MNI ASIA MARKETS ANALYSIS: Rates/Stocks Shrug Off Weak Jobs

HIGHLIGHTS

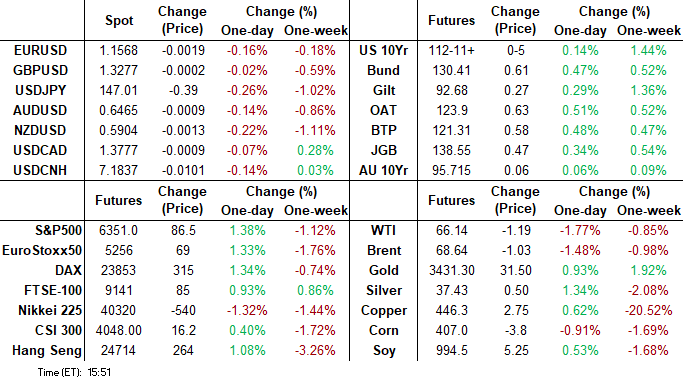

- Treasuries are firmer after the bell, near session highs as projected rate cut pricing holds +/- .5bp vs pre-open highs (*) levels: Sep'25 at -23.2bp (-22.6bp), Oct'25 at -40.6bp (-41.1bp), Dec'25 at -61.4bp (-61.6bp).

- Following Friday's sharp downdraft in the USD, FX markets were more stable Monday, with the USD pulling back only a small part of the post NFP weakness.

- Stocks remain firm late Monday, at/near session highs as markets focus on dovish rate cut pricing and incoming earnings this week, instead of Friday's slowing labor market data.

- Focus Tuesday rests on China composite and manufacturing PMI data, final PMI prints across Europe and the US as well as the US ISM services index for July.

US TSYS

MNI US TSYS: Holding Firm, Focus on Tuesday PMIs, ISM Services Data

- Treasuries remain firmer after the bell, Sep'25 10Y futures drifting near session highs for much of the second half. Curves reversed early steepening as bonds rebounded, focus on dovish rate cut pricing instead of Friday's slowing labor market data.

- Tsy Sep'25 10Y futures currently trades +4.5 at 112-11 vs. 112-14 high, curves flatter: 2s10s -2.157 at 50.855, 5s30s -1.554 at 104.770.

- The weak payrolls report dominated what had been a decent-sized hawkish reaction from a patient Fed Chair Powell not giving a nod to a September rate cut at Wednesday’s FOMC press conference. Nonfarm payrolls growth underwhelmed at 73k in July (cons 104k) but the major headline was the -258k two-month downward revision, of which -139k came from the private sector and -119k from the public sector.

- Projected rate cut pricing holds +/- .5bp vs pre-open highs (*) levels: Sep'25 at -23.2bp (-22.6bp), Oct'25 at -40.6bp (-41.1bp), Dec'25 at -61.4bp (-61.6bp).

- Factory orders fell -4.8% M/M (sa, cons -4.8) in June after 8.3% (initial 8.2) in May as they confirmed gyrations driven by nondefense aircraft in the previously released durable goods data (-52% M/M in June after 232% in May).

- Look ahead to Tuesday: China composite and manufacturing PMI data, final PMI prints across Europe and the US as well as the US ISM services index for July.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.34% (-0.05), volume: $2.885T

- Broad General Collateral Rate (BGCR): 4.32% (-0.04), volume: $1.143T

- Tri-Party General Collateral Rate (TCR): 4.32% (-0.04), volume: $1.109T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $129B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $287B

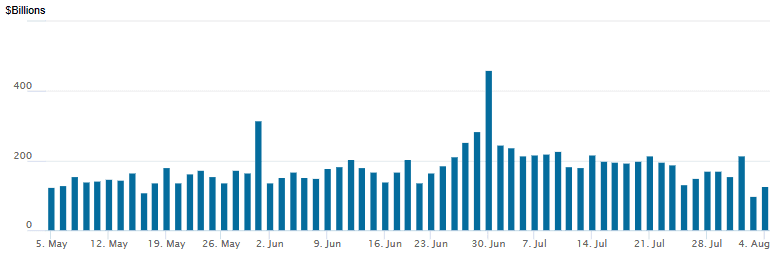

FED Reverse Repo Operation

RRP usage rebounds to $125.730B this afternoon from $97.426B Friday (lowest levels since April 25), total number of counterparties at 26. Lowest usage of the year at $54.772B on Wednesday, April 16 -- in turn the lowest level since April 2021 - compares to July 1: $460.731B highest usage since December 31.

