MNI ASIA MARKETS ANALYSIS: Risk-Off, US Shutdown Ties Record

HIGHLIGHTS

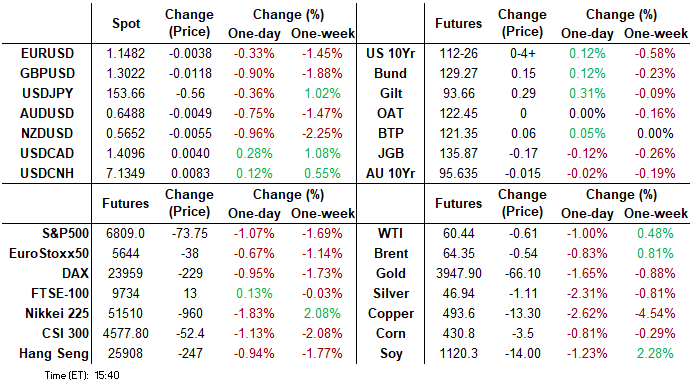

- Treasuries edged higher on moderate risk-on unwinds ahead Wednesday's non-government produced economic data: ADP employment, S&P Global US Services/Composite PMI and ISM Services.

- Further upward pressure on the greenback was on show Tuesday, prompting the USD index to establish its position back above the 100 mark, at fresh recovery highs. The index traded to within 4 pips of the August 01 highs.

- Stocks remain in weaker territory late Tuesday, near session lows amid moderate risk-off support in rates. Focus is on late cycle corporate earnings as the US Government shutdown ties the longest in history at 35 days.

- Analysts' outlooks for Wednesday's refunding reflect almost no expectations for any major changes, likelihood of increased bill issuance.

US TSYS

MNI US TSYS: Tsys Hold Higher Levels Ahead Midweek Data & Tsy Refunding Annc

- Treasuries look to finish modestly higher Tuesday - upper half of narrow session range as markets await Wednesday's non-government produced economic data: ADP employment, S&P Global US Services/Composite PMI and ISM Services as well as US Tsy Quarterly Refunding annc.

- Currently, the Dec'25 10Y contract trades +4.5 at 112-26 vs. 112-28.5 high, 10Y yield -.0272 at 4.0832%. The contract needs to trade above 113-18+, the Oct 28 high to signal a possible bullish reversal. Key resistance and the bull trigger is at 114-02, the Oct 17 high.

- The next two days see some private sector labor indicators that likely will see particular attention this week with a lack of BLS releases. ADP is expected to see some stabilization after recent job losses, with added questions over how its regular monthly report correlates with a newly published weekly series, whilst the Challenger report offers a look at hiring plans for a second important seasonal month.

- Analysts' outlooks for Wednesday's refunding reflect almost no expectations for any major changes, but there is increasing attention being paid to the likelihood of increased bill issuance ahead as coupon sizes aren't increased until well into 2026 at least.

- Greenback underpinned Tuesday, prompting the USD index to establish its position back above the 100 mark, at fresh recovery highs. The index traded to within 4 pips of the August 01 highs. Price action led an impressive lurch lower for spot gold, which briefly extended declines to 1.8% on the day to $3,930/oz.

- Stocks expected to announce earnings after the close include: Arista Networks Inc, Live Nation Entertainment, Corteva, Rivian Automotive, Advanced Micro Devices, American International Grp, Mosaic Co, Pinterest, Match Group, AES Corp, Super Micro Computer, Amgen Inc.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.13% (-0.09), volume: $3.237T

- Broad General Collateral Rate (BGCR): 4.09% (-0.06), volume: $1.159T

- Tri-Party General Collateral Rate (TCR): 4.09% (-0.06), volume: $1.122T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.86% (-0.01), volume: $107B

- Daily Overnight Bank Funding Rate: 3.86% (-0.01), volume: $195B

FED Reverse Repo Operation

RRP usage slips to $16.893B with 13 counterparties this afternoon - from $23.792B Monday. Compares to $2.435B on October 24 (lowest level since mid-March 2021) and the year's highest usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR/Treasury option flow remained mixed Tuesday, modest volumes with SOFR seeing a rise in low delta calls in second half, Treasuries segued to puts. Underlying futures firmer - off highs, curves little changed. Projected rate cut pricing gains slightly vs. late Monday levels (*): Dec'25 at -17.2bp (-16.4bp), Jan'26 at -26.4bp (-24.6bp), Mar'26 at -34.9bp (-32.9bp), Apr'26 at -41.4bp (-39.1bp).

