MNI ASIA MARKETS ANALYSIS: Rocky Day for Tsys, Rate Cuts Rise

HIGHLIGHTS

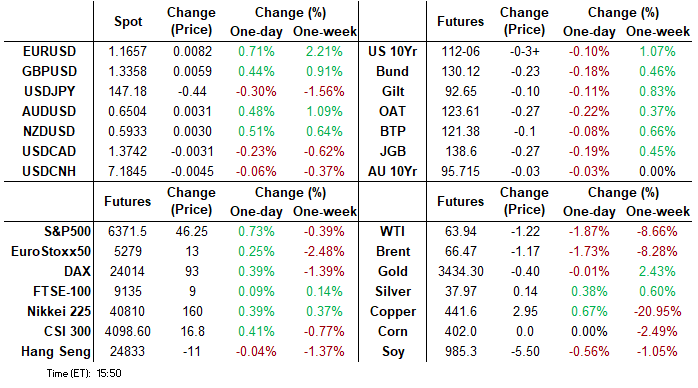

- Treasuries look to finish near steady (FVU5) to mixed, curves steeper with the short end outperforming after the bell.

- Rates had gapped lower midmorning: TYU5 tapped 111-26.5 low before rebounding almost as quickly, not headline or Block driven though some 60k TYU traded over short period - deemed likely error driven.

- Speculation over whether Pres Trump will announce new Russia sanctions or nominees for Fed governor or BLS head, however, tethered risk appetites somewhat.

- The USD resumed the recent spell of weakness Wednesday, helping the ICE USD Index through the post-NFP low.

- Focus Thursday on ECB's economic bulletin, US weekly jobless claims & unit labor costs, and latest Chinese trade balance numbers. Fed's Bostic expected to address monetary policy shortly after BoE rate decision.

US TSYS

MNI US TSYS: Treasuries Reverse Midmorning Knee-Jerk Dive, 10Y Note Sale Tailed

- Treasuries look to finish near steady (FVU5 -.25) to mixed, curves steeper (2s10s +3.084 at 51.452) with the short end outperforming. Rates had gapped lower midmorning: TYU5 tapped 111-26.5 low before rebounding almost as quickly, not headline or Block driven though some 60k TYU traded over short period - deemed likely error driven.

- The Sep'25 10Y futures contract currently trades 112-07 (-2.5). Treasury futures remain strong on the back of the post-NFP rally having cleared resistance into the bull trigger at 112-12+, the Jul 1 high. This opens the May 1 high for direction at 112-23, a multi-month high. Clearance here opens retracement levels layered between 113-07 and 113-23.

- Speculation over whether Pres Trump will announce new Russia sanctions or nominees for Fed governor or BLS head, however, tethered risk appetites somewhat. Trump reportedly wants to meet with Putin and Zelenskiy next week sometime.

- Treasury futures retreated slightly (TYU5 -7 at 112-07.5, 4.2375% yld) after the $42B 10Y note auction (91282CNT4) tailed 1bp: drawing 4.255% high yield vs. 4.245% WI; 2.35x bid-to-cover vs. 2.61x prior.

- Limited midweek data, focus turns to ECB's economic bulletin tomorrow, US weekly jobless claims & unit labor costs, and latest Chinese trade balance numbers. Fed's Bostic expected to address monetary policy shortly after BoE rate decision.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.34% (+0.01), volume: $2.863T

- Broad General Collateral Rate (BGCR): 4.33% (+0.02), volume: $1.167T

- Tri-Party General Collateral Rate (TCR): 4.33% (+0.02), volume: $1.137T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $115B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $268B

FED Reverse Repo Operation

RRP usage bounces to $91.966B this afternoon from $84.356B yesterday (lowest levels since April 25), total number of counterparties at 22. Lowest usage of the year at $54.772B on Wednesday, April 16 -- in turn the lowest level since April 2021 - compares to July 1: $460.731B highest usage since December 31.

US SOFR/TREASURY OPTION SUMMARY

Call volumes remain strong in the second half, interest in downside put structures have risen as underlying futures remain weaker in Reds-Blues (SFRU6-SFRM9). Projected rate cut pricing gains vs. morning (*) levels: Sep'25 at -23.6bp (-22.6bp), Oct'25 at -39.9bp (-38.4bp), Dec'25 at -60.1bp (-58.3bp), Jan'26 at -71.4bp (-68.9bp).

