MNI ASIA MARKETS ANALYSIS: Stocks Up, Yields Mixed On FOMC Eve

HIGHLIGHTS:

- Short-End Yields Underperform On US Curve Ahead Of Wednesday's Fed Decision

- Notable Sterling Weakness Sees EURGBP Surge to Cycle Highs

- Equities Hit Fresh Highs; Crude Oil, Gold Pull Back

US TSYS: Light Bear Flattening On FOMC Eve

Treasury cash yields were little changed Tuesday, with anticipation building ahead of Wednesday's likely Fed cut and possible decision to end QT.

- Yields rose to session highs in early trade alongside a strong equity cash open (the S&P 500 rose to a fresh all-time high above 6,900 on tech strength), but soon faded to trade relatively flat on the session.

- A poor 7Y Note sale (0.8bp tail) ended the month's auction schedule on a sour note, but there was little broader market reaction.

- In data, Conference Board consumer confidence was mixed, with the headline index deteriorating less acutely than expected and the "labor differential" stabilizing after a multi-year low posted in the prior month - suggesting little additional urgency for the Fed to cut rates to buoy employment.

- On that front we also got a surprise announcement from ADP that they would henceforth produce a weekly private payrolls update, the first of which showed a solid-by-recent-standards 57k gain in the 4 weeks to Oct 11, potentially underpinning cautious sentiment in rates.

- The short-end underperformed overall in a slight bear flattening move, with Fed funds implied holding about 1.5bp higher on the session covering FOMC meetings through next June. This came as effective Fed funds ticked up another 1bp Monday, mitigating the signal derived from futures for actual rate moves.

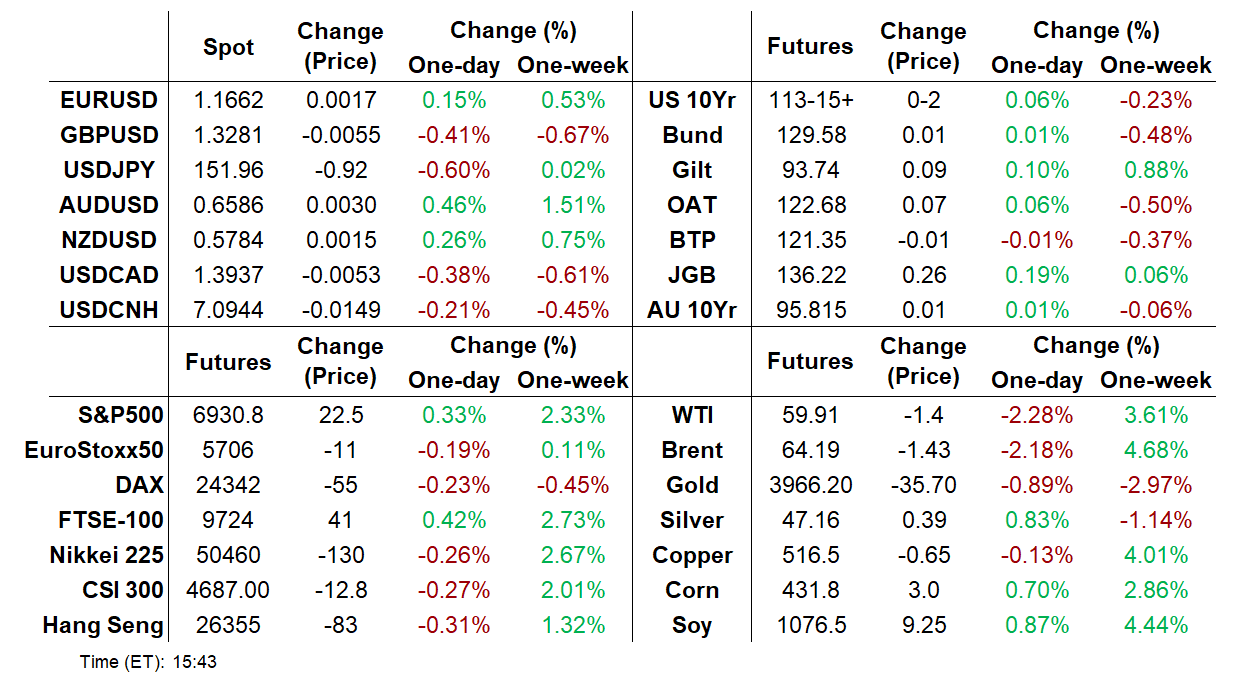

- Cash levels in late afternoon NY trade: the 2-Yr yield is up 0.6bps at 3.488%, 5-Yr is up 0.2bps at 3.606%, 10-Yr is down 0.2bps at 3.9776%, and 30-Yr is down 0.5bps at 4.5474%. In futures, Dec 10-Yr (TY) up 1.5/32 at 113-15 (L: 113-9.5 / H: 113-18.5) amid solid though unremarkable volumes.

