MNI ASIA MARKETS ANALYSIS: Stocks Extend New Record Highs

HIGHLIGHTS

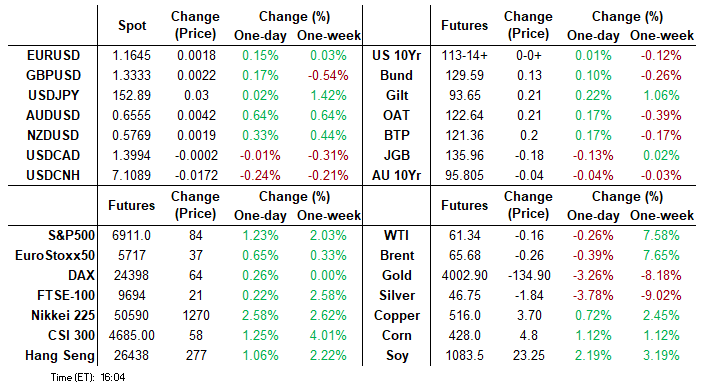

- US Treasuries look to finish mixed, curves flatter (5s30s -3.807 at 94.768) with bonds leading a rebound off morning lows Monday, the 27th day of the US Govt shutdown.

- Focus on Wednesday's FOMC - overwhelmingly expected to cut the funds rate by 25bp for a 2nd consecutive meeting on October 29, bringing the target range to 3.75-4.00%.

- Stocks continue to drift at/near record highs late Monday, sentiment buoyed amid trade optimism between the US & China.

- Higher core yields and the sharp gains for major equity benchmarks initially weighed on the Japanese Yen, with USDJPY extending its most recent rally ahead of the European open to trade within one pip of the key 153.27.

US TSYS

MNI US TSYS: Bonds Reverse Early Weakness, Curves Twist Flatter Ahead Wed's FOMC

- Treasuries are mixed after the bell, curves flatter (5s30s -3.996 at 94.579) with bonds outperforming - leading a bounce off midmorning lows; 27th day of the US Govt shutdown.

- Currently, Dec'25 TY contract trades -1 at 113-13 vs. 113-14.5 high, 10Y yield -.0097 at 3.9910%. A bullish structure in Treasuries remains intact and recent weakness appears to be a correction. The breach of a key resistance at 113-29, the Sep 11 high, confirmed a resumption of the medium-term uptrend.

- Spot Gold is now down 10% from last week’s all-time highs of $4,381.5, with an easing of US/China trade tensions being cited as the driver of today’s pullback. While the USD index came under some pressure, the sharp unwind for spot gold has offset the greenback pessimism somewhat

- Focus on Wednesday's FOMC - overwhelmingly expected to cut the funds rate by 25bp for a 2nd consecutive meeting on October 29, bringing the target range to 3.75-4.00%.

- Projected rate cut pricing vs. late Friday levels (*): Oct'25 at -24.5bp (-24.2bp), Dec'25 at -48.1bp (-50.2bp), Jan'26 at -61bp (-63.7bp), Mar'26 at -72.7bp (-75.8bp).

- Stocks continue to drift at/near record highs late Monday, sentiment buoyed amid trade optimism between the US & China. Officials from the two countries have reached basic consensus on arrangements to address their respective trade concerns following two days of talks in Kuala Lumpur, the People’s Daily reported.

- Earnings expected after the close include Whirlpool Corp, Alexandria Real Estate, Olin Corp, Waste Management, Nucor Corp, Brown & Brown, Welltower, Avis, Cadence, F5 and Amkor Technology.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.24% (+0.00), volume: $3.000T

- Broad General Collateral Rate (BGCR): 4.21% (+0.00), volume: $1.136T

- Tri-Party General Collateral Rate (TCR): 4.21% (+0.00), volume: $1.111T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.11% (+0.00), volume: $90B

- Daily Overnight Bank Funding Rate: 4.11% (+0.00), volume: $180B

FED Reverse Repo Operation

RRP usage climbs to $10.642B with 13 counterparties this afternoon from $2.435B Friday (lowest level since mid-March 2021). Compares to this year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR/Treasury options flow leaning toward downside puts outright & spread, modest overall volumes on day 27 of the US gov shutdown. Off first half lows, underlying futures are mixed, curves flatter with bonds outperforming (5s30s -3.175 at 95.400). Projected rate cut pricing vs. late Friday levels (*): Oct'25 at -24.5bp (-24.2bp), Dec'25 at -48.1bp (-50.2bp), Jan'26 at -61bp (-63.7bp), Mar'26 at -72.7bp (-75.8bp).