SOFR Options:

Block, 5,000 SFRF6 96.25/96.75 4x5 call spds, 4.5 net - 4 legs over ref 96.435

2,000 SFRZ5 96.25/96.31/96.44 broken call flys ref 96.255

-4,000 SFRH6 96.50 calls, 12.0 vs. 96.44/0.42%

+5,000 SFRZ5 96.37/96.87 call spds, 1.5 vs. 96.25/0.16%

+3,500 SFRM6 96.25/96.31/96.43 put trees, .25

3,000 SFRU6 97.25/98.00 call spds vs. 96.25 puts

2,000 SFRH6 96.37 puts

2,000 SFRZ5 96.12/96.25 2x1 put spds

+2,000 SFRX5 96.18/96.25/96.31 put trees, 3.5

4,000 SFRX5 96.18 puts, 1.0 last

1,500 SFRM6/0QM6 96.25/96.50 put spd spd covered, 3.0 net

7,000 0QZ5 97.00/97.25 call spds, 5.5 vs. 96.92/0.25%

Treasury Options:

6,500 TYZ5 112.75/114 call spds, 36 ref 112-26.5

1,900 FVZ5 109.75/110.5 call spds ref 109-10.25

3,000 TYZ5 112.75 puts, 26 ref 112-24.5

8,000 Wednesday wkly 30Y 118 calls, 5 ref 117-10 (exp 11/5)

3,000 TUZ5 104.25 calls, 5.5 ref 104-05.62

13,000 TUZ5 103.87/104.37/104.5/104.87 broken put condors ref 104-05.5 to -05.62, 7.5 net

+1,500 TYZ5 112.5 puts, 20

+1,200 TYG6 113 calls, 54 vs. 112-21/0.45%

+1,500 TYZ5 113.25 calls, 15 vs. 112-22.5/0.30%

+2,000 TYZ5 113.5/114/114.5 1x3x2 call flys, 0.0

+1,250 TYZ5 113/113.5/114 call flys, 5 vs. 112-31.5/0.04%

+2,000 FVZ5 110.5 calls, 2.5 vs. 109-10.5/0.09%

+5,000 TYZ5 111.5/112.25 put spds vs. 113.75 calls, 0.0

+2,000 TYZ5 113 calls, 23 vs. 112-26/0.44%

+3,500 TYG6 114 calls, 35 vs. 112-25.5/0.30%

MNI BONDS: EGBs-GILTS CASH CLOSE: Light UK Bull Steepening On Fiscal Factors

European yields fell modestly Tuesday, partially retracing Monday's rise.

- A broader risk-off move helped underpin core EGBs in early trade, but didn't provide a significant boost.

- Regional data was limited, with more focus on fiscal developments in the UK.

- UK Chancellor Reeves' pre-budget appearance appeared to signal incoming tax increases, with the government hoping to pave the way for BOE rate cuts via tighter fiscal policy.

- That helped the UK curve bull steepen lightly, with Germany's bull flattening. Periphery / semi-core EGB spreads widened slightly.

- Wednesday's schedule includes German factory orders and final services PMIs, along with multiple ECB speakers (including Villeroy and Nagel) and BOE's Breeden not to mention the Swedish Riksbank decision. Focus remains on Thursday's BOE however.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.1bps at 1.997%, 5-Yr is down 1.3bps at 2.255%, 10-Yr is down 1.3bps at 2.654%, and 30-Yr is down 1.4bps at 3.237%.

- UK: The 2-Yr yield is down 1.1bps at 3.784%, 5-Yr is down 0.8bps at 3.899%, 10-Yr is down 1bps at 4.425%, and 30-Yr is down 0.4bps at 5.204%.