- The FOMC decision at 1400ET with Chair Powell press conference a half hour later is Wednesday's main event, though earlier in the session we will get weekly MBA mortgage applications and pending home sales data as well as the Bank of Canada decision (25bp cut expected).

- As noted in our preview, MNI's base case is for an immediate end to QT to be announced Wednesday alongside the well-priced 25bp rate cut. PDF here

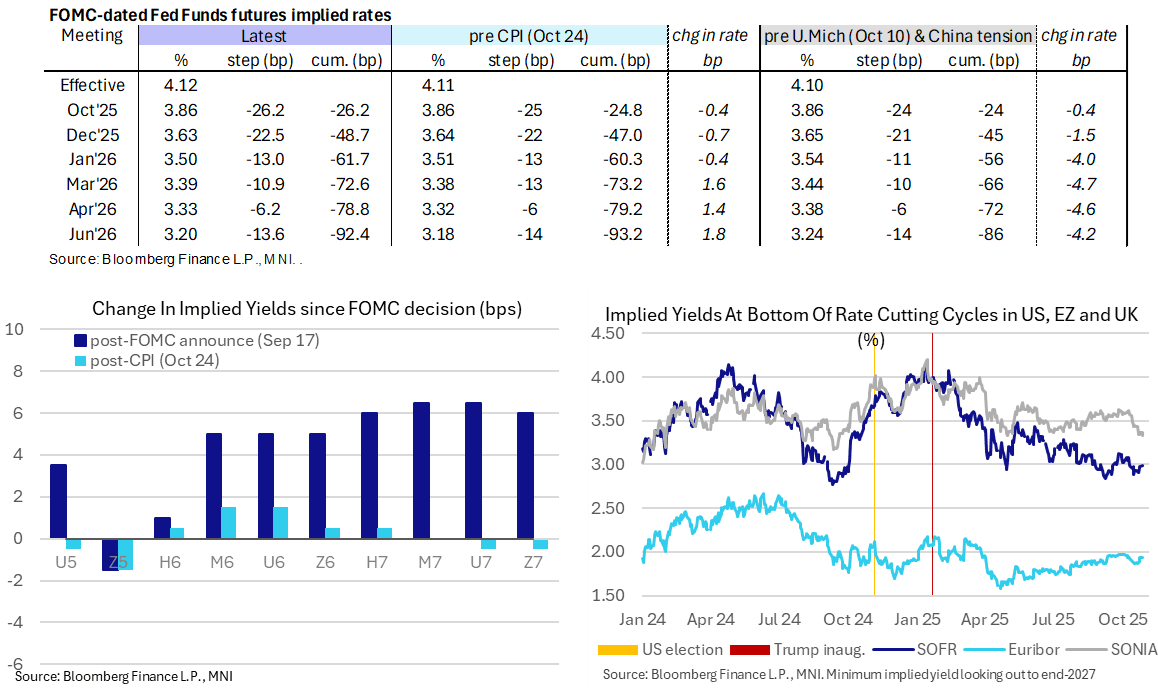

STIR: Fed Terminal On Track To Close At Joint High Since Renewed China Tensions

- Fed Funds implied rates are holding earlier increases, 1.5bp higher on the day across Dec-Jun 2026 meetings.

- The moves were possibly helped by new ADP weekly data crudely pointing to private payrolls gains worth 57k over the latest four weeks along with equity indices pushing onto new record highs.

- Ahead of tomorrow’s FOMC decision, markets still broadly eye back-to-back cuts before a shift to a quarterly pace with a subsequent cut in March, but with slightly less conviction on a June cut.