US SOFR/TREASURY OPTION SUMMARY

Robust SOFR & Treasury option volumes reported Monday, mixed wing trade with better put trade leading volumes. Underlying futures firmer, short end lagging as curves reverse early steepening. Projected rate cut pricing has +/- .5bp vs pre-open highs (*) levels: Sep'25 at -23.2bp (-22.6bp), Oct'25 at -40.6bp (-41.1bp), Dec'25 at -61.4bp (-61.6bp), Jan'26 at -73.6bp (-73.1bp).

SOFR Options:

4,125 SFRZ5 96.31 straddles,

+30,000 SFRU5 95.75/95.87 put spd vs. SFRZ5 95.81/95.93 put spd spd, 1.0-1.25 net flattener

+10,000 SFRH6 96.37 puts, 19.5 vs. 96.495/0.44%

+5,000 2QU5 95.68 straddles, 27.5

-3,000 SFRZ5 96.18/96.37 2x1 put spds 2.5

+4,000 SFRM6 96.75/97.25 call spds 1.5 over 2QM6 96.25/96.75 call spds

+6,000 0QZ5 97.25/97.50 call spds 6.0 ref 96.965

-10,000 SFRZ5 96.12/96.37/96.62 call flys, 5.0

+6,000 0QV5 97.25/97.50 call spds, 6.0 ref 96.865

+2,500 SFRU5 96.18/96.25 call spds, .625 ref 95.94

+5,000 2QH6 97.00/97.25/97.50 call flys, 2.75 ref 96.80

-4,000 SFRV5 96.37/96.62 call spds, 6.0 ref 96.605/0.18%

-19,100 SFRZ5 95.75/95.87/96.25/96.37 put condors, 6.0 ref 96.30

Block, 5,500 SFRM6/2QM6 96.75/97.25 call spd spds

1,500 SFRZ5 96.50/96.68/96.75 broken call flys ref 96.295

3,500 SFRU5 95.93/96.00/96.06 call flys ref 95.945

over 9,700 SFRU5 96.00 calls ref 95.94

2,250 SFRQ5 96.00/96.25 call spds ref 95.945

1,500 SFRV5 96.37/96.62/97.00 call flys ref 96.275

3,000 SFRV5 96.50/96.75 call spds ref 96.265

Block/screen 4,000 SFRZ5 95.75/95.87/96.00 put trees

4,500 SFRZ5 95.68/95.81 2x1 put spds

2,000 0QH6 97.25/97.50 call spds ref 96.925

2,400 SFRH6 96.12 puts ref 96.48

1,500 SFRH6/3QH6 97.00/97.50 call spd spds

-5,500 SFRH6 96.00/96.25/96.37 put trees, 1.0 ref 96.465/0.13%

Treasury Options:

+40,000 wk1 TY 111.75/112 put spds, 3 (exp 8/6)

2,500 TYU5 111 puts, 10 ref 112-10.5

5,000 TYU5 111.5/113.25 call spds ref 112-10.5

+20,000 FVU5 107.5/108.25/109 put flys, 12 vs. 109-07.5/0.14%

over 10,300 TYU5 108.5 puts ref 112-07.5

1,500 TYX5/TYZ5 112.5/114 call spd spds ref 112-08.5

3,200 TYU5 108/109.5 put spds ref 112-07.5

16,000 TYU5 113 calls, 19-20 ref 112-06 (total volume over 29.4k)