SOFR Options:

-4,000 0QZ5 96.75/97.00/97.50/97.75 call condors, 8.75 ref 96.935

Block, 10,000 0QQ5 96.75 puts, 2.5 vs. 96.855/0.20%

+50,000 0QZ5 98.00/98.37/98.50 broken 1x1x1 call flys, 2.75-30 ref 96.935

+20,000 SFRZ5 96.25/96.75 1x2 call spds, 7.75-8.0 ref 96.27

+8,000 SFRZ5 95.93/96.18/96.37/96.50 put condors, 0.75 ref 96.26

+10,000 SHRH6 96.37 puts, 19.5 ref 96.48/0.42%

+10,000 SFRQ5 95.81/95.87 put spds, 1.0 ref 95.94

+5,000 SFRZ5 96.00/96.12/96.25/96.37 call condors, 3.5 ref 96.265

+20,000 SFRZ5 96.50/96.87 call spds, 4.75 ref 96.255

+5,000 SFRZ5 96.25/96.50/96.75 call flys, 4.875

+3,000 SFRV5 96.31/96.43/96.50 broken call flys, 2.62 ref 96.255

+5,000 SFRU5 96.12/96.25 call spds, 1.25 ref 95.935

-2,000 SFRZ5 96.00/96.68 strangles, 11.5 ref 96.25

+4,000 SFRX5 96.25/96.37/96.50/96.62 call condors .25 over SFRZ5 95.62/95.857 put spd

Update, over +10,000 SFRZ5 96.56/96.68/96.75 1x3x2 broken call flys, 0.5

-4,000 SFRU5 95.75/95.81/95.93/96.00 call condors, 2.5 ref 95.925

+4,000 SFRH6 98.00 calls, 2.5 ref 96.47

-10,000 0QZ5 96.50/96.75 2x1 put spds 1.5

+5,000 SFRU5 96.18/96.25 call spds .62

+20,000 SFRZ5 99.00 calls, 0.25 ref 96.245

+6,000 SFRU5 95.81/95.87/96.00/96.06 call condors, 3.75 ref 95.925

+4,000 SFRU5 95.93/96.00 call spds ref 95.925

Treasury Options:

5,000 TYU5 111.5/113 strangles, 28

-13,000 wk2 TY 112 puts, 9 vs. 112-02/0.43%

3,800 USU5 105/USV5 109 put spds, 18

Block 8,310 USU5 104/USV5 108 put spd, 13 vs. 115-28/0.08%

+4,000 TYZ5 109.5 puts, 29 vs. 112-03.5/0.25%

-7,500 wk5 TY 111.5 puts, 20

3,700 USU5 104/USV5 108 put spd

-10,000 FVU5 109.25 calls, 13

+5,000 FVV5 108.25/108.75 2x1 put spds 6 vs. 109-01.75/0.17%

+1,500 FVU5 109/109.75 1x2 call spds 6 vs. 108-28.75/0.08%

2,500 wk3 TY 112.75/113.25 call spds ref 112-02

5,500 TYU5 110 puts, 2-3 ref 112-02.5

27,000 Weekly Wednesday TY vs. wk2 TY 112 put spds, 7 net on the 3 day package where the first leg expires today. Or possibly a 3 day roll where open interest in the Wednesday option is 46,380 - in which case - more to trade soon.

MNI BONDS: EGBs-GILTS CASH CLOSE: Late Sell-Off Cements German Bear Steepening

European curves steepened Wednesday, with Bunds underperforming Gilts ahead of the BOE decision.

- Early trade saw modest bear steepening across the space, with German supply weighing on long-end Bunds.

- Yields began to rise in late afternoon but suddenly spiked less than 30 minutes before the European cash close on what some desks called an erroneous trade. While yields came back down, they closed well off their lows.

- German factory orders data were weaker than expected, compared with Italian industrial production which surprised to the upside and Eurozone retail sales which were largely in line. None of the data had any major market impact.

- The German curve bear steepened slightly on the day, with the UK's twist steepening. Periphery/semi-core EGB spreads closed mixed.

- Thursday's BOE decision is the calendar highlight of the week - MNI's preview is here.

- Along with the expected 25bp rate cut, focus will be

on the vote split, the tone of the press conference, any changes to assumptions in the scenarios and any signalling ahead of September’s QT decision.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1bps at 1.918%, 5-Yr is up 2bps at 2.235%, 10-Yr is up 2.6bps at 2.65%, and 30-Yr is up 3.5bps at 3.173%.