- Cumulative cuts from 4.12% effective: 26bp for tomorrow, 48.5bp Dec, 61.5bp Jan, 72.5bp Mar, 79bp Apr and 92.5bp Jun.

- MNI Fed Preview: https://media.marketnews.com/Fed_Prev_Oct2025_With_Analysts_2c9e326366.pdf

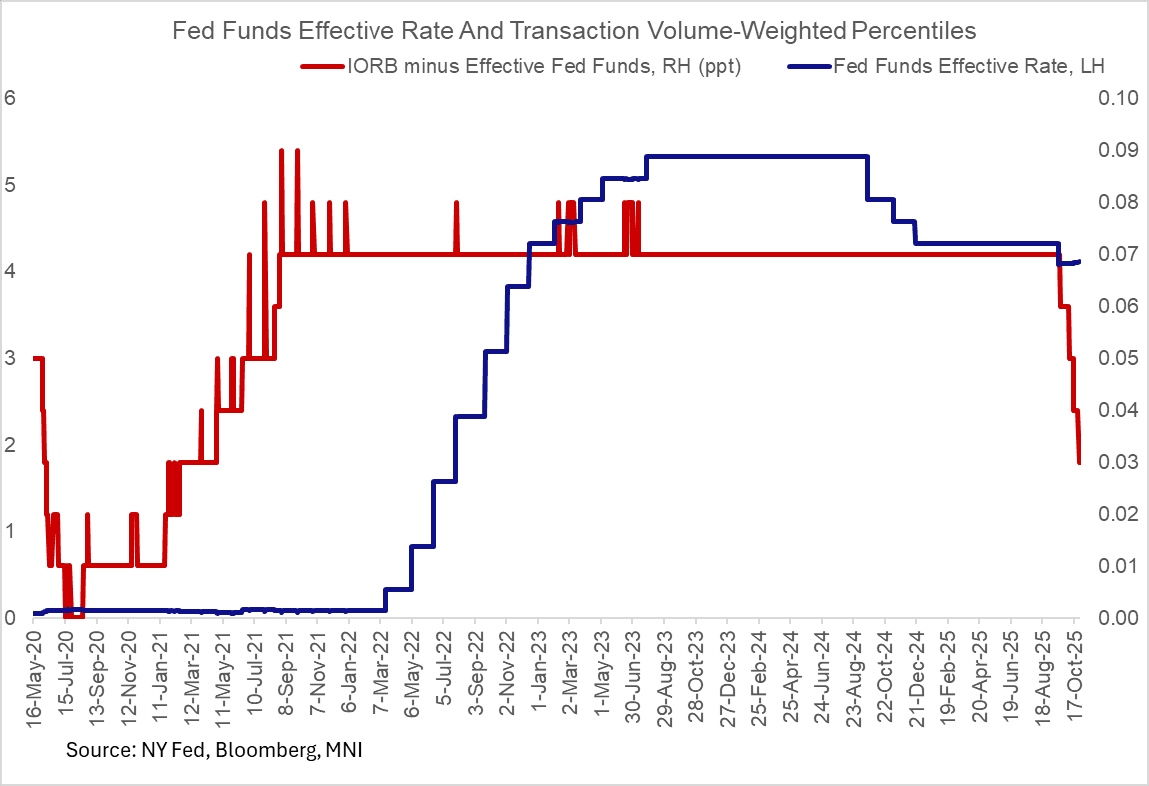

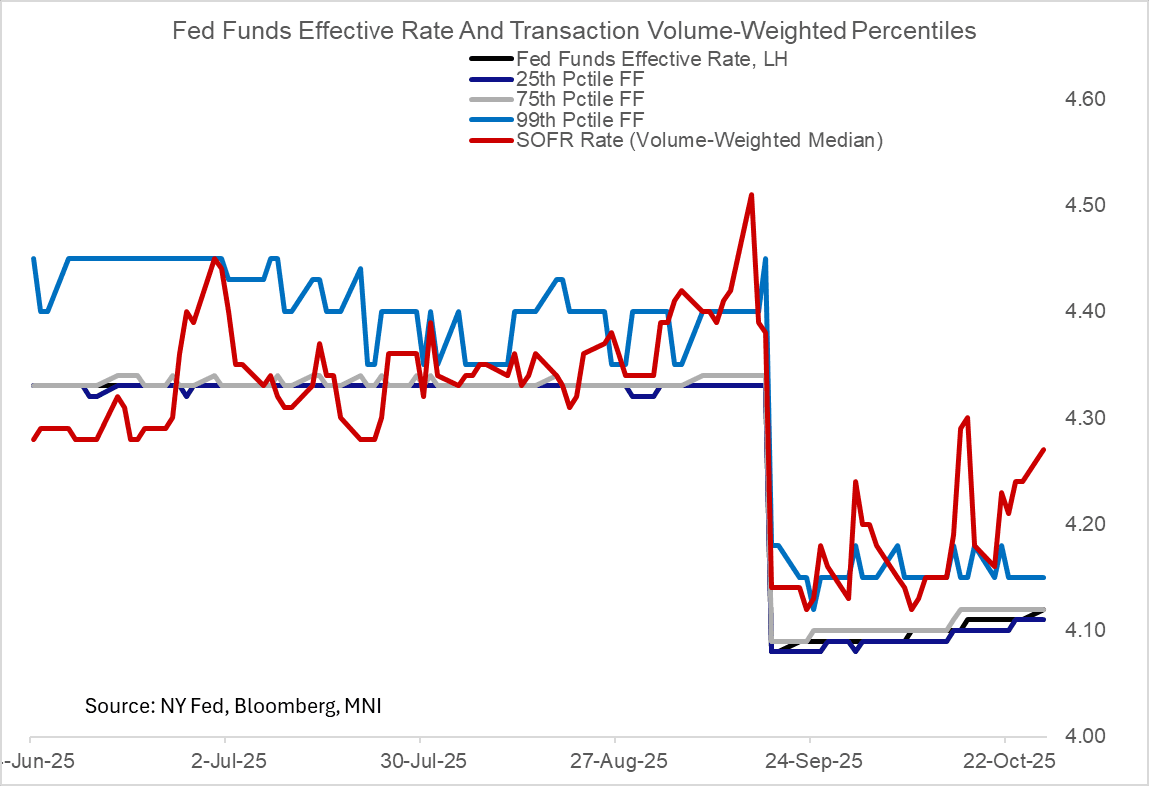

- Note the latest 1bp increase to a 4.12% EFFR yesterday, a semi-surprise being the fourth increase since the September FOMC meeting. That's just 3bp below IORB after having been consistently 7bp below for most of the cycle. This move has been flagged as a risk for several sessions now, with the EFFR percentiles ticking higher.

- SOFR futures meanwhile have seen a larger paring of earlier losses and currently range between 1.5 tick lower (H6) to 1 tick higher (Z7).

- The SOFR implied terminal yield of 2.99% (H7) is unchanged on the day, at its joint highest close since Oct 9 i.e. since the increase in US-China trade tensions on Oct 10.

MNI ANALYSIS

MNI ECB Preview: Enjoying The Good Place

- We have published and e-mailed to subscribers the MNI ECB Preview, including MNI analysis plus analyst views on what to expect at this month's meeting.

- Please find the full report here: https://media.marketnews.com/ECB_Preview_Oct2025_307fe9619a.pdf

NETHERLANDS: MNI Publishes Election Preview

- Download Full Report Here: https://media.marketnews.com/MNIPOLITICALRISK_Netherlands_Election_Preview_Oct25_add1c6bd94.pdf

- Dutch voters go to the polls on 29 October in a snap general election to elect the 150 members of the lower chamber of the Dutch parliament, the House of

Representatives. In this preview, we provide a rundown of the main political parties, an explanation of the electoral system and government formation

process, a chart pack of opinion polling and prediction market odds, hypothetical post-election scenarios with assigned probabilities, and sell-side

analyst views of the contest.

US TSYS/OVERNIGHT REPO: Rate Uptick Bolsters Case For QT End This Week

Money market / repo rates showed a notable uptick Monday, with the prints landing just as the FOMC sat down for its 2-day meeting to decide the next move on balance sheet runoff. SOFR, BGCR, and TGCR all rose 3bp, remaining stubbornly above the Fed's IORB rate suggesting that reserves are less ample than they had been.

