MNI ASIA MARKETS ANALYSIS: Stagflationary ISM Services

HIGHLIGHTS

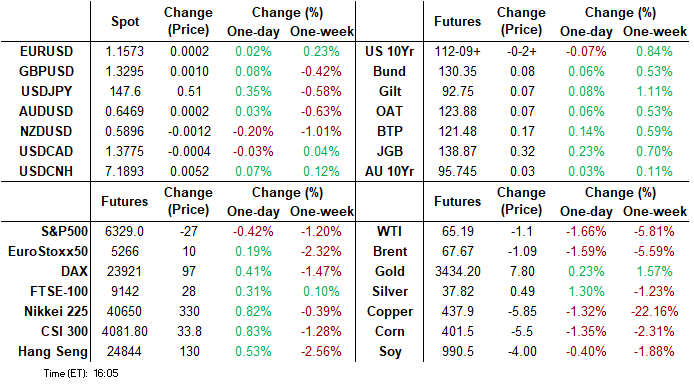

- Treasuries look to finish mixed Tuesday, curves twisting flatter (2s10s -3.513 at 47.995) with 2s-10s lagging modest gains in Bonds.

- July's ISM Services data more "stagflationary" than anticipated, with a dip in activity amid a pickup in price pressures.

- The USD Index remained rangebound Tuesday, however the inability of markets to press the USD lower still after Friday's NFP print may suggest the price is building a base.

- German factory orders, Italian industrial production and the Canadian services PMI data are the data highlights Wednesday. Fed's Cook, Collins and Daly are also set to make appearances.

US TSYS

MNI US TSYS: Tsy Curves Twist Flatter, July ISM Services Data Stagflationary

- Treasuries look to finish mixed Tuesday, curves twisting flatter (2s10s -3.504 at 48.004) w/ 2s-10s down 2.5-4 following stagflationary July's ISM Services data and a weak 3Y auction that drew 3.669% high yield vs. 3.662% WI.

- The headline Services PMI reading fell by 0.7 points to 50.1 (51.5 expected, 50.8 prior), merely a 2-month low but suggesting that an expected pickup in momentum and sentiment is not materializing.

- Meanwhile, S&P Global final PMIs for July were stronger than first thought, with the services PMI further confirming a fresh high since December. The soon to be released ISM Services will provide a useful alternative indicator for services activity in July after undershooting by 2.1pts back in June.

- The USD Index remained rangebound Tuesday, however the inability of markets to press the USD lower still after Friday's NFP print may suggest the price is building a base. The JPY was the poorest performing currency against all others in G10, aiding EUR/JPY to recovery back toward Y171.

- Trump spoke on his possible Fed picks to replace Kugler following her resignation over the weekend. The President declared he had a shortlist of 4, which includes both Kevin Warsh and Kevin Hassett, and while the President said he may use this Fed pick as a precursor to selecting the next Fed chair, he remained vague about the timing of such an announcement.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.33% (-0.01), volume: $2.828T

- Broad General Collateral Rate (BGCR): 4.31% (-0.01), volume: $1.141T

- Tri-Party General Collateral Rate (TCR): 4.31% (-0.01), volume: $1.117T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $117B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $265B

FED Reverse Repo Operation

RRP usage retreats to $84.356B (lowest levels since April 25) this afternoon from $125.730B yesterday, total number of counterparties at 23. Lowest usage of the year at $54.772B on Wednesday, April 16 -- in turn the lowest level since April 2021 - compares to July 1: $460.731B highest usage since December 31.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury call options drove Tuesday volumes, particularly in SOFR via flys and condors centered on Dec'25 to Mar'26 expirys. Underlying futures mixed, curves flatter with 2s-10s weaker after TYU5 climbed to May 30 highs overnight (112-15.5). Projected rate cut pricing pulling back from late Monday (*) levels: Sep'25 at -22.6bp (-22.9bp), Oct'25 at -38.4bp (-39.6bp), Dec'25 at -57.7bp (-59.5bp), Jan'26 at -68.9bp (-71.1bp).

SOFR Options:

Block, 6,500 SFRZ5 95.68 puts, 0.75 ref 96.245

+20,000 SFRZ5 96.25/96.37/96.50/96.62 put condors vs. 95.75/95.87/96.00/96.12 put condor, .25 net

