added to the risk-on tone after Pres Trump announced deal with Japan late Tuesday.

- Financial Times article posited US/EU were closing in on a 15% deal added to the positive sentiment - despite WH advisor Navarro saying to take the FT story "with a grain of salt".

- Existing home sales fell more than expected in June, to 3.93M (seasonally-adjusted annualized rate), vs 4.00M expected and 4.04M in May (upwardly revised by 10k). That's a 9-month low, breaking an 8-month streak of sales above 4 million.

- MBA composite mortgage applications inched up 0.8% (sa) last week, essentially flat after -10% and +9.4% in the previous two weeks. New purchase applications outperformed after some rare trend underperformance since June, rising 3.4% after -11.8% compared to -2.6% after -7.4% for refis.

- Stocks surged (new record high for SPX eminis at 6393.75), US$ retreated back to early July levels (BBDXY -2.74 at 1193.06).

- Focus turns to Thursday's data: weekly claims, S&P Global US Mfg/Services PMIs and New Home Sales.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.28% (-0.02), volume: $2.692T

- Broad General Collateral Rate (BGCR): 4.27% (+0.00), volume: $1.115T

- Tri-Party General Collateral Rate (TCR): 4.27% (+0.00), volume: $1.092T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $107B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $273B

FED Reverse Repo Operation

RRP usage slips to $189.632B this afternoon from $196.374B yesterday, total number of counterparties at 30. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to July 1: $460.731B highest usage since December 31.

US SOFR/TREASURY OPTION SUMMARY

Decent SOFR & Treasury option volumes reported Wednesday, mixed trade with low delta puts outpacing calls by the close. Underlying futures weaker but off lows. Projected rate cut pricing cools slightly vs. late Tuesday (*) levels: Jul'25 at -1.2bp, Sep'25 at -16bp (-16.4bp), Oct'25 steady at -28.7bp, Dec'25 at -44.8bp (-45.6bp).

SOFR Options:

+20,000 SFRU5 95.75/95.81/95.93/96.00 call condors 2.12-2.25

+3,000 0QZ5 97.25/97.75/98.00 1x3x2 call flys 4.0 ref 96.825

+14,000 SFRZ5 95.75/95.87/96.25/96.37 put condors 5.75-6.0

+5,000 SFRU5 95.87/96.12 call spds 1.25 over 95.62/95.75 put spds ref 95.835

+5,000 SFRU5 95.87/96.00/96.12 call flys w/ 95.62/95.75 2x1 put spds, 5.5

2,000 SFRU5 95.62/96.00 strangles

-2,000 2QQ5/2QU5 96.37 puts, 1.75 ref 96.77

-5,000 0QU5 97.50/98.50 call spds vs. 2QU5 97.50/98.00 call spds, 0.75 flattener

-5,000 0QU5/2QU5 97.50/98.50 call spds, 0.75

-4,000 SFRQ5/SFRU5 96.00 call spds, 1.25 ref 95.835

Block/screen, +44,265 SFRQ5 95.62 put, cab (reduced from 103k)

Block/screen, +8,284 0QQ5 97.00/97.25 call spds, 3.0

2,000 0QZ5 98.00 calls ref 96.865

2,000 SFRX5 96.31/96.50 call spds ref 96.11

7,200 SFRU5 95.62/95.68 2x1 put spds, 0.5 ref 95.835

10,000 0QQ 96.87 calls ref 96.785

3,000 SFRU5 96.00/96.37 call spds, 1.75 vs. 95.845/0.05%

+2,000 SFRU5 96.00/96.25 call spds, 1.5 vs. 95.845/0.05%

Treasury Options:

4,300 TYU5 110.5/112 call spds, 46 ref 111-05.5

over 17,400 FVU5 108.5 calls ref 108-14.5 to -14.75

+2,000 TYQ5 111 straddles, 26

+2,000 TYQ5 111/111.5 1x2 call spds, 10

-1,500 TYU5 111/112.5 call spds, 34 vs. 111-05.5/0.32%

-1,500 wk5 TY 111 puts, 20 vs. 111-02.5/0.43%

-1,500 TYU5 109 puts, 7

MNI BONDS: EGBs-GILTS CASH CLOSE: Late Tariff Surprise Sinks Bunds, Gilts Pre-ECB

EGBs and Gilts weakened Wednesday, with bear steepening in the German and UK curves.

- Core yields had gapped higher to start the day on positive trade news (US-China, US-Japan developments) and a poor 40-year Japanese bond auction, but were broadly flat/lower over the course of the session as concerns lingered over EU countermeasures against proposed US tariffs.