SOFR Options

Block, 8,000 SFRZ5 96.50/96.56 call spds, 0.50 ref 96.36

Block, 8,000 SFRZ5 96.50/96.62 call spds, 0.50 ref 96.36

Block, 8,000 SFRZ5 96.43/96.50 call spds, 0.75 ref 96.36

+20,000 SFRH6 96.62/96.75/97.25 broken call trees, 0.75

+20,000 SFRZ5 96.50/96.62 call spds, 1.0 ref 96.36

+4,000 2QH6 96.25/96.43/96.62 put trees, 1.75

9,000 SFRZ5 96.25/96.37/96.50 put trees, 7.5

-2,000 0QX5 96.25/96.75/96.87 put flys, 1.5 vs. 96.97/0.08%

2,500 0QX5 96.75 puts, 0.25 ref 97.005

+2,200 SFRX5 96.50/96.56 call spds, 0.25 ref 96.36

Treasury Options

20,000 wk5 FV 108.75/109/109.25/109.5 put condors (exp 10/31)

7,646 TYH6 107.5/109/110.5 put flys ref 113-03

2,000 TYF5/TYG5 112 put spds, 13 ref 113-03

2,000 USZ5 118/119/120/121 call condors, 118-09

16,900 Friday wkly 10Y/TYZ5 113 put spd

2,000 TUF6 104/104.25/104.38/104.5 put condors ref 104-14.75

+1,250 TYZ5 114 straddles, 119 vs. 113-06/0.43%

+1,500 TYZ5 112 calls, 126 vs. 113-09/0.87%

+2,500 TYZ5 112.5 puts, 15 vs. 113-09/0.28%

-1,200 TYZ5 113.25 straddles, 106-107 vs. 113-05.5/0.05%

over -8,000 wk5 TY 113 puts, 10-11, (exp 10/31)

-5,000 USZ5 116/118 put spds, 46 vs 117-28/0.28%

-2,700 TUG6 104.5 straddles, 34-33

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilt Yields Resume Descent

European bonds broadly gained ground on Monday.

- Core EGBs and Gilts were pressured early by news of a potential China-US trade breakthrough over the weekend, spurring a broad risk-on move.

- But the sell-off petered out by late morning, with yields descending in orderly fashion throughout the rest of the session with no clear driver, ahead of month-end and the ECB decision/Eurozone data later this week.

- In a session with limited data, German IFO came in mixed (current assessment missed, expectations beat).

- On the day, the German curve twist flattened with the UK's bull flattening. Gilts performed overall, carrying through from last week's outperformance.

- OAT spreads moved largely in line with other semi-core EGBs despite a modicum of relief from Friday's lowering of France's outlook by Moody's, as opposed to a fall in the credit rating itself.

- Tuesday's schedule includes the ECB Bank Lending Survey and CPI expectations, though that's not expected to have any impact on the ECB's expected rate hold Thursday. Otherwise the week's highlight is the Eurozone October flash inflation round, with the ECB in its pre-meeting media blackout period. is on the quiet side in the UK (our weekly outlook is here).

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.4bps at 1.972%, 5-Yr is down 0.3bps at 2.228%, 10-Yr is down 1bps at 2.616%, and 30-Yr is down 1.7bps at 3.189%.

- UK: The 2-Yr yield is down 1.8bps at 3.781%, 5-Yr is down 1.9bps at 3.883%, 10-Yr is down 3bps at 4.402%, and 30-Yr is down 3.8bps at 5.181%.