- Italian BTP spread up 0.3bps at 74.6bps / French OAT up 0.4bps at 78.2bps

MNI EGB OPTIONS: Condors Remain In Vogue Across Rates

Tuesday's Europe rates/bond options flow included:

- RXZ5 131/132cs, bought for 4 in 3.8k

- ERM6 98.125/98.50/98.875 call fly, bought for 5 in 10k

- ERM6 98.75 call, paper pays 1.0 in 9k

- ERM6 98.18/98.25/98.37/98.43c condor, bought for 0.75 in 4k total

- SFIZ5 96.15/96.25/96.35/96.45 c condor, sold at 4.5 in 5k

- SFIG6 96.50/96.40/96.25/96.05p condor sold at 3.75 and 3.5 in 4.56k

- SFIH6 96.45/96.55/96.65/96.75c condor vs 96.25/96.15ps, bought the condor for 1.5 in 11k total on the day

- SFIJ6 96.70/96.80 call spread paper paid 2.75 on 8K vs. 96.555

MNI FOREX: USD Index Extends Towards Aug Highs, Notable GBP and NZD Weakness

- Further upward pressure on the greenback was on show Tuesday, prompting the USD index to establish its position back above the 100 mark, at fresh recovery highs. The index traded to within 4 pips of the August 01 highs. Price action led an impressive lurch lower for spot gold, which briefly extended declines to 1.8% on the day to $3,930/oz. Across the G10, dented risk sentiment weighed significantly on the likes of AUD and NZD, while additional fiscal headwinds added further pressure on GBP.

- GBPUSD extended notably lower, with downside momentum building on a break of 1.31. UK Chancellor Reeves’ pre-budget appearance provided her clearest signal yet that sizeable tax rises are incoming (suggested by the statement of working in the national interest, rather than political popularity), as well as indicating her intention to pave the way with fiscal policy to allow for further BoE rate cuts.

- As we approach the APAC crossover, GBPUSD sits below 1.3041, the Apr 14 low, another bearish technical development for the pair. 1.2971 will act as interim support on the way to 1.2709, a key medium-term level.

- NZDUSD tracks lower for a fifth consecutive session on Tuesday, significantly breaching both trendline support (drawn from the April lows) and the recent cycle low of 0.5683. Coupled with the NZDUSD extension lower, AUDNZD was also in focus Tuesday, after two separate rallies stalled just ahead of key medium-term resistance at 1.1491.

- We have highlighted that a break of this level would place the cross at its highest point since 2013, with plenty of attention on the level/1.1500 ahead of NZ employment data, which highlights the APAC calendar on Wednesday.

- Central bank decisions in Sweden, Poland and Brazil are also due tomorrow, while US ISM services data are also scheduled.

MNI OPTIONS: Expiries for Nov5 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1525(E630mln), $1.1600-20(E1.4bln)

- EUR/GBP: Gbp0.8745(Gbp753mln)

- USD/JPY: Y153.35-50($905mln)

- NZD/USD: $0.5650(N$1.2bln), $0.5675(N$1.2bln)

MNI US STOCKS: Late Equities Roundup: Weaker Into Late Cycle Earnings, Midweek Data

- Stocks remain in weaker territory late Tuesday, near session lows amid moderate risk-off support in rates. Focus is on late cycle corporate earnings as the US Government shutdown ties the longest in history at 35 days, while Wednesday sees non-government produced economic data: ADP employment, S&P Global US Services/Composite PMI and ISM Services.

- Currently, the DJIA down 308.53 points (-0.65%) at 47032.11, S&P E-Minis down 79.75 points (-1.16%) at 6804.25, Nasdaq down 437.7 points (-1.8%) at 23399.8.

- A mix of Pharmaceutical, Energy, Materials and Information Technology sector shares continued to decline in late trade: Zoetis -12.66%, CDW Corp -10.12%, Albemarle Corp -8.08%, Palantir Technologies -7.93%, Gartner -6.88%, Synopsys -5.97%, Skyworks Solutions -5.96%, Marathon Petroleum -5.92% and Micron Technology -5.76%

- Weighing on the Consumer Discretionary sector - notable declines also reported in cruise lines: Norwegian Cruise Line -15.37%, Carnival Corp -9.35% and Royal Caribbean Cruises -7.09%.

- Conversely, the Financials sector, particularly insurance providers continued to outperform in late trade: Apollo Global Management +5.69%, Willis Towers Watson +3.01%, Global Payments +2.93% and Travelers Cos Inc +2.75%. Health Care sector shares followed: Henry Schein +9.39%, Waters Corp +6.46%, Centene Corp +3.80% and Molina Healthcare 3.30%.