- That seemingly set yields on course to rise modestly for the day, with slight bear steepening. But there was a late twist when just before the cash close, the Financial Times reported that the EU and US were close to reaching a trade deal (including 15% tariffs on US imports from the EU) which would stave off a harsher regime being imposed from Aug 1.

- That news saw core EGB and Gilt yields spike to their highest levels of the day into the close, and judging from futures would have headed higher yet.

- The bear steepening move in the German and UK curves was reinforced, with Gilts underperforming on the day.

- As we noted in our latest Europe Pi update (PDF Here), longs have been building going into the ECB decision which may have helped exacerbate the move.

- Periphery/semi-core spreads tightened smartly into the close as well, leaving them tighter on the day led by Spain and Portugal.

- Thursday's calendar highlights are July flash PMIs and of course the ECB decision.

- MNI's ECB preview is here - we will be closely watching Lagarde's characterisation of risks at the press conference, which will likely shape the market reaction.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 3.2bps at 1.844%, 5-Yr is up 4.2bps at 2.194%, 10-Yr is up 4.9bps at 2.639%, and 30-Yr is up 5.6bps at 3.173%.

- UK: The 2-Yr yield is up 3.9bps at 3.881%, 5-Yr is up 4.7bps at 4.044%, 10-Yr is up 6.6bps at 4.635%, and 30-Yr is up 8.2bps at 5.482%.

- Italian BTP spread down 2.1bps at 82.3bps / Spanish down 2.5bps at 58.9bps

MNI EGB OPTIONS: Schatz, Euribor / Sonia Call Structures Feature Wednesday

Wednesday's Europe rates/bond options flow included:

- DUQ5 107.40/107.50/107.60 call fly paper paid 0.75 on 2K

- DUU5 107.00/107.20/107.40 call fly paper paid 5.5 on 4K

- ERZ5 98.25/37/50/62 call condor paper paid 3 on +6.5K

- SFIZ5 96.60/96.85/97.10 call fly vs. SFIZ5 96.05 puts paper buys the puts back vs. selling the calls fly package trades for 1.00 & 1.25 on 10K

MNI FOREX: Antipodean FX Outperforms Amid Resolute Equities

- AUD and NZD remain the clear outperformers on Wednesday, benefitting from the buoyant price action for major equity benchmarks on the back of a US/Japan trade deal being reached overnight. Renewed bearish dollar sentiment this week is underpinning the move higher for antipodean FX, with the latest comments from Tsy Sec Bessent stating that negotiations with China are on track also providing a tailwind.

- Specifically for AUDUSD, spot pierced a cluster of daily highs to reach a fresh recovery high of 0.6601. The renewed strength has been bolstered by the pair failing to close below its 50-day EMA, keeping the bullish trend setup intact. Above 0.66, resistance is scant until 0.6688, the Nov 07 high, printed shortly after the US election last year. Additionally, 0.6700 represents the 76.4% retracement of the Sep 30 ‘24 - Apr 9 bear leg.

- Following a very volatile APAC trading session, USDJPY traded with a moderately dovish bias across Wednesday, reaching a new weekly low of 146.11. Spot has since bounced back to unchanged levels as markets continue to assess the offsetting forces of a Japan/US trade deal and the uncertain future of PM Ishiba. Today’s low came within 23 pips of key 50-day EMA support, which now intersects at 145.88.

- The euro received a boost in late European trade as financial times reported that the EU and US are closing in on a trade deal that would impose just 15% tariffs on European imports, similar to the agreement Donald Trump struck with Japan this week. EURUSD had been trading in negative territory prior to the headlines, but rose to a fresh weekly high of 1.1761 in the aftermath.

- Overall, EURUSD has operated in a contained range as we approach tomorrow’s flash PMI data and the ECB decision and press conference. Bullish trend conditions continue to prevail with focus remaining on 1.1829, the Jul 1 high and the bull trigger.

EQUITIES

MNI US STOCKS: Late Equity Roundup: SPX Eminis New Highs, US/EU Trade Deal or Not

- Stocks continued to pull higher late Wednesday, SPX emini new record of 6393.75, Nasdaq near Monday's record high of 21077.37, while the DJIA still has a ways to go to breach December 4 '24 high of 45073.63.

- Currently, the DJIA trades up 472.62 points (1.06%) at 44973.58, S&P E-Minis up 44.25 points (0.7%) at 6391, Nasdaq up 114.9 points (0.5%) at 21007.38.

- The two main drivers for the rally were better than expected earnings from a wide swath of stocks (still early in the current cycle) and optimism over trade deals after Pres Trump announced a sweeping trade deal with Japan late Tuesday.