- Italian BTP spread down 1.3bps at 77.7bps / French OAT down 0.7bps at 80.1bps

MNI OPTIONS: Rates Trade Remains Brisk, Slightly More Mixed Vs Recent Upside Slant

Monday's Europe rates/bond options flow included:

- ERX5 97.9375/97.875ps, bought for 0.5 in 8k

- ERZ5 98.00c, sold at 1.5 in 6k

- ERH6 98.37/98.62cs vs 0RH6 98.37/98.62cs, bought the mid for 1 in 12k total (Short Cover). That structure traded in around 100k back in June

- ERH6 99.25c, bought for 0.25 in 3.4k

- ERH6 98.37/98.62cs vs 0RH6 98.37/98.62cs, bought the mid for 1 in 7k

- ERM6 98.4375/98.50/98.5625c fly, bought for 0.25 in 1.25k.

- ERM6 97.9375/97.75ps, bought for 2 in 8k

- ERM6 98.00/98.0625/98.125/98.1875c condor, bought for 0.25 in ~15k

- SFIX5 96.15/96.20/96.25/96.30c condor, bought for 2 in 10k

- SFIZ5 96.35/96.60cs,sold at 1.5 in 3k

MNI FOREX: AUD Remains Top of G10 Leaderboard amid China Optimism

- Risk sentiment has been buoyed Monday, amid optimism surrounding US-China trade negotiations which comes ahead of Thursday's Trump-Xi meeting. While the USD index came under some pressure, a further sharp unwind for spot gold has offset the greenback pessimism. AUD outperforms all others in G10, most notably impacted owing to its high beta status and sensitivity to the Chinese economy.

- Furthermore, RBA Bullock's comments playing down recent job weakness and mentioning they are in a "pretty good" position on both jobs and CPI added to topside momentum for AUDUSD, which remains 0.65% higher on the session above 0.6550. Today’s boost has strengthened a bullish underlying theme, and spot has narrowed the gap to initial resistance at 0.6574, the 50.0% retracement of the Sep 17 - Oct 14 bear leg.

- Higher core yields and the sharp gains for major equity benchmarks initially weighed on the Japanese Yen, with USDJPY extending its most recent rally ahead of the European open to trade within one pip of the key 153.27. Price action did reverse amid a broader dollar offer ahead of the NY crossover, however, USDJPY’s dip to 152.57 was very short-lived. Spot has returned back above 153.00, and the pair looks set to extend a winning streak to seven consecutive sessions. Clearance of the bull trigger at 153.27 would confirm a resumption of the medium-term uptrend.

- Despite the generally flat USD Index, USDCNH has broken lower today, building on a strong session for China FX overnight. The rate has tested below 7.1050 for the lowest print since September, narrowing the gap with key support into 7.0851, the cycle low. Moves follow the stronger-than-expected CNY fix (7.0881, the lowest in over 12 months), consistent with the bank's long-held push for further internationalization and expanded use - which the bank reiterated on Friday last week after the conclusion of the government's 4th plenum.

- Central banks highlight this week's calendar, with the Bank of Canada and the Fed holding policy meetings on Wednesday, before the Bank of Japan and the ECB follow Thursday.

MNI OPTIONS: Expiries for Oct28 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E874mln), $1.1625-35(E1.9bln)

- USD/JPY: Y152.50($720mln), Y152.95-00($1.0bln), Y153.35-50($609mln)

- AUD/USD: $0.6475(A$573mln)

EQUITIES

MNI US STOCKS: Late Equities Roundup: Drifting At/Near Record Highs

- Stocks continue to drift at/near record highs late Monday, sentiment buoyed amid trade optimism between the US & China. Officials from the two countries have reached basic consensus on arrangements to address their respective trade concerns following two days of talks in Kuala Lumpur, the People’s Daily reported.

- Late headline: Reuters reported that Amazon plans to cut 30,000 corporate jobs, the stock pared gains (+1.12% at 226.72).

- Currently, the DJIA trades up 242.9 points (0.51%) at 47447.96 vs. 47,532.73 record high, S&P E-Minis up 70.0 points (1.03%) at 6897 vs. 6,898.75 record high, Nasdaq up 396.8 points (1.7%) at 23604.15 vs. record high of 23,617.12.