- Stocks expected to announce earnings after the close include: Arista Networks Inc, Live Nation Entertainment, Corteva, Rivian Automotive, Advanced Micro Devices, American International Grp, Mosaic Co, Pinterest, Match Group, AES Corp, Super Micro Computer, Amgen Inc.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Monitoring Support

- RES 4: 7000.00 Psychological round number

- RES 3: 6993.12 3.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6974.04 3.382 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 1: 6953.75 High Oct 30 and the bull trigger

- PRICE: 6832.50 @ 14:58 GMT Nov 4

- SUP 1: 6804.03/6786.25 20-day EMA / Intraday low

- SUP 2: 6698.11 50-day EMA

- SUP 3: 6571.25 Low Oct 17

- SUP 4: 6540.25 Low Oct 10 and a key short-term support

The trend condition in S&P E-Minis is unchanged, it remains bullish and the latest pullback appears corrective. Attention is on support at the 20-day EMA, at 6804.03 (pierced). A clear break of this average would signal scope for a deeper retracement and expose the 50-day EMA at 6698.11 - a key pivot support. The bull trigger has been defined at 6953.75, the Oct 30 high. Clearance of this hurdle would confirm a resumption of the uptrend.

MNI COMMODITIES: Precious Metals Fall As Dollar Extends Gains, Crude Declines

- Precious metals underperformed on Tuesday amid a risk-off tone in markets and broad gains in the US dollar. The USD index rose back above the 100-mark to fresh recovery highs.

- That price action led an impressive lurch lower for spot gold, which briefly extended declines to 1.8% on the day to $3,930/oz. Currently, gold sits 1.5% lower at $3,941.

- Meanwhile, silver is down by 1.6% at $47.3/oz, albeit also off earlier session lows at $46.88.

- For gold, today’s losses mark an extension of the bear cycle that started Oct 20. The retracement since Oct 20 has allowed an overbought trend condition to unwind. The 20-day EMA has been breached, signalling scope for a test of the 50-day EMA, at $3,867.7.

- For silver, trend signals are bullish, and recent weakness is considered corrective. Support to watch lies at the 50-day EMA, at $46.096, which remains intact. However, a break would signal scope for a deeper retracement towards $41.135, the Sep 17 low.

- Elsewhere, crude prices are lower as oversupply concerns are fuelled by elevated levels of oil at sea while the market also weighs the implications of OPEC’s latest meeting.

- WTI Dec 25 is down 0.9% at $60.5/bbl.

- On Sunday, OPEC+8 agreed to a modest 137kb/d output target hike in December with a pause through Q1.

- WTI futures remain in a corrective cycle for now. Price recently traded through the 50-day EMA at $61.03, signaling scope for a stronger recovery, with sights on key resistance at $65.77, the Sep 26 high.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 05/11/2025 | 0700/0800 | ** | Manufacturing Orders | |

| 05/11/2025 | 0745/0845 | * | Industrial Production | |

| 05/11/2025 | 0815/0915 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0815/0915 | ** | S&P Global Composite PMI (final) | |

| 05/11/2025 | 0830/0930 | *** | Riksbank Interest Rate Decison | |

| 05/11/2025 | 0845/0945 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0845/0945 | ** | S&P Global Composite PMI (final) | |

| 05/11/2025 | 0850/0950 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0850/0950 | ** | S&P Global Composite PMI (final) | |

| 05/11/2025 | 0855/0955 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0855/0955 | ** | S&P Global Composite PMI (final) | |

| 05/11/2025 | 0900/1000 | * | Retail Sales | |

| 05/11/2025 | 0900/1000 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0900/1000 | ** | S&P Global Composite PMI (final) | |

| 05/11/2025 | 0930/0930 | ** | S&P Global Services PMI (Final) | |

| 05/11/2025 | 0930/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 05/11/2025 | 1000/1100 | ** | EZ PPI | |

| 05/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 05/11/2025 | 1315/0815 | *** | ADP Employment Report | |

| 05/11/2025 | 1330/0830 | *** | Treasury Quarterly Refunding | |

| 05/11/2025 | 1445/0945 | *** | S&P Global Services Index (final) | |

| 05/11/2025 | 1445/0945 | *** | S&P Global US Final Composite PMI | |

| 05/11/2025 | 1500/1000 | *** | ISM Non-Manufacturing Index | |

| 05/11/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 05/11/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 05/11/2025 | 1610/1610 | BOE Breeden At SALT Blockchain Event | ||

| 06/11/2025 | 2330/0830 | ** | average wages (p) | |

| 06/11/2025 | - | NorgesBank Meeting | ||

| 06/11/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 06/11/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 06/11/2025 | 0030/1130 | ** | Trade Balance |