- A semi-surprise was the 4th increase in the Fed Funds effective rate since the September FOMC meeting, with a 1bp uptick to 4.12%. That's just 3bp below IORB after having been consistently 7bp below for most of the cycle. This move has been flagged as a risk for several sessions now, with the EFFR percentiles ticking higher (the published EFFR is a volume-weighted median of overnight fed funds transactions).

- As we noted in our Fed meeting preview, we expect the FOMC to end balance sheet runoff this week, as it assesses the reserve regime to have moved from "abundant" to at/near "ample" - the latest rate moves only reinforce the likelihood of a QT end.

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.27%, 0.03%, $3019B

* Broad General Collateral Rate (BGCR): 4.24%, 0.03%, $1131B

* Tri-Party General Collateral Rate (TGCR): 4.24%, 0.03%, $1103B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.12%, 0.01%, volume: $88B

* Daily Overnight Bank Funding Rate: 4.11%, no change, volume: $176B

US OPTIONS: US Options Roundup - Oct 28 2025

Tuesday's US rates/bond options flow included:

- TY (14th Nov) 112.50p, sold at '02 in 27k (weekly option)

- TYZ5 111.50p, bought for '03 in 10k.

- SFRZ5 96.375/96.50cs 1x2, bought for 0.5 in 2k.

- SFRZ5 96.56/96.68cs, traded for 0.75 in 2.5k.

- SFRZ5 96.50/96.62cs, traded for 1 in 10k.

- SFRZ5 96.43/96.50/96.56c fly, traded for 0.25 in 5k.

- SFRH6 96.75c, sold at 7.75 in 2k.

- SFRH6 96.62/96.87cs 1x2, bought for 0.25 in 2.5k (traded on Screen).

- SFRM6 96.75 Straddle, bought for 40.5 in 1.5k.

- 0QH6 96.87/97.25/97.62c fly 1x3x2, bought for 1.5 in 4k (traded on Screen).

- 0QX5 97.25/97.375 cs traded for 1 in 2.5k (block trade).

- 0QH6 97.00/96.62ps 1x2, traded for 8 in 1k.

- 2QH6 96.87c, bought for 18 in 20k.

BONDS: EGBs-GILTS CASH CLOSE: Gilt Outperformance Continues

European yields closed mostly flat/lower Tuesday, with Gilts notably outperforming once again.

- EGBs appeared weighed down for most of the session with supply a key theme (Germany, Finland, Italy all issuing). Gilts gained despite a late selloff ahead of the cash close on no discernable trigger.

- Cash 10Y Gilts outperformed Bunds for the 11th session in 12, with soft food inflation signs in the latest BRC shop price monitor the latest development aiding sentiment. The 10Y Gilt/Bund spread saw its tightest close since Sept 2024 (177.68bp).

- Overall the German curve leaned bear steeper, with the UK's bull steepening. Periphery/semi-core EGB spreads to Bunds tightened modestly.

- In data, ECB 1/3/5-year consumer expectations were steady at 2.7%, 2.5% and 2.2% respectively.

- The Federal Reserve meeting is the highlight of the global agenda Wednesday ahead of Thursday's ECB decision (as well as the BOJ decision, and Eurozone inflation/GDP data).

- MNI's ECB preview went out today (link) - no change in rates is expected, with attention on the communication of the balance of risks.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.3bps at 1.975%, 5-Yr is up 0.5bps at 2.233%, 10-Yr is up 0.7bps at 2.623%, and 30-Yr is up 0.2bps at 3.191%.

- UK: The 2-Yr yield is down 0.8bps at 3.773%, 5-Yr is down 1bps at 3.873%, 10-Yr is down 0.2bps at 4.4%, and 30-Yr is down 0.7bps at 5.174%.

- Italian BTP spread down 0.5bps at 77.2bps / French OAT down 0.2bps at 79.9bps

EUROPE OPTIONS: Further Rate Call Spread Buying Alongside Large Sonia Put Condor

Tuesday's Europe rates/bond options flow included:

- ERH6 98.0625/98.25cs, bought for 3.5 in 10k

- ERM6 98.12/98.25cs vs 97.9375p, bought the cs for 0.5 in 2k

- SFIZ5 96.30/96.20/96.15/96.05p condor, bought for 4 in 15k

- SFIH6 96.90/97.00cs, bought for 0.75 in 1.5k

- SFIH6 96.35/96.25ps 1x2, bought for 0.25 in 1.5k

FOREX: Notable Sterling Weakness Sees EURGBP Surge to Cycle Highs

- Renewed pessimism for GBP has been on show Tuesday, amid increasing signs that UK Chancellor Reeves will have to raise income tax at the November 26 budget to fill a widening fiscal hole. Furthermore, the FT reported yesterday evening that the OBR is expected to cut its trend productivity forecast by a larger-than-expected 0.3pp, providing an additional sterling headwind.