-8,000 0QZ5 97.25/97.50 call spds, 5.62 ref 96.95

+20,000 0QH6 97.25/97.50 call spd w/

+20,000 0QH6 97.25/97.50/97.62 call flys AND

+20,000 0QH6 97.25/97.50/97.75 call flys, paying 13.5-13.75 total on package

-5,000 SFRU5 95.75/95.81/96.06/96.12 iron condors, 2.25 ref 95.94

+65,000 SFRZ5 96.25/96.37/96.50/96.62 call condors, 2.75 ref 96.26

+10,000 SFRU5 96.12/96.18 call spds .87

+10,000 SFRU5 96.18/96.25 call spds .62

-5,000 SFRU6 95.87 puts, 6.0

+1,500 SFRZ5 96.25 straddles, 33.5

8,000 SFRU5 96.06/96.12/96.18 call flys ref 95.935

Block, 12,000 SFRU5 96.00/96.25 call spds 3.25 ref 95.95

over 8,000 SFRU5 96.00 calls, 5.0 last ref 95.935

2,000 SFRU5 95.87/96.00 combos ref 95.935

1,750 0QZ5 97.00/97.12 call spds ref 96.95

9,300 SFRZ5 96.25/96.37/96.50/96.62 call condor ref 96.27 to -.265

1,700 SFRU5 95.75/95.87 put spds, ref 95.935

2,000 SFRU5 95.75/95.81/95.87/95.93 put condors ref 95.945

Treasury Options:

+18,500 wk5 TY 113.25 calls, 20 ref 112-07/0.25%

-3,000 TYU5 112.25 straddles, 108 appr implied vol 5.76%

+3,000 TYQ5 113 calls, 19

1,000 TYV5 104.5/107.5 3x1 put spds ref 112-08.5

7,900 wk2 TY 112 puts, 9 last ref 112-10.5 (exp 08/08)

over 4,200 TYU5 113.5 calls, 13 last

2,500 TYU5 112/113 call spds, 28 ref 112-14

MNI BONDS: EGBs-GILTS CASH CLOSE: Mixed After Initial Rally

EGB and Gilt yields finished up from their intraday highs Tuesday to trade mixed overall.

- Early trade was constructive, with Friday's poor US employment report continuing to buoy core instruments. At the onset of the session, the 10Y Bund yield hit its lowest intraday levels since Jul 23; for Gilts, Jul 2.

- However yields would mostly drift higher from there despite few evident catalysts, as equities and the US dollar pulled back.

- Data was relatively non-impactful. We saw above-expected Spanish and French industrial production alongside slight downward revisions to Eurozone final July services/composite PMIs, with UK services PMI seeing an upward revision. Eurozone June PPI was a touch lower than expected.

- A soft US ISM Services reading saw bonds rally, though a higher prices paid component muted the impact.

- For the session, both the UK and German curves leaned slightly flatter, with Gilts underperforming despite a solid 10Y UK auction. Periphery/semi-core EGB spreads were mostly tighter on the day, with 10Y BTPs failing to close below the 80bp mark to Bund.

- German factory orders highlight Tuesday's docket, with Italian industrial production and Eurozone retail sales also due. Thursday's BOE decision remains the calendar highlight of the week - MNI's preview is here.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.7bps at 1.908%, 5-Yr is down 0.2bps at 2.215%, 10-Yr is unchanged at 2.624%, and 30-Yr is up 0.3bps at 3.138%.

- UK: The 2-Yr yield is up 2bps at 3.826%, 5-Yr is up 1.8bps at 3.956%, 10-Yr is up 0.7bps at 4.516%, and 30-Yr is up 1.2bps at 5.339%.

- Italian BTP spread down 0.1bps at 80.2bps / French OAT down 0.3bps at 65.9bps

MNI OPTIONS: Lighter Trade In Euribor Calls (And ESTR Basis)

Tuesday's Europe rates/bond options flow included:

- ERZ5 98.50 call sold at 1 in 2k

- ERZ5 98.375 call bought for 2.25 in 4k

- TKYM5 11.5k at 98.07 (ESTR futures basis trade)

MNI FOREX: USD Index May be Building a Base

- The USD Index remained rangebound Tuesday, however the inability of markets to press the USD lower still after Friday's NFP print may suggest the price is building a base. ISM services data came in mixed, with headline activity softer-than-expected against a higher-than-expected prices paid subcomponent, and proved USD negative upon release, but the pullback was mild.

- The JPY was the poorest performing currency against all others in G10, aiding EUR/JPY to recovery back toward Y171. This keeps markets clear of the uptrending 50-dma support at 169.04, ahead of which the outlook remains bullish, and targets 171.85 - the 50% retracement for the fade off the cycle high at 173.97.

- Meanwhile, Trump spoke on his possible Fed picks to replace Kugler following her resignation over the weekend. The President declared he had a shortlist of 4, which includes both Kevin Warsh and Kevin Hassett, and while the President said he may use this Fed pick as a precursor to selecting the next Fed chair, he remained vague about the timing of such an announcement.

- GBP fared better, rising against most others in G10 as markets look ahead to Thursday's BoE rate decision. The MPC are expected to cut rates by 25bps, and anything other than this would mark a sizeable surprise against expectations. It's the vote split among the MPC that should prove more consequential - and should provide a strong signal for the Bank's easing plans through the second half of this year. Despite today's modest recovery, a bearish theme in GBPUSD remains intact for now - despite Friday’s rally. Last week’s sell-off resulted in a breach of the bear trigger at 1.3365, the Jul 16 low. The break confirms a resumption of the downleg that started Jul 1 and highlights a clear breach of the trendline drawn from the Jan 13 low.