- Stocks climbed to new highs after Financial Times article posited the US & EU "close in on 15% tariff deal". Brief second half consolidation: Treasuries bounced off lows while stocks continued to extend highs even after WH official Peter Navarro saying to take the US/EU deal story "with a grain of salt".

- Industrials, Health Care and Energy sector shares continued to lead gainers in the second half: Lamb Weston Holdings +16.74%, GE Vernova +13.90%, TE Connectivity +11.37%, Baker Hughes +10.83%, Thermo Fisher Scientific +10.77%, General Motors +7.92%, Lennox International +7.58%, General Dynamics +6.30% and Moderna +6.29%.

- Other laggers outside of Tech included: Enphase Energy -14.12%, NextEra Energy -6.29% and EQT -4.84%, Albemarle -5.50% and Fiserv -15.56%

- Earnings expected after today's close: T-Mobile US, Mattel, Chipotle Mexican Grill, Molina Healthcare, CSX Corp, O'Reilly Automotive, Tesla, ServiceNow, Crown Castle, United Rentals, Rollins, QuantumScape, Alphabet, Alaska Air, Las Vegas Sands, Viking Therapeutics, IBM, and Valero Energy Corp.

MNI EQUITY TECHS: E-MINI S&P: (U5) Northbound

- RES 3: 6439.88 1.500 proj of the May 23 - Jun 11 - 23 price swing

- RES 2: 6402.44 1.382 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6393.75 Intraday high Jul 23

- PRICE: 6388.00 @ 1515 ET Jul 23

- SUP 1: 6288.25 Low Jul 17

- SUP 2: 6264.70/6120.59 20- and 50-day EMA values

- SUP 3: 6075.25 Low Jun 24

- SUP 4: 5959.00 Low Jun 23

S&P E-Minis have traded to a fresh cycle high this week. The climb confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Note that moving average studies are in a bull-mode position highlighting a clear dominant uptrend. Sights are on 6381.50, a Fibonacci projection. Key support is at the 50-day EMA, at 6120.59. Support at the 20-day EMA is at 6264.70.

MNI COMMODITIES: Gold Falls As Trade Tensions Ease, Crude Edges Down, Copper Rallies

- Spot gold has fallen by 1.1% to $3,394/oz on Wednesday, as trade concerns eased with the US announcing a trade deal with Japan and progress on talks with the EU.

- The EU and US are closing in on a trade deal that would impose 15% tariffs on European imports, the FT wrote.

- A bull cycle in gold that started June 30 remains intact, however, with the yellow metal still 1.3% higher on the week. A continuation higher would open $3,451.3, the June 16 high.

- Initial firm support to watch is $3,282.8, the July 9 low.

- Meanwhile, crude has been steady today, with WTI Sep 25 broadly unchanged at $65.3/bbl.

- A bearish theme in WTI futures remains intact, with the sharp reversal from the June 23 high continuing to highlight scope for an extension lower. Support to watch is the 50-day EMA, at $64.70. This average has been pierced, and a clear break of it would expose $58.17, the May 30 low.

- Initial resistance to monitor is $69.41, the 50.0% retracement of the Jun 23 - 24 high-low range.

- Elsewhere, copper has rallied by a further 1.9% to $583/lb, taking gains this week to 4%, amid ongoing uncertainty about the potential 50% copper tariff.

- Copper futures remain bullish, with price briefly piercing the July 8 high at $589.55 earlier today. Above here, sights are on the $600.0 handle.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 24/07/2025 | 0600/0800 | * | GFK Consumer Climate | |

| 24/07/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 24/07/2025 | 0700/0900 | ** | PPI | |

| 24/07/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 24/07/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 24/07/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 24/07/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 24/07/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 24/07/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 24/07/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 24/07/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 24/07/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 24/07/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 24/07/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 24/07/2025 | 1100/0700 | *** | Turkey Benchmark Rate | |

| 24/07/2025 | 1215/1415 | *** | ECB Deposit Rate | |

| 24/07/2025 | 1215/1415 | *** | ECB Main Refi Rate | |

| 24/07/2025 | 1215/1415 | *** | ECB Marginal Lending Rate | |

| 24/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 24/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 24/07/2025 | 1230/0830 | ** | Retail Trade | |

| 24/07/2025 | 1230/0830 | ** | Retail Trade | |

| 24/07/2025 | 1245/1445 | ECB Press Conference | ||

| 24/07/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 24/07/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 24/07/2025 | 1400/1000 | *** | New Home Sales | |

| 24/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 24/07/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 24/07/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 24/07/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 24/07/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 10 Year Note | |

| 25/07/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 25/07/2025 | 2330/0830 | ** | Tokyo CPI |