- While GBPUSD is down 0.42% on the day, EURGBP has had a more notable 0.6% move, rising to the highest level since 2023. Momentum picked up on a break of key resistance at 0.8769, and a close above this level would bolster bullish trend conditions. Topside targets for the move include 0.8835 and 0.8875, the April 2023 high.

- Strength for the major equity indices have weighed significantly on the likes of GBPAUD (through 2.0244 to print new multi-month lows) and GBPCAD (through 1.8561 to new multi-week lows). For AUDUSD specifically, Tuesday gains put the price through 0.6574 Fib resistance, tilting the near-term outlook bullish toward 0.6629 next, a key short-term level.

- Despite two-way price action for USDJPY across the European and US sessions, the pair is holding onto initial losses that were sustained during APAC hours. The positive yen impulse was provided by optimism surrounding official US-Japan talks. Treasury Secretary Bessent emphasized the need for sound monetary policy to keep inflation expectations anchored and avoid FX volatility.

- USDJPY is currently down 0.45%, with the 151.76 session lows marking a 1% correction from yesterday’s highs of 153.26. First important support to watch lies at 151.09, the 20-day EMA.

- Australia Q3 CPI headlines the economic data calendar on Wednesday, before the focus turns to BOC and Fed rate decisions.

COMMODITIES: Crude, Gold Pull Back

- Crude has fallen today as the market looks to tomorrow’s Fed decision and Sunday’s OPEC meeting. US/China trade optimism is being weighed against oversupply concerns while the market continues to monitor the impacts of US sanctions on Russian supply.

- WTI Dec 25 is down by 2.2% at $60.0/bbl.

- OPEC meets on Sunday to decide the December output target which could rise again, although there is little spare capacity outside Saudi Arabia. The group is leaning towards another modest output boost, four Reuters sources said.

- For WTI futures, initial support is at $59.64, the Oct 23 low, with key support and the bear trigger at $55.96, the Oct 20 low.

- Initial resistance is at $62.59, the Oct 24 high.

- Meanwhile, spot gold has fallen further today, with price briefly piercing the $3,900/oz level, before paring the move.

- Currently, gold is down by 0.7% at $3,956.

- Spot is now down by almost 10% from last week's all-time highs of $4,381.5, with the easing of US/China trade tensions being cited as a driver of the pullback.

- The move has seen support at the 20-day EMA, at $4,037.0, breached this week, signalling scope for a deeper retracement, towards the 50-day EMA, at $3,842.7.

- Initial resistance is at $4,161.4, the Oct 22 high.

| Date | GMT/Local | Impact | Country | Event |

| 29/10/2025 | - | Bank of Japan Meeting | ||

| 29/10/2025 | 0001/0001 | * | Brightmine pay deals for whole economy | |

| 29/10/2025 | 0030/1130 | *** | CPI Inflation Monthly | |

| 29/10/2025 | 0030/1130 | *** | CPI inflation | |

| 29/10/2025 | 0700/0800 | Flash Quarterly GDP Indicator | ||

| 29/10/2025 | 0700/1500 | ** | MNI China Money Market Index (MMI) | |

| 29/10/2025 | 0800/0900 | *** | GDP (p) | |

| 29/10/2025 | 0930/0930 | ** | BOE Lending to Individuals | |

| 29/10/2025 | 0930/0930 | ** | BOE M4 | |

| 29/10/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 29/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 29/10/2025 | 1100/1200 | ** | PPI | |

| 29/10/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 29/10/2025 | 1345/0945 | *** | Bank of Canada Policy Decision | |

| 29/10/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 29/10/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 29/10/2025 | 1430/1030 | BOC press conference | ||

| 29/10/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 29/10/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 29/10/2025 | 1800/1400 | *** | FOMC Statement |