- German factory orders, Italian industrial production and the Canadian services PMI data are the data highlights Wednesday. Fed's Cook, Collins and Daly are also set to make appearances.

MNI OPTIONS: Expiries for Aug06 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500-10(E1.6bln), $1.1550-65(E1.4bln), $1.1600(E1.1bln

- USD/JPY: Y147.00($1.3bln), Y152.00($1.0bln)

- GBP/USD: $1.3250(Gbp650mln)

MNI US STOCKS: Late Equities Roundup: Inching Lower After Mixed Earnings Results

- Stocks hold modestly weaker late Tuesday, near lows as carry-over buy-the-dip support that buoyed Monday's action loses momentum. Currently, the DJIA trades down 50.65 points (-0.11%) at 44123.82, S&P E-Minis down 26.75 points (-0.42%) at 6329.75, Nasdaq down 123.8 points (-0.6%) at 20930.18.

- Sector trade remained generally mixed with Materials/Utility, Consumer Discretionary, Pharmaceuticals and Tech stocks leading both gainers and decliners in late trade.

- Leading decliners includes: Gartner -28.48% after missing revenue guidance, Vertex Pharmaceuticals -19.14%, TransDigm Group -13.85%, Zebra Technologies -10.96%, Henry Schein -8.87%, Eaton Corp -6.41%, IDEXX Laboratories -5.83%, ONEOK -4.40%, Datadog -4.24%, Accenture -4.17% and Monolithic Power Systems -4.09%.

- Gainers included: defense stock Axon Enterprise +14.91% after better than expected earnings and several analyst upgrades, Leidos Holdings +6.92% on strong AI demand driving better than expected earnings, Pfizer +5.27%, Archer-Daniels-Midland +5.26%, Intel +3.97%, UnitedHealth Group +3.80%, CVS Health +3.25%, Dow +3.15%, Newmont Corp +2.65%.

- Late Tuesday earnings announcements: Amgen Inc, Rivian Automotive, Arista Networks, Advanced Micro Devices, Match Group, Mosaic, Snap, International Flavors & Fragrances and Super Micro Computer.

MNI EQUITY TECHS: E-MINI S&P: (U5) Corrective Pullback Extends

- RES 4: 6523.63 1.764 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6500.00 Round number resistance

- RES 2: 6477.31 1.618 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6468.50 High Jul 31 and the bull trigger

- PRICE: 6350.50 @ 1350 Aug 5

- SUP 1: 6264.25 Intraday low

- SUP 2: 6288.25 Low Jul 17

- SUP 3: 6241.00 Low Jul 16

- SUP 4: 6189.50 50-day EMA

The trend set-up in S&P E-Minis remains bullish and short-term weakness is considered corrective. Note that the contract has traded through support at the 20-day EMA, at 6336.64. The breach signals scope for a deeper retracement and opens the 50-day EMA at 6189.50. Clearance of this average is required to signal a stronger reversal. The primary trend remains up, key short-term resistance and the bull trigger is 6468.50, the Jul 31 high.

COMMODITIES

MNI AMERICAS OIL: WTI crude markets continued to lose ground

August 5 - Americas End-of-Day Oil Summary: WTI crude markets continued to lose ground following news Russia is considering a Ukraine air-truce offer to Trump in order to avoid secondary US tariffs. Also, market oversupply concerns persist as economic fears and another widely expected OPEC+ output hike have added pressure, offsetting risk of Russian supply disruption.

- Oil is finding some support from the threat of secondary tariffs on Russia if a ceasefire with Ukraine is not agreed before the August 8 deadline. US President Trump said special envoy Steve Witkoff will go to Russia this week.

- Trump made comments that low energy prices would pressure Putin to stop the war in Ukraine, seemingly clashing with his pressure on India to cease purchases of Russian oil or face higher tariffs.

- Trump said on Truth social that he will “be substantially raising the Tariff paid by India to the USA” due to Indian ‘buying and then selling on Russian oil’.

- China is also a major importer of Russian crude but has not yet been named specifically.

- WTI Sep futures were down 1.7% at $65.16

- WTI Oct futures were down 1.7% at $64.19

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 06/08/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 06/08/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 06/08/2025 | 0800/1000 | * | Industrial Production | |

| 06/08/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 06/08/2025 | 0900/1100 | ** | Retail Sales | |

| 06/08/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 06/08/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 06/08/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 06/08/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 06/08/2025 | 1800/1400 | Boston Fed's Susan Collins | ||

| 06/08/2025 | 1800/1400 | Fed Governor Lisa Cook | ||

| 06/08/2025 | 1910/1510 | San Francisco Fed's Mary Daly | ||

| 07/08/2025 | 0130/1130 | ** | Trade Balance |