+3,000 TYU5 112/113 1x2 call spds, 3 ref 112-02

2,500 TUU5 103.5/103.75 put spd vs. 104/104.25 call spds ref 103-30.25

1,100 TYU5 109/111 2x1 put spds ref 112-02

1,600 TYU5 109 puts ref 112-02.5

1,300 FVU5 108.25/108.75/109/109.75 broken call condors ref108-31.5

1,800 FVZ5 114 calls ref 109-08

-2,600 TYU5 112.5 calls 27 ref 112-03/0.40%

MNI FOREX: USD Stabilizes, But Little Sign of a S/T Bounce

- Following Friday's sharp downdraft in the USD, FX markets were more stable Monday, with the USD pulling back only a small part of the post NFP weakness. The ICE USD Index saw some support into the 50-dma at 98.303 - however Monday's price action took the form of stabilization rather than any bounce in prices.

- The more stable market Monday aided a recovery in GBP. GBP/USD traded either side of the 1.33 handle - topping Friday's high in the process. Moves come ahead of this Thursday's BoE decision at which markets fully discount a 25bps rate cut. The vote split among the MPC will be carefully watched as a clue for future easing plans across the second half of the year. The bearish theme in GBPUSD remains intact for now - despite Friday’s rally. Last week’s sell-off resulted in a breach of the bear trigger at 1.3365, the Jul 16 low. The break confirms a resumption of the downleg that started Jul 1 and highlights a clear breach of the trendline drawn from the Jan 13 low.

- JPY was the firmest in G10 - prompting a second session of losses for USD/JPY. The rate is now through Friday's low and going further to erase the rally off the mid-July low. Layered support comes in between 145.71 - 145.86 - marking the confluence of the 100-dma, 50-dma and the mid-July lows.

- Meanwhile, CHF was the weakest in G10 - seeing very little reprieve from Trump's decision to install some of the most sizeable tariffs against Switzerland. Reports that the Swiss government are to make a more attractive offers as part of negotiations did little to reverse the CHF weakness, which sees USD/CHF continue to trade either side of the 0.8074 50-dma.

- Focus Tuesday rests on China composite and manufacturing PMI data, final PMI prints across Europe and the US as well as the US ISM services index for July. BoJ minutes are the sole central bank release in G10 - however any further commentary from Fed officials will be carefully watched considering the focus on who could replace Fed's Kugler after her resignation over the weekend.

MNI OPTIONS: Expiries for Aug05 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1425(E1.6bln), $1.1450-56(E574mln), $1.1500(E1.4bln), $1.1550(E2.3bln), $1.1585-00(E3.2bln), $1.1650-60(E784mln)

- USD/JPY: Y146.00($611mln), Y147.45-53($630mln), Y148.00($558mln)

- GBP/USD: $1.3330-60(Gbp1.0bln), $1.3390(Gbp643mln)

- EUR/GBP: Gbp0.8650-70(E1.3bln)

- AUD/USD: $0.6465-80(A$1.2bln)

- USD/CAD: C$1.3850($601mln)

MNI US STOCKS: Late Equities Roundup: IT, Materials Sector Outperforms

- Stocks remain firm late Monday, at/near session highs as markets focus on dovish rate cut pricing and incoming earnings this week, instead of Friday's slowing labor market data. Currently, the DJIA trades up 500.46 points (1.15%) at 44089.01, S&P E-Minis up 80.75 points (1.29%) at 6345.25, Nasdaq up 365.9 points (1.8%) at 21016.17.

- Information Technology and Materials sector shares led gainers in the first half: IDEXX Laboratories surged +26.21% after revenue beat expectations. Meanwhile, materials stocks trade strong: Martin Marietta Materials +4.82%, Newmont Corp +4.07%, Eastman Chemical +3.27% and Vulcan Materials +2.75%.

- As did tech some shares: Monolithic Power Systems +5.68%, F5 Inc +4.58%, Super Micro Computer +4.20%, Palantir Technologies +3.95%, Advanced Micro Devices +3.49%. Other gainers include Williams-Sonoma +5.73%, PG&E Corp +5.35% and Ingersoll Rand +4.79%.