- Communication Services, IT and Consumer Discretionary sector shares continued to lead advances in late trade: QUALCOMM Inc +12.51%, Keurig Dr Pepper +7.68%, Edwards Lifesciences +5.86%, Tesla +5.51%, Robinhood Markets +5.47%, Super Micro Computer +4.91%, Dow Inc +4.33% and ON Semiconductor +3.96%.

- On the flipside, Materials, Utilities and Consumer Staples led declines: miners pressed as spot gold dropped below $4,000/oz (-3.0%): Albemarle -8.10%, Newmont -6.69%, Ford Motor -4.01%, Roper Technologies -3.97%, Revvity -2.97%, United Rentals -2.46% and Archer-Daniels-Midland -2.38%.

- Earnings expected after the close include Whirlpool Corp, Alexandria Real Estate, Olin Corp, Waste Management, Nucor Corp, Brown & Brown, Welltower, Avis, Cadence, F5 and Amkor Technology.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Starts The Week On A Bullish Note

- RES 4: 6953.25 2.000 proj of the Aug 1 - 15 - 20 price swing

- RES 3: 6912.25 3.000 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6900.00 Round number resistance

- RES 1: 6892.50 Intraday high

- PRICE: 6887.25 @ 14:49 GMT Oct 27

- SUP 1: 6812.25/6731.66 High Oct 9 / 20-day EMA

- SUP 2: 6645.22 50-day EMA

- SUP 3: 6540.25 Low Oct 10 and a key short-term support

- SUP 4: 6506.50 Low Sep 5

The trend condition in S&P E-Minis remains bullish and the contract is trading higher today, as it begins the week on a bullish note. The fresh cycle high confirms a resumption of the primary uptrend and maintains the bullish price sequence of higher highs and higher lows. Sights are on the 6900.00 handle next. Initial firm support to watch lies at 6731.66, the 20-day EMA. The 50–day EMA is at 6645.22.

COMMODITIES

MNI PRECIOUS METALS: Spot Gold Below $4,000 And Looking To Close Below 20-day EMA

Spot gold has pierced the $4,000/oz figure and is now down 3.0% on the session, narrowing the gap to support at $3,944.9 (Oct 9 low). A close at current levels would mark the first time gold has closed below the 20-day EMA since mid-August, and signal scope for a deeper retracement towards the 50-day EMA of $3,832.4.

- Spot is now down 10% from last week’s all-time highs of $4,381.5, with an easing of US/China trade tensions being cited as the driver of today’s pullback.

- Last week’s sharp selloff appeared to represent broad-based deleveraging/profit taking after a solid rally since August. Note that CFTC positioning data is still not available due to the US Government Shutdown.

- A corrective cycle in silver is also at play, with spot down 4.4% today at $46.5/oz. Support at the 50-day EMA lies at $45.5. A reminder that silver’s rally to almost $55/oz was exacerbated by a liquidity squeeze in the London physical market. The deeper pullback for silver compared to gold means that long-term trendline support in the Gold/Silver ratio remains intact.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 28/10/2025 | 0700/0800 | * | GFK Consumer Climate | |

| 28/10/2025 | 0900/1000 | ** | ISTAT Consumer Confidence | |

| 28/10/2025 | 0900/1000 | ** | ISTAT Business Confidence | |

| 28/10/2025 | 0900/1000 | ** | ECB Bank Lending Survey | |

| 28/10/2025 | 0900/1000 | ** | ECB Consumer Expectations Survey | |

| 28/10/2025 | 1000/1000 | * | Index Linked Gilt Outright Auction Result | |

| 28/10/2025 | - | FOMC Meeting | ||

| 28/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 28/10/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 28/10/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 28/10/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 28/10/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 28/10/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 28/10/2025 | 1400/1000 | ** | housing vacancies | |

| 28/10/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 28/10/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 28/10/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 29/10/2025 | - | Bank of Japan Meeting | ||

| 29/10/2025 | 0001/0001 | * | Brightmine pay deals for whole economy | |

| 29/10/2025 | 0030/1130 | *** | CPI Inflation Monthly | |

| 29/10/2025 | 0030/1130 | *** | CPI inflation |