- UK: The 2-Yr yield is down 0.5bps at 3.821%, 5-Yr is up 0.3bps at 3.959%, 10-Yr is up 1bps at 4.526%, and 30-Yr is up 2.1bps at 5.36%.

- Italian BTP spread down 0.4bps at 79.8bps / French OAT up 0.7bps at 66.6bps

MNI EGB OPTIONS: Upside-Leaning Structures In European Rates

Wednesday's Europe rates/bond options flow included:

- RXV5 131/130/129p fly, bought for 15.5 in 2k.

- ERH6 99.0/99.50 call spread, bought for 0.75 in 10k

- SFIQ5 96.15/96.20 call spread saw paper pay 1.0 on 7K

- SFIZ5 96.55/96.75cs, bought for 2 in 2k

- SFIZ5 96.60/96.80/97.00/97.20c condor sold at 0.75 in ~1.3k with SFIZ5 96.50/96.70cs, sold at 2.25 in ~2.88k

- SFIM6 96.75/97.50/98.25c fly, bought for 10.25 in 8k

- SFIM6 97.00 calls paper paid 8.75 on 4K vs. 96.535

MNI FOREX: USD Resumes Spell of Weakness on Fed Speculation, Technical Break

- The USD resumed the recent spell of weakness Wednesday, helping the ICE USD Index through the post-NFP low. Prices have also broken interim support at the 50-dma - a level that had drawn notable focus through the YTD downtrend and helped define the downtrend. EUR/USD topping the Friday high and layered resistance between 1.1597-00 further triggered USD selling.

- Interjections from potential next Fed chair Hassett helped weigh on the USD, as he voiced his support for a more Greenspan-like approach to policymaking, with a lesser focus on consensus-forming. This led markets to more quickly price in rates conforming to Trump's preference for easy policy. A later Bloomberg report that suggested Trump was being advised to appoint an interim Fed governor that can skip the Senate nomination process made little impact on pricing - although the expedited timeline could mean a new Trump appointee is installed ahead of the September rate decision.

- Resilient GBP/USD comes despite the NIESR estimates out earlier today that suggests the government are facing a more dire fiscal picture in Autumn than previously expected - suggesting markets are well priced for sharp spending cuts and/or tax rises at the next Budget. Instead, it's the BoE decision Thursday that could be of more consequence, and in particular the vote split: 2-5-2 (50bps cut, 25bps cut, unch) is the modal consensus - and we flag that the baseline projections may become less

useful as a communication tool going forward - and as such, less market relevant. EUR/GBP remains in a nascent uptrend, evident in the recovery from last Thursday's low. Key resistance and the bull trigger remains at 0.8769, the Jul 27 high. - Focus Thursday turns to the ECB's economic bulletin, US weekly jobless claims and unit labor costs and the latest Chinese trade balance numbers. Fed's Bostic is due to be addressing monetary policy shortly after the BoE rate decision.

MNI OPTIONS: Expiries for Aug07 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500(E1.1bln), $1.1600(E957mln)

- USD/JPY: Y146.50($605mln), Y146.93-05($569mln), Y147.65($1.4bln), Y148.00-15($2.0bln), Y148.50($1.2bln)

- EUR/JPY: Y170.00(E770mln)

- AUD/USD: $0.6500(A$1.2bln), $0.6600(A$2.0bln)

- USD/CAD: C$1.3800($700mln)

- USD/CNY: Cny7.2500($836mln)

MNI US STOCKS: Late Equities Roundup: IT & Consumer Sector Shares Outperform

- Stocks remain firm late Wednesday, fully recovering from the prior session's sell-off, tech-heavy Nasdaq outperforming. Currently, the DJIA trades up 150.26 points (0.34%) at 44263.27, S&P E-Minis up 48.75 points (0.77%) at 6373.75, Nasdaq up 245.7 points (1.2%) at 21162.15.

- Stocks started to pare losses after White House officials said Apple will announce a commitment to invest another $100B on US manufacturing today. Speculation over whether Pres Trump will announce new Russia sanctions or nominees for Fed governor or BLS head, however, tethered risk appetites somewhat.

- A mix of IT, Consumer Staples and Discretionary sector shares continued to lead gainers in the second half: Arista Networks +17.91%, Assurant +11.94%, Match Group +10.17%, Apple +5.75%, Walmart +4.13%, Target +3.69%, Amazon +3.64%, McDonald's +3.42%, Tesla +3.34%, Kroger +2.94%, Ross Stores +2.85% and Costco Wholesale +2.82%.