- Not all IT stocks gained Monday, as ON Semiconductor declined -13.36% following weak earnings. Elsewhere, Dexcom -3.52%, Berkshire Hathaway -3.39%, Church & Dwight Co -2.68%, Adobe -2.14%, Kraft Heinz -2.12%, Exxon Mobil -2.08%.

- After Monday’s close: Diamondback Energy, ONEOK Inc, Vertex Pharmaceuticals, Williams Cos, Voyager Technologies, Axon Enterprise Inc, BioMarin Pharmaceutical Inc, Hims & Hers Health, Palantir Technologies and Sterling Infrastructure.

- Early Tuesday announcements from: Pfizer, Apollo Global, Clear Channel Outdoor Holdings, Henry Schein, Archer-Daniels-Midland, DuPont de Nemours, Cummins Inc, Fidelity National Information, TransDigm Group, Molson Coors Beverage, Caterpillar, Marriott International, Duke Energy Corp and Lucid Group.

- Late Tuesday earnings announcements: Amgen Inc, Rivian Automotive, Arista Networks, Advanced Micro Devices, Match Group, Mosaic, Snap, International Flavors & Fragrances and Super Micro Computer.

MNI EQUITY TECHS: E-MINI S&P: (U5) Corrective Pullback Extends

- RES 4: 6523.63 1.764 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6500.00 Round number resistance

- RES 2: 6477.31 1.618 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6468.50 High Jul 31 and the bull trigger

- PRICE: 6350.50 @ 1255ET Aug 1

- SUP 1: 6264.25 Intraday low

- SUP 2: 6288.25 Low Jul 17

- SUP 3: 6241.00 Low Jul 16

- SUP 4: 6189.50 50-day EMA

The trend set-up in S&P E-Minis remains bullish and short-term weakness is considered corrective. Note that the contract has traded through support at the 20-day EMA, at 6336.64. The breach signals scope for a deeper retracement and opens the 50-day EMA at 6189.50. Clearance of this average is required to signal a stronger reversal. The primary trend remains up, key short-term resistance and the bull trigger is 6468.50, the Jul 31 high.

COMMODITIES

MNI AMERICAS OIL: WTI crude is lower on the day

August 4 - Americas End-of-Day Oil Summary: WTI crude is lower on the day, though has reversed steeper losses after Trump said he will be ‘substantially raising’ the tariff rate on India due to its purchases of Russian oil. Excess supply fears amid economic concerns and another widely expected OPEC+ output hike have weighed through the session.

- Fears of Russian supply disruption have been growing in recent weeks with threats to raise tariffs from both Trump and other key US officials.

- OPEC agreed to increase output by 547kb/d in September, above the 411k agreed for August to complete the unwinding of the 2023 voluntary-cuts. There is still another 1.66mb/d of reductions not due to be unwound until 2026 but OPEC says it is keeping its options open, according to Bloomberg.

- Goldman Sachs is not expecting any further OPEC production increases as the market is well supplied and has left its Q4 2025 Brent forecast at $64/bbl and 2026 at $56/bbl.

- WTI Sep futures were down 1.5% at $66.29

- WTI Oct futures were down 1.3% at $65.32

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 05/08/2025 | 0645/0845 | * | Industrial Production | |

| 05/08/2025 | 0700/0900 | ** | Industrial Production | |

| 05/08/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 05/08/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 05/08/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 05/08/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 05/08/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 05/08/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 05/08/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 05/08/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 05/08/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 05/08/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 05/08/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 05/08/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 05/08/2025 | 0900/1100 | ** | PPI | |

| 05/08/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 05/08/2025 | 1230/0830 | ** | Trade Balance | |

| 05/08/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 05/08/2025 | 1230/0830 | ** | Trade Balance | |

| 05/08/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 05/08/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 05/08/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 05/08/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 05/08/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 05/08/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 06/08/2025 | 2330/0830 | ** | average wages (p) |