- A couple notable IT exceptions bucking the move: Super Micro Computer -19.24% after earning outlook disappoints, while Advanced Micro Devices declined -5.81%.

- Leading decliners included Health Care, Materials and Energy sector shares: NRG Energy -14.01%, Mosaic -12.14%, Bio-Techne -10.34%, Charles River Laboratories -8.10%, Rockwell Automation -7.47%, International Flavors & Fragrances -6.54%, Paramount Global -6.17%, Enphase Energy -5.30%, Amgen -5.16% and LyondellBasell Industries -5.06%.

- Companies expected to announce earnings after today's close include: Corteva, McKesson Corp, Occidental Petroleum, AIG, DoorDash, Fortinet, AppLovin, Lyft, Dutch Bros, Airbnb Inc, Zillow Group, Duolingo, MetLife, APA and DraftKings Inc.

MNI EQUITY TECHS: E-MINI S&P: (U5) Corrective Pullback Extends

- RES 4: 6523.63 1.764 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6500.00 Round number resistance

- RES 2: 6477.31 1.618 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6468.50 High Jul 31 and the bull trigger

- PRICE: 6372.00 @ 1445 ET Aug 6

- SUP 1: 6244.36 2.0% 10-dma Envelope

- SUP 2: 6239.50 Low Aug 1

- SUP 3: 6213.75 50% retracement of Jun - Aug Upleg

- SUP 4: 6203.65 50-day EMA

Equities sold off sharply Friday on the back of the soft NFP print - pushing prices through mid-July lows in the process. Since that spell of weakness, price has traded either side of support at the 20-day EMA, at 6325.25, signalling scope for a deeper retracement toward the 50-day EMA at 6203.65. Clearance of this average is required to signal a stronger reversal. The primary trend remains up, leaving key short-term resistance and the bull trigger at 6468.50, the Jul 31 high.

COMMODITIES

MNI AMERICAS OIL: WTI crude reversed lower

August 6 - Americas End-of-Day Oil Summary: WTI crude reversed lower after US Secretary of State Rubio expressed hope following envoy Witkoff’s meeting with Putin. The market had traded higher in volatile trading after an additional 25% tariff was placed on India for its purchases of Russian oil.

- Saudi Arabia raised its September Arab Light OSP to Asia by $1/bbl to +$3.20/bbl, more or less in line with expectations.

- The US issued an additional 25% tariff on India for its purchases of Russian oil. Bloomberg reports that Trump is weighing additional measures targeting Russian oil revenue, such as sanctions on oil tankers and related entities.

- Russia and the US sent ‘signals’ to one another in a Putin-Witkoff meeting today. Trump suggested on Tuesday other countries – including China - may face increased tariffs if they continue buying Russian energy.

- WTI Sep futures were down 1.3% at $64.35

- WTI Oct futures were down 1.3% at $63.39

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 07/08/2025 | 0600/0800 | ** | Trade Balance | |

| 07/08/2025 | 0600/0800 | ** | Industrial Production | |

| 07/08/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 07/08/2025 | 0645/0845 | * | Foreign Trade | |

| 07/08/2025 | 0700/0900 | ** | Unemployment | |

| 07/08/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 07/08/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 07/08/2025 | 1130/1230 | BOE Press Conference | ||

| 07/08/2025 | - | *** | Trade | |

| 07/08/2025 | 1230/0830 | *** | Jobless Claims | |

| 07/08/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 07/08/2025 | 1230/0830 | ** | Preliminary Non-Farm Productivity | |

| 07/08/2025 | 1300/1400 | BOE Decision Maker Panel Data BOE Decision Maker Panel Data | ||

| 07/08/2025 | 1400/1000 | * | Ivey PMI | |

| 07/08/2025 | 1400/1000 | ** | Wholesale Trade | |

| 07/08/2025 | 1400/1000 | ** | Wholesale Trade | |

| 07/08/2025 | 1400/1000 | Atlanta Fed's Raphael Bostic | ||

| 07/08/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 07/08/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 07/08/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 07/08/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 07/08/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 07/08/2025 | 1900/1500 | * | Consumer Credit | |

| 07/08/2025 | 1900/1500 | *** | Mexico Interest Rate | |

| 08/08/2025 | 2330/0830 | ** | Household spending | |

| 08/08/2025 | 2350/0850 | Balance of Payments |